ESG Framework Advisory in Australia

Table of Contents

- 01 Introduction to ESG Framework Advisory in Australia

- 02 ESG Governance Framework

- 03 Risk Management Alignment

- 04 Policy Development

- 05 KPI Dashboard Design

- 06 Stakeholder Reporting

- 07 Board-Level Governance

- 08 Compliance Monitoring

- 09 Annual Review Process

- 10 Challenges and Lessons Learned

- 11 Conclusion and Actionable Insights

01 Introduction to ESG Framework Advisory in Australia

A Paradigm Shift in Corporate Value

There has been a paradigm shift in how the world’s most sophisticated investors and regulators view the value of corporations. In the first half of the last century, the financial aspects of a business were used as the measure of a great business: revenue growth, profitability, and return on equity.

- Those metrics are still priceless, but they are no longer sufficient.

- Questions on environmental stewardship, social responsibility, and governance integrity now accompany serious investment theses, risk discussions in boardrooms, and regulatory filings.

- These are all the three pillars of ESG - and the emergence of a plausible ESG governance system has become one of the most effective strategic concerns of organisations of any size and sector.

Beyond Compliance — Building the Internal Architecture

ESG is not a compliance issue. Any organisation can prepare an ESG report. The harder and more valuable part is developing the internal architecture that enables ESG performance to be measurable, manageable, and improvable.

- This architecture consists of policies, a KPI dashboard, aligned risk management, board-level governance, and compliance monitoring systems.

- These systems have to convert intentions to actual outcomes.

- Not only do organisations that do this correctly survive regulatory and investor scrutiny, but they also build sustainable competitive advantage by dealing with risks that their less prepared counterparts have not recognised.

Who This Guide Is For

This article is aimed at practitioners joining the field of ESG advisory or broadening their knowledge base in accounting, finance, law, sustainability, or corporate strategy.

- It is structured in a logical order of the ESG framework development: policy development, risk management alignment, stakeholder reporting, annual review process, and governance structures.

- The goal is not just to deliver conceptual knowledge, but also the practical structures and terms to add value on day one in an actual ESG program.

- By the time you are done reading, you will have a working model of contributing to - and one day leading - ESG advisory engagements of real complexity and impact.

ESG is not a document; it is a system of operation. It is not the worthiness of its presence in a report, but rather its degree of integration into the organisation’s decision-making, risk management, and accountability systems. |

02 ESG Governance Framework

Why the Framework Is the Foundation

Any plausible ESG program is anchored in a sound, robust ESG governance structure. The structural architecture determines who is accountable to what, how decisions are made and the flow of accountability between the operational level and the board.

- The absence of this base will result in noise rather than signal, even with the most ambitious ESG goals and the most sophisticated KPI dashboard design.

- The ESG governance structure is the foundation on which all other elements are established.

- ESG is either embedded in the organisation or performative, depending on its quality.

The Three-Level Structure

The majority of ESG governance frameworks operate effectively across three levels, each with clear roles and accountability structures.

- Board level: Formal oversight accountability by a defined committee (usually the audit and risk committee or a distinct ESG committee) with clear terms of reference that encompass ESG oversight.

- Executive level: Accountability with a Chief Sustainability Officer, a sustainability-responsible CFO, or an executive ESG steering committee that owns the strategy and goals.

- Operational level: Data stewards, functional owners and working groups that gather data, performance management and initiatives.

- These three levels should be backed by open reporting, well-defined escalation procedures, and a regular flow of information to the board to ensure that the correct, decision-relevant ESG information is available to the board.

Real-World Case Study: Accountability Redesign

One of the most instructive case studies in governance redesign is a multinational consumer goods company that reorganised its ESG governance following investor criticism that it lacked accountability.

- Before the redesign, ESG roles were spread across six business functions, each with its own reporting lines, methodologies, and disclosure practices.

- This resulted in an internally inconsistent, difficult-to-audit ESG report that could not be compared year-on-year.

- The redesign also created a single ESG Management Office that reports directly to the CFO, centralised data-collection protocols, a centralised KPI dashboard, and quarterly reporting to a newly constituted Sustainability and Risk Committee of the board.

- ESG ratings improved significantly over two years, and the questions investors asked at the AGM shifted from the credibility of the disclosures to the content of the strategy.

- Lesson: the design of governance is not bureaucracy, but the precondition of credibility.

03Risk Management Alignment

ESG as a Lens, Not a Separate Risk Category

The greatest shift in ESG thinking of the past 10 years is the understanding that ESG is not a separate risk category, but a prism through which the traditional financial, operational, and strategic risks should be viewed.

- Risk management alignment refers to integrating ESG considerations into an existing enterprise risk management (ERM) framework.

- Climate risk, social licence risk, supply chain sustainability risk, and governance failures should be quantified, tracked, and mitigated, just as credit risk, market risk, and operational risk.

- This integration ensures that ESG risks are named, measured, and owned as part of the ERM structure, rather than treated as peripheral issues.

Starting with a Risk Register Mapping Exercise

Mapping is the crucial initial step towards aligning risk management and ESG. The existing risk register needs to be re-evaluated using an ESG lens to identify overlaps and gaps.

- Determine what ESG-specific factors are already implicitly addressed, e.g., regulatory risk, reputational risk, or supply chain risk.

- Determine their locations of absence - a manufacturing company might have a comprehensive operational risk model but no formal analysis of transition risk in its energy-intensive production processes.

- The financial services organisation may possess effective credit risk management without systematically evaluating its portfolio for physical climate risk.

- This mapping exercise frequently reveals content gaps that need to be addressed before SG risks can be properly incorporated into the ERM framework.

Bridging Technical ESG Analysis and Board-Level Discussion

There are significant implications of the risk management alignment process on the presentation of ESG risks to the board. Regular, structured reporting on climate risks and opportunities should be provided to boards under frameworks such as the TCFD (now embedded in AASB S2).

- Climate risk reporting should be part of the organisation's overall risk profile, rather than a standalone sustainability report.

- This necessitates that the risk function acquire new analytical capabilities: physical and transition risk modelling, financial scale of ESG exposures, and reporting findings in a manner meaningful to directors.

- A bridge between the technical and the strategic - the ability of an expert ESG adviser to translate complicated ESG analysis into the language of the boardroom is one of the most valuable things a skilled ESG adviser can offer.

04 Policy Development

Policies as the Operating Rules of the ESG Framework

The rules of operation for an ESG governance structure are policies. They define what the organisation undertakes, what is expected, what is acceptable practice, and the accountability mechanisms that enable compliance.

- Formulating a quality policy in the ESG field requires legality, strategy, pragmatism, and genuine aspiration.

- It is not as easy to create this combination as it may seem, and the distinction between organisations with mature ESG programs and those with superficial ones is not always clear.

- Policies should not be aspirational; they must include specific commitments, responsibilities, expectations, and consequences for non-compliance.

The Full Spectrum of ESG Policies Required

A complete ESG governance system needs a set of policies that covers the entire environmental, social, and governance spectrum – each addressing a different risk and responsibility.

- Environmental: Climate and Energy Policy, Environmental Management Policy, and, more recently,y a Nature and Biodiversity Policy, due to an increasing awareness of the financial risks associated with nature.

- Social: Human Rights and Modern Slavery Policy, Diversity, Equity and Inclusion Policy, Workplace Health and Safety Policy, and Community Engagement Policy.

- Governance: Code of Conduct, Anti-Bribery and Corruption Policy, Whistleblower Policy, and Tax Transparency Policy.

- All these documents must not only be aspirational but also contain commitments, roles, measurable expectations, and non-sequiturs. for non-compliance

How to Develop Policies That Change Behaviour

Policy development is a systematic process that should go far beyond drafting to produce policies that actually transform organisational behaviour.

- Start with a gap analysis against current external frameworks, including the UN Global Compact, OECD Guidelines on Multinational Enterprises,se or industry-specific standards.

- Process: Go through drafting, internal consultation, legal review, executive approval, board approval, and sharing with all interested parties.

- Policies drafted without consultation with operational teams or published without a similar training and communication program cannot bring about behaviour change.

- Policy development failure: policy-what the organisation does and policy-what the organisation does are not aligned; this is the most frequent failure in policy development and is increasingly detectable by regulators, auditors, and sophisticated investors.

05 KPI Dashboard Design

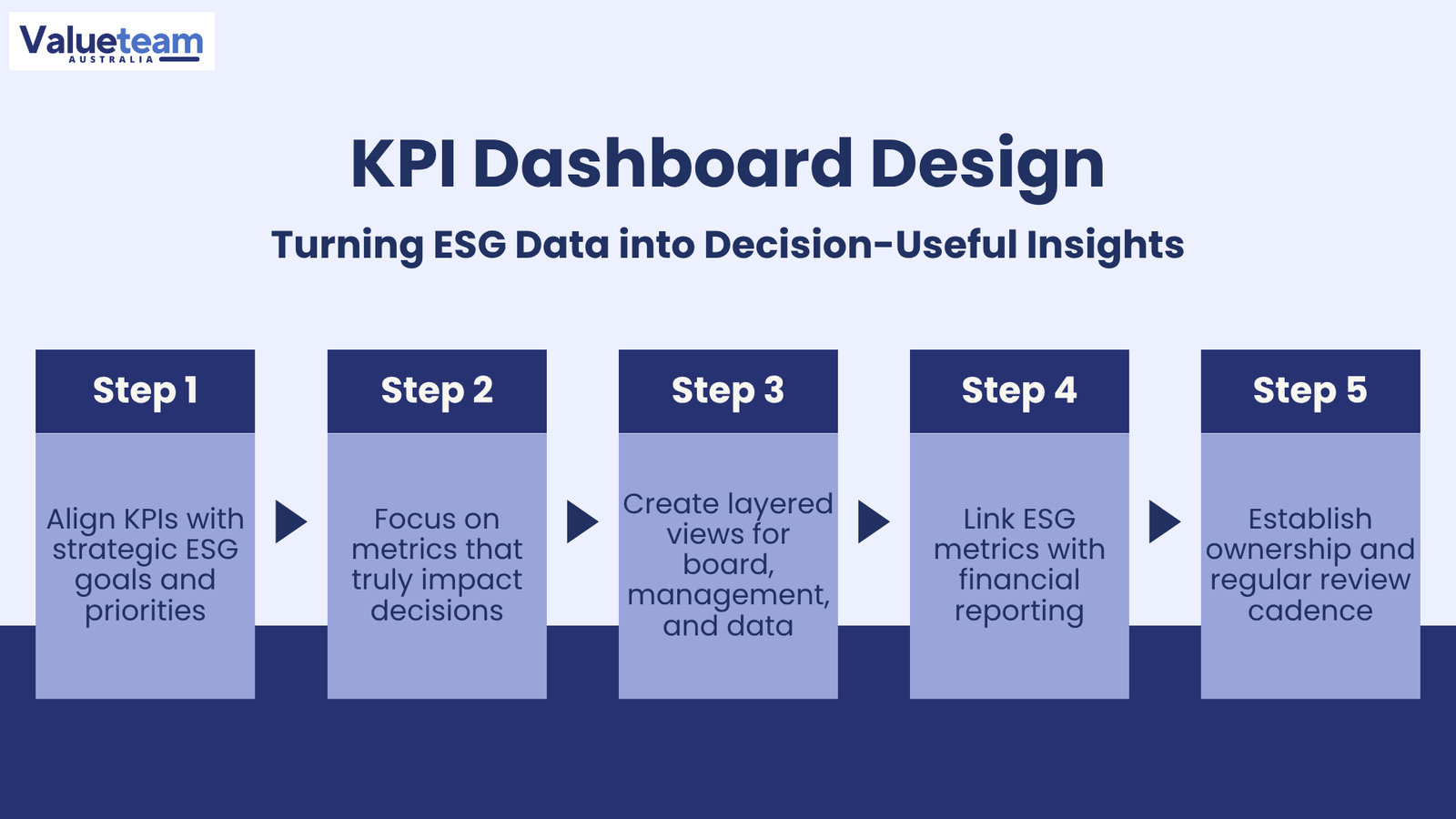

From Raw Data to Decision-Useful Intelligence

Data without a form of querying is simply numbers. A good KPI dashboard system will transform raw ESG data into a concise, consistent picture of the organisation’s performance against its promises.

- It allows management to recognise trends, highlight underperformance, allocate resources, and report credibly to the board and other external stakeholders.

- It is a strategic design exercise and, as such, a governance exercise as much as a technical one.

- The following five steps constitute the methodological process for creating this dashboard and achieving the most sustainable result.

Step 1 — Define Strategic ESG Objectives

Every indicator in a KPI dashboard plan should be linked to a strategic goal. The dashboard design team must be clear about what the organisation is attempting to achieve in all three E, S and G dimensions.

- Choose any metric only after interacting with the outcomes of the materiality assessment, ESG governance structure commitments, and board-approved targets.

- Determine the most important ESG objectives for the business model and for stakeholders.

- A dashboard built without this strategic anchor will yield metrics that never make a story.

Step 2 — Select Materiality-Driven KPIs

The temptation in KPI dashboard design is to measure everything. The science is to quantify what is important. The KPI chosen must be material – that is, the performance on it can reasonably affect the decision-making of investors, lenders, regulators, or other interested parties.

- Industry-specific standards such as the SASB sector standards, the GRI Universal Standards, and the TCFD recommendations provide systematic starting points for KPI selection.

- The chosen KPIs ought to be peer-benchmarkable and in line with the metrics the organisation has reported in its published sustainability report.

- Measures that are not tied to material risks create noise, but not a signal, and smart investors will see through the disconnection at first sight.

Step 3 — Build the Dashboard Architecture

A good KPI dashboard design is structured into multiple levels of granularity, each with a different audience and purpose.

- Board-facing executive summary: Displays the five to ten most important indicators in vivid red-amber-green status and trend lines.

- Operational management dashboard: More business-unit breakdown, allowing performance to be attributed and problems to be detected early.

- Data level: Templates of collection, calculation process, and audit trails, which are the basis of compliance monitoring and external assurance.

- The design should be suitable for every audience, not one undifferentiated data dump that suits no one.

Step 4 — Integrate with Financial Reporting

The most plausible KPI dashboard design is part of the organisation’s financial reporting cycle, not a parallel process.

- ESG measures in financial terms must be presented alongside their traditional financial counterparts, e.g., carbon cost exposure or the financial value of employee turnover.

- The ESG data collection schedule must align with financial close procedures, and sustainability disclosures can be discussed alongside financial statements.

- Control over ESG data should be comparable to control over financial data, particularly when the assurance requirements are more stringent.

- This integration is an indication to auditors, investors, and regulators that sustainability performance is being treated as much as financial performance.

Step 5 — Establish Governance and Review Cadence

A dashboard that lacks a governance cadence is not a management tool, but a document. The last step in KPI dashboard design is to establish the repetitive procedures of collecting, analysing, and taking action on data.

- Clarify who checks the dashboard, how often, and with what authority to instruct remediation, and how performance relative to KPIs is tied to executive responsibility.

- The standard cadence is monthly operational reviews, quarterly executive steering committee meetings and annual board-level reviews.

- The annual review process should also include a formal evaluation of the appropriateness of the KPIs themselves, as the organisation's strategy, stakeholder expectations, and regulatory environment change.

06 Stakeholder Reporting

The External Expression of ESG Governance

Stakeholder reporting is the external expression of an organisation’s ESG governance system – the mechanism through which internal commitments, information and performance are transformed into plausible external reporting that builds trust with investors, customers, employees, regulators and communities.

- Stakeholder reporting quality is emerging as one of the primary indicators by which external stakeholders assess the maturity of a particular organisation's ESG programme.

- The mismatch between aspirational stories and factual information is the surest indicator that the program is substantive or superficial.

- Stakeholder reporting of high quality is not only a compliance issue, but a competitive advantage.

Navigating the Reporting Framework Landscape

The landscape of stakeholder reporting models has taken on a much more structured shape over the past few years, with both compulsory and optional standards now overlaid.

- Australian entities with mandatory climate reporting, as required by AASB S2, have now standardised and prescribed the content and format of climate-related disclosures.

- Besides the required climate reporting, organisations are more likely to report under voluntary standards such as GRI, SASB, or the UN Sustainable Development Goals to provide a broader sustainability perspective.

- The stakeholder reporting art is to combine these different frameworks into a readable, coherent narrative that conveys the organisation's SG story without bombarding the reader with an undifferentiated torrent of data.

Case Study: A Three-Year Stakeholder Reporting Evolution

A European financial services group transformed its sustainability disclosures over three years, serving as an exemplar of how stakeholder reporting can be enhanced through a combination of purposeful and feedback-based approaches.

- Year 1: The report was mainly narrative, with qualitative descriptions of projects and minimal quantification.

- Year 2: Due to pressure on institutional investors, the organisation released a complete set of SASB-aligned metrics and its first limited-assurance statement on Scope 1 and 2 emissions.

- Year 3: The report included quantified outputs of a scenario analysis, a portfolio-level climate risk analysis, and a separately assured sustainability data appendix.

- The improvement of each year was supported by a particular stakeholder feedback loop: investor engagement, ratings agency questionnaires, and regulatory guidance.

- Lesson: stakeholder reporting should be viewed as a continuous improvement programme rather than an annual publication exercise.

Table 1: ESG Reporting Frameworks — Comparison for Practitioners

Framework | Primary Focus | Best Suited For | Relationship to Mandatory Reporting |

|---|---|---|---|

GRI Universal Standards | Extensive (systemic) sustainability effects (double materiality) | General sustainability disclosure: large organisations. | Voluntary; commonly referred to as compulsory climate standards. |

SASB Standards | ESG financially material measures that are industry-specific. | Disclosures that are of interest to investors; benchmarking in the sector. | Voluntary; in line with IFRS S1/ASB S1 concept of materiality. |

TCFD Recommendations | Financial risks and opportunities related to climate change. | Climate plan and risk reporting. | Part of AASB S2 / IFRS S2 – now all but mandatory for in-scope entities. |

AASB S2 / IFRS S2 | Climate-related financial disclosures | Compulsory for in-scope Australian entities. | Compulsory; lodging of ASIC. |

UN SDGs | Donation to development goals in the world. | Narrative congruence; community/social reporting. | Voluntary; can help to engage more stakeholders. |

07 Board-Level Governance

What Board-Level ESG Governance Actually Means

Board-level ESG governance does not consist solely of the right committee being in place. It is regarding the provision of the board, which is ultimately mandated with the long-term custodianship of the organisation, and the information, knowledge, and accountability lines it requires to perform its ESG oversight mandate.

- This is a greater level than most boards are attaining at the moment.

- One of the most effective changes an organisation can undertake is bridging the gap between its formal governance structure and its actual board-level ESG capability.

- Not only are documentation upgrades needed, but actual behavioural change at the board level is also needed.

The Information Dimension: What the Board Needs to See

The KPI dashboard and management reporting are related to the board’s oversight role, though the structure and content of such reporting should be tailored to the board audience.

- Directors need regular, systematic ESG reporting that is both granular enough to be useful for decision-making and compact enough to be readable, in addition to other oversight roles.

- Best practice: quarterly board ESG report of up to ten pages, structured around the material topics recognised during the materiality assessment.

- The report must contain clear performance against targets, trend analysis, and specific items to be decided or directed by the board.

- It should not be a passive reception of this report; it has to be reviewed and challenged, and this cannot be done without at least some directors who are actually ESG literate.

Building Expertise and Accountability on the Board

Both the expertise and accountability aspects of board-level ESG governance are rapidly changing due to investor pressure and shifting governance expectations.

- Investors and proxy advisers now specifically consider the presence of directors on boards with climate or sustainability expertise, determined in the same way as financial expertise.

- Possible solutions for organisations with a capability gap include targeted director training, appointing a director with an ESG qualification, or appointing a senior independent ESG adviser to assist the board's ESG committee.

- The accountability frontier: organisations that explicitly integrate ESG outcomes into the performance regime of directors are in the minority, though this is rapidly changing as institutional investors make it an explicit voting criterion.

08 Compliance Monitoring

The Discipline That Keeps the Framework Honest

The continued discipline that ensures that an ESG governance framework is honest is the effectiveness of compliance monitoring. In its absence, policies are dreamy and impractical, goals are not accountable, and the gap between promises and reality widens.

- Poor compliance monitoring poses regulatory risks and reputational exposure that may compound over time.

- Effective compliance monitoring does not wait until annual reporting cycles to identify problems - it provides mechanisms to be in place that identify problems early.

- Early identification enables problems to be addressed before they become material disclosures or regulatory compliance failures.

The Architecture of an Effective Compliance Monitoring System

A good compliance monitoring framework shares many similarities with the internal control framework applied in financial reporting, modified to the ESG setting.

- Transaction level: Automated data quality controls detect anomalies in ESG data entering the KPI dashboard, including odd spikes in energy consumption, disruptions in supplier questionnaire responses, or discrepancies between operational data and reported emissions.

- Process level: Internal audit of the controls and methodologies of ESG data collection and calculation regularly.

- Governance level: Reporting on compliance status, breaches found, remediation actions, and new areas of regulatory risk to the audit committee or ESG committee regularly.

Tracking the Evolving Regulatory Horizon

Monitoring compliance in the ESG context needs to be in line with an ever-evolving external regulatory environment – one that is rapidly increasing in scope and specificity to Australian organisations.

- Current demands include climate performance reporting under AASB S2, modern slavery reporting under the Modern Slavery Act, and new nature-related reporting frameworks.

- An ESG advisor or internal ESG department should have a current regulatory horizon scan: what is needed soon, how it affects the organisation, and how to build the capacity to meet it before the deadlines elapse.

- Organisations that actively engage in compliance monitoring by building capacity in advance always find the transition to regulation easier and less costly than those that respond to a compliance crisis.

Table 2: ESG Compliance Monitoring — Key Obligations for Australian Entities

Obligation | Governing Framework | Applies To | Key Monitoring Focus |

|---|---|---|---|

Climate-related financial disclosures | AASB S2 / Corporations Act. | In-scope listed and unlisted (phased) | Scope 1, 2 & 3 emissions; governance; scenario analysis; targets. |

Modern Slavery Reporting | Modern Slavery Act 2018 | Entities with >$100M annual revenue | Due diligence of the supply chain, identification of risks, and remediation measures. |

Corporate Governance Disclosures | Principles of ASX Corporate Governance. | Listed entities | Board composition; ESG oversight; remuneration linkage |

Environmental Licensing | State/Territory Environmental Laws | Operations with environmental footprint | License terms; limit of emissions; reporting of incidents. |

Gender Equality Reporting | The Equality Act in the Workplace on Gender. | Employers (private sector) having 100 or more employees. | Gender pay gap, representation at leadership levels, and policies |

09 Annual Review Process

Why the Framework Must Evolve Every Year

A single-designed ESG governance structure is not a structure, but a snapshot. The context under which organisations work is dynamic: regulatory requirements vary, investor expectations vary and the strategy of the organisation, as well as its stakeholder relations, change with time.

- The annual review process is the formalised process through which the framework is kept up to date, relevant and functional.

- It is among the most operationally important processes of the entire ESG program.

- Without this discipline, even the most well-thought-out frameworks will become disconnected from the realities they are expected to deal with.

Four Dimensions of the Annual Review

The four main dimensions are covered in a comprehensive annual review process that deals with another aspect of the continued effectiveness and relevance of the framework.

- Performance assessment: A methodical review of the performance of the organisation in relation to all its ESG targets and commitments during the year in comparison to the previous year, sector benchmarks and peer group information. This is directly linked to the stakeholder reporting cycle.

- Materiality refresh: The reevaluation of the most topical ESG issues of the organisation by engaging stakeholders and conducting environmental scanning, to identify whether the priorities of disclosure are still set accordingly.

- Framework and policy review: A logical assessment of whether the output of policy development, the structure of governance, the process of compliance monitoring, and the design of KPI dashboards are still fit to purpose based on the experience of the last year and the development of best practices.

- Setting or revising specific, measurable ESG commitments over the next year - ambitious enough to indicate a serious purpose, realistic enough to be attained with plausible effort, and tied to the business strategy.

The End Product: Board-Approved ESG Plan

The end product of the annual review process is a tangible product that completes the circle between performance evaluation and future commitment and offers a clear and responsible record of governance.

- The final output is an ESG plan that is approved by the board and is disclosed to different stakeholders as a component of the overall reporting process.

- This plan forms the foundation of the disclosures in the annual sustainability or integrated report.

- It sends a message to investors, employees, and regulators that ESG is an ongoing improvement practice, rather than a periodic compliance activity.

Table 3: Annual ESG Review — Process Flow

Phase | Key Activities | Responsible Party | Output |

|---|---|---|---|

1. Performance Data Collection | Combine all-year-round ESG data in all metrics in the KPI dashboard. | ESG Data Team + Finance. | Complete annual confirmed ESG information. |

2. Performance Assessment | Compare results with targets; find underlying causes of differences; compare with peers. | ESG Lead + Analytics | Performance assessment report |

3. Materiality Refresh | Carry out stakeholder engagement and revise the materiality matrix for use in the next year. | ESG Lead + External Adviser. | Refreshed materiality matrix |

4. Framework and Policy Review | Evaluate policies, governance frameworks, and KPIs and maintain relevance. | ESG Steering Committee | Register of policy update; policy governance memo. |

5. Regulatory Horizon Scan | Determine new and emerging ESG requirements; evaluate applicability and preparedness. | Legal / Compliance + ESG | Regulatory Horizon Report |

6. Target Setting | Prepare ESG targets to be met next year and align them with business planning. | CFO / ESG Lead | Rough draft targets to be reviewed by the executive. |

7. Executive Review | The steering committee evaluates performance, updates the framework and suggests targets. | ESG Steering Committee | Endorsed ESG plan |

8. Board Approval | Reviews, challenges, and formally endorses the board’s annual ESG plan and targets. | Board / ESG Committee | The ESG plan is to be publicly disclosed and approved by the board. |

Table 4: ESG Framework Build — End-to-End Implementation Process Flow

Stage | Activity | Participants | Key Deliverable |

|---|---|---|---|

1. Diagnostic | Determine the level of ESG maturity and identify gaps relative to peer practices and other regulatory demands. | ESG Adviser + Leadership Team. | Maturity assessment report ESG. |

2. Materiality Assessment | Determine and rank material ESG issues by engaging with stakeholders and analysing financial data. | ESG Adviser + Stakeholders | Priority topic register and materiality matrix. |

3. Framework Design | Governance structure, roles, accountabilities and reporting architecture of design ESG. | ESG Adviser + Board + Exec | ESG Governance Department document. |

4. Policy Development | Develop, discuss, and finalise fundamental ESG policies for E, S, and G. | Legal + ESG + HR + Operations | Accepted ESG policy portfolio. |

5. KPI Design | Choose the material KPIs; create data collection templates and the dashboard structure. | ESG Analyst + Finance + IT. | KPI framework and dashboard. |

6. Data Infrastructure | Construct or implement data management systems; establish controls and audit trails. | IT + Finance + ESG | ESG data platform: a guide on a methodology. |

7. Reporting Framework | Develop a design stakeholder report framework and align it with external frameworks. | ESG Leader + Comms + Finance. | Framework of reporting; draft first disclosure. |

8. Assurance and Lodgement | Engage assurance provider; finalise disclosures; lodge with ASIC where required | CFO + Auditor + Legal | Guaranteed sustainability report; lodgement to ASIC. |

10 Challenges and Lessons Learned

Challenge 1 — The Data Problem

The largest long-term issue in the implementation of the ESG governance framework is the data issue. ESG data is harder to collect, certify and verify, as compared to financial data.

- ESG information is distributed among systems that were not designed to produce it, and collected by teams that do not receive data governance training.

- It is also subject to methodological choices that can affect comparability in a manner that is not necessarily transparent.

- The organisations that do this correctly consider KPI dashboard design and data infrastructure to be a capital investment, not an operating cost and invest the budget and human expertise to create the right systems instead of using spreadsheets and manual processes.

- Lesson learned: get the infrastructure ready before you make the commitment, and not after.

Challenge 2 — Organisational Buy-In

The second important challenge is organisational buy-in. The perception of an ESG governance framework as a compliance burden created by a central team will never be deeply embedded within the organisation.

- The best programs are those in which the leaders of business units realise that ESG management is in their best interests - reducing regulatory risk, assisting them in retaining talent, protecting the social licence, and affecting customer buying behaviour.

- The development of such understanding needs to be a deliberate internal dialogue, executive sponsorship and the rigour of connecting ESG outcomes with already appreciated business leader metrics.

- When the head of procurement realises that compliance in the supply chain helps the business to avoid exposure to the Modern Slavery Act and supply disruption, he/she will become an ally and not a resister.

Challenge 3 — Credibility Under Scrutiny

The third issue is credibility. As ESG reporting is now mandatory and audited by an independent body, the gap between what organisations declare and what they can prove is becoming more and more expensive, both reputational and legal.

- Conservative claims, which can be fully justified, are better than ambitious claims that cannot be demonstrated.

- Investors and directors are increasingly becoming more adept consumers of sustainability disclosures - trying to conceal bad performance by making imprecise statements, disclosures that are selective or misleading in terms of metrics are becoming harder to maintain.

- Organisations that have credible, sustainable ESG reporting are honest in their reporting - even of their failures - and demonstrate year-on-year progress based on real changes in their activities.

The ASIC lodgement and assurance procedure is changing the competitive environment of the professional services market, providing real career prospects to early-investing practitioners.

- The ability to assure sustainability is emerging as a major investment for audit firms, the Big Four and specialist sustainability consultancies.

- Sustainability reporting professionals who are aware of sustainability reporting standards and the process of assurance are in demand - and this set of skills is not yet well supplied.

- Early investment in learning about the ASIC lodgement and assurance processes is not only professionally helpful but also a smart career move.

11 Conclusion and Actionable Insights

Why the ESG Framework Matters

One of the most strategically significant changes that organisations can make in the present environment is to transform an informal group of sustainability practices into a fully functioning ESG governance system.

- The components, including risk management alignment, policy development, KPI dashboard design, stakeholder reporting, board-level governance, compliance monitoring, and annual review process, are a system that relies on each other.

- The quality of the system as a whole is defined by the quality of each component.

- Practitioners who comprehend the integration of these components and are able to apply them with rigour and practical intelligence are the most sought-after in the market today.

Five Actionable Steps for Professionals

- Step 1: Get acquainted with the key ESG reporting frameworks: GRI, SASB, TCFD, AASB S2, and UN SDGs. Know not only what they require, but why they are made thus. Everything that follows is based on the conceptual logic of each.

- Step 2 - Learn how to design KPI dashboards: learn what is material about a metric, how metrics are chosen and justified, and how to structure dashboard architecture that is useful to different audiences. This is among the most transferable skills in ESG advisory in a practical manner.

- Step 3 - Invest in risk management alignment knowledge: the reflection and integration of ESG risks with traditional enterprise risk frameworks. With the growing level of corporate scrutiny, those practitioners who understand ESG and ERM are priceless.

- Step 4 — Develop a deep appreciation of compliance monitoring issues in the Australian context: the minimum requirements include the Modern Slavery Act, the Workplace Gender Equality Act, AASB S2, and ASX Corporate Governance requirements, but the regulatory landscape is evolving.

- Step 5: Every engagement is a learning experience: note how organisations learn with their performance data, how they engage with stakeholders, and how they apply that learning to make better targets and stronger structures every year.

The five steps presented below give a tangible development trajectory of junior to mid-level professionals developing expertise in ESG advisory.

The individuals who will be the makers of the future of ESG advisory are the ones who could create the systems, question the assumptions, and hold organisations to the promises they make. ESG is never a destination, but a discipline of continuous improvement, which is rewarded by rigour, honesty, and sincerity. |

ESG is not a destination. It is a continuous improvement field – a field that rewards organisations and professionals who take it seriously, as opposed to acting as performers.