ESOP Valuation Services in Australia

Table of Contents

- 01 Introduction

- 02 What Is Intangible Asset Valuation?

- 03 Why Do Clients Need ESOP Valuation?

- 04 Key Inputs Required for ESOP Valuation

- 05 Common Valuation Methodologies

- 06 Key Value Drivers — What Increases or Reduces ESOP Value

- 07 Common Mistakes Before a Valuation

- 08 Five Key Steps: Information and Engagement Process

- 09 Our Valuation Process

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is ESOP Valuation?

- 03 Why Do Clients Need ESOP Valuation Services in Australia?

- 04 Key Inputs Required for ESOP Valuation

- 05 Common Valuation Methodologies

- 06 Key Value Drivers — What Increases or Reduces ESOP Value

- 07 Common Mistakes Before a Valuation

- 08 Five Key Steps: Information and Engagement Process

- 09 Our Valuation Process

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

The Role of ESOPs in Business

Employee Share Option Plans (ESOPs) are commonly used by companies to attract, retain and incentivise employees, management and other stakeholders. The capacity to provide significant equity participation – a stake in the future value of the business – is one of the most valuable tools founders, boards, and human resource managers can use in a very competitive employment environment.

- For early-stage companies that cannot compete with the compensation packages offered by listed companies, equity compensation is often the only mechanism to attract the talent required to implement a growth strategy.

- In established firms, carefully crafted share option plans are an effective means of ensuring that management incentives are aligned with the creation of shareholder value in a way that cash compensation cannot.

The AASB 2 Requirement

The value of share options and other equity-based incentive plans is often independently valued to ensure they are appropriately reported, taxed, and used to fairly compensate employees. The Australian Accounting Standard on share-based payments (AASB 2) requires companies that issue options, rights or other equity instruments to their employees to recognise a share-based payment cost at the fair value of the instruments at the grant date.

- This applies regardless of whether the entity is listed, its size, or its revenue.

- The share-based payment expense is recognised in the income statement, affecting the reported profit and loss - so the quality of the underlying valuation has a direct impact on the financial statements.

Why This Guide Matters

ESOP valuation is one of the technically least understood areas of the audit for growing companies facing their first external audit, and there is often a significant difference between management’s assumptions and the professional opinion of an external auditor. For mature companies, the annuality of the grant cycle means that ESOP valuation is a formal, annual exercise involving the finance, human resources, audit and tax advisory teams.

- In both cases, it's important to understand how the valuation is calculated, what data is needed, what model is most appropriate, and how the results are applied.

- ESOP valuation is not a "side show" - it is a financially material measure reported in the income statement, and that affects audit reports, tax liabilities, and investors' views of pay practices.

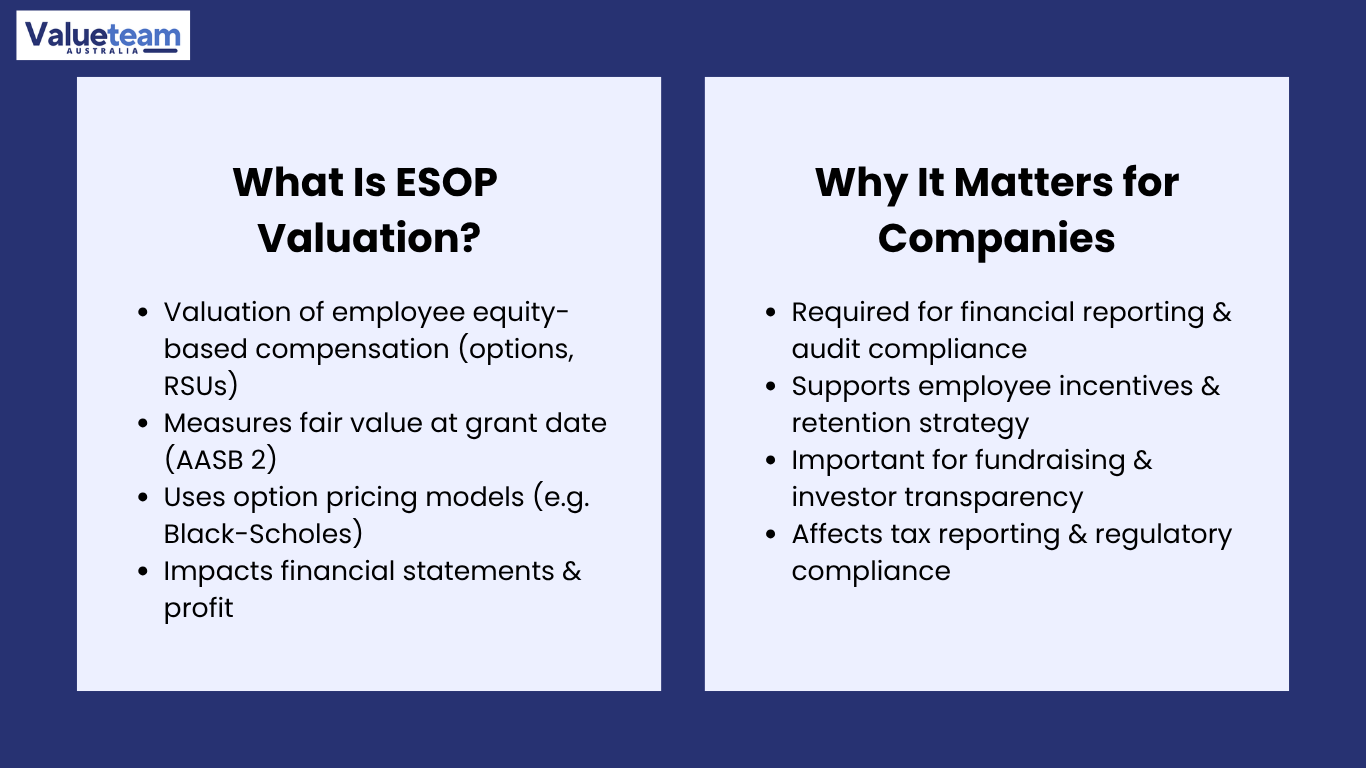

02 What Is ESOP Valuation?

Definition and Scope

ESOP valuation is the independent valuation of the fair value of employee stock options, share appreciation rights, restricted stock units and other equity-based compensation. ESOP valuation is not a business valuation (which measures enterprise value), but rather the valuation of the derivative instruments that give employees exposure to equity value.

- The right to buy shares at a specified exercise price over a period of time.

- Rights to acquire shares if certain performance criteria are met.

- Units that convert to shares after a vesting period.

- Each instrument has its own economic characteristics, option-pricing model assumptions, and accounting treatment under AASB 2.

The Range of Instruments Covered

ESOP valuations cover more than just employee stock options. Equity compensation plans cover a wide variety of instruments.

- Employee stock options: the right to buy shares at a fixed exercise price - the most frequent type, which allows employees to participate in upside potential without having to pay for it.

- Share warrants: equivalent to options but usually issued in different forms.

- Management incentive plans: a combination of options and performance targets (revenue, EBITDA or total shareholder return).

- Phantom stock plans: cash equivalent of a share of stock, determined by reference to the value of the company on a specified date.

- Restricted share units (RSUs): no exercise price; vest and convert to shares upon satisfying time or performance conditions.

- Performance share awards vest only upon achieving certain performance targets, requiring the application of probability weighting.

The Range of Instruments Covered

When to measure is critical to the correct application of AASB 2 and is the key driver of the ongoing accounting for each plan type.

- Equity-settled plans: fair value at grant date is measured and amortised over the vesting period - no remeasurement is needed as the share price fluctuates after the grant.

- Cash-settled plans and liability-type awards: the fair value must be remeasured at each reporting date until settlement, creating an ongoing measurement obligation.

- Knowing the difference between equity-settled and cash-settled accounting treatment, and the measurement requirements that result, is one of the technical skills required.

03Why Do Clients Need ESOP Valuation Services in Australia?

The need for professional ESOP valuation arises regularly in a variety of situations. They occur throughout the commercial life of a business – from the first option grant for a startup through to the annual review of an LTIP for a listed company – and are driven by the interaction of tax law, accounting standards, audit practice and commercial considerations about remuneration and retention of employees.

Financial Reporting

The main driver of demand for ESOP valuations is the accounting for share-based payments (SBP) under AASB 2. Each time an equity-linked compensation instrument is granted to an employee, director or service provider, the entity granting the instrument must recognise an expense over the vesting period equal to the fair value of the instruments granted.

- For non-listed entities, this involves an independent valuation process: a business valuation to determine the equity value, followed by selection and input of an option pricing model.

- Disclosures under AASB 2 require disclosure of inputs, weighted average exercise prices, number of options outstanding, and share-based payment expense for the period. This recurring disclosure requirement relies on quality valuations.

- ESOP valuations are in high demand for the 31 December and 30 June year-end reporting periods, as audit programs require valuations to be completed before share-based payment disclosures can be audited.

Employee Compensation and Incentive Planning

The accounting requirement aside, the valuation of an ESOP has commercial utility in employee retention and management compensation.

- An independently determined fair value provides a credible, objective assessment of the economic value of the equity compensation being offered to the employee (and transparency that well-informed candidates, especially senior ones, increasingly seek).

- For performance-based awards, where vesting is contingent on achieving certain financial or operational milestones, the valuation needs to incorporate the likelihood of achieving those milestones, adding to the complexity that must be carefully considered.

- In the case of equity awards to startups, where the value proposition is a large upside in the upside scenario, the valuation must consider current economic value, the option value of potential growth, capital structure features, liquidation preferences, and exit scenarios.

Fundraising, Investor Reporting and Tax

ESOP valuation touches capital raising, investor reporting, and tax in several ways throughout the life of a business.

- Investor due diligence on any capital raise invariably considers the ESOP and cap table - not just to understand the current equity structure, but to determine the impact of unvested and outstanding options on post-money dilution.

- An ESOP valuation that is well documented and demonstrates a professional approach to valuation, audit, and reporting is a signal to investors of a company's financial maturity.

- Employee option exercises have income tax and payroll tax implications, depending on the value of the shares at the time of exercise, again requiring a defensible valuation methodology.

- Ongoing reporting to the ATO and ASIC, and employee tax reporting support, relies on proper valuation documentation.

04 Key Inputs Required for ESOP Valuation

Understanding the Inputs That Drive Fair Value

The fair value of an equity-based award depends on a set of technical inputs that define the instrument’s economics and its environment. It is important for anyone commissioning, reviewing or auditing an ESOP valuation to understand these inputs, what they are, how they are set and how sensitive the valuation is to changes in each. These assumptions determine the final fair value, and a change in any one can have a material impact.

Understanding the Inputs That Drive Fair Value

Customer relationship valuations reflect the value of an entity’s existing customer relationships – the expectation that they will remain and transact, and the revenue stream that will result from their continued patronage.

Core Pricing Inputs

The following inputs serve as the quantitative basis for the valuation that feeds into the option pricing model.

- Share price/equity value: the current price of the share that the option holder can acquire. For listed companies, this is the market price at the date of grant; for unlisted companies, this requires a separate valuation of the equity, which must be documented and justified.

- Exercise price: the price at which the option holder can purchase the share - this is usually set at or above the current share price to offer a performance challenge. The difference between the share price and the exercise price (the "moneyness" of the option) is a key factor in determining fair value.

- Vesting period: the length of service (and for performance-vesting awards, the period to achieve performance targets) before the option vests. The longer the vesting period, the lower the fair value, as the risk that the conditions will not be met rises.

Market and Behavioural Assumptions

Along with plan-specific inputs, a series of market and behavioural assumptions must be estimated, benchmarked and documented.

- Volatility: the most critical and difficult assumption, especially for unlisted businesses. This increases the value of the option by increasing the likelihood that the share price will be well above the exercise price at maturity. Listed companies are used as proxies for unlisted businesses, adjusted for the target's risk.

- Risk-free interest rate: based on the yield of Australian government bonds with maturity equal to the expected option life.

- Dividend yield: decreases option value, as share price declines on the ex-dividend date - options not receiving dividends. Important for companies with dividend payments.

- Expected forfeiture rate: the proportion of options that will be forfeited due to employee turnover before vesting. Lowers the expected number of instruments that will vest and, as a result,t the accounting expense.

- Early exercise expectations reflect empirical evidence that employees tend to exercise their options before they expire, which affects the option's life and, in turn, its fair value calculated under the pricing model.

Table 1: ESOP Value Drivers — Impact and Sensitivity

Input / Driver | Direction of Impact on Fair Value | Typical Range / Benchmark | Key Sensitivity Note |

|---|---|---|---|

Current share price (equity value) | Higher price → higher value | Valued by their most recent funding round or an independent valuation. | Most directly observable input; unlisted companies need a separate equity valuation. |

Exercise price | Higher exercise price → lower value | Customarily determined at or higher than the grant price. | Out-of-the-money options could be low-fair-valued yet remain incentive-effective. |

Expected volatility | Higher volatility → higher value | Unlisted: 30%–80%+ depending on sector; benchmarked to listed comparables. | Single most sensitive assumption; must be well substantiated using comparable data. |

Option life / contractual term | Longer life → higher value | Typically, 3–10 years for employee options. | Early exercise assumptions shorten the effective life below the contractual maximum. |

Vesting period | Longer vesting → marginally lower per-period value | Typically 1–4 years with a cliff or pro rata vesting. | Impacts the timing of expense recognition; may not affect grant-date fair value. |

Risk-free rate | Higher rate → slightly higher value (call options) | Australian government bonds with maturity matching the expected option life. | More material than in low-rate environments; must be contemporary. |

Dividend yield | Higher yield → lower value | None for most pre-IPO companies; market rate for listed entities. | Modifies share price growth; critical for dividend-paying companies. |

Expected forfeiture rate | Higher forfeiture → lower expense (not fair value) | Based on historical turnover data, typically 5%–20% p.a. | Modifies the number of instruments, not fair value per instrument under AASB 2. |

05Common Valuation Methodologies

Selecting the Right Option Pricing Model

The choice of the option pricing model is one of the key professional judgements in valuing an ESOP. Models vary in their assumptions about the behaviour of share prices, the ability to exercise the option early and the structure of any performance conditions. Using the wrong model can lead to technically flawed and un-auditable results.

Black-Scholes Option Pricing Model

The Black-Scholes Option Pricing Model is the most common method for valuing plain-vanilla employee stock options. It was developed in 1973 and offers an analytical formula for valuing European-style options (exercisable only at expiry), with a single, accurate, fair value derived from a set of defined inputs.

- Inputs: stock price, exercise price, risk-free rate, expected volatility, time to expiry, dividend yield.

- Appropriate for typical employee options with straightforward exercise conditions, no market-based performance conditions, and little early exercise.

- Not suited to: exercise only at expiry (most employee options have American-style rights); early exercise, non-market performance conditions, or complex vesting structures; or to model multiple scenarios for fair value.

- Black-Scholes is the most efficient and suitable model when vesting occurs on a single date, and employment is the only condition. Binomial or Monte Carlo should be used for complex structures.

Binomial / Trinomial Tree Model

The Binomial / Trinomial Tree Model overcomes most of the limitations of the Black-Scholes model by assuming that share prices follow a discrete-time lattice – a tree of possible share price paths over the life of the option, with probabilities attached to each branch.

- The discrete-time nature of the tree makes this model ideal for plans with expected early exercise, multiple vesting conditions, performance hurdles and explicit employee behaviour assumptions, such as the inclination to exercise when the share price reaches a certain multiple of the exercise price.

- Allows the valuer to specify early exercise rules at each node, resulting in a fair value that accounts for the American-style feature of most employee options.

- Recommended for complex plans such as management options with non-market performance hurdles, and options with market-based performance hurdles and service conditions.

- The trinomial version includes an additional branch (no change in share price) at each node for greater accuracy, especially for short time steps or long-term options.

- The difficulty lies in the choice and justification of assumptions about behaviour (particularly the early exercise multiple and the suboptimal exercise factor), which require empirical support and expert judgement for calibration.

Monte Carlo Simulation

Monte Carlo Simulation is the most versatile and complex of the three methods. It works by running thousands of possible share price scenarios under given assumptions and then averaging the payoffs across all scenarios to calculate fair value.

- Best suited to instruments with value dependent on market performance conditions, which cannot be solved analytically or modelled in a simple lattice - most typically TSR-based awards where vesting is dependent on total shareholder return compared to a peer group or index.

- Models market performance conditions where the share price must reach a certain level over an averaging period (which would be difficult to model in a binomial tree).

- Supports multiple exit and capital structure scenarios in a simulation framework, unmatched by other methods.

06 Key Value Drivers — What Increases or Reduces ESOP Value

How the Inputs Drive the Output

Fair value of an employee option or equity-linked award is a function of a series of measurable factors that may not behave intuitively. Finance, HR and boards need to understand these factors – and the impact of changes in each factor – when setting prices, designing vesting schedules and forecasting expenses.

Factors That Increase ESOP Fair Value

All plans are most sensitive to expected volatility. Several other factors generally increase the fair value of employee options.

- Increased expected volatility increases the likelihood that the share price will rise well above the exercise price by the maturity date. Young, high-growth firms - which typically have higher implied volatility than established firms - often have higher per-option fair values, even with identical exercise prices and maturity dates.

- Lower exercise price (in-the-money options): increases the option's fair value, as the option holder already has an intrinsic gain. The most common design is at-the-money options (with an exercise price equal to the current share price), as this guarantees the employee will benefit only if the share price appreciates.

- A longer option life / contractual term allows more time for the share price to rise above the exercise price, thereby increasing the option's time value.

- Higher share price/equity value: the most visible factor; all other things being equal, the higher the price, the higher the option's value.

Factors That Reduce ESOP Fair Value

The fair value reducing factors are also informative for plan designers, as they affect the economics of the incentive and the cost to be recognised for accounting purposes.

- Short vesting period: reduces the time value of the option by shortening the time available for the price to appreciate, thereby reducing the fair value at grant.

- High strike price (out-of-the-money options): decreases the likelihood that the option will be in the money and decreases the expected payoff. A useful tool for setting a higher performance hurdle and lowering up-front accounting cost, out-of-the-money options risk becoming permanently out-of-the-money, thus losing their incentive effect.

- Low expected volatility: reduces upside potential; a real limit to per-option fair value for mature companies.

- High expected forfeiture rates: reduce the probability-weighted number of instruments expected to vest (and hence the total accounting cost to be recognised) - an important consideration for firms with high turnover.

- Highly restrictive non-market performance conditions: reduce the expected (probability-weighted) number of instruments to vest. Under AASB 2, there are different rules for market and non-market conditions - market conditions are incorporated in the fair value at grant-date; non-market conditions affect the estimated number of instruments recognised, not the fair value per instrument.

07Common Mistakes Before a Valuation

Why Preparation Failures Are So Costly

The most common preparation mistakes that cause delays or deficiencies in ESOP valuations, according to our experience, are remarkably similar across companies and ESOP designs. They are also largely avoidable if the company’s finance and legal teams are aware of what is needed and put together a full and accurate documentation package in advance of the engagement. Good preparation increases audit readiness and the likelihood of avoiding last-minute valuation changes that delay the audit and require accounting adjustments to the financial statements.

Incomplete ESOP Documentation — The Most Common Failure

The most prevalent failure in preparation is incomplete ESOP documentation. Plans drafted and developed without written documentation, or whose rules are out of date and do not reflect the actual terms under which options have been granted, can create confusion about the rights and responsibilities of the company and the option holders.

- The absence of grant letters confirming the terms of each employee's option grant (number of options, exercise price, vesting schedule, performance conditions) is another common issue encountered in our first-time ESOP valuations.

- In the absence of grant letters, the valuation adviser cannot verify the terms being valued, and the auditor cannot reconcile the options reported to the grant letters.

Other Common Preparation Issues

In addition to missing documents, there are common technical issues that occur in ESOP valuations and are avoidable with adequate preparation.

- Stale cap table: failure to reflect all outstanding instruments leads to incorrect equity allocation and an inaccurate share price input.

- Wrong vesting assumptions: using assumptions inconsistent with the plan's terms can affect both fair value and the expense recognition profile.

- Excessive volatility assumption: applying a volatility measure inconsistent with the company's risk profile or failing to document it is a common audit issue.

- Consistently low expected option life: failing to account for employees' historical exercise patterns (which are often much earlier than the contractual term) and using Black-Scholes for plans where early exercise is well documented can impact both fair value and expense recognition profile.

- Clients who provide an accurate information package to an ESOP valuation engagement receive faster, more efficient, and defensible valuations.

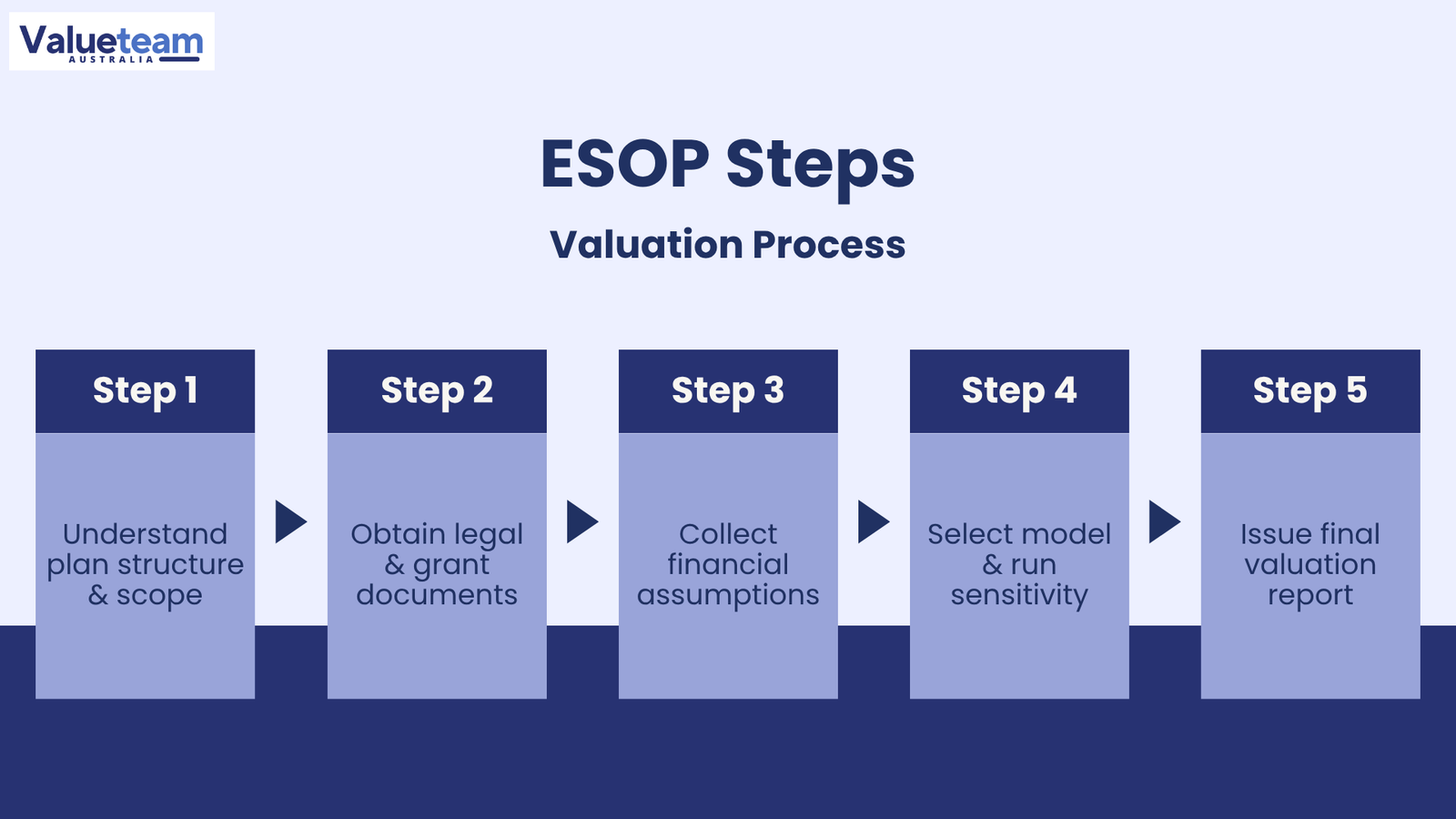

08 Five Key Steps: Information and Engagement Process

The ESOP valuation engagement process can be broken down into five steps, from plan understanding to report delivery. These steps are interrelated, and the output of each step is only as good as the inputs. This process helps companies prepare, allows finance to plan audit support timeframes, and helps practitioners plan their engagements down to the day.

Step 1 — Understand Plan Structure and Scope

The first step in the engagement is to understand the plan design before requesting any documents or choosing a model. This includes the type of instrument granted (employee stock options, RSUs, phantom stock, performance rights, or a combination), the number of participants, the date(s) of the grant, the number of shares granted, and the terms and conditions of the grant.

- In the case of companies with multiple grant dates and/or multiple plan types, or both equity-settled and cash-settled instruments, this scoping exercise needs to be carefully mapped to ensure the instruments are all included and receive the correct accounting treatment under AASB 2.

- Result: a clearly defined scope of engagement that defines what is being valued, for what purpose, as at what date, and in accordance with what accounting and regulatory requirements.

Step 2 — Obtain Legal and Grant Documentation

In the second step, we obtain the legal and grant documents that establish the facts used in the valuation.

- ESOP scheme documents: plan rules, trust deed (if the scheme is structured as a trust), and any amendments to the plan.

- Grant letters: detailing the option terms for each participant or class of participants.

- Shareholder agreement: especially the provisions relating to option holders' rights in the event of an exit, a change of control, or a winding up.

- Any shortfalls in documentation should be remedied at this point - not during the audit.

Step 3 — Collect Financial Assumptions

Once the legal framework has been established, the engagement shifts to collecting the quantitative inputs for the option pricing model.

- The current share price is the most important input for unlisted companies. An independent equity valuation must be performed and documented before the option pricing model is set up.

- The cap table must be up-to-date and complete (including ordinary shares, preference shares, convertible instruments, and outstanding options) to ensure that the total equity value is appropriately distributed across the instruments in the capital structure.

- Other inputs to collect and document: historical volatility of similar listed companies, government bond yield curves for risk-free rate, dividend yield data and expected forfeiture rates based on historical turnover.

Step 4 — Select Model and Run Sensitivity Testing

Once the inputs are collected and documented, the valuation adviser selects the most suitable option-pricing model for the plan being valued.

- Black-Scholes for vanilla plans with straightforward exercise conditions; Binomial / Trinomial Tree for plans with early exercise or non-market performance conditions; Monte Carlo Simulation for plans linked to market performance (e.g. TSR performance rights).

- Sensitivity analysis identifies the impact of changes in key assumptions (especially expected volatility, early-exercise assumptions, and the risk-free rate) on the plan's fair value.

- The sensitivity analysis is a test of the stability of the valuation conclusion to likely changes in the inputs, and a guide to what inputs management and auditors should be most alert to as possible sources of significant fair value change.

Step 5 — Issue Final Valuation Report

The last step is the preparation and delivery of the valuation report, which describes the scope of the engagement, plan characteristics, inputs and assumptions, the model used, sensitivity analysis, and the fair value results for each grant being valued.

For annual audit and financial statement disclosure, the report must provide auditors with the necessary information to test and question assumptions – such as the rationale for the methodology, the basis for calculating comparable volatility, the value per share of equity and the fair value per option at the grant date.

For valuations conducted for employee tax reporting or regulatory disclosure, the report formats and content may vary.

The report is the professional judgement of the valuation adviser – it needs to be technically correct, well documented and withstand the scrutiny of the AASB 2 audit procedures applied to the share-based payment disclosures.

09Our Valuation Process

Why a Structured Process Matters

The practice of ESOP valuations is based on a standardised engagement process. This process allows companies to plan their reporting cycles, gives audit teams insight into the available documentation, and enables HR and finance executives to manage the grant cycle.

- For unlisted companies, the equity valuation step is frequently the longest part of the engagement process, because it involves a full business valuation to determine the share price.

- Companies that maintain a current equity value, documented at each major funding round or at least annually, will dramatically shorten the ESOP valuation timeframe by eliminating this step.

- Keeping an up-to-date share price is not only a financial reporting best practice, but also an operational control for all subsequent processes that rely on it.

Table 2: ESOP Valuation Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — Understand Plan Structure | Discuss the terms of review options, types of plans, the date of the grant, types of participants, and accounting under AASB 2. | Plan document; company brief on the structure of the grant. | Engagement scope memo; AASB 2 classification analysis. |

Step 2 — Information Request | Prepare requests for legal, financial, and assumption data; set up a data room. | Engagement scope. | Detailed information checklist; data room setup. |

Step 3 — Equity Valuation (Unlisted) | Carry out an underlying equity valuation to determine the current share price (for unlisted companies); scrutinise the cap table. | Financial reports, funding rounds, cap table, comparables. | Share price; cap table allocation analysis. |

Step 4 — Assumption Assembly | Collect and document all option-pricing inputs: volatility, risk-free rate, forfeiture rates, and early-exercise assumptions. | Cap table; comparable listed companies; government bond yields; HR turnover data. | A written set of assumptions, including benchmarking justification. |

Step 5 — Model Selection and Calculation | Choose and parameterise a suitable pricing model; run the valuation; perform sensitivity testing on key assumptions. | All assembled inputs; methodology rationale. | Option pricing model output; sensitivity analysis tables. |

Step 6 — Final Report | Write valuation report recording scope, assumptions, model and conclusions; issue report for audit and management use. | All previous outputs; management factual review. | Final signed ESOP valuation report complying with AASB 2. |

10Indicative Timeline and Frequently Asked Questions

Planning Around Realistic Timelines

Knowing realistic engagement timelines is critical for finance departments in managing their audit cycles and HR departments in managing their grant cycles. The length of an ESOP valuation engagement will vary based on plan structure, whether an underlying equity valuation is needed, and the quality of documentation provided up front.

Table 3: Indicative ESOP Valuation Timelines

Assignment Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

Simple grant — listed company, Black-Scholes | 2–3 business days | Adequacy of grant documentation; observable share price. | Straightforward — all inputs are market-observable. |

Standard ESOP — unlisted, single grant date | 1 week | Equity valuation timeline; completed cap table and plan documents. | Requires an equity valuation step to derive the share price. |

Multiple grant dates/participants | 1–2 weeks | Number of different grants; consistency of terms across grants. | More efficient when plan terms are standardised across participants. |

Complex awards — market conditions, Monte Carlo | 2–3 weeks | TSR design; peer group calibration; simulation parameterisation. | Requires detailed plan design review and auditor pre-engagement. |

Startup ESOP with complex capital structure | 2–4 weeks | Complexity of equity valuation, waterfall analysis, and option pool design. | Equity value allocation may require OPM or PWERM. |

Which model is best for ESOP valuation?

The best model depends on the plan’s structural complexity and participants’ exercise behaviour.

- Black-Scholes Option Pricing Model: best for traditional employee options with straightforward exercise conditions, no market-based performance conditions, and little or no early exercise.

- Binomial / Trinomial Tree Model: best for American-style exercise rights, multiple vesting conditions, or non-market performance conditions where the lattice structure is more appropriate to model employee behaviour.

- Monte Carlo Simulation: needed for market-based awards like TSR performance rights, where the payout is based on relative share price performance over a measurement period.

Do startups need ESOP valuation?

Yes – and this is a common miscalculation among early-stage companies in terms of their accounting and compliance requirements.

- The accounting for share-based payments (expense recognition) under AASB 2 is not dependent on the company's listing status, profitability or revenue.

- ESOPs for startups require an equity valuation to determine the current share price, followed by an option-pricing model to determine the fair value of the option granted on the date of grant.

- Companies subject to their first external audit (often at Series A or B funding stage) risk being adjusted by the auditor for previous grants if ESOP valuations were not recorded at the time, which could impact the current and prior period financial statements.

Is this required for the audit?

Yes. The share-based payment expense is a required disclosure in the financial statements of any entity that has awarded equity to employees, directors or other service providers under AASB 2.

- When auditing share-based payment disclosures, auditors need to evaluate the reasonableness of the fair value measurement and the assumptions underlying it, including the expected volatility for unlisted entities and the appropriateness of the chosen model for the plan design.

- The main audit evidence for this is the professionally prepared ESOP valuation report, which sets out the methodology, inputs, benchmarking and sensitivity analysis.

- In the absence of this, companies may face an incomplete audit or even an audit qualification of the share-based payment disclosure.

11 Challenges and Lessons Learned

Challenge 1 — Volatility Estimation for Unlisted Companies

The most common technical challenge in valuing ESOP is volatility estimation for unlisted companies. While listed entities have historical share prices, unlisted companies rely on comparables – and the choice, weighting and adjustment of these comparables is a matter of professional judgement that is important and often contentious.

- For an at-the-money option, a 10% change in expected volatility can change the fair value (and income statement expense) by 20-30%. This is why auditors scrutinise the volatility assumption.

- Practitioner lesson: the volatility benchmarking analysis must be thorough, well-supported, and auditable to the same extent as a material accounting estimate.

- Company lesson: never take a volatility assumption for your ESOP valuation at face value - make sure to understand how it was determined and whether it is appropriate for your company's life cycle, industry and risk profile.

Challenge 2 — Timing of the Engagement

Challenge 2 – Timing ESOP valuation engagements are often initiated late in the audit process – after the audit has started, or even after the draft financial statements have been prepared – with little time to complete a comprehensive process, and pressure on the valuation adviser and auditors.

- Companies that are best positioned to overcome this challenge consider the ESOP valuation process as part of the year-end close - initiating the engagement well before the audit, preparing documents in advance, and having the valuation report to provide to auditors as the audit commences rather than in the middle of the audit.

- Companies with annual grant cycles can benefit from a standard engagement calendar with set trigger dates (depending on the grant date and year-end deadline) that transform the ESOP valuation process from reactive to proactive and controlled.

Challenge 3 — Plan Design Complexity

Challenge 3 – Plan Design Complexity The complexities of valuation encountered in many ESOP engagements – complex performance conditions, non-standard exercise arrangements, cash and equity settlement – are often a direct result of plan designs that have not been sufficiently discussed with the finance and tax teams that will ultimately be responsible for accounting for and valuing the instruments.

- The best investment a company can make in its ESOP program is to include the CFO, external auditor, and valuation adviser in the plan design process to ensure the plan achieves its commercial and incentive goals, and is simple to account for, value and administer.

- A beautifully conceived incentive plan that cannot be valued is not a beautifully conceived plan, no matter how creative its commercial design.

12 Conclusion and Actionable Insights

Why ESOP Valuation Matters

ESOP valuation is mandatory under AASB 2 – it’s not voluntary. All entities that issue equity-linked instruments to employees, directors or service providers must comply, whether large or small, listed or unlisted, profitable or not. The valuation standard impacts the quality of financial statements, audit findings, tax implications, and investor confidence in pay practices.

- Consider ESOP valuation as part of the regular pace of business, rather than a response to an audit, as a governance practice.

- Start valuations at the grant date.

- Keep a complete, up-to-date cap table as part of regular governance.

- Maintain up-to-date documentation of the ESOP scheme and ensure grant letters are accurate before an option is exercised or financial statements are prepared.

- Firms that follow this practice will have shorter, cheaper, and more defensible ESOP valuations than those firms that scramble to put their house in order at the end of the year.

For Finance and HR Teams

The most practical takeaway from this guide is the need to manage the ESOP as an ongoing governance process rather than an annual compliance project.

Understand which equity instruments are outstanding, have grant documents for all grants, keep the cap table up to date, and check whether any new grants have been issued that need to be valued before the next audit.

Companies that follow this process consistently achieve shorter, simpler, and more profitable ESOP valuations than those that have never gone through it before and are under time pressure to complete a deal or an audit.

Five Actionable Steps for Practitioners

For early- and mid-career professionals seeking to build expertise in ESOP valuation, here are some action items.

- Build proficiency in each of the three option pricing models (Black-Scholes, Binomial / Trinomial Tree, Monte Carlo Simulation) - not only in how to use these models, but also when and why they are best applied for different plan structures.

- Develop a strong understanding of AASB 2: notably the equity-settled vs. cash-settled, market vs. non-market performance conditions, and the remeasurement requirements for liability-classified awards.

- Build equity valuation expertise for unlisted entities - the integrity of the share price underpins all subsequent calculations, and deficiencies here are amplified throughout the valuation.

- Build strong volatility benchmarking skills: keep a current list of industry-relevant comparables and know how to apply listed-company volatility to the risk profile of unlisted companies.

- Get exposure to the entire ESOP process - plan design, award documentation, valuation, accounting journal entries, audit procedures, and employee tax reporting - as a wide range of skill sets that set you apart from the rest.

Our ESOP valuation practice spans the gamut of equity compensation instruments, plan designs, and regulatory settings – from a simple employee stock option in a start-up, to complex TSR-based performance rights in a listed company. We start with understanding your plan design and reporting obligations, and finish with a valuation you can trust for your financial statements, your auditors, and your employees. If everyone knows the value of equity compensation, that value should be determined by an independent valuation. |