Intangible Asset Valuation in Australia

Table of Contents

- 01 Introduction

- 02 What Is Intangible Asset Valuation?

- 03 Why Do Clients Need Intangible Asset Valuation?

- 04 Types of Intangible Assets Commonly Valued

- 05 Key Valuation Approaches

- 06 Key Value Drivers — What Increases or Reduces Intangible Value

- 07 Common Mistakes Before a Valuation

- 08 Information and Documents Required — Five Key Steps

- 09 Our Valuation Process

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is Intangible Asset Valuation?

- 03 Why Clients Need Intangible Asset Valuation in Australia?

- 04 Types of Intangible Assets Commonly Valued

- 05 Key Valuation Approaches

- 06 Key Value Drivers — What Increases or Reduces Intangible Value

- 07 Common Mistakes Before a Valuation

- 08 Information and Documents Required — Five Key Steps

- 09 Our Valuation Process

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

What Intangible Asset Valuation Is

Intangible asset valuation is the process of determining the fair value of non-physical assets that contribute to a company’s long-term value and economic success. Intangible assets are not physical assets like plant, property and equipment, but they are often the most valuable component of an enterprise in the modern economy.

- A pharmaceutical firm's portfolio of patents, a technology company's proprietary software, a consumer goods company's brand, and a professional services company's long-term customer relationships all create tangible, measurable, and valuable economic benefits.

- These assets will not appear on any balance sheet - and this is where the professional intangible asset valuation process adds the most value.

- The identification, measurement, and disclosure of intangible assets is a core professional skill in today's corporate finance, M&A, tax and dispute resolution practices.

Who This Guide Is For

If you are an acquirer trying to understand what you’re paying for in an acquisition, a CFO dealing with the accounting consequences of an acquisition, a tax director involved in an intercompany IP transfer, or an entrepreneur looking to monetise a proprietary technology platform, the success of your position will depend on the quality of the intangible asset valuation that underpins it.

- This guide explains what intangible asset valuation is, how it works, the information needed, the pitfalls commonly encountered, and the process followed to arrive at a credible valuation.

- This guide is for practitioners in M&A advisory, accounting, law, and executive management, providing a reference for understanding this discipline.

In the 21st century, the most important assets are those that are not on the balance sheet. Recognising, valuing and arguing for the value of those assets is one of the most important analyses in corporate finance today. |

02 What Is Intangible Asset Valuation?

Definition and Core Concept

Intangible assets are non-monetary, non-physical assets that yield future economic benefits. The valuation establishes the fair value of these assets based on their anticipated economic benefits, using approaches suitable for the type of asset and its intended use.

- Intangible asset valuation differs from traditional business valuation, which measures the value of the entire enterprise, in that it assesses the value of specific non-physical assets that create value.

- Historical cost accounting principles do not allow internally developed intangibles (such as customer lists, brands, and technology) to be recorded on the balance sheet.

- When the same intangibles are purchased in a business combination, AASB 3 requires them to be separately recognised and valued at fair value, and this is where professional intangible asset valuation provides most of its financial reporting benefits.

The Range of Assets That Require Valuation

The range of intangible assets that require professional valuation is broad and ever-growing as new types of digital and data assets become increasingly important to businesses.

- Trademarks: The reputation that underpins customer preference and price premiums.

- Customer relationships and customer contracts: The value of a base of existing customers and the revenue they will bring in the future.

- Patents and technology: The commercial exploitation rights to innovation.

- Software and home-grown systems: Becoming the primary source of revenue for technology companies.

- Licences and permits, non-compete agreements, domain names and digital assets, and intellectual property rights: All examples of different types of intangible value with varying approaches to valuation.

03Why Clients Need Intangible Asset Valuation in Australia?

The list of triggers that require professional valuations of intangible assets spans the entire commercial life cycle of a business, from the initial acquisition of an IP-rich target to the cross-border sale of a fully developed technology platform. Both practitioners and clients need to understand the broad spectrum of triggers, as the valuation’s purpose affects the scope, conduct, and reporting of the work.

Mergers, Acquisitions and Purchase Price Allocation

The most technically challenging and most common context for valuing intangible assets is the purchase price allocation (PPA) after a business combination under AASB 3.

- The consideration paid for an acquired entity must be allocated to all the assets and liabilities of the acquired entity at their fair values as of the date of acquisition, including intangible assets that may not have been recognised on the target's balance sheet.

- This means valuing each intangible asset identified - be it a brand name, a list of customers, a software platform or a portfolio of patents.

- Any remaining consideration is allocated to goodwill, which must be tested for impairment each year.

- So, the first PPA is crucial - it establishes the basis for all future reporting periods.

Financial Reporting

In addition to PPA, intangible asset valuations are needed for fair value measurements under AASB 13, impairment testing under AASB 136, and audit assistance to auditors reviewing management’s fair value estimates.

- Companies with significant intangible asset balances have ongoing valuation requirements that must be addressed to satisfy their auditors.

- For public companies, ASIC's financial reporting surveillance reviews the quality and timeliness of the inputs to valuation - such as discount rates, royalty rates, attrition rates and useful economic lives.

- An inadequate analysis can result in audit qualifications, restatements or inquiries by the regulator.

Tax and Transfer Pricing

Tax and intangible assets are among the most complex and important areas of tax.

- Tax reporting issues are triggered by the purchase, sale or transfer of intangible assets - such as capital gains tax and deferred tax.

- IP migration and intercompany transfers require especially robust valuations in light of the ATO's well-publicised interest in cross-border intangible transactions.

- AUSTRAC obligations are not tender obligations. They are enforceable in law and backed by some of the highest civil penalties in Australian commercial law.

Litigation, Disputes and Strategic Purposes

The valuation of intangible assets is also required in a variety of litigation, dispute and strategic commercial settings, each of which has its own evidentiary and independence considerations.

- Disputes between shareholders often relate to the value of intangible assets, such as a computer platform or a customer list, built up during a joint venture.

- Intellectual property infringement cases require the calculation of damages resulting from the unauthorised use of an asset.

- Legal advice and expert reports in such matters must comply with the jurisdiction's evidentiary requirements, including the Expert Witness Code of Conduct.

- Licensing, benchmarking of royalty rates, sale of intellectual property, and financial support for financing using IP as collateral are just some of the commercial applications of intangible asset valuation.

04 Types of Intangible Assets Commonly Valued

The range of intangible assets valued by professionals is broad, and each type has its own analytical features, data needs, and analytical preferences.

Brand and Trademark Valuation

Brand and trademark valuation is one of the most publicised and most complex applications of intangible asset valuation. A brand is not just a symbol or name, but the reputation capital that has been built, resulting in customer preference, pricing power, and the ability to earn a return in excess of that earned by an unbranded entity.

- In M&A transactions, the brand is often the most important component of the premium over the net tangible assets.

- In brand monetisation and licensing, the brand value is used to determine the royalty rates paid by licensees.

- The relief-from-royalty method, which values the brand as the present value of the royalty payments the business would otherwise have to pay, is the most common method for valuing brands in PPA and standalone valuations.

Customer Relationship Valuation

Customer relationship valuations reflect the value of an entity’s existing customer relationships – the expectation that they will remain and transact, and the revenue stream that will result from their continued patronage.

- This includes customer contracts with fixed terms and remaining term lengths, as well as the ongoing customer base in businesses where the relationship is not contractually defined.

- The value must reflect the churn-adjusted revenue streams - the likelihood that current customers will continue to transact, discounted for the attrition that inevitably takes place.

- The multi-period excess earnings method (MPEEM), which separates the earnings attributable to the customer relationships from those attributable to all other assets, is the most popular in the PPA environment.

Technology and Software Valuation

Technology and software valuation is one of the most sought-after specialisations within the field of intangible asset valuation, reflecting the rise of technology-based business models and the associated increase in technology-related mergers and acquisitions.

- Valuation of software platforms, SaaS (Software-as-a-Service) products, patents covering technical innovations and algorithms underpinning data-driven businesses all need to take account of the commercial value of the technology in its present form and how that value is likely to change over time.

- The risk of obsolescence - the speed with which other technologies may diminish the commercial value of the asset - is a key insight in valuations of technology and one of the hardest to make.

- The income approach (using incremental cash flows attributable to the technology) and the cost approach (using the cost to recreate the platform or software) are widely used, either separately or together.

Intellectual Property Valuation

Intellectual property valuation is a broad term that refers to the valuation of patents, trademarks, trade secrets and proprietary processes – the legally protected innovations and knowledge resources that are the unique sources of competitive advantage for businesses.

- Valuation of patents involves consideration of the uses of the protected innovation, the duration of the patent's legal protection, the substitutes available to users if they do not have access to the patent, and the market for licensing similar IP.

- Valuation of trade secrets, such as proprietary formulations, manufacturing processes, customer and pricing information, is complicated because they are only valuable if they remain secret, and neither formal registration nor legal terms determines their lifespan.

- Professionals in the pharmaceutical, manufacturing, consumer products, and technology industries need to be aware of these issues to provide reliable valuations.

05Key Valuation Approaches

The three major families of valuation methods used to value intangible assets – the income approach, the market approach and the cost approach – reflect different conceptualisations of the value of an intangible asset. Practical application requires not only technical competence in each approach, but also the skill to choose and apply the approach that is most suited to the particular asset and purpose, and to use other approaches to corroborate the primary approach.

Income Approach

The income approach is the most common approach used in valuing intangible assets, because it captures the value of most intangible assets – the expected future economic benefits.

- Relief from royalty method: Values the asset as the present value of the royalty payments the business avoids by owning rather than licensing the asset. The primary method for brands and trademarks.

- Excess earnings method: Values the asset by calculating the earnings attributable to it after deducting the returns attributable to all other contributing assets - the main method for customer relationships and enabling technologies.

- Incremental cash flow method: Values the asset by comparing the cash flows it generates with those it would generate in its absence, measuring the contribution of the intangible.

- Multi-period excess earnings method (MPEEM): A longer-term variant of the excess earnings method that is tailored to the primary value-generating intangible in a PPA. The most complex of the income approach methods.

- Widely used for brands, technologies and customer relationships.

Market Approach

The market approach is based on comparable market evidence from comparable transactions to benchmark the value of the subject intangible asset. It provides the evidence that gives the methodology quantitative rigour.

- Royalty benchmarking: Relies on databases of license transactions to determine the market rate for the use of comparable assets, providing an empirical basis for the royalty rate in the relief-from-royalty method.

- Comparable IP transactions: Sales or acquisitions of comparable intangible assets by comparable parties offer direct evidence of the price paid for assets of comparable type, quality and commercial characteristics.

- Licensing agreements and comparable brand sales: provide the empirical foundation for the market approach - based on observed transactions.

- Key difficulty: Intangible asset transactions are frequently confidential, partially disclosed, or involve combining intangible assets with other assets, making it hard to isolate the value of the intangible asset being valued.

Cost Approach

The cost approach is based on the cost to replace or recreate an intangible asset with a substitute of equal or similar utility.

- Typically used for internally-developed software, proprietary databases, digital platforms and replacement technologies - assets for which the replacement cost is the most relevant basis of value.

- The cost approach involves the estimation of the fully loaded cost of recreation -f development time, labour, testing and integration costs, and the opportunity cost of development, with an adjustment for obsolescence.

- It is seldom the only approach to valuing commercially active intangibles. Still, it can serve as a sanity check against income-based valuations and is the main approach for valuing assets that are cost centres rather than revenue centres.

06 Key Value Drivers — What Increases or Reduces Intangible Value

The Relationship Between Value and Uncertainty

The factors that drive the value of an intangible asset are, for the most part, the opposite of the factors that drive uncertainty about the value of an intangible asset. Intangible assets with robust legal protection, long remaining lives, and recurring cash flows attributable to the asset are valued more highly. Those with unclear legal ownership rights, a short remaining life or cash flows that are hard to assign receive discounts.

- Awareness of these factors - and their relative significance for different types of assets - is vital for professionals building valuation models and for clients who want to ensure the greatest value is assigned to their intangible assets.

Factors That Increase Intangible Asset Value

Legal protection is one factor that increases the value of intangible assets. Other factors support a high value for most intangible assets.

- Strong legal protection: A patent with remaining years of protection and active enforcement, or a trademark registered across all relevant jurisdictions with a consistent history of use, provides a defensible legal basis for exclusivity and commercial value.

- Renewable income: The attribute that makes customer relationships and software-as-a-service so valuable - the cash flow predictability that translates into higher present values and/or lower discount rates.

- Long customer relationships and low attrition: Prolonging the effective, useful economic life of customer relationships.

- Proprietary technology: Technology that addresses a significant commercial need and has few substitutes is valuable, and the value is reflected in the price.

- Brand recognition, a long useful life with continuing investment and significant licensing opportunities: All adding value to intangibles.

Factors That Reduce Intangible Asset Value

Factors that decrease intangible asset value are also very helpful to clients when preparing for a valuation. They add uncertainty, risk, or time restrictions, which buyers, investors, and auditors will discount.

- Litigation regarding ownership, validity, infringement: Creates contingent liabilities that obfuscate the value of otherwise economically successful intangibles.

- Limited remaining life: A patent nearing expiry, a customer contract with a limited remaining term, a software platform nearing obsolescence - all reduce value by reducing the time over which cash flows can be generated.

- Insufficient protection or registration: A brand being used but not properly registered, or a software platform in use but not properly assigned by the developers, creates ownership uncertainty, reducing value.

- Customer attrition risk: Shortens the economic life of customer assets and, therefore, their present value.

- Outdated technology and reliance on specific contracts that don't renew: Both pose concentration and time risks that are reflected in the valuation discount rate and the asset's useful life.

Table 1: Intangible Asset Value Drivers — Impact and Management

Value Driver | Direction | Why It Matters | How to Strengthen Before Valuation |

|---|---|---|---|

Legal protection and registration | Increases value | Lays down justifiable proprietorship and exclusivity. | Register trademarks and patents; audit and renew filings; ownership audits. |

Recurring and contracted revenue | Increases value | Brings visibility of cash flow and aids in increased multiples. | Formalise customer arrangements; where feasible, convert them into multi-year contracts. |

Retention of customers and low churn. | Increases value | Prolongs the practical, useful life of relationships with customers. | Retention of documents by cohort; determine and mitigate churn drivers. |

Unique/defensible technology | Increases value | Symmetric replacement promotes high royalty fees. | Keep competitive advantage; record patent portfolio. |

Good brand awareness and investment. | Increases value | Prices and licenses potential. | History of document brand investments; maintain industry branding standards. |

Legal disputes over ownership / IP | Reduces value | PC creates contingent liability and ownership uncertainty | Clean up or disclose; secure clean IP ownership chain records. |

Short remaining legal or commercial life | Reduces value | Period of economic benefit extraction of compresses. | Re-register; renegotiate contracts to lengthen term. |

Churn and concentration risk with customers. | Reduces value | Reduces anticipated cash flow from customer relations. | Diversify the customer base; enhance customer retention; record customer attrition by cohort. |

07 Common Mistakes Before a Valuation

Why Preparation Failures Are So Common

The types of preparation mistakes that make intangible asset valuations more difficult, according to practitioners, are remarkably consistent across industries and asset types. In most cases, they are also avoidable – if the client understands what is needed before the engagement starts and prepares accordingly.

- Good preparation not only enhances accuracy and efficiency but also protects the defensibility of the valuation conclusion if it is subject to external scrutiny by auditors, tax examiners, or the courts.

Incomplete IP Documentation — The Most Common Failure

The most common failure in preparation is inadequate IP documentation. Companies often enter an intangible asset valuation engagement without a complete and up-to-date inventory of IP assets.

- They may not know which trademarks are registered and in which countries, may not know the ownership history of software developed by contractors who were not asked to assign their IP rights, and may not know how much life remains in a patented asset whose renewal date has not been tracked.

- Absence of ownership documentation - the lack of formal IP assignments from the software developers, founders or contractors - is particularly problematic, as it introduces legal uncertainty as to whether the business actually owns the asset being valued.

- Valuation of an asset subject to an uncertain title is not a good basis for any commercial, accounting or tax decision.

Other Common Preparation Issues

Some other common preparation issues can affect the quality of the valuation.

- No documentation of claimed customer relationships: When the valuer is engaged to value a customer base, but cannot find the contracts or customer data to support the nature and duration of the relationships.

- Unrealistic revenue projections for technology or brand assets without supporting market analysis.

- No clear rights to the underlying joint development or licensing arrangements.

- No royalty benchmarks to support the relief from royalty analysis for brand or technology assets.

- The highest-quality intangible asset valuations are developed by practitioners who treat the information-gathering process as an investigation, identifying gaps in ownership, questioning uncorroborated assumptions, and documenting the evidence for all critical inputs before modelling begins.

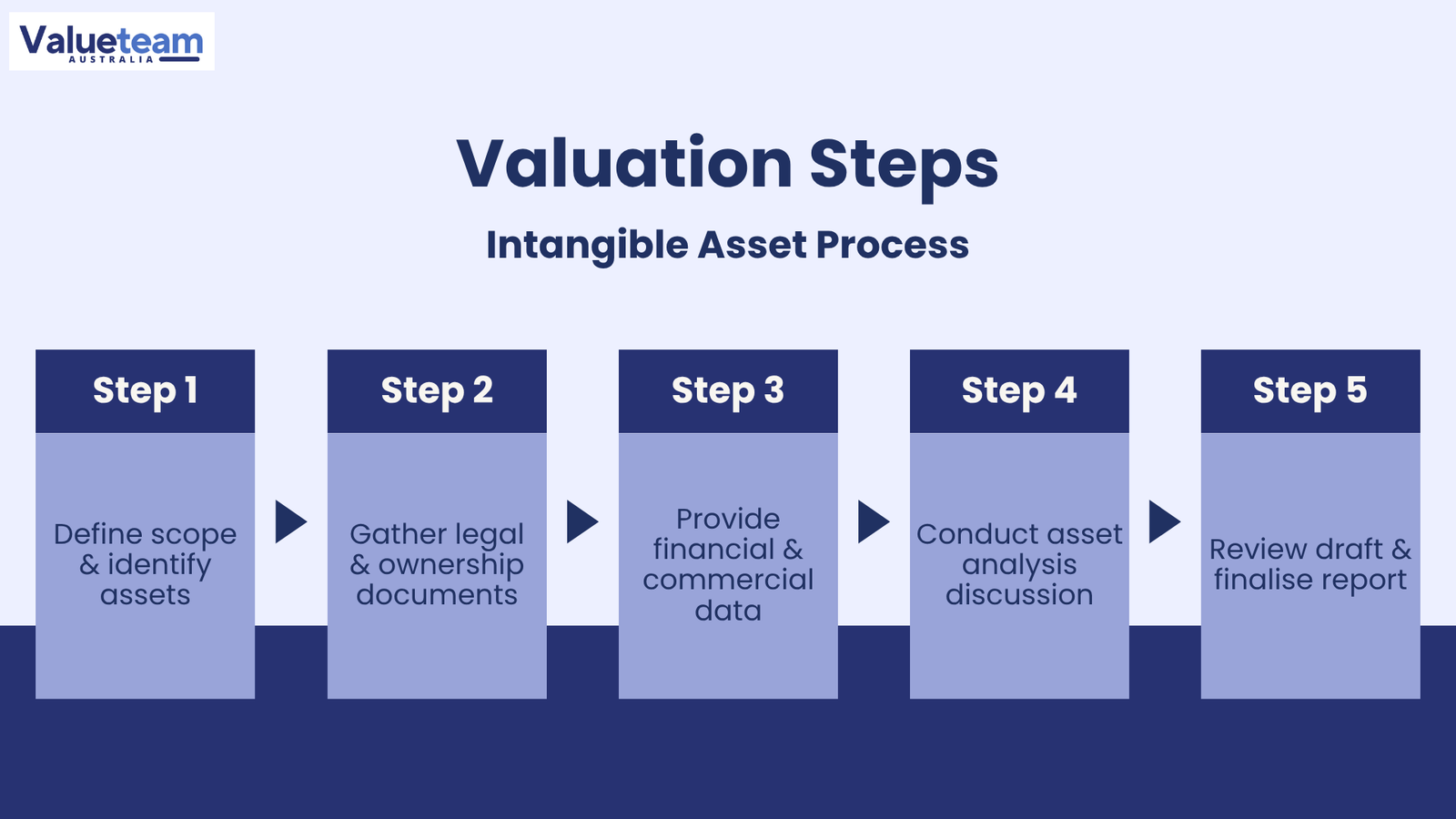

08 Information and Documents Required — Five Key Steps

The information-gathering phase of an intangible asset valuation engagement is organised into five steps: defining the scope, gathering information, analysing the information, preparing the final report, and delivering the final report. Each step builds on the previous one, and the success of each depends on the client’s preparation.

Step 1 — Scope and Asset Identification

The process starts with a scoping discussion before requesting documents to determine the valuation nature, the assets being valued, the valuation date, and the standard of value.

- For a PPA, this means identifying all intangibles acquired in the transaction that are significant enough to be separately identified and valued.

- For a tax engagement, this involves identifying the asset being transferred and the countries involved.

- For a litigation engagement, this involves understanding the scope of the court's instructions and what question the expert is being asked to answer.

- This step avoids the most common and expensive type of rework in valuations: realising midway through the engagement that the asset being valued is not the asset that the client actually wanted valued.

Step 2 — Obtain Legal and Ownership Documentation

The second step is to obtain legal documentation to confirm ownership and legal attributes of each identified asset. Any ownership gaps identified here need to be resolved before valuation.

- IP documents: Trademark registration certificates demonstrating the name of the registered owner, the country of registration and whether it has been renewed; trademark and patent certificates which demonstrate its validity and the life of the registered right.

- Assignments, licences and sub-licences that impact asset ownership or use.

- For software and technology assets: Software development agreements, contractor IP assignment deeds, and open-source licence compliance reports.

- For customer relationship assets: Master service agreements, subscription agreements and renewal terms that govern the legal relationship.

- Any ownership gaps identified here should be addressed before the valuation, not subsequently.

Step 3 — Provide Financial and Commercial Data

With the legal structure in place, the process turns to gathering the financial and commercial data that will be used in the quantitative analysis.

- Revenue (by product/asset): Historical and forecast revenue streams for each identified intangible, in sufficient detail to support the cash flow attribution analysis.

- Assumption setting out the rationale for projected revenue growth, margin and investment needs - documented and justified.

- For customer relationship assets: Attrition data: Historical customer retention rates by cohort, churn drivers, and changes in the customer base since the valuation date.

- Licensing agreements and royalty arrangements that provide direct market evidence for benchmarking of the royalty rate.

- For assets being valued in an acquisition context: Acquisition documents such as the sale and purchase agreement and/or pricing schedules.

Step 4 — Attend Asset Analysis Discussion

The asset analysis discussion is the qualitative heart of the intangible asset valuation engagement – akin to the management discussion in a business valuation.

- The valuer's adviser explores the commercial characteristics of each asset: the competitive landscape in which the brand operates, the technology roadmap for the software platform, the nature and quality of customer relationships, and the continuing commercial value of the patent portfolio.

- The discussion provides the valuer with the information to make judgements about the useful economic life, risk of obsolescence, the likelihood of the projected revenue streams and the critical assumptions that will be tested in the sensitivity analysis.

- Clients that invest time to think through the commercial story of each asset - and can explain the drivers of value for each asset in detail - tend to have better, more robust valuations.

Step 5 — Review Draft and Finalise

The final step is management review of the draft valuation report – a critical opportunity to check for accuracy, but with limitations on what can be reviewed.

- An opportunity to verify the factual data - descriptions of assets, ownership arrangements, revenue allocation rules, contractual arrangements - and ensure the report reflects the commercial reality of each asset.

- It is not a debate of the valuation outcome: the professional judgement of the valuation adviser must be independent and objective, and any factual amendments must be justified and not based on preference.

- For PPA and financial reporting valuations, the review is also coordinated with the audit team to ensure the methodology and conclusions are acceptable to the auditors before the report is issued.

- Once the factual review is complete and issues are resolved, the report is issued as the professional opinion of the adviser.

09Our Valuation Process

Why a Structured Process Matters

A clear and transparent process is the foundation of sound intangible asset valuation practice. Knowing this process supports the client in planning appropriately, understanding the timeframe involved, and working effectively with the valuation adviser throughout.

- By far the most significant driver of engagement length is the quality of the legal documentation provided at Step 2.

- Incomplete IP ownership, missing registration certificates, or undocumented contractor IP assignments can lengthen an engagement from days to weeks, as these issues must be resolved before the valuation analysis can be completed with confidence.

- Clients who proactively audit IP ownership and gather a complete set of documentation before the engagement starts consistently get the best results in the shortest time.

Table 2: Intangible Asset Valuation Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — Scope Discussion | Identify the purpose, type of asset, valuation date, and the standard of value used; confirm the terms of engagement. | Client brief: trade or reporting situation. | Engagement scope memo; signed engagement letter. |

Step 2 — Information Request | Prepares a request form for IP registration, including legal, financial, and commercial information. | Engagement scope | Information checklist; document portal or data room set up. |

Step 3 — Asset Analysis | Evaluate the legal ownership, useful economic life, competitive position and contribution of cash flow of each of the identified assets. | IP documents, contracts, revenue data, and management discussion notes | Inventory of assets; useful life evaluations; ownership. |

Step 4 — Methodology Selection | Choose a primary valuation technique for each asset and cross-check it; locate benchmarks for royalties and similar data. | Characteristics of assets: use; market information. | Methodology memo, rate of royalty benchmarks, and similar transactions data. |

Step 5 — Draft Analysis | Construct valuation models; prepare assumptions; sensitivity analysis; prepare draft report. | All the financial and qualitative inputs are similar. | Draft management report of valuation to management and the auditor. |

Step 6 — Final Report | Response to factual review comments; respond to auditor feedback (where appropriate); publish final signed report. | Factual review by the management; auditor questions. | Final signed intangible asset valuation statement. |

10Indicative Timeline and Frequently Asked Questions

Planning Around Realistic Timelines

Time is a key practical consideration for clients and practitioners in intangible asset valuation. The nature of the documentation and analysis that may be required varies greatly depending on the type of asset and the purpose of the engagement – and realistic timelines can help clients plan for their transactions, reporting and tax returns accordingly.

Table 4: Indicative Intangible Asset Valuation Timelines

Assignment Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

Simple standalone asset valuation | 3–5 business days | Fullness of IP and monetary records. | Makes assumptions regarding all the documentation at the beginning of the engagement. |

Standard intangible asset valuation | 1–2 weeks | Size of portfolio; intricacy of cash stream attribution. | Principles PPA on 2-3 identified intangibles. |

Complex PPA with multiple intangibles | 3–5 weeks | Number of acquired intangibles; MPEEM contributing asset framework | Has to be coordinated with auditors; it depends on the financial close schedule. |

Tax/transfer pricing IP valuation | 2–4 weeks | The length documentation requirements of the ATO arm, OECD TP guidelines. | Should create up-to-date records of TP defence. |

Litigation/expert report | Varies — court-driven | Scope of instructions; discovery; expert conclave requirements | Under the Expert Witness Code of Conduct, time is directed by the court. |

What Intangible Assets Can Be Valued?

The full range of intangible assets that can be valued includes brand names and trademarks, customer relationships and customer contracts, patents and proprietary technology, software and in-house developed systems, licences and permits, non-compete agreements, domain names and other digital assets, and intellectual property rights more broadly.

- If an asset produces economic benefits, and its value can be documented - either by income streams, market data or replacement cost - then it can be valued.

- The limiting factor is nearly always the lack of documentation and data to support the application of a valid method, rather than the lack of a method itself.

Which Method Is Most Common?

The most common method for valuing brands and trademarks, as well as technology and software, is the relief-from-royalty method because it provides a market-based, intuitive basis of value that auditors and regulators can understand.

- In PPA valuations, the most common method for valuing the customer relationship is the multi-period excess earnings method (MPEEM), which is specifically designed to isolate the value of the dominant asset in a contributing asset structure.

- The most convincing valuations use two or more methods and triangulate.

Is This Required for Acquisitions?

Yes. The AASB 3 standard requires all intangible assets acquired by the acquirer to be identified and measured at the acquisition date.

- If the intangible assets of the entity being acquired, such as its brand valuation, customer relationship valuation, technology and software valuation, or intellectual property valuation, are material, a professional PPA is required.

- The results flow through to the post-acquisition financial statements - which assets are separated from goodwill, and their amortisation - and will be scrutinised by external auditors as part of the audit of the financial statements for the year of acquisition.

11 Challenges and Lessons Learned

Challenge 1 — The Ownership Problem

The ownership problem is the most common issue in intangible asset valuations. The ownership of an intangible asset is completely a legal construct, and one that is far more tenuous than most business owners realise until ownership is tested in a valuation or transaction.

- Software programming done by a contractor who was paid but not asked to assign IP rights, a brand name that has been widely used in the marketplace but registered in a country where the registration has expired, a technology platform where the basic algorithm was developed by a founder prior to the company being incorporated - these are all common but potentially serious ownership issues.

- The practitioner lesson: don't take ownership for granted, check the chain of title.

- The client's lesson: do an IP ownership audit long before any transaction or reporting event that requires the intangibles to be valued. If the issue is detected six months before a transaction, it can be fixed; if it is detected during due diligence, the transaction could be lost.

Challenge 2 — Useful Economic Life Estimation

The second challenge is estimating useful economic life. The useful life of an intangible asset is one of the most important decisions in the valuation process – it defines the time period over which the cash flows are forecast and discounted, and for PPA purposes, the amortisation expense that will be charged to the acquirer’s profit and loss statement for many years to come.

- Estimating the useful life of a customer relationship requires consideration of historical retention rates, customer contract length and the factors that might prompt a customer to switch.

- Estimating the useful life of a technology platform requires analysing the rate of technological innovation in the industry and the investment required to stay competitive.

- Estimating the useful life of a brand requires assessing past investments in the brand and market factors that may devalue or enhance it.

- Both require industry knowledge, rigour, and documentation - and it is judgment that will be most heavily challenged by auditors and opposing experts.

Challenge 3 — Keeping Market Intelligence Current

Challenge 3 – Keeping the Royalty Rate and Comparable Transaction Databases Current. Comparable licensing royalty rates shift with market forces, new technology and competition.

- Comparable transaction multiples fluctuate with M&A market conditions.

- Those who provide the best valuations of intangible assets are those who have the most up-to-date information on royalty benchmarks and comparable transactions.

- They value the currency of their market knowledge as an important business resource - not as a research project performed at the time of a particular assignment.

12 Conclusion and Actionable Insights

Why Intangible Asset Valuation Matters

Intangible asset valuation is the process of determining the fair value of non-physical assets that affect a business’s economic performance and value, and it is more important than most businesses appreciate until it is too late.

- These assets are typically the primary components of value, particularly for technology, brand and service firms.

- Their identification, measurement, and reporting are the foundation of credible M&A transactions, accurate financial reporting, tax reporting, and dispute settlement.

- A sound valuation helps businesses support transactions, financial statements, tax returns, restructuring and other initiatives, and business decisions - and the support is only as good as the valuation.

For Business Owners and Management Teams

The practical takeout from this article is to keep an up-to-date inventory of IP assets.

- Understand what intangible assets the business has, have official documentation of ownership, ensure that registration certificates are current and renewed, and periodically assess whether new events have resulted in new intangible assets that have come into being, and should be identified, protected and documented.

- Companies that follow this practice have shorter, less stressful, and more profitable valuations than those that are trying to piece together their intangible asset landscape for the first time under the gun of a deal or reporting deadline.

Five Actionable Steps for Practitioners

For early- and mid-career professionals seeking to develop their skills in valuing intangible assets, the following five steps offer a learning plan.

- Step 1 - Master the technical details of the three main methodological approaches: the income approach (relief from royalty, excess earnings, and MPEEM); the market approach (royalty benchmarking and comparable IP transactions); and the cost approach for internally developed assets.

- Step 2 - Acquire a deep understanding of the financial reporting standards that generate the most common valuation situations: AASB 3 for PPA, AASB 138 for intangible asset recognition and amortisation, AASB 136 for impairment testing, and AASB 13 for fair value measurement.

- Step 3 - Build and keep up-to-date royalty and comparable transaction databases (market intelligence is as important as modelling).

- Step 4 - Invest in gaining industry experience in one or two areas where intangibles are important; technology, pharmaceuticals, consumer goods, and financial services are the most common. The capacity to apply general approaches with a degree of industry-specific knowledge is what sets a good analyst apart from a good adviser.

- Step 5 - Gain experience on PPA assignments early in your career, because the discipline of the contributing asset framework, the rigour of the MPEEM, and the coordination with external auditors that PPA demands will train you in more ways than any other type of intangible asset assignment.

Our intangible asset valuation advisory services span the range of asset types, uses and regulatory settings – from valuations of brands and customer relationships for M&A and PPA, to IP transfer pricing advice, to expert reports for litigation and shareholder disputes. Our work starts with your assets and needs, and concludes with a defensible answer. |

The most important assets in the economy are the intangible ones. The work is to make them visible, measurable and defensible – and it is important work.