ESG Reporting Guide in Australia

Table of Contents

- 01 Introduction

- 02What Is ESG Reporting?

- 03 Why Do Companies Need ESG Reporting?

- 04 ESG Reporting Frameworks Used in Australia

- 05 Key Components of ESG Reporting

- 06 Scope 1, 2 and 3 Emissions Explained

- 07 ESG and Business Valuation Impact

- 08Five Key Steps: The ESG Reporting Process

- 09Key Challenges in ESG Reporting

- 10Our ESG Reporting Process

- 11 ESG Reporting by Industry and Situation

- 12Indicative Timeline and Frequently Asked Questions

- 13 Challenges and Lessons Learned

- 14Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is ESG Reporting in Australia?

- 03 Why Do Companies Need ESG Reporting Guide in Australia?

- 04 ESG Reporting Frameworks Used in Australia

- 05 Key Components of ESG Reporting

- 06 Scope 1, 2 and 3 Emissions Explained

- 07 ESG and Business Valuation Impact

- 08 Five Key Steps: The ESG Reporting Process

- 09 Key Challenges in ESG Reporting

- 10Our ESG Reporting Process

- 11 ESG Reporting by Industry and Situation

- 12 Indicative Timeline and Frequently Asked Questions

- 13 Challenges and Lessons Learned

- 14Conclusion and Actionable Insights

01 Introduction

The Purpose of Impairment Testing

Environmental, Social, and Governance (ESG) reporting is increasingly a critical element of corporate disclosure and value enhancement in Australia. What started as a voluntary practice has become a fundamental aspect of how companies are valued by investors, funded by banks, rated by regulators and trusted by the communities they serve.

- This transformation has been driven by a combination of regulatory requirements, capital market developments, and empirical research showing that firms with better ESG practices have more sustainable performance.

- Investors now expect companies, regulators, and stakeholders to report on their management of environmental, social, and governance (ESG) factors.

The Regulatory Shift: From Voluntary to Mandatory

In Australia, this has shifted from voluntary to mandatory. The requirement for climate-related financial disclosures, as part of the Australian Sustainability Reporting Standards (ASRS) and aligned with the International Sustainability Standards Board (ISSB), represents the most significant shift in financial reporting in decades.

- Listed and large organisations are now obliged to report on their governance, strategy, risk, and metrics related to climate-related risks and opportunities.

- Those who have been working on ESG Reporting in Australia proactively are well served in this regard, compared to those who have been forced to do so reactively.

The Broader Benefits of ESG Reporting

ESG Reporting in Australia supports organisations in reporting on sustainability performance, risks, and access to funding. It’s more than regulatory compliance.

- Investors have incorporated ESG considerations into their investment strategies, assessing companies on environmental, social and governance performance, and board governance.

- Sustainability-linked loans from lenders are priced based on specific ESG targets, with lower rates for companies that achieve their goals.

- For financial, accounting, strategy, legal and advisory professionals, ESG Reporting in Australia is quickly becoming a core, not specialist, competency.

ESG reporting is not communication; it is risk management and governance. Those who understand it as such will be better prepared for all the regulatory, investor, and commercial challenges of the sustainability transition. |

02 What Is ESG Reporting in Australia?

Definition and Core Purpose

ESG Reporting in Australia is the practice of reporting non-financial information about a company’s environmental (E), social (S) and governance (G) practices. ESG Reporting in Australia is different from financial reporting, which explains what the company has done, how much it has spent, and what it owns.

- It provides information that financial statements don't: Is the company's business model sustainable? Is it managing climate risk? Does it have a culture that attracts and keeps employees and avoids major accidents? Does the board have the right incentives and independence?

Who Uses ESG Reporting and Why

It offers insight into a business’s operations beyond its financials. The comprehensiveness, accuracy and reliability of ESG reporting are important to a broader range of stakeholders than any other type of reporting.

- Investors: use it to evaluate the non-financial risks and opportunities that will impact future performance.

- Lenders: use it to assess whether sustainability-linked loan covenants are being met.

- Regulators: use it to track compliance with disclosure obligations and to assess systemic risks.

- Employees and job candidates: use it to determine whether an organisation's actions are consistent with its beliefs.

- Communities and civil society: use it to assess companies' environmental and social performance.

Where ESG Reporting Appears

ESG reports are typically found in annual reports, sustainability reports and investor presentations. The medium and form of disclosure depend on company size, regulatory mandate and audience.

- Companies listed on stock exchanges and subject to the ASRS requirements include climate change disclosures in their annual reports with their financial statements.

- Large companies tend to issue standalone sustainability, or ESG reports that cover the entire ESG landscape in more detail.

- For capital-seeking companies, ESG reporting is front of mind in investment decks and data rooms because savvy investors take ESG performance into account as part of their investment analysis, not as an "add-on".

03Why Do Companies Need ESG Reporting Guide in Australia?

The rationale for ESG reporting has shifted from a moral to an economic argument. ESG reporting companies that do it well are better off on all the commercial fronts – access to capital, risk management, talent management, branding and regulatory compliance.

Regulatory and Compliance Requirements

The direction of travel in Australia has been clear: ESG reporting requirements are increasing in breadth, detail and compliance. The Australian Accounting Standards Board’s Australian Sustainability Reporting Standards (ASRS), in line with the ISSB, mandate climate-related reporting for large entities – governance, strategy, risk management, and targets and metrics – in a standardised manner.

- These are not best practice principles - they are legal requirements enforced by the Corporations Act, overseen by ASIC.

- Companies need time to establish data-collection, governance, and reporting processes for mandatory climate disclosures, which can take several years.

- Australian companies also have a range of other sustainability compliance obligations: the Modern Slavery Act (for companies with turnover greater than $100 million), Workplace Gender Equality Act reporting, ASX Corporate Governance Council principles, and APRA standards for regulated financial institutions.

- Meeting global standards - ISSB, TCFD, and GRI - ensures Australian companies are not only compliant with local regulations but also with international investors and supply chain partners.

Investor and Capital Market Expectations

ESG has evolved from a niche to a mainstream investment consideration. Pension funds, sovereign wealth funds and global equity portfolios now consistently include ESG screening, ratings and engagement as part of their investment due diligence.

- For firms seeking to raise capital (through equity, debt, or private investment), the quality of ESG reporting and the underlying ESG performance impact access to sustainable finance, cost of capital, and the investor base for their securities.

- ESG due diligence is increasingly part of investor screening of growth-stage and pre-IPO companies - and companies that fail to demonstrate credible sustainability performance face a competitive disadvantage in capital markets, and an increased risk of activist investor targeting.

Risk Management

ESG reporting is, first and foremost, a risk management activity. Climate risk assessment (identifying the physical risks (extreme weather, flooding, temperature changes) and transition risks (carbon pricing, technology change, regulatory shifts) is required for in-scope companies under ASRS. Reducing operational risks through improved energy, water, waste, and worker safety management saves money and increases resilience.

- Sustainability supply chain assessments mitigate reputational, operational and regulatory risk.

- Risk mitigation in a world of social media and grassroots activism means ESG is a first-order business issue.

Business Strategy and Long-Term Value Creation

ESG reporting offers a framework for creating long-term value, as well as for compliance and risk management. Those companies that integrate ESG into their business strategy outperform those that view sustainability reporting as something that happens in isolation from the business.

- Uncovering opportunities in the low-carbon economy, increasing operational efficiencies from resource management and creating an employer brand to attract and retain employees.

- Improving their relationships with the communities and regulators on whom they rely.

- Enhanced operational efficiency from energy and water management initiatives, brand building, and stakeholder confidence-building are commercial benefits that accrue over time - and they start with measuring, reporting and improving.

04 ESG Reporting Frameworks Used in Australia

Navigating the Framework Landscape

ESG reporting frameworks have become much more streamlined in recent years, but there’s still a lot to navigate. The frameworks are tailored to different audiences, different uses, and different regulatory jurisdictions. The frameworks of most relevance to Australian companies can be grouped into three broad categories: mandatory regulatory frameworks, internationally accepted voluntary frameworks, and industry-specific disclosure frameworks.

The Mandatory Standard: ASRS and Its Relationship to ISSB and TCFD

The Australian Sustainability Reporting Standards (ASRS) are the main mandatory standard for Australian companies subject to the legislation. The ASRS standards are closely aligned with the ISSB standards (IFRS S1 – general sustainability disclosures; IFRS S2 – climate-related disclosures) as applied in Australia.

- ASRS reporting is mandatory for in-scope companies: it is required under the Corporations Act, and the disclosures are filed with ASIC as part of the statutory annual report.

- The TCFD framework, which preceded the ISSB and provided the conceptual framework for climate-related financial disclosure (governance, strategy, risk management, metrics and targets), is now largely incorporated into the ASRS/ISSB framework. Those that have been reporting under TCFD are well ahead of the curve on ASRS.

Voluntary Frameworks: GRI, CDP, and Sector-Specific Standards

In addition to the mandatory climate standards, the Global Reporting Initiative (GRI) remains the most widely used sustainability framework for reporting on the entire spectrum of ESG issues across environmental, social, and governance areas.

- GRI is valuable for companies that want to report on social and governance issues in detail beyond the climate focus of ASRS, and for companies that want to meet the information demands of a broad range of stakeholders, including NGOs, civil society, and supply chain partners.

- The Carbon Disclosure Project (CDP) is a platform for reporting on climate strategy, emissions, water, and forest management, and investors and procurement managers use CDP scores as benchmarks for comparing environmental performance.

- The choice of the appropriate mix of frameworks depends on the company's scale, sector, listing status, investor profile and the material ESG issues relevant to the company.

Table 1: ESG Reporting Frameworks — Overview and Application

Framework | Governing Body | Primary Focus | Best Suited For | Regulatory Status (Australia) |

|---|---|---|---|---|

ASRS (AASB S1 / AASB S2) | AASB / ASIC | Climate-related financial disclosures | Large/listed Australian entities with mandatory obligations | Mandatory for in-scope entities under the Corporations Act |

ISSB (IFRS S1 / IFRS S2) | IFRS Foundation / ISSB | General sustainability + climate disclosures | Entities with global investors; ASRS aligned | Basis for ASRS; de facto mandatory for ASRS reporters |

TCFD | Financial Stability Board | Climate governance, strategy, risk, metrics | Companies with climate-material operations | Embedded in ASRS / ISSB; phasing into mandatory requirements |

GRI Universal Standards | Global Reporting Initiative | Full ESG spectrum (double materiality) | Comprehensive sustainability reports; broad stakeholder audience | Voluntary; most widely adopted globally |

CDP | CDP (Carbon Disclosure Project) | Climate, water, forests | Industry benchmarking; supply chain transparency | Voluntary; widely required by procurement and investors |

Modern Slavery Act Reporting | Home Affairs / Attorney-General | Supply chain human rights | Entities with >$100M annual revenue | Mandatory under the Modern Slavery Act 2018 |

05Key Components of ESG Reporting

The Environmental, Social, and Governance (ESG) pillars of reporting cover a range of topics, metrics, and disclosure items. Knowing what must be disclosed in each pillar and the standards that govern disclosure in each is the starting point for successful ESG reporting.

Environmental (E) — Emissions, Energy and Climate

The environmental pillar relates to the organisation’s use of resources, emissions and waste, climate risk, and its impact on or contribution to environmental issues affecting the organisation and its communities.

- Greenhouse gas emissions (Scope 1, 2, and 3): the most reported and most highly regulated of the environmental measures - mandated by ASRS and TCFD, and the foundation for corporate net zero pledges and carbon price exposure analyses.

- Energy usage: total energy, renewable energy, and energy intensity (a measure of both climate risk and efficiency)

- Water consumption is becoming increasingly important for companies in water-intensive sectors or operating in water-scarce regions, thanks to the GRI and CDP water initiatives.

- Waste: waste generation, diversion and disposal within the value chain, as a measure of resource efficiency and circularity.

- Climate risk disclosures: the identification, measurement and disclosure of the physical and transition risks from climate change that may impact the organisation's financial and business strategies.

Social (S) — People, Communities and Supply Chain

Social relates to the organisation’s relationships with its people, supply chain and communities.

- Health and safety: accident rates, lost time injury frequency, and health and safety management systems - a core social metric for companies with physical operations, and a measure of cultural safety and operational risk.

- Diversity and inclusion: including gender representation at senior levels, gender pay gap analysis, and inclusion initiatives - increasingly mandated by the Workplace Gender Equality Act, and required by institutional investors as a measure of talent management.

- Employee practices and human rights: covering working conditions, living wage commitments and freedom of association - reflecting both ethical considerations and risk in the supply chain.

- Community engagement practices: showing how the organisation manages its social licence to operate, especially for those with significant local impacts, such as resources, infrastructure, and large employers.

Governance (G) — Structure, Controls and Accountability

The governance pillar relates to the structures, policies and processes that direct and control the organisation – and through which the organisation is accountable to shareholders and other stakeholders.

- Board composition and independence: the make-up of the board, the number of independent directors, diversity on the board, and the particular governance tasks of board committees - a key focus for institutional shareholders and proxy advisers.

- Remuneration: the design of remuneration packages, the criteria for variable remuneration and the relationship between executive incentives and value creation - assessed for the congruence between management actions and shareholder returns.

- Ethics and compliance: code of conduct, whistleblower policy, anti-bribery and corruption policy - signalling the cultural and systemic controls that reduce governance risk.

- Risk management: the approach to identify, monitor and disclose material risks, including ESG risks - increasingly considered a specific governance disclosure under ASRS and TCFD.

06 Scope 1, 2 and 3 Emissions Explained

The GHG Protocol Framework

The Greenhouse Gas (GHG) Protocol’s three-scope classification of corporate emissions is the cornerstone of how we understand and calculate corporate carbon footprints – and the basis for the emissions reporting requirements of ASRS, TCFD and GRI. These three scopes represent different types of emissions and, together, capture the full climate impact of an organisation’s operations and value chain.

Scope 1 — Direct Emissions

Scope 1 emissions are direct greenhouse gas emissions from sources owned or controlled by the entity – stationary combustion (boilers, generators, etc.), mobile combustion (owned vehicles, aircraft), fugitive emissions (refrigeration, gas systems) and process emissions (industrial processes).

- Scope 1 emissions are the most directly controllable by the entity. They are the first to be reduced in corporate decarbonisation initiatives through operational changes such as fuel-switching, electrification and efficiency measures.

- ASRS requires in-scope entities to disclose their Scope 1 emissions as of the first reporting period, making the creation of robust systems to measure Scope 1 emissions a practical first step.

Scope 2 — Indirect Energy Emissions

Scope 2 emissions are indirect emissions from the generation of purchased electricity, steam, heat or cooling consumed by the entity. While the emissions are not physically generated at the entity’s site, the GHG Protocol requires entities to include these emissions in their corporate emissions inventory, as purchasing decisions influence the demand for generation that generates the emissions.

- Scope 2 emissions must be disclosed using both the location-based method (using grid-average emission factors) and the market-based method (using emission factors that reflect the energy the entity has contracted to purchase).

Scope 3 — Value Chain Emissions

Scope 3 includes all other indirect emissions (value chain emissions – upstream and downstream). The GHG Protocol identifies 15 types of Scope 3 emissions, ranging from the production of purchased goods and services to the use and disposal of products sold.

- Scope 3 can be difficult to calculate but is increasingly critical for investors and regulators - it represents more than 80% of emissions for many companies.

- It is the key source of risk for investors in the transition to a net-zero world for supply chains and product portfolios.

07ESG and Business Valuation Impact

The Evidence Base for ESG-Valuation Linkage

The link between ESG and business valuation is one of the most important and widely studied areas in sustainability and finance. ESG-leading firms consistently have a lower cost of capital, lower earnings volatility, lower exposure to regulatory and reputation risk events, and greater long-term total shareholder return performance.

How ESG Factors Affect Valuation

ESG factors are increasingly taken into account in company valuations through their impact on the weighted average cost of capital (WACC), investor risk, long-term cash flow, regulatory risk, and brand value and reputation.

- Cost of capital channel: firms with higher ESG ratings attract a larger pool of investors (including ESG-mandated funds, which cannot invest in firms below a certain ESG rating threshold), thus lowering the equity risk premium and WACC.

- ESG-linked debt: the interest rate on debt finance is linked to the achievement of specific ESG milestones, directly linking ESG performance to the cost of debt financing.

- Cash flow channel: lower regulatory risk reduces the likelihood and severity of regulatory fines, penalties and restrictions; higher operational efficiency from energy and resource management reduces input costs; and a higher social licence to operate reduces the community and regulatory resistance that leads to delays and cost blowouts in large projects.

The Cost of Weak ESG Practices

The value effects of poor ESG practices are also real – and potentially more visible because poor ESG outcomes attract negative media coverage, shareholder activism and regulatory action that destroy market value.

- A European automobile manufacturer's governance missteps (hiding diesel engine emissions data) led to fines of over USD 30 billion, a permanent loss of brand value in core markets, and years of management distraction as its competitors accelerated their shift to electric vehicles.

- A multinational fast-fashion retailer whose supply-chain social practices were exposed by investigative journalists suffered a permanent loss of market share among its target consumers due to a consumer boycott.

- Positive ESG performance can add to enterprise value, and negative ESG practices can increase valuation discounts. The link between ESG performance and financial performance is more direct, more immediate, and more tangible than many management teams realise until they are in crisis.

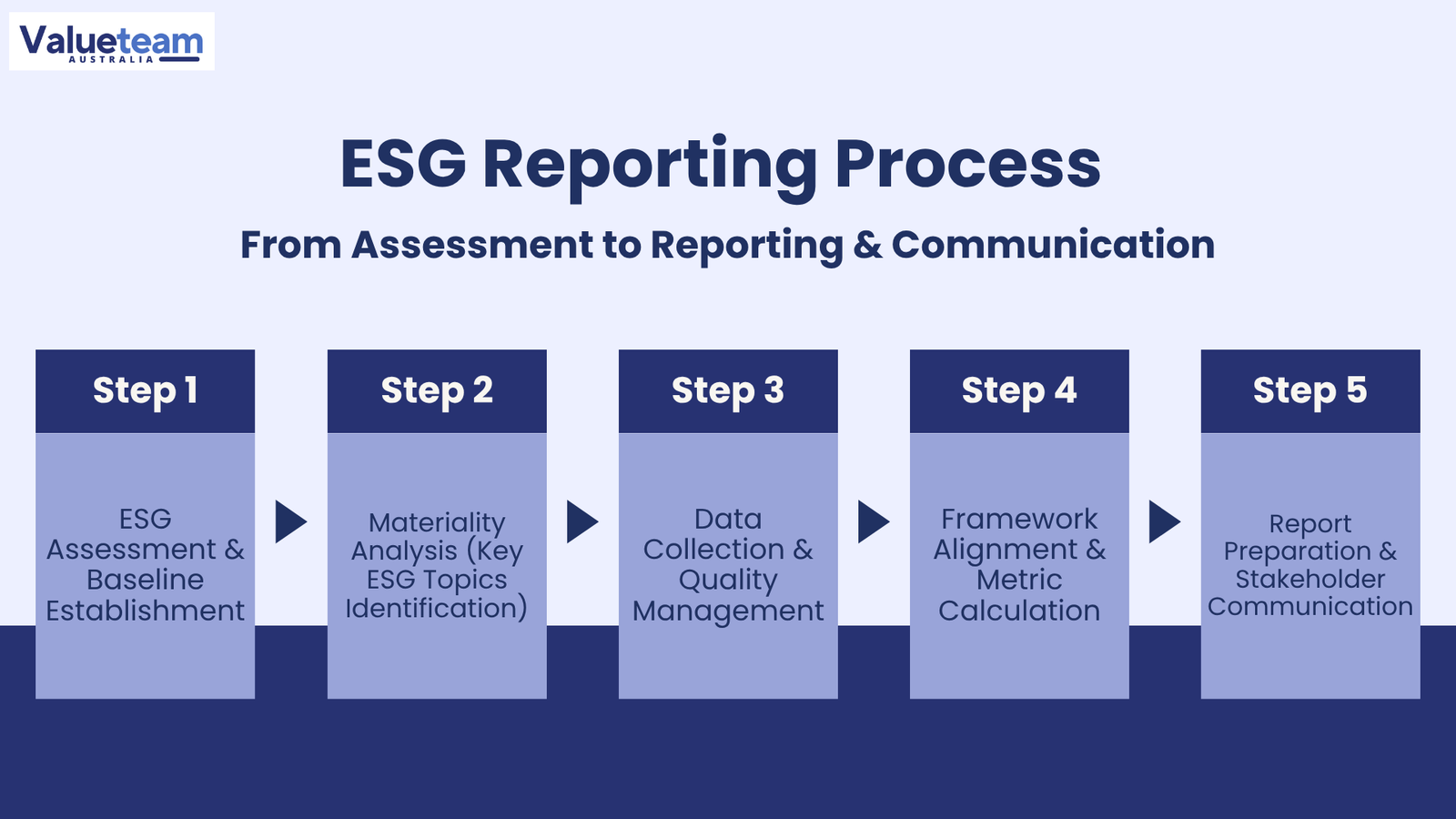

08Five Key Steps: The ESG Reporting Process

The process of developing a high-quality ESG reporting capability has a clear path from assessment and strategy, to data gathering, alignment and reporting. The following five steps are the typical process for a professional ESG reporting engagement – whether the organisation is establishing an ESG reporting capability or enhancing and formalising an existing reporting process.

Step 1 — ESG Assessment and Baseline Establishment

The first step in any successful ESG reporting initiative is to understand the starting point. This involves taking stock of current ESG data collection systems, policies, and reporting; comparing current practices with those of other companies and industry standards; and assessing the gap between current reporting capability and the chosen reporting framework.

- For organisations at an early stage of building ESG reporting capability, this often means that data systems have been established to support operational management rather than external reporting. So the information is there, but not in a form suitable for credible, auditable reporting.

- Recognising these gaps while there's time to address them, rather than waiting until the first reporting deadline, is the most critical part of the preparation.

Step 2 — Materiality Analysis

The materiality analysis is the North Star for all decisions that follow in the ESG reporting process: which ESG topics are relevant and financially material to the business, and therefore which should be prioritised for measurement, management and reporting.

- For companies reporting under ASRS and ISSB, the concept is financial materiality - whether the ESG topic could reasonably be expected to impact the entity's cash flows, access to capital or cost of capital.

- For companies reporting under GRI as well, the concept is double materiality - the impact on the company's finances and the impact of the company on people and the environment.

- The materiality analysis should be undertaken in a process that includes stakeholder consultation, research into industry risks, and management assessment, and the process should be documented in a way that shows auditors and regulators that the scope of disclosure is justified.

Step 3 — Data Collection and Quality Management

The strength of an ESG reporting output is only as strong as the underlying data – and data collection systems are the most challenging of the operational aspects of ESG reporting capability building.

- Emissions data (Scope 1, 2, 3): usually spread across energy bills, fleet records, travel systems and supplier data, so a data collection plan is needed to ensure all sources are accounted for, with a documented methodology and version-controlled calculations.

- HR data for social reporting - headcount, injuries, turnover, pay equity - must be pulled from HR systems and reconciled with payroll.

- For Scope 3 emissions, supplier engagement and spend-based calculations must be developed to provide estimates that are fit for external disclosure - a much higher bar than most companies have used in the past.

Step 4 — Framework Alignment and Metric Calculation

Once data has been gathered and verified, the framework alignment step involves aligning the entity’s ESG disclosures with the requirements of each reporting framework.

- For ASRS: covering the four required pillars (governance, strategy, risk management and targets and metrics) with the necessary level of detail.

- For GRI reporting: addressing the required disclosures for each material topic identified in the materiality assessment.

- For TCFD-compliant reporting: completing the 11 recommended disclosures in the four areas.

- At this point, ESG metrics and calculations (such as greenhouse gas emissions (Scopes 1, 2, and 3), energy intensity ratios, safety performance metrics, and governance metrics) need to be calculated using documented methodologies in accordance with recognised standards and undergo internal quality assurance review.

Step 5 — Report Preparation and Stakeholder Communication

The last step is the preparation and communication of the ESG reporting product – an integrated annual report, a standalone sustainability report, a CDP submission, or a combination – to the target audience.

- The preparation of a high-quality ESG report demands not only the collection and reporting of reliable quantitative information but also the inclusion of engaging and authentic narrative that outlines the organisation's strategy for sustainable development, highlights where performance has not met targets, and outlines a credible improvement plan.

- The report needs to be checked for consistency - that the ESG disclosures are consistent with information contained in the financial statements, directors' report and investor presentations.

- For organisations required to assure their ESG reports under ASRS, they must be prepared to a standard that will withstand scrutiny by an independent assurer.

09Key Challenges in ESG Reporting

Incomplete data collection systems is the most basic, and most frequent, challenge. Operational technology systems are often designed for financial, compliance and efficiency reasons; not for sustainability reporting.

- Energy data might be in several systems across multiple sites, with different data-collection methods; fleet emissions data might be in a logistics system that doesn't export data in a format that can be used to calculate GHG emissions.

- The cost of new capital expenditure to create integrated ESG data systems, and the time to build a data series that can be used to provide useful trend analyses, is substantial and often underestimated until the first reporting deadline.

- The absence of standardised ESG metrics across different industries also complicates matters. Although ASRS and GRI offer detailed guidance, the methods used to calculate industry-specific metrics differ, and there is little consistency between companies even within a single industry.

The Scope 3 Measurement Challenge

The challenge of measuring Scope 3 emissions is especially important as it is technically complex and has significant commercial implications. Scope 3 emissions span 15 categories of the value chain, are based on data from thousands of suppliers and customers, and rely on estimation methods with high uncertainty.

- Primary data from suppliers - the most reliable data source for Category 1 calculations - is often not available, and must be estimated using spend-based or industry average proxies, with significant uncertainty.

- Data collection for Scope 3 involves procurement, supply chain and customer engagement teams that are not used to participating in data collection.

Evolving Requirements and Governance Gaps

The regulatory environment is evolving, which adds urgency and complexity: standards are still evolving, guidance documents are regularly updated, and there are significant differences in the interpretation of requirements among companies, auditors, and regulators.

- Lack of robust ESG governance - ownership, accountability and oversight by the board and executive - means that many ESG reporting processes are technically sound but operationally vulnerable.

- Programmes that rely on a few people, without the processes and governance structures to ensure quality is maintained over time, are especially vulnerable to staff and organisational changes.

10Our ESG Reporting Process

Why a Structured Engagement Process Matters

An ESG reporting engagement process that is structured and well-managed underpins high-quality, auditable sustainability disclosures. The following process is typical of a best-practice professional ESG reporting engagement, from the initial assessment to the final report and disclosure package.

- The process spans the entire process from assessing the current state through to materiality, data collection design, framework mapping, report drafting, assurance and lodgement.

- The process is iterative, and each stage depends on the inputs from the prior stage.

Table 2: ESG Reporting Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — ESG Assessment | Conduct current state assessment; inventory existing data, policies, and disclosures; benchmark against peer practice and framework requirements. | Current ESG reports; sustainability policies; data system documentation. | ESG maturity assessment; gap analysis against target framework requirements. |

Step 2 — Materiality Analysis | Conduct stakeholder engagement; identify and prioritise material ESG topics; document materiality rationale under applicable standard (financial and/or double materiality). | Stakeholder input; industry risk data; regulatory guidance; management interviews. | Materiality matrix; documented rationale for disclosure scope. |

Step 3 — Data Collection Design | Design data collection templates; establish calculation methodologies; identify data owners; build Scope 1, 2, and 3 collection protocols. | GHG Protocol; GRI standards; ASRS requirements; operational data sources. | Data collection templates; methodology guide; Scope 3 category assessment. |

Step 4 — Data Gathering and Validation | Collect energy, emissions, social, and governance data from all relevant sources; validate against source records; address gaps with documented estimation methodology. | Energy invoices; HR systems; fleet data; supplier data; governance policies. | Validated ESG dataset; data quality log; estimation methodology documentation. |

Step 5 — Framework Mapping and Metric Calculation | Map collected data to disclosure requirements of each applicable framework; calculate emissions, ratios, and performance indicators. | Validated dataset; GHG Protocol; ASRS / GRI disclosure requirements. | Calculated metrics; framework alignment map; GHG inventory. |

Step 6 — Report Drafting | Prepare narrative and quantitative disclosures aligned with each framework; draft the ESG report or the sustainability section of the annual report. | All calculated metrics; materiality matrix; management commentary. | Draft ESG report / sustainability disclosures for management review. |

Step 7 — Assurance Preparation and Review | Prepare supporting documentation for assurance provider; coordinate with external assurance team; address queries. | Draft report; calculation workpapers; methodology documentation. | Assurance-ready disclosure package; responded to assurance queries. |

Step 8 — Final Report and Lodgement | Finalise and issue report; lodge mandatory disclosures with ASIC where required; distribute to stakeholders. | Finalised disclosures; assurance statement; management sign-off. | Published ESG / sustainability report; ASIC lodgement (where applicable). |

11 ESG Reporting by Industry and Situation

Why Industry Context Shapes ESG Reporting Priorities

The ESG issues, metrics, and frameworks most relevant to a company are highly dependent on the industry, as material sustainability risks and opportunities differ across industries. The table below outlines the main ESG and framework priorities for the major Australian industry sectors.

- Sector-specific frameworks and standards - such as GRESB for real estate, APRA CPG 229 for financial services, and TNFD for nature-dependent industries - offer further detail to complement the universal standards.

- Knowing the sector-specific materiality is critical for practitioners and companies as they plan their reporting.

Table 3: ESG Reporting Priorities by Industry

Industry | Primary E Focus | Primary S Focus | Primary G Focus | Key Framework Priorities |

|---|---|---|---|---|

Resources and Mining | Scope 1 and 3 emissions; water use; land rehabilitation; tailings management | Indigenous community engagement; occupational health and safety; labour practices | Board independence; resource project approvals; anti-corruption | ASRS (mandatory); TCFD; GRI Mining Sector Standard; CDP |

Financial Services | Financed emissions (Scope 3 Cat. 15); climate risk in loan portfolio; green product development | Financial inclusion; responsible lending; employee diversity | Board risk oversight; executive pay; cyber governance | ASRS (mandatory for large); APRA CPG 229; TCFD; GRI |

Real Estate and Construction | Scope 1 and 2 emissions; building energy efficiency; green building certification; embodied carbon | Worker safety in construction; affordable housing; tenant wellbeing | Asset-level climate risk disclosure; development governance | ASRS; TCFD; GRI; GRESB (real estate benchmarking) |

Retail and Consumer Goods | Scope 3 Category 1 (supply chain emissions); packaging waste; circular economy | Supply chain labour standards; modern slavery; product safety | Board diversity; supplier code of conduct; anti-corruption | Modern Slavery Act; GRI; CDP Supply Chain; ASRS (if large) |

Technology and SaaS | Scope 2 (data centre energy); hardware end-of-life; Scope 3 Category 11 (product use) | Employee diversity; mental health; data privacy and security | Board tech expertise; cyber risk governance; executive compensation | ASRS; GRI; ISO 27001 (data governance); TCFD |

Agribusiness and Food | Land use change; water consumption; Scope 3 (agricultural emissions in supply chain); biodiversity | Farmer livelihoods; food security; worker welfare | Supply chain traceability; food safety governance; animal welfare | ASRS; GRI; TNFD (nature); CDP Water; Modern Slavery Act |

12 Indicative Timeline and Frequently Asked Questions

Planning Around Realistic Timelines

For finance and sustainability professionals responsible for reporting cycles and compliance deadlines, it’s important to know how long to expect to spend on ESG reporting projects. The scope, complexity, and timeframe depend on the type of reporting, the quality of the data systems, and the regulatory requirements.

Table 4: Indicative ESG Reporting Engagement Timelines

Engagement Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

ESG assessment and gap analysis | 2–4 weeks | Company size; existing data availability; number of sites. | Foundational step for all subsequent reporting work. |

First-year ESG / sustainability report (standard) | 2–3 months | Materiality process; data collection system maturity; framework scope. | Longer where data systems require significant development. |

ASRS-compliant climate disclosure (large entity) | 3–5 months (initial year) | Scope 3 readiness; scenario analysis development; assurance preparation. | Subsequent years materially faster once systems are established. |

Annual ESG report (established program) | 6–8 weeks | Data collection efficiency; year-on-year change in metrics or disclosures. | Efficiency improves significantly with each reporting cycle. |

ESG materiality assessment only | 3–5 weeks | Stakeholder engagement scope; industry complexity. | Standalone engagement or component of first-year program. |

Is ESG reporting mandatory in Australia?

ESG reporting in Australia is rapidly transitioning from voluntary to mandatory. The Australian Sustainability Reporting Standards (ASRS) mandate climate-related financial disclosures for large businesses and listed entities, on a staggered basis with Group 1 entities (the largest) first.

- Modern slavery disclosures are already mandatory for entities with an annual turnover of $100 million or more under the Modern Slavery Act 2018.

- The Workplace Gender Equality Act requires private sector employers with 100 or more employees to report on gender equality.

- Mandatory climate reporting is coming - and those companies that build their reporting capability in the lead up to their first reporting year will have a smoother transition.

Do ESG factors affect valuation?

Yes – and the evidence is growing and wide. ESG factors impact valuation in several ways.

- Weighted average cost of capital (WACC): lower for firms with good ESG performance, due to lower equity risk premium and access to sustainable finance.

- Risk perception: lower, leading to a lower discount on cash flows.

- Sustainability of future cash flows: greater, lowering regulatory, operational and reputational risks.

- Reputation: higher, leading to higher prices and loyalty.

- Good ESG performance can add to enterprise value, and poor ESG performance can lead to higher discounts on value - and the link between ESG and financial performance is more direct and more immediate than many management teams realise until they are faced with a crisis.

Which ESG framework should we use?

The choice of ESG reporting frameworks depends on the company’s size, listed status, regulatory requirements, investor profile, and material ESG issues.

- For Australian companies with mandatory climate reporting obligations, ASRS (and therefore ISSB/TCFD) compliance is required.

- For those companies that want to go beyond climate and provide comprehensive sustainability reporting, the Global Reporting Initiative (GRI) offers the most comprehensive and recognised framework for the full ESG spectrum.

- For companies in particular sectors, such as real estate (GRESB) or financial services (APRA CPG 229), or with substantial supply chain carbon exposure (CDP supply chain), industry-specific frameworks add detail.

- Most advanced reporters use multiple frameworks, with compliance with mandatory regulatory frameworks as the starting point, and the addition of other voluntary frameworks to address the specific needs of stakeholders.

13Challenges and Lessons Learned

The Infrastructure Investment Imperative

The most common lesson from companies that have successfully transitioned from voluntary ESG reporting to mandatory, assured sustainability reporting is the need for infrastructure investment. Gaps in data collection systems cannot be addressed in the last months before you have to file a mandatory report – it is a multi-year infrastructure problem.

- Organisations that used their first voluntary ESG report as a wake-up call to identify and close data gaps, and to use the reporting process as a diagnostic exercise to improve capabilities, were well prepared for mandatory reporting.

- The takeaway: begin to develop data collection systems now, even if you have years before you are required to report. Your investment will snowball rather than force you to play catch-up in a short time.

The Scope 3 Programme Lesson

The Scope 3 emissions challenge is worth a separate mention, as it is the most technically challenging and commercially significant component of the shift to comprehensive ESG reporting.

- For most organisations - especially those in financial services, retail and professional services - Scope 3 emissions far exceed Scope 1 and 2 emissions combined, and are the main way investors view climate transition risk.

- Those companies that are ahead of the pack have begun their Scope 3 programmes early - experimenting with collection methods with their largest suppliers, working with their procurement teams to gather data, and relying on industry average emissions factors as a starting point, moving to primary data over time and through multiple reporting cycles.

- For practical purposes, it is too late to start measuring Scope 3 once it becomes mandatory.

The Governance Lesson

ESG reporting initiatives that are led by a small sustainability team, without board sponsorship, executive ownership, or integration with the company’s planning and financial reporting cycles, are always weak – they may produce technically proficient reports,. Still, they lack the organisational clout to drive operational changes that would make the reports reflect performance improvements.

- The companies with the most authentic ESG reporting are those in which the CFO is responsible for climate disclosure and the financial statements.

- Where the board is presented quarterly reports on ESG performance alongside financial performance, where executive remuneration is explicitly tied to the delivery of material ESG performance targets.

- This governance structure is not only best practice but, under ASRS, a disclosure requirement.

14Conclusion and Actionable Insights

Why ESG Reporting Matters

ESG reporting is increasingly critical for corporate transparency and long-term value creation in Australia, and this will only accelerate as regulatory requirements for ESG disclosure grow, investor expectations for ESG performance increase, and the business implications of ESG performance are increasingly reflected in the capital markets.

- ESG reporting enables companies to communicate their sustainability performance, manage risks and enhance access to capital - but only if the reporting is reliable, the data is accurate, and the governance practices that generate the data are integrated into the organisation's business model.

- Those organisations that are taking the time to develop ESG reporting capability now are setting themselves up for a competitive advantage that will grow over time.

For Companies Beginning Their ESG Reporting Journey

The most practical advice is to begin with the materiality assessment – not the report. Knowing which ESG topics are material to your company, its shareholders, and regulators is the compass that will guide you in building data collection and processing capabilities, establishing governance processes, and directing management effort.

- It's far less useful - and less credible - to have a report that covers all the possible ESG topics, but with a light touch, than to have a report that covers the material topics with rigour, depth and an acknowledgement of how and where to improve.

- Start with the materiality analysis, use that to guide the data investment, and then the report.

Five Actionable Steps for Practitioners

For entry and mid-level professionals looking to gain expertise in ESG reporting, the following areas offer a development roadmap.

- Build familiarity with the main frameworks - ASRS, ISSB / IFRS S1 and S2, TCFD, and GRI - and their inter-relationships, disclosure requirements and appropriate use cases.

- Develop technical skills in greenhouse gas (Scope 1, 2, and 3) emissions measurement - GHG Protocol, choice of emissions factors and particular issues in collecting and estimating Scope 3 emissions.

- Build proficiency in the process of materiality assessment - both financial materiality (ASRS and ISSB) and double materiality (GRI) - because materiality analysis is the starting point of any ESG reporting practice.

- Build knowledge of the value link between ESG and financial performance - that is, how ESG factors impact the cost of capital (WACC), investor risk, long-term cash-flow sustainability, brand value and reputation.

- Get involved in the assurance aspect of ESG reporting - because as limited and reasonable assurance services grow under ASRS, the skill to comprehend and support the assurance process will be one of the most sought after and valuable skills in the ESG reporting discipline.

Our ESG reporting advisory services help organisations across the full gamut of sustainability reporting: ESG assessment, materiality, framework alignment, emissions calculations, report preparation, and support for the assurance process. The services are based on the regulatory framework of ASRS and the needs of informed investors – and deliver disclosures that are authentic, defensible and fit for purpose. ESG reporting is not a chore; it is a mirror that reflects an organisation’s true values, practices, and priorities. Such transparency is the key to sustainable value. |