Purchase Price Allocation (PPA) Valuation Guide in Australia

Table of Contents

- 01 Introduction

- 02 What Is Purchase Price Allocation?

- 03 Why Do Clients Need PPA Valuation?

- 04 Key Components of a PPA Exercise

- 05 Key Valuation Approaches Used in PPA

- 06 Key Drivers That Affect PPA Valuation

- 07 Common Mistakes in PPA Valuation

- 08Five Key Steps: The PPA Engagement Process

- 09 Valuation Approaches by Asset Class

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is Purchase Price Allocation Valuation in Australia?

- 03 Why Do Clients Need PPA Valuation?

- 04 Key Components of a PPA Exercise

- 05 Key Valuation Approaches Used in PPA

- 06 Key Drivers That Affect PPA Valuation

- 07 Common Mistakes in PPA Valuation

- 08 Five Key Steps: The PPA Engagement Process

- 09 Valuation Approaches by Asset Class

- 10Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

What is Purchase Price Allocation

Purchase Price Allocation (PPA) is an accounting process essential to businesses undertaking an acquisition. It is an intersection between M&A advice, accounting standards, and financial reporting – and one of the most complex tasks that a CFO, financial controller or external auditor will perform in the post-acquisition period.

- When a company is acquired, the purchase price paid by the acquiring company is not simply the value of the acquired company's assets as recorded on its books, but also the strategic premium for the acquired company's future earnings, market share, human capital, technology, and customer relationships.

- PPA is the accounting process that formalises that premium - turning a single transaction into a bunch of separately valued assets and liabilities that can be identified, reported, and, in the case of intangibles with finite lives, amortised.

The Analytical and Reporting Significance of PPA

PPA involves allocating the total consideration paid to acquire an entity to the acquired assets and assumed liabilities at their fair values. This is not a mechanical accounting process, but a significant analytical one with long-term financial reporting ramifications.

- It affects the acquirer's earnings through the amortisation of the recorded intangibles.

- It impacts the acquirer's balance sheet by recognising assets and liabilities at the acquisition date.

- It affects ongoing impairment testing requirements through the remaining balance of goodwill (after allocating all identifiable assets and liabilities).

- So the PPA process leads to financial reporting consequences that affect the acquisition in every subsequent period.

Who This Guide Is For

PPA is a key element of financial reporting, audit and transparency in mergers and acquisitions. The PPA requirement can be a significant operational and governance challenge for companies undertaking their first acquisition, requiring coordination between the finance team, external auditor, legal advisers, and specialist valuation advisers within the short timeframe of the post-acquisition financial close process.

- Knowledge of PPA - what it is, how it works, and how to produce a high-quality outcome - is increasingly a vital professional skill for corporate finance, accounting, and M&A advisers.

- This book provides that knowledge in a tangible way for junior and mid-level professionals, and for those looking to join the profession.

A successful Purchase Price Allocation (PPA) is not a compliance-driven accounting project; it is the final financial roadmap for what was bought and for how much. Every subsequent period after the acquisition is reported based on the PPA prepared on the acquisition date. |

02 What Is Purchase Price Allocation Valuation in Australia?

Definition and Core Concept

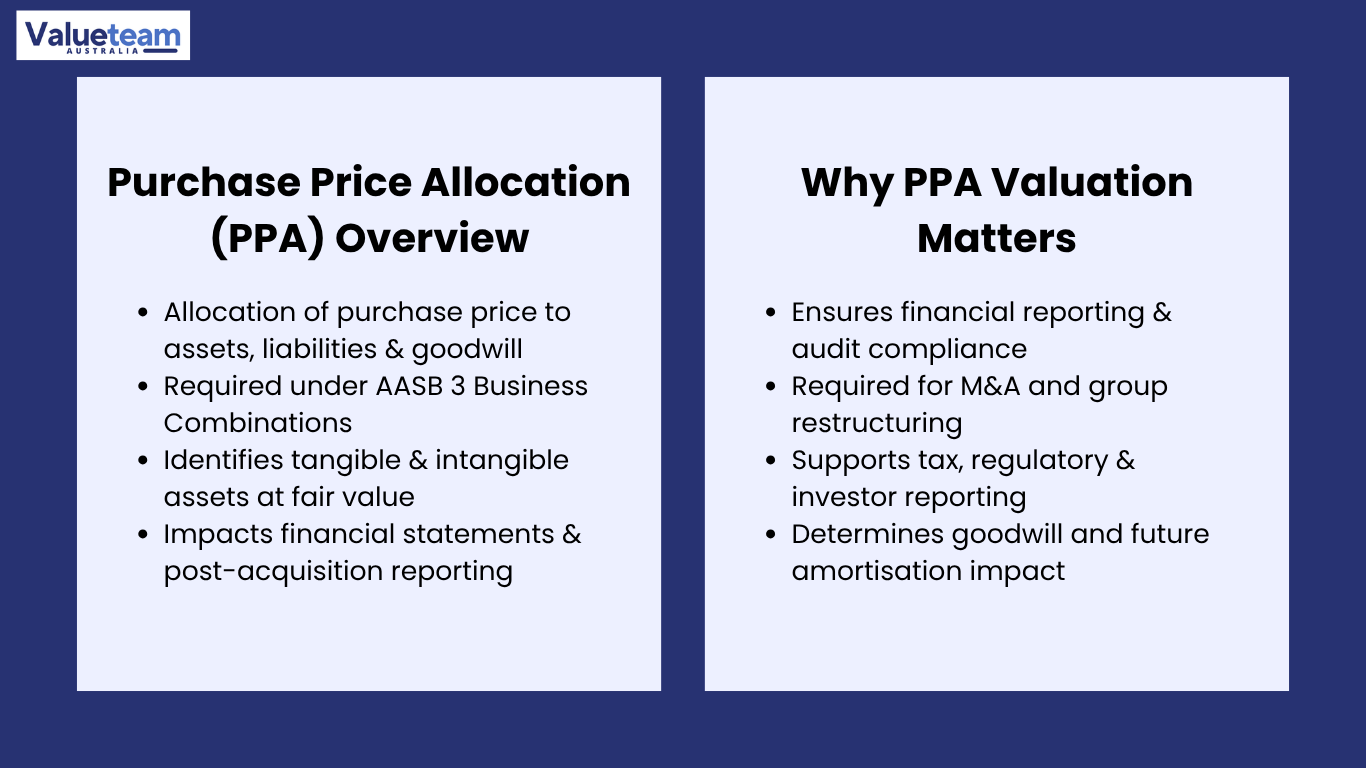

Purchase Price Allocation is the allocation of the purchase price of a business to identifiable tangible assets, identifiable intangible assets, liabilities assumed and goodwill. In Australia, this is done in accordance with AASB 3 Business Combinations, the accounting standard that addresses the accounting for a business combination in the acquirer’s financial statements.

- Under AASB 3 (which is essentially identical to the international standard IFRS 3), the acquirer is required to identify and measure all the acquired business's assets and liabilities at their fair values at the date of acquisition - even if they were not recognised on the target business's pre-acquisition balance sheet.

- This is why the PPA exercise is so tricky: most of the most important assets of a business today - customer relationships, brand, technology platforms, assembled workforce - are not recognised on the balance sheet under historical cost accounting, but must be identified, valued and recognised at fair value in the PPA.

The Conceptual Logic of PPA

The underlying logic of PPA is simple: the buyer has paid a particular price for a combination of economic assets and liabilities, and this price must be reflected in the financial statements to reflect the purchase.

- If a business is purchased for $200 million and the net tangible assets are only $50 million, the remaining $150 million must be accounted for.

- Some of the $150 million may reflect the value of customer relationships that generate steady, ongoing cash flows. Some may represent a unique technology platform or a well-known brand that enables pricing power.

- Anything left over - after all identifiable assets and liabilities have been valued at fair value - is goodwill, which represents the elements of the acquisition value that are not separately identified and measured: synergies, workforce in place, future growth opportunities and the business rationale for the premium paid.

Downstream Financial Statement Implications

The purpose of PPA is to report the acquisition at fair value for financial reporting purposes. This goal has some significant implications for all future periods.

- The balance sheet following the acquisition will usually not be a simple amalgamation of the two pre-acquisition balance sheets - new intangible assets will be recognised, assets and liabilities will be revalued at fair value, and there will be a goodwill balance equal to the purchase price less the fair value of the net assets acquired.

- The income statement will reflect the amortisation of finite-lived intangibles: customer relationships are often amortised over 3-12 years, technology over 3-7 years and brands over their expected useful life.

- These flow-on effects on the financial statements are important for those advising on and reviewing the results of a PPA.

03Why Do Clients Need PPA Valuation?

The circumstances that require PPA valuation are well documented in accounting standards and audit requirements – but it’s more than just a compliance issue. Any practitioner in this field needs to understand the full purpose of PPA and what the different parties to an acquisition are seeking to achieve.

Financial Reporting and Audit Compliance

The statutory financial reporting standard (AASB 3) is the primary driver of PPA demand. A PPA must be prepared for all business combinations where the acquirer obtains control of another entity, and the results must be reflected in the statutory financial statements for the period in which the business combination was effected.

- Under AASB 3, the measurement period for determining the fair values is up to 12 months from the date of acquisition, with provisional amounts adjusted to final fair values.

- The PPA market is robust at year-end, when audit requirements kick in for companies that have undertaken significant or complex acquisitions.

- The external auditor needs to determine whether the fair value accounting in the PPA is complete and reasonable, including whether all intangible assets have been identified, the valuation bases are appropriate, and the assumptions made are reasonable.

- A well-documented and professional PPA report is a critical component of any audited acquisition, as compliance with accounting standards (and the audit opinion based on it) depends on the quality of this documentation.

Mergers, Acquisitions and Group Restructuring

PPA is a key component of mergers, acquisitions, group restructurings, and the annual reporting cycle. Under AASB 3 acquisition accounting, all assets and liabilities acquired are initially recognised at fair value at the date of acquisition, and the PPA is the source of the fair values used in the initial recognition entries.

- For companies with multiple acquisitions in a financial year, or those in industries with high M&A activity, PPA is a regular engagement handled as part of the annual financial close.

- Group restructurings (mergers, demergers, internal restructurings, and step acquisitions) can create PPA requirements that are not as apparent as an acquisition but are equally complex from an accounting and valuation perspective.

- Business combinations between entities under common control are generally excluded from AASB 3, but the line between common control and third-party transactions is not always clear-cut.

Tax, Regulatory and Investor Reporting

The importance of PPA goes beyond the financial statements. The PPA exercise feeds into several downstream requirements for tax, regulatory and investor reporting.

- The PPA must consider the allocation of the purchase price between taxable and non-taxable assets, cost bases and deferred tax assets and liabilities that result from differences between the fair values and the tax cost bases of the assets acquired.

- Multinational structures can also be involved, with the PPA potentially required to meet the requirements of several tax and accounting systems.

- For public companies, the accuracy and completeness of the PPA exercise are essential for regulatory reporting to stock exchanges and other regulators, investor announcements post-acquisition, and board transparency about the assets and value drivers acquired.

04 Key Components of a PPA Exercise

To understand any PPA exercise, it is important to be familiar with the four components of a PPA: identifiable tangible assets, identifiable intangible assets, liabilities assumed, and goodwill. Each component has its own identification, measurement and accounting treatment under AASB 3.

Identifiable Tangible Assets

The identifiable tangible assets in a PPA are the business’s physical assets acquired, which are remeasured to their fair values at the date of acquisition. Property, plant and equipment (PPE) is usually the most significant tangible asset category for businesses with significant physical assets.

- The fair value of PPE may be significantly different from book value (which may reflect many years of depreciation) and market value (which is based on the highest and best use, not current use).

- Plant and equipment need to be tested for physical and functional obsolescence. A manufacturing line installed five years ago may have a high book value but a low fair value if the technology used in the line has improved significantly.

- Finished goods are measured at net realisable value; raw materials at replacement cost, as opposed to the lower of cost and net realisable value in the historical financial statements of the target.

- Cash and receivables are measured at fair value with credit risk considered. The collectability of receivables at the time of the acquisition can sometimes expose problems not apparent during pre-acquisition due diligence.

Identifiable Intangible Assets

Identification and valuation of identifiable intangible assets is the most complex and important part of most PPA analyses. Under AASB 3, an intangible asset must be recognised separately from goodwill if it meets either the contractual-legal criterion or the separability criterion. So many assets that are not recognised on the target’s balance sheet need to be identified and valued.

- Customer relationships are a very common and valuable intangible in business-to-business and service industries. The retention rate determines the value of the revenue stream and the period over which the relationship is expected to be economically beneficial.

- Brands and trademarks - the reputation of the acquired business, reflecting the customer preference and loyalty the brand engenders. Often valued using the relief from royalty approach.

- Computer systems and software - especially proprietary systems that generate revenue, using a combination of the income approach (for revenue-generating systems) and the cost approach (for internally developed systems).

- Contracts and order backlog - the value of specific contracts as at the date of sale, providing certainty of future cash flows.

- Covenants not to compete, licences, and permits - completing the usual list of intangible assets, with each having its own valuation techniques and useful lives.

Liabilities Assumed

Liabilities acquired in the business combination must also be measured at fair value at the date of the acquisition – regardless of whether they were previously recognised in the financial statements of the acquired business.

- Simple liabilities such as borrowings, trade payables, and employee entitlements are generally easy to determine. Debt instruments with non-market interest rates will not have a face value of 100% and should be discounted.

- Contingent liabilities must be recognised in the PPA if they are a present obligation arising from a past event and the fair value can be measured reliably - even if an outflow is not probable. This is lower than the IAS 37 threshold for standalone financial statements.

- The recognition of contingent liabilities not previously recognised by the target is a frequent source of liability recognition in PPAs.

Goodwill

Goodwill is the residual – the amount by which the purchase consideration (including the fair value of any previously held interests and non-controlling interests) exceeds the net fair value of all the identifiable assets acquired, and liabilities assumed. Goodwill is not amortised but is subject to impairment testing each year, under AASB 3 and AASB 136.

- As a result, the amount of goodwill is dependent on the identification and measurement of intangible assets in the PPA.

- If the PPA does not recognise and value all significant intangible assets, the goodwill balance will be overstated due to the overstatement of the unallocated premium and understatement of the finite-life amortisable intangibles that should have been recognised.

- Goodwill is supposed to capture the synergies from the acquisition, the workforce, the growth opportunities and the control premium benefits. As a result, its accounting quality is only as good as the PPA analysis.

05Key Valuation Approaches Used in PPA

The income approach, market approach and cost approach, the three approaches to valuation in PPA, are applied to individual assets, not groups of assets. The method chosen for each asset must be the most appropriate for that asset, and the selection and application of the valuation method are among the key auditor focus points for PPA.

Income Approach

The income approach is the most common in PPAs because most intangible assets are valued based on the economic benefits they are expected to generate, and the present value of those future benefits is the conceptually most appropriate definition of fair value.

- Discounted cash flow (DCF) method: used for assets for which a series of directly attributable cash flows can be estimated and discounted to present value.

- Multi-period excess earnings method (MPEEM): the most common variant of the income approach for the key intangible in a PPA, usually customer relationships. This values the cash flows attributable to the acquired customer base, net of the returns attributable to all other contributing assets (the contributory asset charges).

- Relief-from-royalty approach: an income approach that values an intangible based on the royalties that the entity would have to pay if it did not own the intangible. It is the most frequently used approach for brands and trademarks, and is also commonly used for technology assets for which royalty benchmarking data is available.

Market Approach

The market approach uses comparable market transaction data to support or test the fair value conclusions reached under the income approach. It provides the empirical basis that grounds the methodology.

- Licensing royalty rate benchmarks from licensing databases provide empirical evidence for the royalty rate used in the relief-from-royalty analysis.

- Similar acquisitions of comparable businesses offer evidence of transaction multiples for particular asset types, which can be used to verify the reasonableness of income approach results.

- Royalty licensing transactions for similar intangible assets - particularly those involving brand and technology royalties - provide evidence of the price at which similar assets are sold between unrelated parties.

- The major issue with the market approach for PPAs is the lack of directly comparable information. M&A deals are generally structured around portfolios of assets, and the prices paid for specific intangible assets are not publicly available in sufficient detail to be compared.

Cost Approach

The cost approach values an intangible asset as the cost of replacing it with an asset of equal utility. It is appropriate for assets whose value is more appropriately measured by replacement cost rather than the income approach.

- It is most often used to value internally developed software and technology platforms, proprietary databases and data management systems, and other support assets.

- The cost approach involves estimating the total cost of the asset, including time and labour costs, testing and integration costs, and the opportunity cost of time spent developing the asset.

- Critically, the cost estimate is adjusted for obsolescence: physical deterioration, functional obsolescence (technical inferiority relative to a modern equivalent), and economic obsolescence (external factors that diminish the asset's usefulness).

- The usual approach for income-producing assets is to use the income approach as the primary method and the cost approach as a complement, triangulating a defensible fair value estimate using both.

06 Key Drivers That Affect PPA Valuation

From Acquisition Rationale to Valuation Inputs

The same drivers that drive the value of each asset in a PPA also drove the price of the acquisition – but in a PPA, these drivers must be translated into quantitative inputs for each asset’s valuation model. This knowledge assists finance teams and advisers in identifying where the greatest value will be allocated, and helps management teams understand their post-acquisition financial statements.

Factors That Increase Value Attribution in a PPA

Several factors tend to increase fair value attribution for the major intangible asset classes in a PPA.

- High customer retention: a high historical retention rate for the customer base results in longer cash flows attributable to the customer relationship intangible, supporting a higher fair value and longer useful economic life for the intangible.

- High contract visibility: the percentage of future revenue contracted at the date of acquisition reduces forecast uncertainty in the MPEEM analysis and justifies a higher value by applying a lower discount rate to the first few years of cash flows.

- Brand awareness: justifies a higher royalty rate in the relief-from-royalty analysis and a longer useful life for the brand.

- Technology scalability: scalable platforms with increasing revenue and no associated costs increase earnings leverage and hence attributable cash flows.

- Cash flow predictability: for all assets, the lower the risk in projected cash flows, the lower the discount rate that should be applied, and the higher the present value of future cash flows.

Factors That Reduce Value Attribution in a PPA

The risk factors that reduce value attribution in a PPA are the same risks a prudent acquirer would have identified in its due diligence.

- High customer churn: a company with a 30% annual customer turnover will have a customer relationship intangible asset with a short useful life and a relatively low fair value.

- Uncontracted, short-term revenue: creates uncertainty beyond the near term, increasing the discount rate and the discounting of the estimated cash flows.

- Technology obsolescence: a technology platform nearing the end of its competitive life will have a short effective life and a low income approach to fair value.

- Regulatory or legal uncertainty: unresolved litigation, regulatory investigations or uncertain IP ownership results in contingent liabilities that reduce net asset values and may prevent some intangibles from being recognised at fair value.

- A lack of past success reduces confidence in the income approach estimates, typically leading to higher discount rates and lower growth rates.

Table 1: PPA Value Drivers — Impact by Asset Category

Value Driver | Asset Category Most Affected | Direction of Impact | Analytical Mechanism |

|---|---|---|---|

High customer retention rate | Customer relationships | Increases value and useful life | Extends cash flow projection period in MPEEM; reduces attrition-driven discount. |

Contracted vs uncontracted revenue | Customer relationships; order backlog | Contracted revenue increases value | Reduces projection uncertainty; supports a lower discount rate for near-term flows. |

Brand strength and market recognition | Trademarks and brands | Higher recognition increases value | Supports a higher royalty rate in relief from royalty; extends useful life. |

Technology scalability and roadmap | Software and technology | Scalable platforms increase value | Higher attributable cash flows per dollar of investment; lower obsolescence risk. |

Customer churn rate | Customer relationships | Higher churn reduces value | Shortens effective useful life; increases attrition-driven discount in MPEEM. |

Contract duration and renewal probability | Contracts; customer relationships | Shorter duration reduces value | Compresses forward cash flow visibility; increases discount rate. |

Technological obsolescence risk | Software and technology | Higher obsolescence reduces value | Shortens useful economic life; reduces income to approach fair value. |

Contingent liabilities and legal uncertainty | All categories | Reduces net asset value | Recognised liabilities reduce residual goodwill; unresolved issues increase discount. |

07Common Mistakes in PPA Valuation

Why PPA Errors Are Particularly Costly

Practitioners tell us that the errors that most commonly jeopardise the quality and auditability of PPA exercises fall into a handful of failure modes. Companies that are implementing the PPA process need to understand these failure modes as much as practitioners conducting the analysis – the consequences of a poorly executed PPA process flow through several reporting periods via amortisation charges, impairment testing on an incorrect asset base, and the need to restate if errors are detected after the measurement period has ended.

Failure to Identify All Intangible Assets

The most significant failure in PPA practice is the failure to identify all intangible assets. The acquirer must recognise all identifiable intangible assets that meet the contractual-legal or separability criteria – not just those expected at the time of the acquisition.

- Technology, professional services and consumer businesses often have intangible assets - assembled workforces, profitable contracts, non-compete agreements, domain names, regulatory approvals - that are not front-of-mind for the acquisition, but which must be identified and valued.

- Failure to identify and recognise these assets overstates the goodwill balance, understates the balance of amortisable intangibles and understates the effect on future earnings of amortising acquisition-related intangibles.

- If an auditor identifies an omission in the PPA audit, it will be required to be corrected - often with a tight reporting deadline, creating pressure and cost in a complex process.

Incorrect Useful Life Assumptions

The second most prevalent quality issue in PPAs concerns incorrect useful-life assumptions. The useful economic life of each intangible is used to calculate the cash flow projection period in the income approach valuation model and the amortisation charge in the financial statements.

- Overestimating useful life reduces the annual amortisation expense and increases reported earnings in future periods. Underestimating has the opposite effect. They both misstate earnings in all post-acquisition periods.

- Useful life estimation must be based on empirical evidence: past customer retention patterns for customer relationships; technology roadmap and competitive intelligence for software and technology assets; past brand investment and market parameters for trademarks.

- Most importantly, the useful life used in the valuation model (where it affects the cash flow projection period) must be the same as the useful life used in the accounting treatment (where it affects the amortisation period).

Inconsistent Financial Projections Across Valuation Models

Inconsistent or volatile financial projections across valuation models are a recurring audit issue in PPA valuations.

- If the DCF model used to value the consideration paid and the MPEEM model used to value the customer relationships are based on different revenue and margin projections, inconsistencies will emerge that auditors will challenge.

- The PPA valuation models must be based on consistent management assumptions (adapted to market participant assumptions as per the fair value standard) rather than entity-specific or model-specific assumptions.

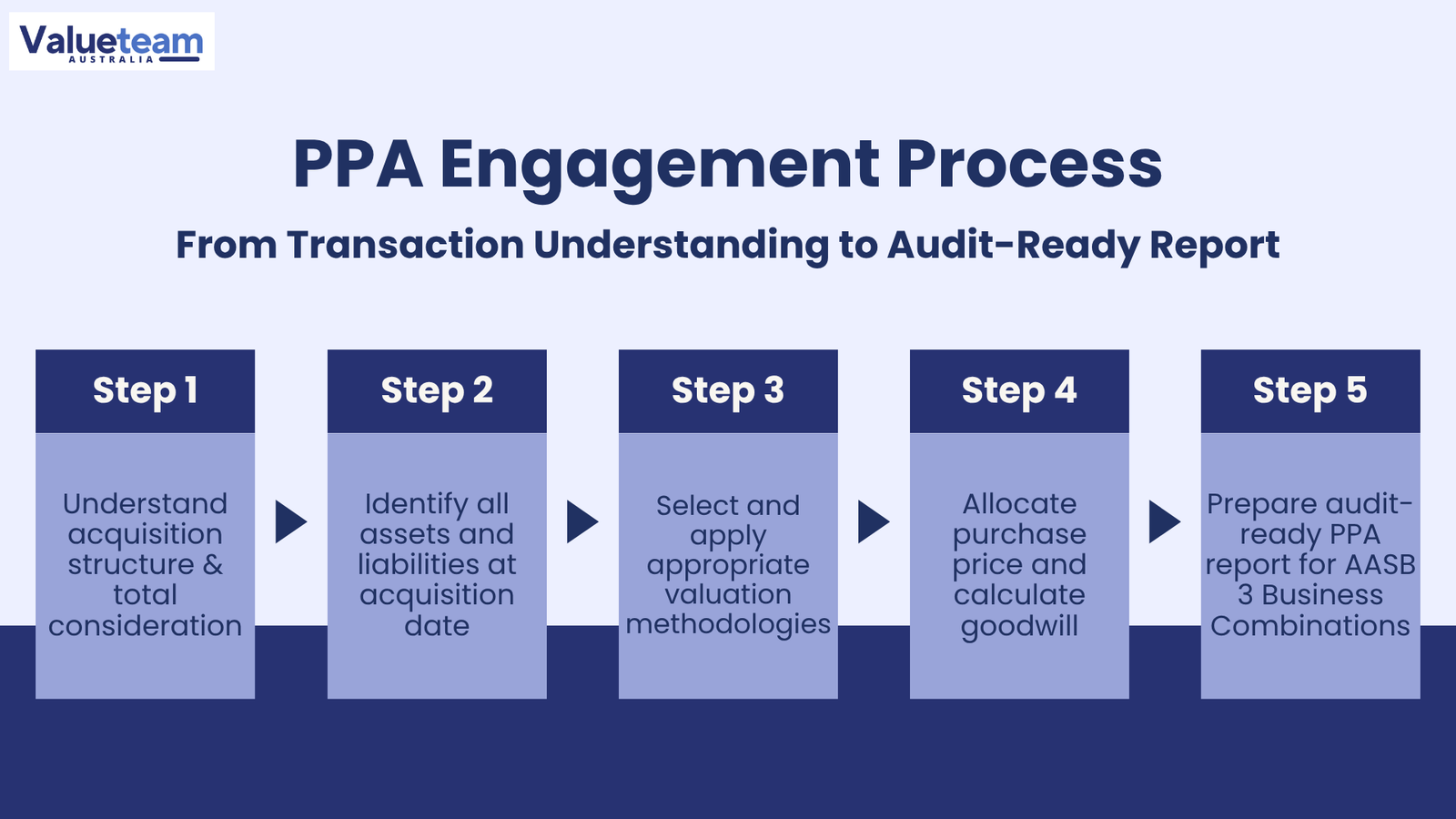

08Five Key Steps: The PPA Engagement Process

The PPA engagement process can be broken down into five key steps, from understanding the transaction to the audit-ready report. Each step is dependent on the success of the previous one: the better the output of each step, the better the next; and the urgency of post-acquisition reporting requires careful preparation at each step.

Step 1 — Understand Acquisition Structure and Consideration

The PPA does not start with valuation models; it starts with understanding the transaction. This involves a careful analysis of the share purchase agreement (SPA) and the transaction.

- The form of consideration must be defined: cash, scrip, deferred, contingent or a combination, and the fair value of each component.

- The nature of the transaction must be established: whether it is a business combination (as defined in AASB 3) or an asset acquisition, which has different accounting treatment.

- The acquisition date must be established; it serves as the measurement date for all assets and liabilities of the PPA.

- The total consideration to be allocated must be determined, including the fair value of any contingent consideration, any existing ownership interests in the target, and any non-controlling interests.

- This also establishes the scope of the PPA: the entities and assets involved, as well as the reporting and timing requirements.

Step 2 — Identify All Assets and Liabilities

The identification phase is the most complex phase of the PPA and the phase where the most errors occur. It involves the valuation team examining the acquired business and identifying all assets and liabilities as at the acquisition date (including items not on the target’s pre-acquisition balance sheet).

- The data collected in this phase - the audited financial statements and management accounts, the asset register, the customer contracts, legal agreements, the acquisition valuation model and information on contingent liabilities - provides the evidentiary support for the identification of assets and the inputs to the valuation models.

- The goal is to identify all assets and liabilities, classify them by type, match them to the appropriate valuation approach, and organise them for incorporation into a single, integrated valuation model.

Step 3 — Select and Apply Valuation Methodology

Once the asset inventory is complete, the valuation team chooses the best approach for each asset class and builds the valuation models.

- The key intangible assets - usually customer relationships valued by MPEEM and trademarks and brands valued by the relief-from-royalty method - must be populated with inputs for discount rates, royalty rates, attrition rates and useful economic life, benchmarked to comparable market data and documented to provide audit evidence.

- All models must be based on a consistent set of forecast assumptions from the perspective of a market participant, as required by AASB 13 (fair value measurement, not entity-specific synergy assumptions that drove the purchase price.

- Discount rates must reflect the risks of the assets' cash flows, not a single enterprise discount rate, which would distort the relative risk-adjusted values of the assets.

Step 4 — Allocate Purchase Price and Calculate Goodwill

Once the fair values of the identifiable assets and liabilities are determined, the PPA allocation table is built. The consideration paid is compared to the total fair value of the identifiable net assets, and the difference is allocated to goodwill.

- The allocation table must balance: all purchase consideration must be allocated to an asset, a liability, or goodwill; there should be no residual.

- Deferred tax considerations must be accounted for: the differences between the accounting fair values and the tax cost bases of the acquired assets result in deferred tax liabilities (for assets valued above their tax base) or deferred tax assets (for liabilities recognised above their tax values), which must be accounted for in the allocation table and also in the goodwill calculation.

- Calculating this can be more complex than it seems, especially when the transaction involves a sophisticated consideration structure and/or is cross-border.

Step 5 — Prepare Audit-Ready PPA Report

The last step is to prepare the PPA report – the main evidence document for the auditor to review the acquisition accounting, the supporting document for the AASB 3 financial statement disclosures, and the management reference for useful life and amortisation assumptions in subsequent reporting periods.

- A good PPA report describes the acquisition structure and consideration, the methodology and evidence used to identify each recognised asset and liability, the valuation methodology used for each asset class and the justification for its use, all key assumptions with benchmarking evidence, sensitivity analysis, the entire allocation table and the deferred tax analysis.

- The report should be prepared to the same standard as what a highly experienced AASB 3 auditor would expect in an audit (that is, the same standard as any other material accounting estimate in the financial statements).

09Valuation Approaches by Asset Class

Why Methodology Selection Is a Key Technical Judgement

PPAs value different types of assets differently, and choosing the appropriate methodology for each asset is a key technical judgement in the process. The table below lists the approaches commonly adopted in practice for each asset type, the required inputs and the common useful life ranges encountered by practitioners and auditors.

- The selection of the methodology for each asset is a key area of focus for the auditor in reviewing the PPA; it should be justified based on the asset's characteristics, the intended use of the valuation, and the available data.

- In most cases, the best practice for revenue-generating intangibles is to adopt a primary income approach methodology and triangulate the value with the cost approach or market data, if available.

Table 2: PPA Valuation Approaches by Asset Class

Asset Class | Primary Methodology | Key Inputs Required | Typical Useful Life (AASB 3) |

|---|---|---|---|

Customer relationships | Multi-period excess earnings method (MPEEM) | Attrition rate, revenue by customer cohort, contributory asset charges, discount rate. | 3–15 years based on industry and churn rate. |

Trademarks and brands | Relief from royalty method | Benchmarks of royalty rates, brand revenue, discount rate, and useful life. | Indefinite (unless there is a foreseeable limit) or 5–20 years and above. |

Software and technology platforms | Income approach (incremental cash flow) + cost approach | Revenue attributable to platform; replacement value; obsolescence value. | 3–7 years (technology); more in case of an active investment platform. |

Order backlog / in-process contracts | Income approach (direct cash flow of contracts) | Contract revenue, cost to complete, margin, and discount rate. | Duration of contracts (typically < 1 year to 3 years). |

Non-compete agreements | Income approach (with and without method) | Competition risk to revenue; likelihood of competitors’ entry; discount rate. | Term of the contract (usually 2–5 years). |

Licences and permits | Relief from royalty or cost approach | Value of regulatory licence; replacement cost; licence category royalty rate. | Term of the remaining licence or indefinite, whether renewable. |

Property, plant and equipment | Market approach (direct comparison) or cost approach | Market comparables; replacement cost; physical/functional obsolescence. | Remaining useful life per physical condition assessment. |

Goodwill (residual) | Residual — not separately valued | Total consideration less the fair values of net identifiable assets. | Not amortised; impaired annually under AASB 136. |

10Indicative Timeline and Frequently Asked Questions

Planning Around Realistic Timelines

For companies with post-acquisition reporting deadlines, knowing how long a PPA engagement is likely to take is critical in planning. While the 12-month measurement period allowed under AASB 3 may indicate a long time to complete the PPA, in reality, the first post-acquisition audit is often the most complex deliverable, and the PPA must be substantially complete before the acquisition accounting audit can be completed.

Table 3: Indicative PPA Engagement Timelines

Assignment Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

Simple acquisition (limited intangibles) | 1 week | Fullness of SPA and financial information package. | Businesses with few intangible identification requirements and asset-light. |

Standard PPA (2–4 identified intangibles) | 1–2 weeks | Quality of customer data; availability of contracts and forecasts. | The most prevalent case of SME and mid-market acquisitions. |

Complex PPA (multiple intangibles, cross-border) | 3–5 weeks | Jurisdictional complexity, number of asset classes, and audit coordination. | Public companies, complicated capital structure, and large business mergers. |

Pre-acquisition engagement (partial) | Concurrent with the transaction | Due diligence materials; deal timeline. | Considerably shortens after-close time; advisable in all acquisitions. |

Finalisation within the measurement period | Up to 12 months post-acquisition | Difficulty of provisional amounts; later information. | AASB 3 allows a 12-month measurement period for finalising provisional amounts. |

Why is PPA required? Why is PPA required?

AASB 3 Business Combinations requires PPA for all acquisitions that are a business combination – that is, when the acquirer obtains control of a business as defined by AASB 3. The standard applies to all entities that prepare general-purpose financial statements under Australian Accounting Standards, regardless of their size, listing status, or whether the acquired entity is listed or unlisted.

- The goal is to ensure the acquisition is accounted for at fair value in compliance with financial reporting standards, so that investors, creditors, and other users of the financial statements can understand what has been acquired and the value at which it was acquired.

What is the most important part of PPA?

Recognition and measurement of identifiable intangible assets is invariably the most important – and complex – part of a PPA.

- Intangibles are usually the largest component of the excess purchase price over tangible net assets, require special valuation techniques to measure, and have the most significant long-term impact on the financial statements through amortisation and impairment processes.

- A PPA that correctly identifies and values all significant intangible assets establishes a much better and more meaningful basis for financial reporting in the years following the acquisition than one that simplifies the intangible landscape by allocating all value to goodwill.

Is PPA required for every acquisition?

PPA applies to all transactions that are a business combination under AASB 3 – broadly speaking, any transaction in which the acquirer obtains control over a business, rather than an asset or group of assets that are not a business.

The line between a business combination and an asset acquisition can be blurry, and determining whether an acquisition is a business combination under AASB 3 requires careful consideration of whether the acquired entity has the inputs, processes, and outputs that constitute a business.

The treatment of asset acquisitions differs: assets and liabilities are measured at cost on a fair value basis; intangibles are not separately accounted for; and goodwill is not recognised.

An incorrect classification of a business combination as an asset acquisition is a significant accounting error that may require restating the financial statements.

11 Challenges and Lessons Learned

Challenge 1 — The Timing Problem

The timing problem is the most persistent structural issue in the PPA practice. PPA is a post-merger activity, but the underlying data – complete financial, complete customer contract files, operational and management’s assumptions about the future – are available during the due diligence period before the transaction closing.

- Once the deal closes, management is focusing on integrating the acquired entity, and the audit timeframe is driving the engagement to be completed more quickly, potentially compromising the quality of the PPA.

- Those companies that handle this challenge best consider PPA as a transaction workstream, rather than an audit service. Engaging the PPA adviser in the due diligence process, reviewing the transaction documents in the data room, and starting the initial identification and valuation work before the close of the transaction consistently deliver superior results compared to the "fire drill" often seen in poorly managed PPA processes.

Challenge 2 — Consistency Between the Acquisition Model and PPA Projections

The second common challenge relates to the consistency between the model used to support the acquisition and the models used to value the PPA assets.

- The acquirer will typically prepare a financial model to justify the acquisition, projecting revenue growth, margin expansion, and synergies to support the purchase price. The PPA uses a variant of those projections to value the acquired assets at fair value as if a market participant held them.

- The differences between these two uses of the projections - the acquisition model, which reflects the acquirer's assumptions and synergies; the PPA, which reflects market participant assumptions, not entity-specific synergies - can be a source of confusion and audit difficulty.

- CFOs and finance directors should be mindful of this difference from the start of the transaction process, and ensure the assumptions in the acquisition model are documented in sufficient detail to facilitate the preparation of market-participant-adjusted PPA projections.

Challenge 3 — The Importance of an Iterative, Collaborative Process

The third lesson is the importance of an iterative and collaborative PPA process.

- The most effective PPA engagements are not those in which the adviser hands the auditor a finished piece of work on day one - they are those in which the adviser and auditor have worked together to agree the scope of intangibles to be identified, to select the most appropriate methodology and agree the assumptions to be used, and to resolve issues before they become audit qualifications.

- Finance teams that recognise the value of this iterative process and ensure that the process is supported by starting the engagement early and facilitating communication between the valuation adviser, audit team, and internal finance team consistently deliver faster, more effective and more cost-efficient PPA engagements than those that approach the process as a series of handovers.

12 Conclusion and Actionable Insights

Why PPA Matters

PPA is one of the most significant accounting rules that apply to an acquisition, with tangible and lasting impacts on the acquirer’s financial statements, its subsequent reporting, and investors’ perception of what was actually acquired and for how much.

- It requires allocating the total consideration paid for the target to the acquired assets and liabilities at fair value - including assets that were not previously reported on the target's balance sheet.

- It involves specialised valuation techniques for each asset class and a robust, audit-proof report for external auditors, regulators, and savvy investors.

- It's a key indicator of the quality of acquisition governance within the company.

For Companies Preparing for an Acquisition

The key take-out for companies preparing for an acquisition is the importance of early engagement – before the acquisition event, rather than waiting for urgency to drive the audit.

- Early engagement allows for more thorough identification of intangible assets, improved valuation models, documented assumptions, a more efficient audit process, and reduced costs.

- The 12-month measurement period allowed by AASB 3 is a limit, not a goal. Businesses that do so are forced to make estimates that are later revised, disclose measurement period uncertainties that confuse investors, and spend money in the last few months that could have been avoided.

Five Actionable Steps for Practitioners

For early-career and mid-level professionals seeking to develop their careers in valuation, accounting, or M&A advisory, here are some actionable steps.

- Understand AASB 3 and AASB 13 (the accounting standards for business combinations and fair value measurement) as the regulatory framework in which all PPA work is undertaken.

- Build technical proficiency in all three valuation approaches: the income approach (DCF, MPEEM, relief-from-royalty); the market approach (royalty benchmarking, comparable transactions); and the cost approach (internally developed software, technology infrastructure).

- Learn to identify intangible assets - the ability to spot all assets that meet the AASB 3 recognition criteria is the most important and most distinctive skill in PPA practice.

- Understand the contributory asset model behind the MPEEM: the rationale of contributory asset charges, the build-up of the weighted average return on assets (WARA), and its link to the transaction discount rate - among the most complex and challenging areas of PPA practice.

- Look for experience in full-cycle PPA engagements, from transaction review to auditor sign-off - the ability to manage the entire process, including the auditor, is what sets PPA professionals apart from those who know the models but not the process.

Our Purchase Price Allocation (PPA) consulting services help acquirers with the process of complying with AASB 3 – from the identification and valuation of intangible assets to audit reporting and financial statement disclosure. The process starts with understanding your transaction and ends with a PPA that your auditors can trust. You can’t know a transaction until you know its PPA. It’s not just a compliance obligation; it’s a commitment to financial transparency that benefits all those who rely on the acquiring entity’s financial statements. |