Carbon Emissions Advisory in Australia

Table of Contents

- 01 Introduction

- 02 Carbon Emmisions Advisory in Australia Overview

- 03 Scope 1 Emissions

- 04 Scope 2 Emissions

- 05 Scope 3 Emissions

- 06 Data Collection and Controls

- 07 NGER and AASB S2 Alignment

- 08 Reduction Targets

- 09 Net Zero Roadmap — Five Steps to Decarbonisation

- 10 Carbon Risk and Opportunity Assessment

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 Carbon Emissions Advisory in Australia Overview

- 03 Scope 1 Emissions

- 04 Scope 2 Emissions

- 05 Scope 3 Emissions

- 06 Data Collection and Controls

- 07 NGER and AASB S2 Alignment

- 08 Reduction Targets

- 09 Net Zero Roadmap — Five Steps to Decarbonisation

- 10 Carbon Risk and Opportunity Assessment

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

Carbon as a Financial Variable

Carbon is no longer just an environmental concern; it is now one of the largest financial variables for businesses in the twenty-first century. Carbon intensity of organisational operations has now affected almost all aspects of organisational financial performance and strategic positioning.

- Carbon exposure influences energy and raw material prices, capital availability, regulatory compliance, customer purchasing decisions, and long-term asset sustainability.

- Knowledgeable practitioners who understand how to measure, control, and report carbon emissions Australia are among the most marketable professionals in finance, accounting, sustainability, and corporate advisory.

- Demand for this expertise is soaring amid new market regulations.

The Three-Scope Framework

The frame of reference for understanding corporate carbon exposure comprises three conceptualised dimensions that, in combination, provide a holistic picture of an organisation’s greenhouse gas footprint.

- Scope 1 Emissions: Direct emissions of sources owned or controlled by the entity.

- Scope 2 Emissions: Indirect emissions of purchased energy.

- Scope 3 Emissions: Indirect emissions in the broader value chain - upstream and downstream.

- The Australian in-scope entities will be required to report Scope 1 and Scope 2 emissions in the first year, with Scope 3 to be added thereafter, which is simply a practical reality that Scope 1 and Scope 2 are more measurable and verifiable, and the data structure required to support Scope 3 is more time-consuming to establish.

Purpose and Scope of This Guide

This article is a working guide for junior to mid-level professionals building expertise in carbon advisory, whether you are trained in accounting, engineering, corporate finance, law, or environmental science.

- Addresses the technical aspects of emission measurement, data collection and control.

- Covers the strategic aspects of setting plausible reduction goals and a net-zero roadmap.

- Researches the fundamental functions of carbon risk and opportunity assessment and assurance support.

- By the end, you will have a reasonable, practical framework to work on - and eventually lead - carbon emissions Australia advisory engagements of real complexity and importance.

Carbon management cannot be a stand-alone sustainability practice- it is a vital financial discipline. In-scope Australian entities must report Scope 1 and Scope 2 emissions in year one, and Scope 3 at a later time. Organisations that internalise this early will be in a far better position to address all the regulatory, investor, and commercial challenges that the energy transition will present. |

02 Carbon Emissions Advisory in Australia Overview

What Carbon Advisory Encompasses

Carbon advisory is at the intersection of climate science, financial analysis, regulatory compliance ESG and strategic planning. Its practitioners help organisations learn about their carbon footprint, the risks, and the opportunities presented by the transition to a lower-carbon economy.

- The scope of work involves establishing credible reduction commitments, creating operational pathways to the reductions, and providing the disclosures required by investors, regulators, and other stakeholders.

- Carbon advisory, which has developed from a niche environmental consulting specialty into a mainstream professional services capability.

- Every year, it becomes increasingly intertwined with mainstream financial advisory work.

How the Field Has Expanded

The range of carbon advisory over the past ten years has significantly increased beyond the compliance orientation of the initial ten years, and the complexity of what organisations are expected and required to do has increased.

- Initial focus: helping organisations comply with the NGER scheme, managing exposure to carbon pricing, and creating GHG inventories to submit to the regulator.

- Current scope: strategic decarbonisation planning, carbon credit strategy, analysis of climate-related scenarios, integration with financial planning and capital allocation, and facilitating the independent assurance process.

- Because Scope 1 and 2 reporting begin in the first year and Scope 3 is implemented over time, the greatest immediate advisory requirement is to establish a credible measurement and disclosure capacity for direct and energy-related emissions, as well as a credible Scope 3 program.

The Commercial Drivers of Demand

An expanding business landscape aligns with the regulatory landscape, underscoring the structural need for carbon advisory services at all levels of seniority across industries.

- Customers are incorporating decarbonisation requirements into procurement contracts - a major consumer goods company aiming to be net zero by 2040 is already asking its top 100 suppliers to provide certified emissions data and commit to their own reduction targets as a condition of staying on the supplier list.

- Carbon-related demands: Lenders and investors are making carbon-related demands through sustainability-linked loan covenants and ESG investment requirements.

- This is one of the most significant structural forces redefining the demand for carbon advisory and creating career opportunities across all industries through the value chain of carbon responsibility.

03Scope 1 Emissions

What Scope 1 Emissions Include

Scope 1 Emissions are the direct aspect of the carbon footprint of an organisation – the greenhouse gases produced by sources owned or controlled by the organisation. They may account for the greatest proportion of the total footprint and be the element most directly under operational control in organisations with substantial physical activity.

- Stationary devices such as boilers, furnaces, and generators.

- Mobile combustion in company-owned or leased vehicles and aircraft.

- Refrigerant and gas leaks.

- Chemical or physical reactions during manufacturing that produce process emissions.

Measurement Requirements and Regulatory Framework

To be accurate, a systematic inventory, appropriate emission factors, and adherence to the GHG Protocol and Australian regulatory requirements are necessary.

- Organisations are required to develop an inclusive list of all sources of emissions.

- The emission factors (the coefficients that convert activity data, such as fuel use, into CO2-equivalent emissions) should be selected and used consistently.

- The NGER participants should compute and disclose Scope 1 Emissions using the prescribed methodologies outlined in the National Greenhouse and Energy Reporting (Measurement) Determination, which sets out approved methodologies, emission factors, and data quality criteria for each category of emission source.

- Scope 1 and 2 reporting: Because Scope 1 and 2 reporting is mandatory during the first year, the most time-sensitive capability gap is ensuring Scope 1 is measured correctly during that period.

Technical Challenges in Scope 1 Measurement

Although Scope 1 Emissions are the most direct to quantify, they still pose significant technical challenges that require intentional investment in methodology and systems.

- Fugitive gases: Fugitive gases, such as natural gas systems (methane), HVAC systems (refrigerant discharges), and industrial processes (emissions), are notoriously difficult to measure accurately.

- Available methodological tools include leak detection and repair schemes, continuous emissions monitoring systems, and mass balance estimates - each with its own assumptions and uncertainties.

- Under AASB S2, the uncertainty surrounding Scope 1 estimates should be recorded and its materiality evaluated - a very high disclosure requirement compared to what most organisations used to.

- This higher bar encourages direct investment in better measurement systems rather than in better calculation methodology.

04 Scope 2 Emissions

What Scope 2 Emissions Represent

The indirect greenhouse gas emissions of the production of electricity, steam, heat or cooling that an organisation purchases and consumes are called Scope 2 Emissions. Although the physical emissions occur at the power plant rather than on the organisation’s premises, both the GHG Protocol and AASB S2 mandate that they be included in the corporate carbon footprint.

- The logic: purchasing decisions generate emissions, and the buyer should be duly responsible for the resulting emissions.

- Scope 2 Emissions from purchased electricity are the largest controllable portion of the total footprint in most commercial, professional services, and retail businesses.

- The completeness and quality of Scope 2 Emissions measurement should be of high priority to all reporting entities since Scope 1 and 2 reporting is required in year one.

Location-Based vs Market-Based Accounting

The Scope 2 Guidance of the GHG Protocol has also introduced a two-method accounting framework that practitioners should be familiar with. Both methods are to be reported in accordance with AASB S2 and can yield significantly different results.

- Location-based approach: Relies on average emission intensity factors for the grid areas where the organisation is situated, using the actual generation mix in the electricity market.

- Market-based approach: Reflects the real-world purchase of electricity under contract, such as renewable energy certificates, power purchase agreements, or green tariffs.

- The two approaches may yield significantly different results in organisations that have invested in renewable energy procurement.

- This two-way reporting is changing the nature of organisational thinking and reporting regarding their renewable energy strategy.

Reduction Strategies and the Additionality Question

The most commercially viable first step on the decarbonisation journey for most organisations is to mitigate Scope 2 Emissions; however, practitioners need to be aware of key nuances when recommending reduction actions.

- The rapid decline in renewable energy prices, long-term power purchase agreements, and robust renewable energy certificate markets have enabled large Scope 2 cuts within typical commercial planning horizons.

- Critical difference: additionality is whether a renewable energy claim is new generation to the grid, or merely an accounting device through the purchase of certificates that does not lead to physical generation.

- Advanced investors and assurance providers increasingly doubt this distinction.

- Organisations whose Scope 2 disclosure is based solely on certificate purchases and no additionality will find it difficult to be credible as disclosure requirements become more stringent.

05Scope 3 Emissions

The Full Picture of an Organisation's Climate Impact

Scope 3 Emissions are the most detailed statement of an organisation’s climate impact and are the most difficult to measure. They include all other indirect emissions in the value chain – from the extraction of raw materials to the disposal of the sold products at the end of life.

- The GHG Protocol identifies 15 types of Scope 3 Emissions, including purchased goods and services, capital goods, business travel, use of sold products, and investments.

- Scope 3 Emissions in most organisations, particularly financial services, retail, technology and professional services, contribute to more than 90% of the total corporate carbon footprint.

- The Scope 3 reporting requirement has a phased introduction. Still, the late date is no excuse to postpone preparation; the lead time required to build credible Scope 3 measurement capacity means organisations must start building the capability now.

Measurement Challenges and Methodology Choices

The measurement of Scope 3 Emissions is essentially a data availability and methodological consistency issue. Practitioners should be familiar with the options available and their limitations.

- Primary activity data of suppliers - the best foundation of the Category 1 calculations - is often not available, particularly where smaller suppliers in emerging markets have not yet built their own GHG accounting capacity.

- Without primary data, organisations rely on spend-based or industry-average emission factors, or a blend of primary and secondary data.

- Both approaches involve some level of uncertainty, and the selection of the methodology and the provision of clear reporting are crucial parts of any plausible Scope 3 disclosure under AASB S2.

Why Scope 3 Investment Is Strategically Necessary

The business case for investing in Scope 3 accuracy has become much stronger now that mandatory disclosure frameworks are more mature and investor scrutiny has increased.

- Under AASB S2, in-scope entities are required to report their Scope 3 Emissions with a description of how they were calculated, categories that they cover and sources of estimation uncertainty.

- Investors increasingly use scope 3 data to assess climate risk at the portfolio level, especially for assets financed by banks and investment managers, and to assess the true quality of net-zero commitments.

- An organisation that pledges to go net zero by 2050 yet lacks any serious plan to mitigate its Scope 3 footprint - which could easily be many times its direct emissions - is making a commitment which sophisticated stakeholders will soon realise is structurally unsound.

06 Data Collection and Controls

Why Data Quality Is the Foundation

It is only when the quality of a carbon emission disclosure matches the information on which it is based that it can be trusted. Data collection and controls are the simplest feature of the whole carbon advisory practice, supporting all calculations, metrics, assurance opinions, and regulatory submissions.

- All the numbers in the GHG inventory and sustainability report rely on the soundness of the data pipeline - of where activity data is generated in operations, collected, validated, calculated, and aggregated.

- An audit-quality data pipeline is not a project - it is a long-term operational discipline.

- As Scope 1 and 2 emissions are required to be reported in year one of in-scope Australian entities, organisations are under extreme pressure to have available and trusted data on at least these two scopes as soon as possible.

Architecture of an Effective Data Control Framework

A robust data collection and control structure reflects the internal control environment for financial reporting, modified to suit the ESG data environment.

- Transaction level: Operational systems (utility meters, fuel management systems, fleet telematics, production monitoring platforms) provide automated data feeds that minimise manual entry and related errors.

- Manual collection: Structured templates that define data fields, units and calculation instructions provide consistency across business units and geographies.

- Entity-level validation: Data rules indicate anomalies, like sudden spikes in consumption, data gaps, or unrealistic emission factors, before they spread through the inventory.

- Group-level consolidation: The controls ensure that the organisational boundary is preserved and that intercompany transactions are eliminated appropriately.

The Assurance Imperative

The science of data gathering and controls has gained new urgency due to the expansion of mandatory assurance requirements for GHG reporting.

- An assurance provider must have sufficient, relevant evidence that the figures are free of material misstatement, which cannot be done where the data trail between the source and the final report is incomplete or untraceable, or where the controls are not documented.

- In this way, organisations that generate their GHG inventory in hand-populated spreadsheets (without version control, calculation audit trails, or formal review and approval) will not be able to support a credible assurance engagement.

- Organisations with a compulsory disclosure and assurance regime will have to invest in specific ESG data management systems and documented data collection and control processes. This is not to be postponed.

Table 1: GHG Data Collection Framework — Sources, Quality Risks, and Controls

Emission Source | Typical Data Source | Primary Quality Risk | Key Control |

|---|---|---|---|

Scope 1 — Stationary combustion | Invoices of fuel purchases, meter readings. | Mismatched units; lack of invoices between periods. | Automated utility feeds; monthly reconciliation to procurement records |

Scope 1 — Mobile combustion | Fleet fuel cards, telematics, logbooks | Uncovered vehicles; types of fuel mixtures. | Integration of the fleet management system; cross-checking vehicle registry. |

Scope 1 — Fugitive emissions | Purchase records for refrigerant and leak detection records. | Underreporting; incomplete coverage of LDAR. | Refrigerant census annually; documentation of the LDAR program. |

Scope 2 — Electricity | Smart meter data, utility invoices. | Several suppliers; lack of invoice period gaps. | Supplier data portal; monthly imports automatically; period-end accruals. |

Scope 3 — Purchased goods | ERP expenditure information; supplier surveys. | Poor availability of primary data; approximate spend. | Supplier engagement program; preference based on primary data to favoured suppliers. |

Scope 3 — Business travel | Travel management system, expense claim. | Individual card bookings; lost information. | Travel management system API; policy that requires centralised booking. |

07 NGER and AASB S2 Alignment

The NGER Scheme — Australia's Original Carbon Reporting Framework

The Australian carbon reporting environment is characterised by two quite distinct yet closely interrelated regulatory frameworks. The National Greenhouse and Energy Reporting (NGER) scheme has been the main tool of corporate greenhouse gas and energy reporting in Australia since 2008.

- The Clean Energy Regulator administers NGER and applies to those that exceed specific emission or energy consumption levels.

- It is based on a financial year reporting cycle, with specified calculation methodologies defined in the NGER Measurement Determination.

- NGER data is used to inform national greenhouse gas accounts and to support the Safeguard Mechanism, which establishes baseline emissions limits for large industrial facilities.

How AASB S2 Differs and Why Both Matter

AASB S2 is a new mandatory climate reporting standard, based on IFRS S2, with a radically different structure and intent from NGER.

- NGER is concerned with proper measurement and regulatory reporting. In contrast, AASB S2 is a model of financial disclosure designed to provide investors with decision-useful information on climate-related risks and opportunities.

- The requirements of AASB S2 for disclosing emissions are not restricted to the NGER boundary; they apply to the entire Scope 1, Scope 2, and Scope 3 footprint, as stipulated by the GHG Protocol.

- The difficulty of matching NGER and AASB S2: Direct and energy-related emissions will be the most urgent to match, and will demand a higher level of accuracy, controls, and disclosure than NGER has historically demanded.

Navigating the Overlap in Practice

One of the most marketable skills in carbon advisory is the capacity to understand the interdependence of NGER and AASB S2, and to navigate the differences between the two in practice.

- Different organisational boundaries can exist across frameworks and must be explicitly reconciled.

- The emission factors and methodologies approved by NGER might have to be augmented or modified to meet the scope and greater disclosure requirements of AASB S2.

- The most directly useful type of advisory support is being offered by practitioners who can fluently translate between the two regimes, i.e., who can explain to clients where their NGER compliance already satisfies AASB S2 requirements and where further work is required.

08 Reduction Targets

Why Credible Targets Matter

Setting plausible reduction goals is one of the most important steps an organisation can take in its carbon management process. A properly developed target suggests a real strategic purpose, establishes a clear mandate for operational and capital-allocation decisions, and provides an accountability framework for reporting progress annually.

- An ill-designed target, such as one that is opaque, based on a haphazard approach, or not aligned with operational reality, may create reputational risk, investor scepticism, and regulatory exposure as greenwashing assertions are subject to increased scrutiny.

- As in-scope Australian entities report Scope 1 and Scope 2 Emissions starting in year one and Scope 3 to follow, reported Scope 1 and Scope 2 baselines with a clear forward plan will be the most plausible near-term reduction targets.

The SBTi Framework

The Science-Based Targets Initiative (SBTi) framework has significantly clarified the structure of plausible reduction targets, providing a widely recognised external validation system that investors and lenders are increasingly using as a standard expectation.

- SBTi-validated targets should align with the level of decarbonisation needed to cap global warming at 1.5 degrees Celsius, consistent with the latest climate science.

- At least Scope 1 and Scope 2 Emissions should be covered by near-term targets. Scope 3 objectives must be met if Scope 3 accounts for more than 40 per cent of the total footprint, as is the case with most service-sector and consumer-facing companies.

- SBTi validation provides third parties with credibility that cannot be duplicated by internal procedures and is becoming a precondition for institutional investors and sustainability-based financing systems.

Balancing Ambition with Operational Feasibility.

The target-setting process should strike a balance between scientific ambition and operational feasibility. Technically consistent goals that presuppose decarbonisation pathways but lack a viable implementation plan are aspirations, not promises.

- The most plausible reduction targets are made retrospectively based on a detailed decarbonisation pathway - the understanding of what reductions can be achieved by what operational interventions, what capital investment is required, over what time, and at what cost.

- This bottom-up methodology ensures that targets are owned by the operational teams that will provide them, are part of capital planning and budgeting, and can be measured against specific milestones.

- A remote 2050 horizon, as the main accountability instrument, with no near-term milestones tied to specific interventions, is becoming increasingly unacceptable to investors and assurance providers.

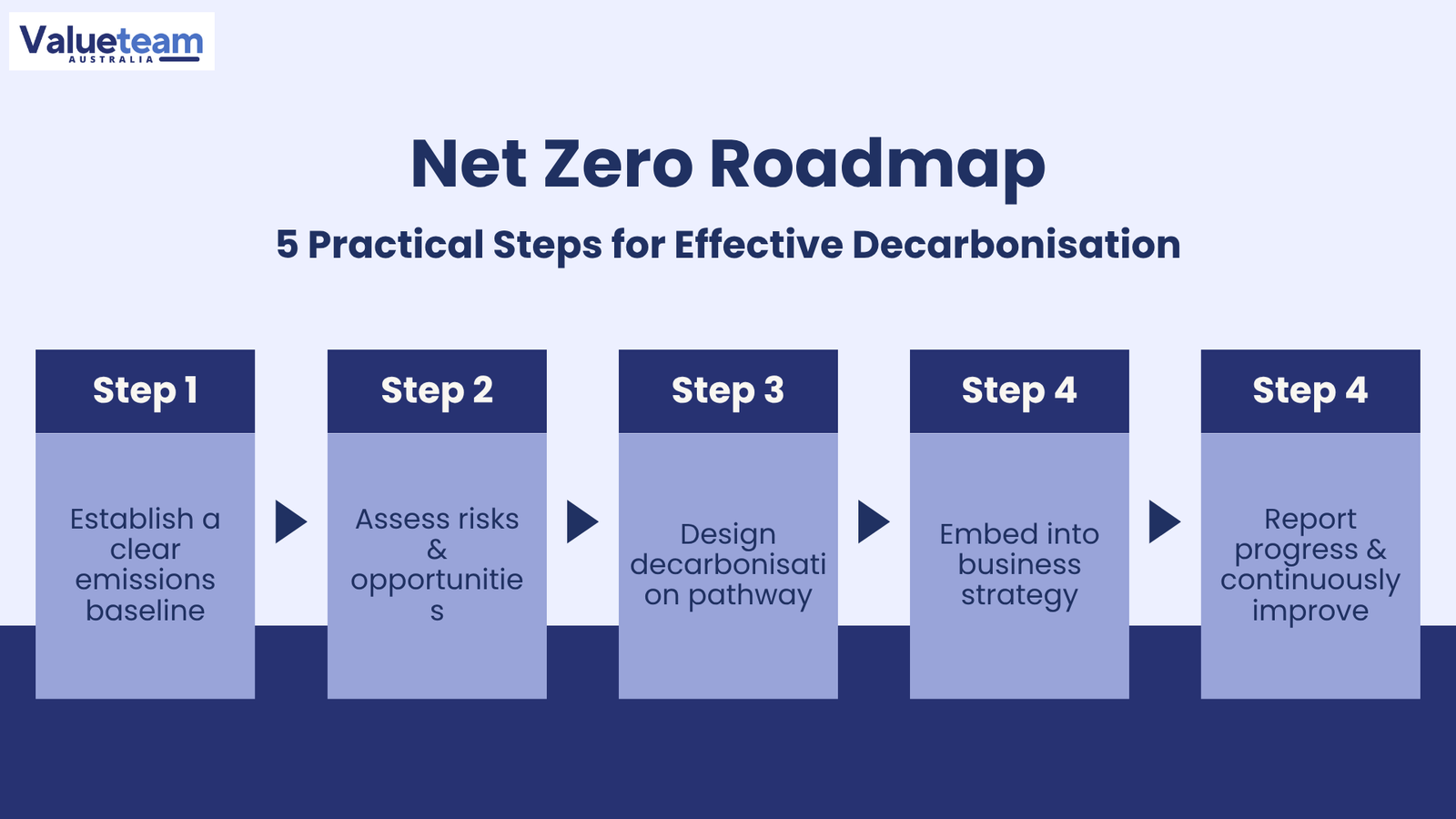

09 Net Zero Commitment Roadmap — Five Steps to Decarbonisation

What a Net Zero Commitment Roadmap Is — and Is Not

A net zero commitment roadmap is not a document but a dynamic plan of action that links the organisation’s current emissions position to its net zero commitment through a sequence of realistic, funded and responsible actions.

- Creating a roadmap that is both scientifically plausible and operationally viable is one of the most complex tasks in carbon advisory.

- It involves combining technical emissions analysis, financial modelling, operational planning, and stakeholder engagement into a cohesive whole.

- The five steps below are the systematic process that can produce the most lasting and justifiable results.

Step 1 — Establish a Verified Emissions Baseline

Every net-zero roadmap starts with a transparent, proven picture of the organisation’s current emissions situation – strong enough to withstand the scrutiny of investors and assurance providers.

- Prepare a complete GHG inventory comprising Scope 1, Scope 2 and the material categories of Scope 3 Emissions, in accordance with GHG Protocol and relevant NGER requirements.

- Choose a base year, which depends on the quality of data and representativeness - ideally a recent year with complete, verifiable data not skewed by a one-off event.

- The quality of data collection and controls must be adequate to enable external assurance at the point of origin - investors and assurance providers will test the baseline in the same manner as the destination.

Step 2 — Assess Carbon Risks and Opportunities

The organisation should understand the financial cost of its carbon exposure across its entire value chain before embarking on a decarbonisation pathway.

- A strict carbon risk and opportunity analysis overlaid to identify where carbon pricing, regulatory reforms, technological upheaval, and market changes pose the most significant financial threats in the inventory.

- The more organisations are exposed to transition risk, the greater their financial incentives to accelerate decarbonisation - the assessment quantifies this.

- Organisations that face high physical climate risks must incorporate resilience into their roadmap alongside decarbonisation.

- This evaluation informs the sequencing and the ambition level of the net-zero roadmap.

Step 3 — Design the Decarbonisation Pathway

The technical heart of the net-zero roadmap is the decarbonisation pathway, a phased programme of emission-reduction interventions superimposed on the emissions inventory, along with capital requirements, timelines, and projected reductions for each intervention.

- The abatement cost is widely used to structure interventions: low-cost interventions (energy efficiency, fleet electrification), medium-cost interventions (on-site renewables, process heat decarbonisation), and high-cost frontier interventions (industrial carbon capture, green hydrogen).

- Pathway should also discuss how the remaining emissions that cannot be eliminated by the target date will be treated, through high-quality carbon removals, direct air capture or other removals.

- A residual removal plan should align with the organisation's stated net-zero standard and the credibility expectations of stakeholders.

Step 4 — Mobilise Capital and Operations

A net-zero roadmap, as a strategy document, is useless. The most important thing is to translate the roadmap into the organisation’s financial planning, capital allocation, and operations management systems.

- Add decarbonisation capital spending to multi-year capital plans - make it visible and fundable like other strategic investments.

- Add carbon costs to project hurdle rates to ensure investment decisions are made systematically and reflect carbon implications.

- Introduce internal carbon pricing as an incentive system for operational managers, which influences the investment decisions and the performance in terms of emissions.

- The organisations that run quickest on their roadmaps are always those that have decarbonisation as a line-management task - with clear ownership, specific resources, and executive and board leadership.

Step 5 — Report, Assure, and Iterate

A net-zero roadmap needs to be continually updated and revised as performance data is gathered, technology costs vary, the regulatory environment evolves, and the organisation’s strategy is developed.

- Annual reporting on the progress of roadmap milestones — supported by independent verification of the supporting emissions data — serves as the external accountability mechanism and the internal performance improvement discipline.

- The most believable organisations do not treat their net-zero roadmap as a fixed document: they clearly demonstrate what they are doing well and what they are not doing well.

- They show readiness to revise and reinforce the roadmap as evidence mounts up- that is the sign of true commitment and not a show-going compliance.

10Carbon Risk and Opportunity Assessment

What the Assessment Is and Why It Matters

The carbon risk and opportunity assessment is an analytical process through which an organisation systematically identifies, evaluates and prioritises the financial impacts of the shift to a lower-carbon economy and the physical impacts of climate change.

- It provides the basis for the organisation's climate-related disclosures under AASB S2.

- It also makes the strategic contribution of guiding the development of the net-zero roadmap, establishing reduction goals, and integrating carbon factors into capital allocation and risk management.

- A shallow evaluation yields superficial strategy - a rigorous one yields real competitive insight and, more and more, competitive edge.

Quantifying Transition Risk — The Carbon Pricing Example

The majority of Australian organisations that have conducted their first carbon risk and opportunity assessment have focused on transition risks. The most readily measurable is carbon-pricing risk.

- Overlapping a fixed price per tonne of carbon on its confirmed Scope 1 Emissions inventory allows an organisation to estimate its financial exposure to a carbon price.

- A mid-sized cement producer, which conducted this analysis, discovered that even a mid-range carbon price of 75 per tonne would raise its cost base by almost 18 million per year, more than 10 times its annual EBIT.

- This finding instantly made decarbonisation a strategic imperative and changed the entire capital allocation discussion.

- This is the financial-based approach that makes a rigorous carbon risk assessment appear different from a qualitative risk register exercise.

The Opportunity Dimension — Often Underdeveloped

The opportunity dimension of the evaluation is just as important as the risk dimension, but it is often underdeveloped. The transition to a net-zero economy is creating considerable business opportunities.

- Low-carbon products and services: Customers and procurement teams that have decarbonisation as part of their supply chain are increasingly demanding low-carbon products and services.

- Green financing is offered at reasonable rates to organisations that demonstrate credible decarbonisation efforts.

- Carbon credit markets can create new sources of revenue - a European industrial gas company discovered that its existing carbon capture facilities could be reused to produce high-quality carbon credits within a voluntary carbon market standard, a new source of revenue to help it cover part of its own decarbonisation expenses.

- Lesson: A well-constructed assessment would consider both sides of the transition equation, not just the risk.

11 Challenges and Lessons Learned

Challenge 1 — The Baseline Problem

The most challenging problem in carbon advisory practice is the baseline issue. Many organisations are declaring far-reaching reduction goals and detailed net-zero plans before having a stable, validated GHG baseline.

- In the case of the baseline being unreliable - because of bad data collection and controls, inconsistent methodology or poorly defined organisational boundaries - all further target and reduction claims are unreliable as well.

- Scope 1 and Scope 2 Emissions are the most urgent, as they must be reported in the first year. Organisations that have yet to determine a stable baseline are already lagging behind the regulatory curve.

- And the moral of the story is: Be firm in preparing the groundwork before you set targets. Making a false start is to make everything false afterwards.

Challenge 2 — The Scope 3 Emissions Gap

The same challenging discussion is present in nearly all organisations that have published a net-zero commitment when it comes to the full picture of their value chain footprint. The most common category is Scope 3 Emissions, but it is also the most difficult to handle.

- Purchased goods and services, use of sold products, or financing of emissions are much more significant than direct emissions in most organisations and are beyond the direct operational control of the reporting entity.

- The Scope 3 reporting requirement is introduced in phases, but since preparation cannot be delayed, the lead time required to achieve real measurement capability must be considered.

- The organisations that have advanced most are those that started supplier engagement early, invested in primary data collection on their largest sources of emissions, and considered Scope 3 in procurement requirements and product development decisions.

Challenge 3 — The Integration Gap

The third significant obstacle is integration – the danger that carbon management will continue to be a siloed sustainability activity, as opposed to being integrated into capital planning, financial reporting, risk management, and operational decision-making.

- A carbon role that is not linked to the rest of the organisation will not achieve the scale or pace of emissions reduction needed to be credible when setting targets.

- The NGER and AASB S2 convergence is a positive forcing mechanism: compulsory financial disclosure generates the organisational need to apply the same rigour and integration to carbon information as to financial information.

- The most rapid decarbonisation organisations are those that have institutionalised carbon as a line management concern, integrated carbon costs into investment decision models, and integrated carbon performance reporting into the regular information flows of the CFO and the board.

- Practitioners who help clients make and take action on this shift are doing their most truly valuable work.

12 Conclusion and Actionable Insights

Why Carbon Advisory Is a Career-Defining Field

One of the most rapidly developing and truly important professional areas of the modern world is carbon emissions advisory. The intersection of obligatory reporting, investor expectations, and commercial value chain demands has imposed structural, long-term demand upon practitioners able to integrate technical emissions expertise with monetary acumen, regulatory expertise, and strategic advisory ability.

- The entire spectrum of carbon advisory work will become more complex and commercially significant throughout the careers of the people joining the market today.

- It is not the understanding of climate science per se that renders carbon advisory professionals the most valuable, but rather the skill of applying that science to financial risk, strategic opportunity, and plausible organisational action.

- The work is essentially a work of translation - between the material and the financial, between the technical and the strategic, between what is quantified and what is revealed.

Five Actionable Steps for Practitioners

The five steps that follow provide a tangible roadmap for junior- to mid-level professionals to develop expertise in carbon emissions advisory in Australia.

- Step 1 - Develop a solid technical base in GHG accounting: learn the GHG Protocol Corporate Standard and the NGER Measurement Determination. These are the foundations of any serious carbon emissions Australia work - the ability to be competent in boundary-setting, in the choice of emission factors, in calculation techniques, and in quality assurance is the foundation on which all other things are based.

- Step 2 - Master the NGER and AASB S2 relationship: know the points of convergence and divergence and how to reconcile the two in practice. This skill is now in short supply compared to demand.

- Step 3 - Take time to learn about the Scope 3 challenge: familiarise yourself with the 15 GHG Protocol categories, the different calculation methods and their levels of accuracy, and the new supplier engagement and primary data collection approaches that are enhancing the quality of Scope 3 data across industries. This is the boundary of measuring carbon.

- Step 4 - Learn the assurance support process internally: know what assurance providers review, how they evaluate the quality of GHG inventory, and what organisations should prepare to have a successful engagement. This is where the skills in data collection and controls are most directly tested since Scope 1 and 2 reporting is mandatory starting with the first year.

- Step 5 — Treat net-zero roadmap and reduction target work as strategic finance—they are. Those practitioners who introduce financial rigour to decarbonisation planning - linking emission paths to capital plans, cash flows, business model resilience - will provide the most truly valuable advisory results.

The price of carbon increasingly characterises the twenty-first-century economy. Individuals who learn to quantify it rigorously, care about it strategically, and tell the truth will be among the most impactful practitioners of their time. |