Business & Company Valuation Services in Australia

Table of Contents

- 01 Introduction

- 02 What Is Business and Company Valuation?

- 03 Why Do Clients Need a Valuation?

- 04 Key Valuation Approaches

- 05 Key Value Drivers — What Increases or Reduces Business Value

- 06 Common Mistakes Businesses Make Before a Valuation

- 07 Information and Documents Required — Five Key Steps

- 08 Our Valuation Process

- 09 Valuation Methodologies by Situation

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is Business & Company Valuation?

- 03Why Do Clients Need a Valuation?

- 04 Key Valuation Approaches

- 05 Key Value Drivers — What Increases or Reduces Business Value

- 06 Common Mistakes Businesses Make Before a Valuation

- 07 Information and Documents Required — Five Key Steps

- 08 Our Valuation Process

- 09 Valuation Methodologies by Situation

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

What Business Valuation Is

Business and company valuation refers to the process of arriving at an economic estimate of a company, business unit, shares, or ownership interest using acceptable valuation methods and professional judgment. It is a subject area that is at the intersection of financial analysis, strategy, market research, and law – one that is heavily applied in practice to all stakeholders.

- Any figure negotiated to reflect a transaction price, a financial statement, a dispute, or information about a capital raise will only be as good as the valuation that underlies it.

- Valuation is not a mechanical process - it involves real involvement in the particular business situation, the valuation's purpose, and the market in which the business is carried out.

- A technically competent contextually blind valuation, i.e. one where the valuer has used a standard approach to valuation and has not actually thought about the context of the business, is of little value to any stakeholder.

When a Valuation Is Needed

Informed decisions can be made using valuation, whether you are about to raise capital, buy or sell a business, comply with financial reporting requirements, or address shareholder issues. What all these contexts share is the requirement of an objective, defensible and methodologically sound evaluation of value.

- A valuation should consider the specific characteristics of the business, the valuation purpose, and the market and economic context in which the business operates.

- Valuation advisory services help the clients understand the fair value of their business and the key drivers of enterprise and equity value.

- Understanding this landscape is among the most marketable skills a professional in corporate finance, accounting, law, or executive management can possess.

A valuation is not merely a number; it is a substantiated argument of value that, when subject to review, should be capable of surviving the scrutiny of boards, investors, auditors, courts, and regulators. The quality of the argument is what determines the utility of that argument. |

02 What Is Business & Company Valuation?

The Fundamental Question a Valuation Answers

A business valuation is used to determine the fair market value of a business or a specific ownership interest. It is, in its simplest form, an analysis that responds to a question that seems so obviously easy to answer: what a willing, informed buyer would pay a willing, informed seller in an arm’s-length transaction to buy this business or this interest?

- The complexity of this question is that every business is unique; it is an industry with its history, management quality, growth patterns, risk exposure, and valuation purpose, which influence the methodology and the result.

- The extent to which a business valuation can reach is broader than most stakeholders realise.

The Full Scope of Valuation Types

The variety of circumstances and interests to which a professional valuation is needed is greater than most individuals are aware of, and includes both total enterprise value and particular ownership interests.

- Full company valuation: Determines the total enterprise value and the value of equity that can be ascribed to all shareholders.

- There are two definitions of equity shares or minority/controlling stake valuation: The value of a specific percentage of a type of shares, not necessarily a pro-rata value of the total equity, particularly where control premiums or minority discounts are in play.

- Enterprise value analysis: The total valuation of the company with debt, which is used to calculate debt-adjusted equity values.

- Unlisted and private company valuation: Necessary where there is no price in a public market.

- Fair value of business units or subsidiaries: Needed when restructuring a company or reporting its financial results.

Methodology Depends on Context

The valuation method depends on the purpose, business stage, financial performance, and the available market data. No single-fit-all method exists.

- A start-up with significant intellectual property and a great market opportunity, but no revenues, is valued very differently from a mature, cash-generating business with a long track record.

- A firm that a strategic buyer is acquiring will be valued differently from one that is being evaluated for financial reporting under AASB 13.

- The art and the professional rigour of business valuation is to select and use the approach that best fits the specific situation, and to make a conclusion that is justifiable, articulate about its assumptions, and actually useful to the stakeholders to which it is applied.

03Why Do Clients Need a Valuation?

The list of cases that may require a professional business and company valuation is wider than most people are inclined to believe. The most noticeable trigger, a business sale or acquisition, is only one among a broad spectrum of valuation markets that includes capital markets activity, financial reporting requirements, tax and regulatory compliance, and dispute resolution. Awareness of the full range of triggers is important for practitioners, as the valuation’s purpose directly influences all methodological and presentation decisions.

Fundraising and Investment

Angel investors, venture capital, private equity, or institutional ‘investors’ equity fundraising almost always include a valuation to provide a starting point for negotiating the price at which new capital will be issued.

- A believable, independently supported valuation, versus an unsupported in-house estimate, can be the difference between a fair dilution and an ugly one for a founder negotiating with a private equity firm.

- Transactions in private equity and venture capital, negotiations with investors, and new share issuances all have different valuation requirements. Sometimes they need multiple valuations within the same process.

- The quality of the analysis determines the quality of the outcome.

Mergers, Acquisitions and Restructuring

The most obvious cases when a valuation is used are the acquisition of a company or the sale of a business. Still, the valuation needs in M&A go far beyond the top-tier price of the transaction.

- Purchases under AASB 3: Purchase price allocation (PPA) must be made, including the identification of all purchased assets and liabilities at fair value.

- Internal group restructuring and mergers and demergers create both commercial and regulatory valuation requirements, such as setting arm's-length prices for intra-group transfers, justifying court approval of schemes of arrangement, and providing the foundation for tax reporting of gains and losses.

Financial Reporting

Certain valuation requirements in financial reporting are among the most prevalent and non-discretionary; they are mandated by accounting standards that are not optional for entities that prepare general-purpose financial statements.

- Fair value measurement under AASB 13, purchase price allocation (PPA) under AASB 3, impairment testing under AASB 136 and ESOP / share-based payment valuation under AASB 2 are all repetitive statutory provisions.

- The reliability of the financial statements on which auditors and investors depend is directly affected by the quality of the valuations underlying these disclosures.

- The PPA process can be the most technically challenging valuation exercise that organisations that have made acquisitions and are in their first post-acquisition reporting year will experience.

Tax, Regulatory and Dispute Matters

Valuation requirements are produced for tax reporting, transfer pricing support, regulatory submissions, and compliance reporting and must satisfy standards and methodologies set by the ATO and other regulatory bodies.

- Shareholder conflict, partner departure, litigation issues, and buyouts all require valuations that are as rigorous and independent as to withstand cross-examination, often in litigation cases where cross-examination will subject the expert's opinion to intense scrutiny.

- The quality of accuracy, documentation, and methodological defensibility demanded in such situations is materially better than that required in commercial advisory valuations.

- Practitioners need to learn to differentiate and adjust their work to the situation.

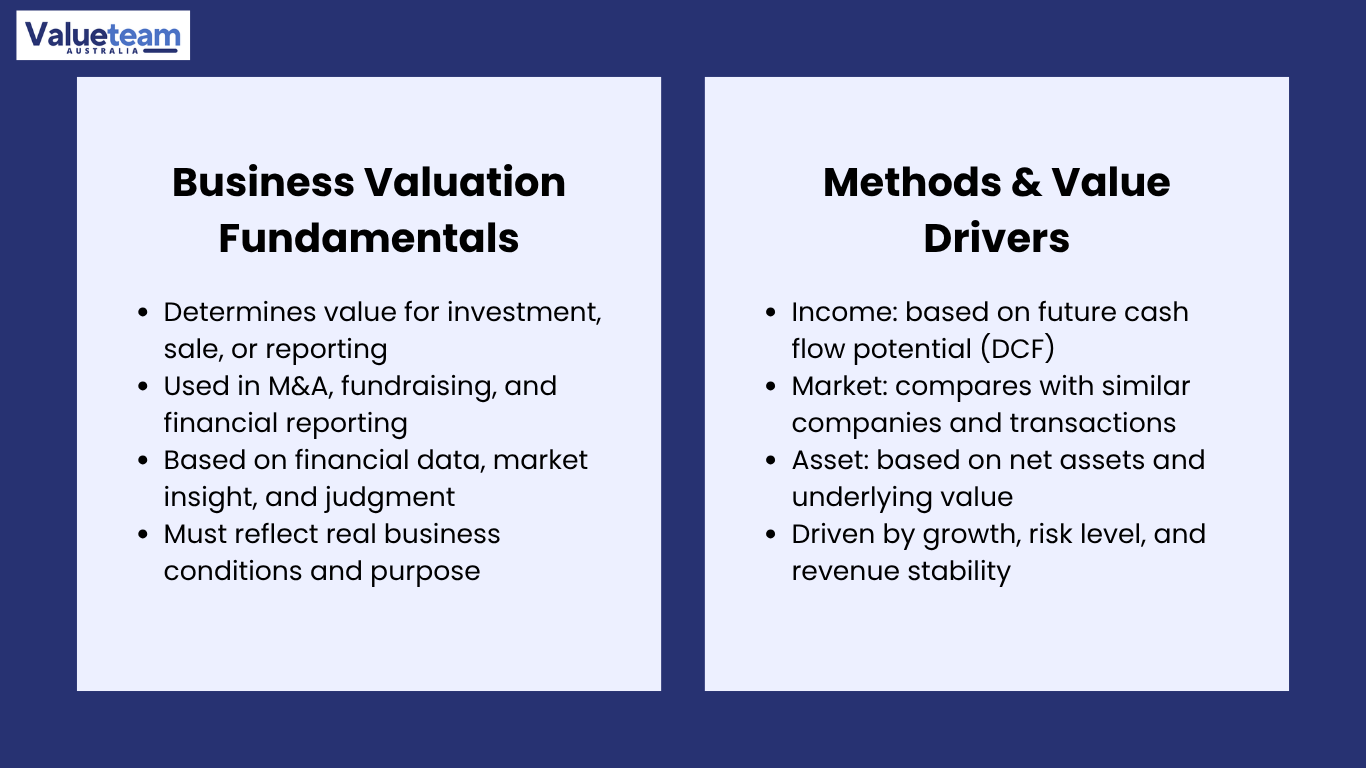

04 Key Valuation Approaches

The three key methodological families of professional business and company valuation are based on three different concepts of value. Seasoned practitioners choose the most suitable approach – or a combination of approaches – depending on the characteristics of the business and the purpose of the engagement, and cross-checks to challenge the plausibility of the main conclusion.

Income Approach — Discounted Cash Flow

The income approach appraises the business based on its future economic advantages – the present value of the cash flows that the business is expected to produce in the future. The discounted cash flow (DCF) method is the most popular form of this approach.

- The DCF technique accumulates the estimated cash flows over a forecast horizon, calculates a terminal value that represents the going-concern value of the business after the forecast horizon, and discounts both to present value at a discount rate / WACC that reflects the risk of the cash flows.

- Sensitivity analysis of the key assumptions, particularly the discount rate, terminal growth rate, and revenue and margin projections, is an important element of any plausible DCF analysis.

- It is a common strategy for expanding and successful businesses, in which earnings potential and growth curves are the main determinants of value.

Market Approach — Comparable Evidence

The market approach involves applying comparable market data to determine the value of the subject business relative to how the market values similar businesses.

- Real-time market pricing information is available on similar listed companies, which can be translated into valuation multiples, most usually EBITDA multiples and revenue multiples, which can be applied to the target company.

- Precedent transactions provide evidence of the prices actually paid in completed acquisitions of similar businesses and capture the control premium that acquirers pay to acquire a business outright.

- This method is best used in markets with active M&A activity and a large number of publicly traded comparables.

- The comparability test is essential: it is more difficult to find companies or transactions that are truly similar in terms of business model, size, risk profile, and growth opportunities than it might seem, and the quality of the comparables selection is as critical as the mathematical implementation of the multiples.

Asset-Based Approach

The asset-based approach is a valuation method that places value on the business in terms of the fair value of the net assets of the business, that is, the total assets less the total liabilities, and not the earning capacity of the business.

- It is the natural primary method of holding companies, real estate businesses, and asset-intensive businesses where enterprise value is primarily based on the underlying asset value.

- It is also applied in liquidation cases where a going-concern assumption is not feasible.

- In the majority of operating businesses with proven earnings potential, an asset-based approach usually establishes a floor value rather than a primary value, providing a helpful cross-check to the income and market approaches.

- Under AASB 13, this method requires assets to be recorded at fair value rather than historical cost, which may require independent valuations of certain types of assets, including real property, plant and equipment, and intellectual property.

05Key Value Drivers — What Increases or Reduces Business Value

Why Value Drivers Matter

It is as important to understand what drives business value as it is to understand the methodologies used to measure it. For business owners considering a transaction or raising capital, understanding which characteristics warrant a premium valuation and which lead to a discount helps them focus their investments and operational improvements on those most likely to maximise their results.

- Value driver analysis provides investors and advisers with an analytical prism to benchmark a business's valuation multiple against its industry peers and determine whether it is rational.

Factors That Increase Business Value

The drivers, which tend to add value to business, have a common factor: they reduce risk in future cash flows and increase confidence in the business’s capacity to continue or grow its earnings.

- Recurring and contracted revenue - recurring and long-term contracts, or highly integrated customer relationships, offer visibility and predictability, which can be valued at a higher multiple.

- Recurring and contracted revenue - recurring and long-term contracts, or highly integrated customer relationships, offer visibility and predictability, which can be valued at a higher multiple.

- A mature and autonomous management team capable of operating the business without the founder minimises key-person risk and supports business continuity after the sale.

- A picture of a business with a full valuation comprises stable and growing EBITDA margins, a robust growth pipeline, proprietary IP and technology, long-term contracts, strong brand positioning, and good ESG and governance practices.

Factors That Reduce Business Value

The value drivers are, in most aspects, the reverse of the factors that reduce value – they add risk, uncertainty, or dependency, which buyers and investors will discount.

- One of the most significant and common valuation discounts in private company deals is customer concentration risk, in which a few customers generate disproportionate revenue.

- Founder dependency creates key person risk: the business's value may not survive a change of ownership unless the founder can transfer his relationships, knowledge, or reputation to a new management team.

- Weak margins, litigation risk, poor compliance, regulatory risk, irregular cash flows, and poor operating history all add to the risk discount on the estimated earnings.

- Knowing these factors will enable clients to take steps before a valuation engagement to fortify their position.

Table 1: Key Value Drivers — Impact on Business Valuation

Value Driver | Direction of Impact | Why It Matters | How to Strengthen |

|---|---|---|---|

Recurring and contracted revenue | Increases value | Lowers earnings uncertainty; justifies a high multiple. | Enter into long-term contracts; build subscription/retainer systems. |

Customer diversification | Increases value | Minimises concentration risk; safeguards revenue base. | Actively broaden customer base; avoid >20% single-customer dependency |

Experienced and independent management team | Increases value | Reduces founder dependency; supports operational continuity post-sale | Develop leadership depth; document processes and succession plans. |

Stable and growing EBITDA margins | Increases value | Increased margins help multiples rise, and discount rates fall. | Discover and mitigate cost inefficiencies; emphasis on margin-accretive revenue. |

Customer concentration (single customer >30%) | Reduces value | Brings about binary revenue risk; initiates discount or deferred consideration. | Branch out; do not depend on bigger clients. |

Founder dependency / key person risk | Reduces value | Buyer is unable to purchase the intangible value when there is no transfer of value. | Decentralise and document; build team capacity; reduce founder-based connections. |

Litigation and compliance exposure | Reduces value | Develops contingent liability; raises risk discount. | Decide or publish transparently; keep compliance frameworks up to date. |

ESG and governance quality | Increases value | Minimises reputational, regulatory, and ESG risk and is gaining popularity among institutional buyers. | Invest in ESG reporting; enhance board and audit supervision. |

06 Common Mistakes Businesses Make Before a Valuation

Why Preparation Matters

The most frequent discovery of long-term valuation practitioners is that most businesses enter into a valuation engagement in a state of readiness that injects time, cost and uncertainty into the process – and that in some instances leads to a valuation conclusion that would have been far more favourable had the business been better prepared.

- Many businesses are postponed due to the absence or incompleteness of information.

- The good news is that a majority of these issues can be avoided - understanding them before engaging a valuation adviser enables businesses to mitigate them before the engagement itself.

- Proper preparation always enhances the quality and efficiency of the valuation result.

Unrealistic Financial Projections

Among the most common (and most damaging) errors in preparation is showing unrealistic financial forecasts. Any good valuation adviser will question management forecasts that assume much greater revenue growth than industry standards, improvements in margins without a clear operational foundation, or low capital requirements.

- Well-developed forecasts are bottom-up, based on recognised revenue opportunities, are tied to specific operational investments, and are pessimistic enough to be realistic.

- Valuation process: A management discussion typically accompanies the valuation process, particularly to challenge the reasonableness of the projections. Businesses that have not thought deeply about their assumptions are always poorly served by the process.

- Those that have been done are more thorough and favourable analyses.

Other Common Preparation Failures

Besides forecasting, other common preparation problems may make the valuation process difficult or invalid.

Out-of-date financials: Financial statements older than 12 months may not reflect current business conditions.

- Lack of a cap table or an ambiguous shareholder structure can make it impossible to determine the value of a particular ownership interest without first clarifying the shareholder structure.

- Unfinished business plans: These do not allow the valuer to get the strategic background of the financial projections.

- Unreported debts: These surface during due diligence and undermine confidence.

- Lack of supporting assumptions: The valuer cannot determine credibility without a written justification of the main financial projections.

- Prepared businesses always perform better than unprepared businesses in a competitive M&A process.

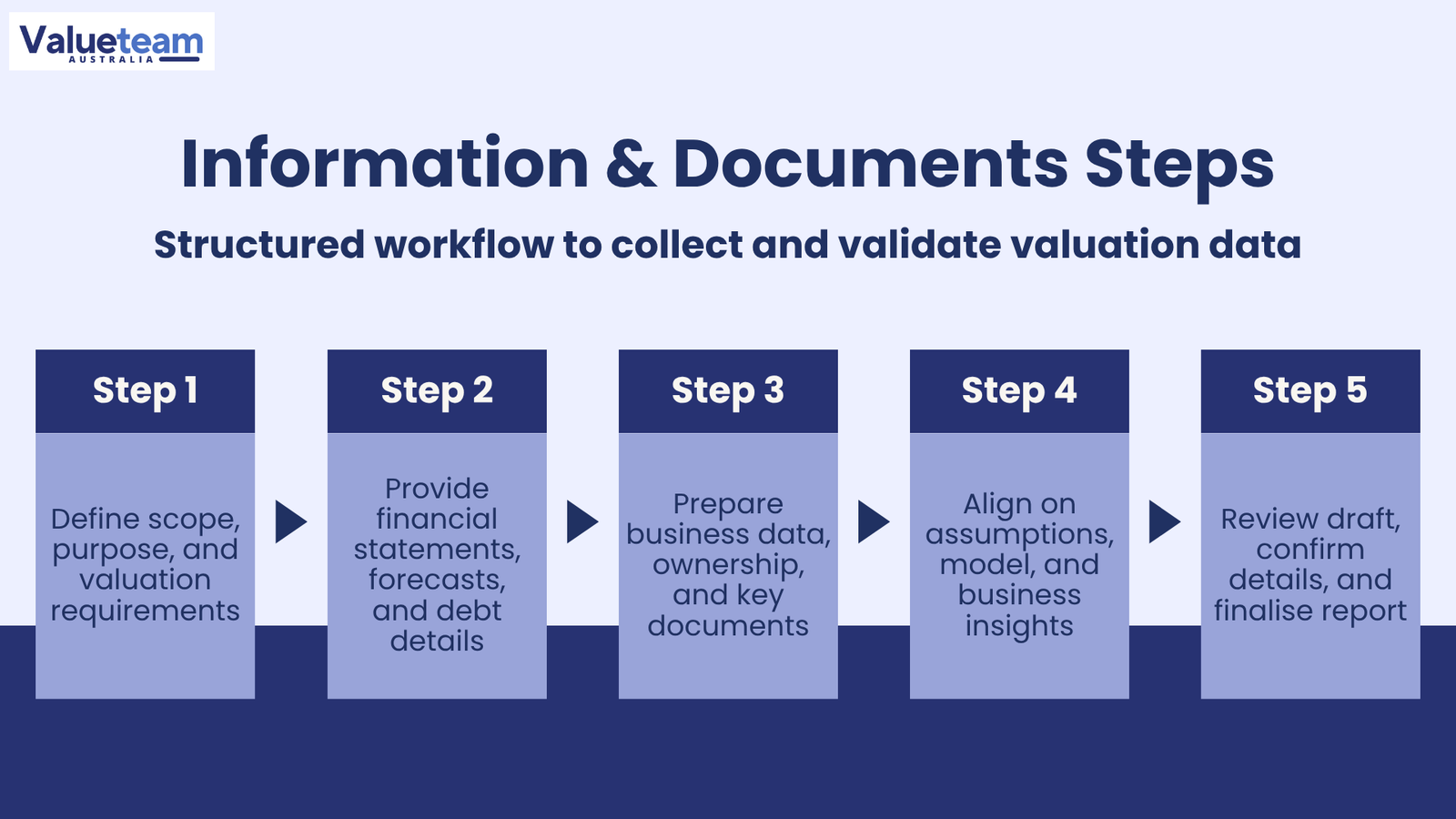

07Information and Documents Required — Five Key Steps

To conduct the valuation, a comprehensive financial and operational information package from management is usually needed. Instead of putting this as a checklist, the five steps below outline the information-gathering process as a structured engagement workflow – to collect the right information at the right place, facilitate a productive management dialogue, and generate a valuation conclusion based on the actual circumstances of the business.

Step 1 — Engage and Define Scope

It is not information gathering; it is clarity of purpose. The valuation adviser works with the client before seeking any documents to determine the valuation purpose, the standard of value to be used, the valuation date, and the interest to be valued.

- This scoping conversation identifies everything that will follow: what will be requested, how it will be done, and the format and content of the final report.

- A valuation done to support a private equity transaction will require different documentation and a different level of analysis than a valuation for a financial reporting impairment test.

- The engagement should be scoped before the information request.

Step 2 — Provide Financial Information

The basic financial information request is the quantitative foundation of the valuation analysis, and it directly establishes the quality and confidence of the valuation conclusion.

- Three years of financial statements (income statement, balance sheet, and cash flow statement) to determine the historical performance base.

- The last period of management accounts is to take a picture of the current period.

- Forward projections of budgets and forecasts with documented assumptions.

- A debt schedule that lists all the drawn facilities, terms, covenants and security arrangements.

- The quality of the valuation conclusion is directly influenced by whether the financial statements are audited or reviewed, whether the management accounts are prepared consistently, and whether documented assumptions support the forecasts. Step 3: Prepare Supporting Business Data.

Step 3 — Prepare Supporting Business Data

Financial data does not give the whole picture of a business. Facilitating business data gives the business a structural background to evaluate the quality and sustainability of the financial performance.

- The business plan is to give a strategic background to the financial projections.

- The ownership/cap table - to allow the assessment of the particular ownership interest being valued.

- Customer concentration data that displays the revenue distribution of the top customers.

- Large contracts, such as terms, renewals, and costs.

- Any litigation or legal issues that carry contingent liability.

- Compliance and ESG information, where appropriate, is becoming a standard component of the information package for transactions with institutional investors that have formal ESG screening.

Step 4 — Attend Management Discussion

The qualitative focus of the valuation engagement is the management discussion, which is usually held with the CEO and CFO and often with the major operational leaders.

- The valuation adviser investigates the business model and positioning, the assumptions underlying the financial forecasts, the significant risks and opportunities of the business, and anything that is not sufficiently reflected in the written information.

- Through this discussion, the valuer will make informed decisions on the quality of earnings, the soundness of projections, the strength of the management team, and the value drivers and risks that will ultimately lead to the valuation conclusion.

- The key is that companies that plan well (by considering their assumptions, addressing perceived weaknesses, and maintaining a consistent strategic story) are always better analysed than those that come to the discussion unprepared.

Step 5 — Review Draft and Finalise

The final step in the information and engagement process is review of the draft valuation report – a valuable opportunity, but with obvious limitations on what it can cover.

- Management also learns to spot and correct factual errors, justify the rationale for some assumptions, and ensure the report is true to the business case.

- It is not a negotiating opportunity: the professional valuation adviser's opinion on value should be independent and objective, and any corrections to facts should be based on evidence, not preference.

- After draft review and factual matters resolved, the final report is published - the professional opinion of the valuation adviser with analysis, evidence and documented methodology.

08 Our Valuation Process

Why Process Transparency Matters

A structured, transparent engagement process is one of the most significant quality indicators a valuation advisory firm can offer. This knowledge will assist clients in better preparing, setting more realistic expectations about the time and effort involved, and engaging their adviser more constructively at each stage.

- The time frame of a valuation engagement is largely dependent on the pace and completeness with which management may supply the requested information.

- Advisers can deliver high-quality valuations in a short period with fully prepared, well-organised information packages.

- The best thing a business can do when a valuation is required is to have its information package in order before the engagement process begins.

Table 2: Valuation Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — Initial Discussion | Know the purpose, extent and date of valuation; concur on the standard of value and interest being valued. | Client brief, purpose and context. | Engagement scope memo; signed engagement letter. |

Step 2 — Information Request | Provide a detailed information checklist to management; establish a data room/document exchange protocol. | Engagement scope | Formatted information request; set up data room. |

Step 3 — Management Discussion | Talk about business model, competitiveness, assumptions made to get projections, and critical risks. | Financial package; business plan; management accounts | Meeting notes; key assumption register; risk log |

Step 4 — Financial Analysis | Test and reconcile past financials; assess forecast quality; test key value drivers and risks. | 3 years financials; forecasts; management discussion notes | Normalised financial model; determined value drivers. |

Step 5 — Valuation Methodology | Choose primary valuation techniques and cross-check them; find similar companies and transaction information. | Normalised financials; industry research; databases of comparables. | Valuation model (DCF + market multiples / asset-based) |

Step 6 — Draft Report | Write a draft valuation report including complete methodology, assumptions, analysis and conclusion; send to the client so that they can review the facts. | Valuation model: all the financial and qualitative inputs. | Report on draft valuation to be reviewed by the management. |

Step 7 — Final Report | Dispose of factual review remarks; issue final report; give signed final opinion. | Review management’s comments on the facts. | Final signed report of valuation. |

09Valuation Methodologies by Situation

Why Methodology Selection Is Critical

The most practically important lesson of business valuation is that different situations require different methodological tools – and that the use of an inappropriate methodology, or the appropriate methodology without adequate adjustment to the specific situation, will lead to a valuation that is technically correct but of no commercial value.

- The table below summarises the key valuation approaches applicable in each situation and the most significant considerations for selecting the methodology.

- The similarity in all these situations is the necessity to apply the methodology that best represents the peculiarities of the business and the object of the valuation, and test the major finding with at least one alternative methodology.

- Valuations made according to a single methodology that has not been cross-checked are more readily contested: by an expert advisor to a sophisticated acquirer, by an auditor reviewing an impairment assessment, or by a rival expert in a court of law.

Table 3: Valuation Methodologies by Business Situation

Situation | Primary Methodology | Key Considerations | Common Cross-Check |

|---|---|---|---|

Startup / early-stage (pre-revenue) | Revenue mmultiple/optionpricing model | No historical profits; IP and market value-based value. | Scorecard / Berkus / VC technique of cross-reference. |

Startup / early-stage (revenue, pre-profit) | High discount rate / multiple revenue with high discount rate. | The key value driver is negative or minimal EBITDA and a growth trajectory. | Comparable VC transaction multiples |

Mature, profitable business — M&A | DCF + EBITDA market multiples | Quality of earnings; sustainability of growth; considerations of control premium. | Check run-through; NAV floor check. |

Asset-heavy / holding company | Net Asset Value (NAV) / adjusted book value | Fair value of underlying assets; any intangibles that are not fully recorded. | The income approach is used in conducting business. |

Financial reporting — purchase price allocation | Fair value AASB 3 / AASB 13. | All identifiable assets and liabilities have to be identified and valued. | Standalone real property and intangible asset appraisals. |

Goodwill impairment testing | Value in use (DCF) / FVLCD under AASB 136 | CGU definition, cash flow projections, WACC calibration | Cross-check in market capitalisation (listed entities) |

Shareholder dispute/litigation | Purpose-specific; based on court order or agreement. | Autonomy; transparency of methodology; commitments of the expert witnesses. | Various methods are used to prove robustness. |

Tax and transfer pricing | Arm-length market value per ATO guidelines. | Certain ATO methodology requirements and documentation requirements. | DCF and analogies to triangulate arm length price. |

10Indicative Timeline and Frequently Asked Questions

Understanding Engagement Timelines

The most significant issue for clients who hire a valuation adviser is timing. Business decisions often do not afford time for extensive analysis, and knowledge of the actual time frame within which a valuation engagement can be completed and what drives it is useful for planning.

- The indicative timelines below show average engagement times by complexity, based on the information available from management.

Table 4: Indicative Valuation Engagement Timelines

Assignment Type | Typical Timeline | Key Determinant | Notes |

|---|---|---|---|

Simple/indicative valuation | 3–5 business days | Quality and completeness of information given. | Discussable with the management. |

Standard business valuation | 1–2 weeks | Complicated business model and financial structure. | Assumes that the information is provided in time. |

Complex M&A or restructuring valuation | 2–4 weeks | Several organisations have a multinational, complicated capital structure. | May entail various valuation strategies and steps. |

Financial reporting valuation (PPA / impairment) | 2–5 weeks | List of acquired assets; complexity of identification of intangibles. | Needs to be coordinated with the audit team and the financial close schedule. |

Dispute/litigation valuation | Varies — court-driven | Scope of instructions; discovery process; expert conclave requirements | Open to independent review requirements and protocols of expert witnesses. |

How Is Business Value Calculated?

Business and company valuation uses three primary methodological approaches, which can be used individually or in combination, to provide a plausible valuation.

- Discounted cash flow (DCF) technique: Future cash flows are estimated and discounted to present value.

- Market method: Based on EBITDA multiples, revenue multiples, or prior transactions of similar companies.

- Asset-based approach: This approach is most suitable for holding companies and asset-intensive businesses.

- Professional valuations usually involve the use of a combination of methods and cross-check results to test the reasonableness of the primary conclusion.

Can Startups Be Valued Without Profits?

Yes. The valuation of equity shares of pre-profitable businesses is typically based on revenue multiples from similar venture-backed transactions, option pricing models, or milestone-based valuation models that account for the business stage and the metrics of value creation at that stage.

- Some relevant metrics include user counts, contracted revenue, the size of the addressable market, and IP strength.

- Not that there is no appropriate method, but rather the quality and credibility of the market data and assumptions upon which the method is founded are the challenge.

Do You Support Legal and Dispute Matters?

Yes, provided there are proper scope and independence requirements. Shareholder disputes, partner exits, court issues, and other required valuations are prepared to a higher standard of independence and documentation than commercial advisory valuations.

- These issues must be followed by the Expert Witness Code of Conduct that is applicable in the jurisdiction.

- In this regard, practitioners must be ready to defend their methodology and results in the face of cross-examination - the quality of the underlying analysis and documentation must become the primary concern.

11 Challenges and Lessons Learned

Managing Expectations

Managing expectations is the biggest problem with commercial valuation engagements. When business owners have spent years (even decades) developing a business, they tend to have an emotional connection to a figure of value that may have little to do with what the market will bear.

- When a strict, independently prepared valuation is well below expectations, the initial response is often to doubt the process rather than to respond to what the analysis is telling him.

- The finest valuation advisers work this dynamic with professional integrity and true empathy, making the analysis transparent, explaining why the particular factors have led to the conclusion, and what the client can do to bridge the gap between the present and desired value.

- A client who leaves a valuation engagement with a clear understanding of his/her value position and a clear way to improve it has been much better served than a client who was given a number he/she agreed with but was not clear on how to improve it.

The Information Quality Challenge

The second major challenge is information quality. Unrealistic forecasts, a lack of cap table information, unreported liabilities, and stale financials are prevalent in private company valuation engagements.

- The skilled practitioner establishes procedures for detecting such issues early and addressing them before they pollute the analysis.

- Lesson to junior practitioners: never assume, always verify. A revenue projection that assumes a 30 per cent growth rate per year in a market growing at 5 per cent is not information for the model; it is a question to answer.

- Unaccounted lapses in the table of cap are not a minor administrative issue - they are a possible substantial risk to the conclusion of the valuation.

- Systematic data quality testing, practised with professional scepticism and without apology, is one of the most important skills that a valuation practitioner can acquire.

Staying Current in an Evolving Field

The third difficulty is staying up to date with an ever-evolving discipline. The accounting standards, regulatory requirements, market data, and macroeconomic conditions change in ways that directly influence the quality of valuation work.

- Regulatory requirements for fair value measurement, purchase price allocation (PPA), and impairment testing are revised regularly in response to changes in accounting standards and evolving audit expectations.

- The market information that underlies similar listed companies and precedent transactions analysis varies with each transaction and each quarterly earnings report.

- Macroeconomic factors that influence the calculation of the discount rate/WACC include interest rates, equity risk premiums, and market volatility.

- The most regularly plausible valuations made by practitioners are those who regard the currency of their market knowledge, awareness of standards, and expertise in their sector as a professional responsibility, not a luxury.

12 Conclusion and Actionable Insights

Why Valuation Quality Matters

Business and company valuation is the art and science of coming up with an economic estimate of the value of a company, business unit, shares or ownership interest with the help of accepted valuation techniques and professional judgment – and it is a process that is important in more situations than most stakeholders fully realise until they find themselves in one.

- A good valuation provides an informed foundation to make decisions when you are raising capital, buying or selling a business, complying with financial reporting standards, or settling shareholder disputes.

- The organisations and individuals who approach the valuation process intelligently, understand its purpose, prepare thoroughly, and utilise the results to make better decisions will always achieve better results than those who treat it as an administrative obligation.

For Business Owners and Management Teams

The greatest practical implication of valuation for business owners and management teams is that planning for valuation begins years before the specific transaction or reporting occasion.

- The value drivers considered key, such as recurring revenue, customer diversification, depth of management, stability of margins, ESG, and quality of governance, are built over years through carefully planned strategic and operational decisions, rather than created in the weeks before an engagement.

- The owners of businesses that know their value drivers and work on them as a part of continuous strategic discipline will always have superior valuation results compared to those who do not think about value until they have to.

- The information request checklist is not merely a pre-engagement to-do list, but a business-readiness diagnostic that can yield operational improvements decades in the future.

Five Actionable Steps for Practitioners

For junior and mid-level professionals becoming experts in business and company valuation, the following five steps constitute a systematic growth plan.

- Step 1: Technical fluency in the three methodological families: the income approach (including DCF and sensitivity analysis), the market approach (including EBITDA multiples, revenue multiples, and precedent transactions), and the asset-based approach - not just how to do them but when and why to use which.

- Step 2 — Get acquainted with the regulatory backgrounds to determine valuation requirements: AASB 3 and purchase price allocation (PPA); AASB 136 and impairment testing; AASB 13 and fair value measurement; and the ATO requirements for tax reporting and transfer pricing support.

- Step :3 The methodology for developing genuine business and industry knowledge is no better than the judgment that is brought to bear on it, and good judgment cannot be made without profound acquaintance with the industries and business models that are being valued.

- Step 4 - Develop effective communication skills: the ability to communicate a valuation conclusion effectively, demonstrate major drivers and assumptions to a non-technical audience, and defend your position when questioned is as critical as the technical quality of the underlying analysis.

- Step 5 — Use each engagement as a learning experience: the most seasoned practitioners are those who proactively derive lessons from each engagement about what worked, what was challenged, and how the analysis might have been improved.

Our valuation advisory services help clients understand the fair value of their business and the significant forces that govern enterprise and equity value across all transaction, reporting, and dispute situations. It starts with identifying your specific needs and ends with a solution you can rely on. |

A great valuation does not just tell you the value of a business today; it also explains how and why, and what you can do to alter that figure. That is the conversation to have.