AML / KYC Compliance Advisory Australia

Table of Contents

- 01 Introduction

- 02 AML / CTF Regulatory Framework

- 03 AUSTRAC Obligations

- 04 Customer Due Diligence

- 05 Enhanced Due Diligence

- 06 PEP and Sanctions Screening

- 07 Ongoing Monitoring

- 08 Suspicious Matter Reporting

- 09 AML Program Documentation — Five Key Steps

- 10 Risk Assessment and Risk-Based Approach

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 AML / KYC Compliance Advisory Australia Framework

- 03 AUSTRAC Obligations

- 04 Customer Due Diligence

- 05 Enhanced Due Diligence

- 06 PEP and Sanctions Screening

- 07 Ongoing Monitoring

- 08 Suspicious Matter Reporting

- 09 AML Program Documentation — Five Key Steps

- 10 Risk Assessment and Risk-Based Approach

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

Financial Crime and the Compliance Imperative

Financial crime is not trumpeting itself. It is moved quietly through clean banking systems, trading systems, real estate transactions, and electronic payment systems, exploiting gaps in compliance regimes, lax customer vetting processes, and inadequate monitoring systems to launder the proceeds of heinous crimes.

- Anti-money laundering and know-your-customer compliance aim to close those loopholes.

- The Australian Transaction Reports and Analysis Centre (AUSTRAC) is one of the most prolific financial intelligence agencies in the world, which anchors this effort in Australia.

- Knowledge of how to create, establish, and run a compliance program that meets AUSTRAC requirements is not merely a regulatory requirement but a major professional competency for anyone in financial services, professional services, or corporate advisory.

The Scale of the Problem

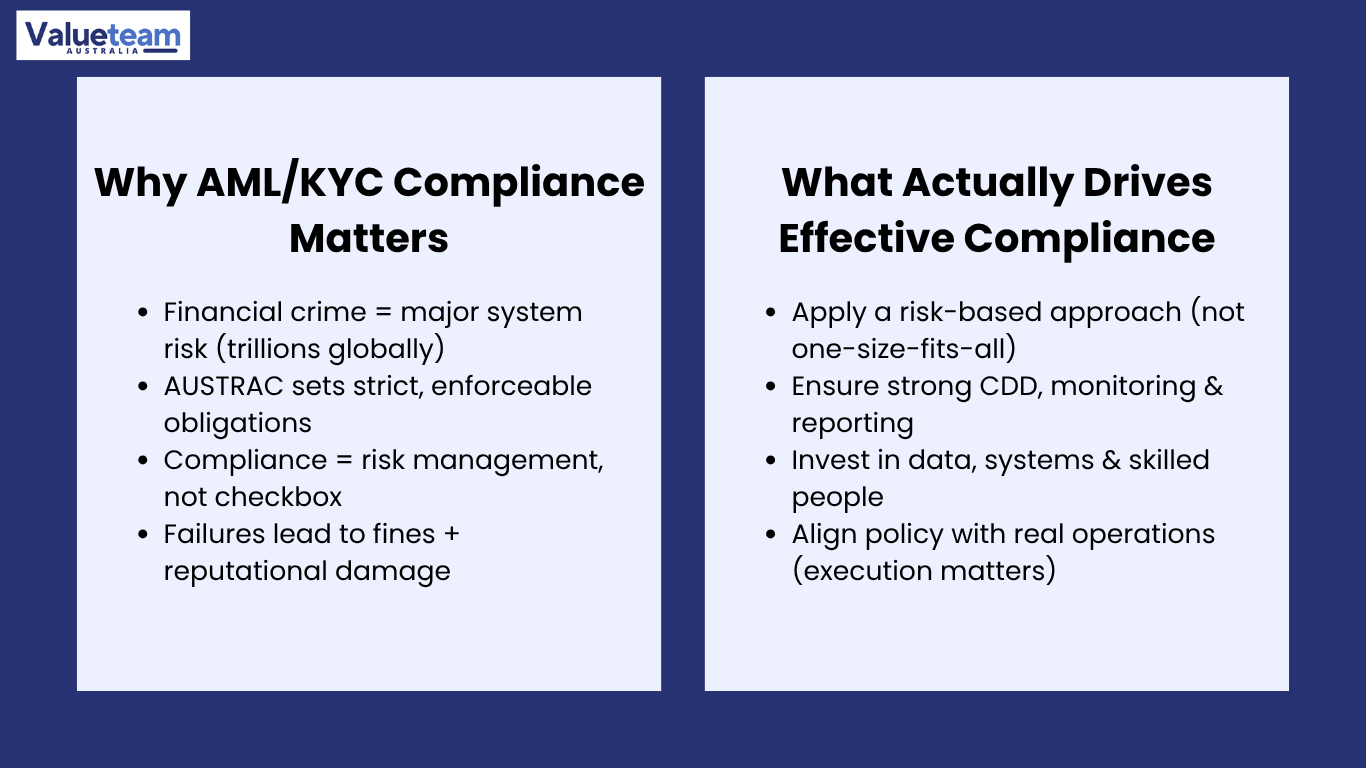

The scale of the problem that the AML/KYC compliance solves is not abstract. It is one of the greatest current risks to the soundness of the global and Australian financial systems.

- Money laundering is estimated to be 2-5% of world GDP each year, trillions of dollars circulating in the financial system disguised, funding drug trafficking, human trafficking, terrorism and evasion of sanctions.

- Geographic location: Australia has an open economy and a developed financial system, which makes it an easy target for criminals.

- The AUSTRAC's risk-based AML/KYC expectations fall in the middle of the compliance requirements for reporting entities, spanning all areas of program design, from initial risk assessment through continued monitoring and reporting of suspicious matters.

- The impact of system failures, as experienced by numerous global institutions, can amount to fines of hundreds of millions of dollars and long-term reputational damage.

Who This Guide Is For

The guide is designed to help junior to mid-level professionals build or expand their understanding of AML and KYC compliance, whether you are in a compliance department, a financial crime unit, an audit or advisory position, or entering the sector as a law, accounting, or risk management graduate.

- Discusses the architecture of a successful AML/CTF program in logical order, starting with the regulatory framework and entity requirements behind it, to the customer due diligence, enhanced due diligence, and PEP and sanctions screening.

- Covers the operational aspects of continuous monitoring, reporting suspicious matters, AML program documentation, and independent review.

- Intends to offer organisation, language, and practical knowledge to contribute practically on the first day.

AML/KYC compliance is not a tick-the-box exercise; it is a risk management area. The number of pages does not determine the value of a policy manual; rather, it is how well it can detect, intercept, and hinder the circulation of criminal money in and out of the financial system. |

02 AML / KYC Compliance Advisory Australia Framework

The Legislative Foundation

The Australian AML/CTF regulatory framework includes the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) and its Rules – a legislative framework that has been continuously improved since it was enacted and is now going through its most significant reform in nearly 20 years.

- The AML/CTF Act outlines the responsibilities of reporting entities - businesses that offer specified services as outlined in the Act.

- AUSTRAC has important rule-making authority to elaborate on how these obligations are met.

- The key to meeting all downstream compliance requirements is understanding the structure of this legislation.

Two Tiers of Designated Services and the Tranche 2 Reforms

The AML/CTF regulatory system divides designated services into two groups, and major changes are being made that will significantly increase the number of entities subject to the framework.

- Tier 1 - financial services - is the most regulated category, and includes banking, lending, currency exchange, payment services, securities dealing, superannuation, and insurance.

- The reforms of tranche 2 will be expanded to encompass more professional service providers such as real estate agents, lawyers, accountants, and dealers of high-value goods - areas that FATF has long considered a high financial crime risk in Australia.

- The Tranche 2 reforms represent the largest increase in the AML/CTF regulatory regime since the Act was established. They will place a significant number of businesses and professionals under AUSTRAC's regulatory regime for the first time.

The International Dimension — FATF and Australia

As professionals move into the compliance arena, it is equally important to understand the international AML/CTF regulatory environment as it is to understand what is needed domestically.

- The AML/CTF regime in Australia is aimed at the enforcement of the FATF Recommendations - the global standard of anti-money laundering and counter-terrorism financing.

- The risk-based AML/KYC expectations of reporting entities in Australia reflect the risk-oriented approach embedded in FATF's global regime.

- The FATF also conducts periodic mutual reviews of its member countries' compliance, and Australia's performance in these reviews directly influences the regulatory expectations AUSTRAC imposes on reporting entities.

- Familiarity with the FATF Recommendations offers a concept map that clarifies how every particular requirement within the local framework came into existence and the rationale behind it.

03AUSTRAC Obligations

The Core Set of Obligations

The AML/CTF Act and Rules impose obligations on AUSTRAC, including the methods by which a reporting entity must address the threats of financial crime to which it is exposed. When these requirements are met properly, they make the Australian financial system much less susceptible to criminal exploitation.

- Register with AUSTRAC before offering specified services.

- Find out and confirm the customers they are dealing with.

- Track business dealings and transactions continuously.

- Notify AUSTRAC about suspicious issues and threshold transactions.

- Have a program on AML/CTF that addresses Part A (the enterprise-wide risk assessment and management framework) and Part B (the customer due diligence program).

- Keep records that allow reconstruction of financial transactions.

The Risk-Based Approach in Practice

Risk-based AML/KYC expectations of AUSTRAC remain the focal point of reporting entities in Australia – how obligations are construed and implemented in practice.

- A bank that receives and sends large amounts of international wire transfers to high-risk jurisdictions will have a radically different risk profile than a domestic payment processor serving small retail businesses, and AUSTRAC anticipates that each will have a compliance program designed to reflect its risk profile.

- The risk-based approach implies that no standard set of controls is prescribed, and all entities should use them in the same way.

- Reporting entities should assess the types of money laundering and terrorism financing risks they are exposed to, the likelihood and seriousness of those risks, and adopt controls appropriate to their risk profile.

- This, though, is both the strength and the challenge of the AUSTRAC obligations framework: it is flexible, but flexibility requires real analytical judgement.

The Consequences of Non-Compliance

The enforcement actions by AUSTRAC have, in certain instances, provided graphic examples of the repercussions of non-compliance, serving as a warning to practitioners.

- High-profile litigation of financial institutions in Australia has resulted in civil penalty proceedings, enforceable undertakings, and settlements of unprecedented scale ordered by the court.

- The underlying reasons were not exotic or highly technical: they were design failures in basic compliance programs, failures of consistent monitoring regimes to spot suspicious patterns, governance failures that permitted known weaknesses to persist, and a culture that viewed compliance as a cost centre rather than a risk management discipline.

- AUSTRAC obligations are not tender obligations. They are enforceable in law and backed by some of the highest civil penalties in Australian commercial law.

04 Customer Due Diligence

The Foundation of the KYC Requirement

The basis of the KYC requirement is customer due diligence (CDD), the process by which a reporting entity recognises its customers, assesses the nature and purpose of the business relationship, and collects the information necessary to oversee it continuously.

- CDD must be either before or concomitant to the initiation of a specified service.

- It consists of three basic elements: customer identification (collection of information about the customer), customer verification (matching the information to credible and independent sources), and beneficial ownership identification (determining who the ultimate owner or controller of a legal-entity customer is).

CDD Requirements by Customer Type

The customer due diligence requirements vary according to the customer’s nature, with greater complexity added as the legal structure becomes more complex.

- Personal customers: Full name, date of birth, and address of residence are usually mandatory and confirmed by a government-issued identity document, such as a passport or driving licence.

- Corporate customers: The reporting entity should verify the entity's existence and registration, its directors and senior officers, and identify beneficial ownership by any chain of holding entities to the ultimate natural person owner.

- Trusts, partnerships, and other non-corporate structures: The entity type must be correctly mapped with the appropriate identification requirements.

- The use of digital identity verification technology has altered how CDD is practically implemented in various ways. However, it is not a legal requirement; verification must still meet satisfactory standards under the AML/CTF Rules.

CDD as an Ongoing Discipline, Not a One-Off Event

Among the greatest practical lessons concerning customer due diligence, it is important to note that it is a dynamic process, rather than a one-time compliance event during onboarding.

- The data collected during the onboarding process serves as the benchmark against which subsequent transactions and behaviours are measured.

- When a customer alters circumstances- a shift in beneficial ownership, a shift in business activity, not the one outlined at the time of onboarding, or a shift in source of funds- the CDD record should be revised to indicate the change.

- Reporting entities that use KYC as a checkbox when opening an account, rather than as a data management and monitoring discipline, are bound to create discrepancies between their customer data and the actual risk profile of their customer base.

- These gaps not only impede the effectiveness of the continuous monitoring but also the quality of reporting suspicious matters.

05Enhanced Due Diligence

When EDD Is Required

Enhanced due diligence (EDD) is an enhanced version of the standard customer due diligence process applied to customers and business relationships that have a greater likelihood of money laundering or funding terrorism.

- The AML/CTF Act and Rules require EDD in certain situations, such as when dealing with a politically exposed person (PEP), an unusual or high-value business relationship or service, or when the entity itself has determined that the customer or relationship is high-risk.

- The risk-based AML/KYC expectations of AUSTRAC remain the focus for reporting entities in Australia, and EDD is the main tool used to apply greater scrutiny to higher-risk relationships.

What Enhanced Due Diligence Involves

Enhanced due diligence is far beyond the usual identification and verification procedures; it involves a more thorough understanding of the customer’s financial situation and the nature of the relationship.

- Inquiring further information about the origin of the customer and their source of money - not who the customer is, but where their money is.

- Building a more comprehensive understanding of the business relationship's purpose and nature.

- Carrying out a more intensive analysis of the beneficial ownership structure.

- Adding more scrutiny to the transactions conducted in the relationship.

- The establishment or maintenance of high-risk relationships must be approved by senior management.

- EDD may also involve negative media screening, external intelligence gathering, and other transaction-monitoring parameters specific to the customer's risk profile, particularly when the customer is of very high risk.

Real-World Case Study: The Cost of Under-Escalating EDD

One lesson learned from a regulatory review of a mid-sized European private bank was that it had used standard CDD procedures for a category of customers who were evidently meant to have received an escalation of due diligence, underscoring the impacts of under-escalation.

- The targeted customers were international private clients with complex multi-jurisdictional wealth structures, a profile that clearly exceeded the institution's EDD trigger criteria.

- The review established that more than 60 per cent of this group had no documentation of their sources of wealth on file and that senior management approval to accept high-risk relationships had become a rubber stamp rather than a real test.

- Some of the remediation programs required a full retrospective EDD refresh for the impacted customer base, a redesign of the EDD approval process, and specific training for relationship managers on the improved due diligence requirements.

- Lesson: EDD should be a real enhancement of the due diligence process - not just more of the same poor process.

06 PEP and Sanctions Screening

What PEP and Sanctions Screening Is

PEP and sanctions screening is the process by which reporting entities identify customers, beneficial owners, and related parties who are politically exposed persons or listed on sanctions lists maintained by domestic and international authorities.

- These two screening requirements differ, yet are often performed using the same screening system.

- The two are indispensable components of a good AML/KYC program.

- Although in many areas of AML/CTF compliance, design is at the discretion of the entity, the AML/CTF Act and Rules are not prescriptive regarding the measures to be taken to screen PEPs and conduct sanctions screenings; these are not risk-based design decisions, but rather prescriptive ones.

Politically Exposed Persons — Identification and Obligations

A politically exposed individual (PEP) is any individual who has or has held a high government position – heads of state, high-ranking politicians, high-ranking military officers, high-level executives of state-owned corporations and their close relatives and close associates.

- PEPs are high-risk money launderers because of their roles, which could offer opportunities and motives to misuse public funds, accept bribes, or obtain illicit funds in other ways.

- A PEP identification does not imply that the business relationship should be rejected; rather, it indicates that due diligence should be strengthened, senior management should sanction the relationship, and continuous monitoring should be increased.

Sanctions Screening — Harder Obligations

Sanctions screening has even more rigorous requirements than PEP identification. The compliance response is fundamentally different when one of the customers or counterparties is matched with a sanctions list.

- Sanctions lists maintained by DFAT (Australian Department of Foreign Affairs and Trade), the UN Security Council, and other relevant bodies should be screened.

- When a customer or counterparty is determined to be a sanctioned person or entity, it is often impossible to transact business with them, and the issue should be reported to the appropriate internal and external authorities as soon as possible.

- Sanctions screening is not a one-off onboarding process but rather an ongoing process since sanctions regimes and lists are constantly updated, and in some cases, at a very fast rate in reaction to geopolitical developments.

- The operational criterion for any reporting organisation with a large customer base is automated screening technology that provides real-time or near-real-time notifications when existing customers are found on updated lists.

- The quality of screening, including list coverage, matching logic, and the review and disposition of alerts, is among the areas of concern during AUSTRAC examinations and independent reviews.

07 Ongoing Monitoring

The Operational Core of AML/KYC Compliance

The essence of AML/KYC compliance is ongoing monitoring, i.e., continuous monitoring of the activity and behaviour of the customer base by a reporting entity, intended to identify activity inconsistent with the customer’s pre-existing profile and report it for investigation and possible reporting.

- Even the most thorough CDD and EDD processes are just a picture of the risk situation at the moment of onboarding - they are not able to predict how customer behaviour can evolve.

- Criminal behaviour is generally exhibited through changes over time, and it is during this period that the capacity for ongoing monitoring to identify it is most useful.

- Risk-based AML/KYC expectations of reporting entities in Australia still recognise ongoing monitoring as an essential aspect of the compliance assessment framework of the compliance assessor, AUSTRAC.

Rules-Based and Behavioural Monitoring

A successful continuous monitoring system should combine two complementary surveillance approaches: rule-based transaction monitoring and behavioural analytics.

- Rules-based monitoring: Notifies about specific transaction patterns according to pre-defined thresholds and typologies.

- Behavioural analytics: Establishes a baseline of normal activity at the individual customer level and notifies when activity is substantially different from the baseline.

- Some of the common typologies that effective monitoring systems are constructed to detect are: structuring (the deliberate disaggregation of transactions to evade reporting thresholds), layering (the movement of money across accounts very quickly to conceal origin), unusual international wire activity, transactions that do not match the profile or income of the customer, and sudden changes in the volume of transactions or pattern.

- Scenarios and thresholds should be entity-specific to its risk profile and customer base - a common and major compliance risk is an off-the-shelf monitoring configuration that has not been customised to the entity-specific business.

The Human Dimension — Analysts and Escalation

The human aspect of continuous surveillance is equally important as the technology. Automated systems create alerts; they need to be interpreted by trained analysts.

- Queues of alerts increasing faster than the analyst capacity is a typical failure mode that undermines the performance of even technically advanced monitoring systems.

- Analysts with little knowledge of their sector (unable to determine the commercial context of suspicious transactions) will not reliably distinguish real suspicious activity from explicable transaction patterns.

- Pathways of escalation that are not well understood or consistently applied imply that even properly identified suspicious activity does not reach decision-makers.

- All three failure modes can be prevented by investing in analyst training, well-defined escalation procedures, and proper staffing for the monitoring role.

08 Suspicious Matter Reporting

The Intelligence-Generating Obligation

The reporting mechanism of the AML/CTF Act that places some of the most direct intelligence-generating requirements on reporting entities is known as suspicious matter reporting (SMR), which obligates reporting entities to provide information to AUSTRAC regarding customers or transactions where there is a reasonable suspicion of money laundering, financing of terrorism, or serious criminal offending.

- Based on this information, AUSTRAC creates a financial intelligence image that helps law enforcement agencies with their investigations, asset recovery, and national security operations.

- The quality and timeliness of reporting suspicious matters are not just regulatory issues; they are of utmost importance to the overall effectiveness of Australia's financial crime response.

When to Report and the Tipping-Off Prohibition

Two of the most practically significant aspects of reporting suspicious matters are knowing when the obligation to report arises and what may not be done after a report is made.

- The filing obligation of an SMR is caused by suspicion, a standard that is below certainty or reasonable belief. Reporting entities should not wait until they have the entire picture before filing.

- The reporting obligation is absolute, and it is accompanied by a tipping-off prohibition: the entity should not inform the subject of the report that an SMR has been made.

- One of the most pragmatic problems with SMR is how to balance the need to keep serving a suspicious customer without drawing their attention to the investigation, with the risk management aspect of maintaining the relationship.

Quality Over Quantity — The Intelligence Value of SMRs

There is a growing regulatory emphasis on the quality of suspicious matter reporting, rather than its quantity. Having a large number of reports is not very useful if they are not actionable.

- Reports that only state the factual situation of a transaction, do not justify why the situation is suspicious or why the activity falls under a known typology, and do not provide contextual information to guide intelligence action are of little value to AUSTRAC and law enforcement.

- High-quality SMR will demand analysts with extensive knowledge of the financial crimes typologies - able to detect suspicious patterns, reasons why they are suspicious, and what contextual information will make the report most helpful to the regulator.

- This is an art that is developed by experience, conscious learning and specific training - and investing in this ability is one of the best-paying projects that any compliance department can undertake.

Table 1: AML/KYC Obligations — Summary Reference for Reporting Entities

Obligation | Legal Basis | Key Requirement | AUSTRAC Focus Area |

|---|---|---|---|

Enrolment | AML/CTF Act s.76 | Pre-register and then offer assigned services as a reporting entity. | Fullness and completeness of enrolment information. |

Customer Due Diligence | AML/CTF Rules Ch. 4 | Verify and identify customers; verify beneficial owners. | Standards of verification; fullness of beneficial ownership tracing. |

Enhanced Due Diligence | AML/CTF Rules Ch. 4 | Enforce extra vigilance with risky customers and relationships. | Suitability of EDD triggers; the quality of the source of wealth documentation. |

PEP and Sanctions Screening | AML/CTF Rules; Autonomous Sanctions Act | Screen PEPs and sanctions-listed customers at onboarding and throughout ongoing operations. | List coverage, matching logic, alert review and disposition process |

Ongoing Monitoring | AML/CTF Act s.36 | Keep track of transactions and business relationships in real time. | Calibration of scenario, quality of alerts, capacity and ability of analysts. |

Suspicious Matter Reporting | AML/CTF Act s.41 | Report suspicious activities to AUSTRAC as soon as possible (within 24 hours of terrorism financing) | Timeliness and quality of reports; tipping off prevention. |

Threshold Transaction Reporting | AML/CTF Act s.43 | Report any cash transactions of AUD 10,000 or above to AUSTRAC. | Complete or complete in TTRs; accuracy of customer identification in TTRs. |

Record Keeping | AML/CTF Act s.105 | Maintain CDD, transaction and compliance records for 7 years. | Availability of records to be analysed. |

09AML Program Documentation — Five Key Steps

What AML Program Documentation Is

AML program documentation is the formal report of the compliance framework of a reporting entity – the set of policies, procedures, risk assessments, and governance documents that explain how the reporting entity identifies, controls, and limits its money laundering and terrorism financing risks.

- Under the AML/CTF Act, all reporting entities should have an AML/CTF program that is broken down into two parts: Part A (that is, the enterprise-wide risk assessment and general governance framework), and Part B (that is, the specific customer due diligence, enhanced due diligence, ongoing monitoring, and other customer-facing requirements).

- The following five steps provide a methodological approach to creating AML program documentation that is both operationally and regulatorily compliant.

Step 1 — Conduct a Risk Assessment

A sound AML program documentation exercise commences with a stringent risk assessment conducted in accordance with the risk-based approach.

- Determine the money laundering and terrorism financing risks inherent to the business model of the entity - the nature of the products and services it offers, the nature of its customers, the route it uses to deliver its services, and the jurisdictions it faces.

- The risk assessment cannot be a hypothetical activity: it needs to be based on the entity's own transaction data, the typology reports of AUSTRAC and FATF, and the specific vulnerabilities of the environment in which the entity operates.

- A risk assessment that enumerates generic risk types without tying them to the entity's details will not meet the expectations of the AUSTRAC risk-based AML/KYC framework.

Step 2 — Design Part A and Part B of the AML/CTF Program

After the risk assessment is complete, the entity must design its AML/CTF program with all necessary components.

- Part A: Documents the board and executive governance policies, appointment of the compliance officer and their responsibilities, the risk management policy throughout the organisation, staff due diligence and screening policies and the independent review of the program policies.

- Part B: Documents the specific due diligence procedures for customers, including customer due diligence types, circumstances warranting increased due diligence, PEP and sanctions screening, and the monitoring framework.

- The two sections must be precise enough to be helpful to staff and detailed enough to demonstrate to AUSTRAC that the entity has taken its compliance obligations seriously.

Step 3 — Implement Policies and Procedures

Compliance theatre is an AML program contained within a policy manual that has never been implemented in the day-to-day operations that the staff actually perform. The most important challenge in implementation is bridging the gap between program design and operational reality.

- The operations need to be defined for each type of staff: relationship managers, operations teams, compliance analysts, and customer service officers, including what, when, and how each group should do.

- These procedures should be incorporated into the technology systems and processes that employees actually work with: the CDD platform, the transaction monitoring console, and the case management system for reporting suspicious matters.

- Procedures in a different document that the staff will never look at will not result in compliant behaviour.

Step 4 — Train Staff and Embed the Culture

The most technologically advanced AML program will not work if the individuals implementing it are unaware of their duties or do not take them seriously. A yearly online module is not enough to train the employees on effective AML.

- All new employees should be trained in induction.

- Functional training on functions that have increased exposure to AML, especially relationship management and transaction monitoring.

- Refresher training in case of a change in typologies or the introduction of new rules.

- Scenario-based training to create authentic analytical skills and not rote knowledge of processes.

- In addition to training, a real compliance culture cannot be developed without top management serving as a role model, holding individuals accountable when compliance fails, and establishing a culture of whistleblowing in which employees feel free to voice their concerns without fear of reprisal.

Step 5 — Conduct Independent Review

The AML/CTF Act requires reporting entities to conduct an independent evaluation of their AML/CTF program at least once every three years, or more often if the entity’s risk profile or regulatory environment has significantly changed.

- The independent review should consider the sufficiency of the program, the efficiency of its implementation, and whether it continues to reflect the entity's current risk profile.

- It should be done by a person who is not involved in day-to-day compliance duties, i.e., usually the internal audit team, which is sufficiently independent of the compliance function, or an external adviser.

- The outcomes of the independent review should be reported to the board or the appropriate committee, and the gaps identified should be addressed through a written remediation plan.

10Risk Assessment and Risk-Based Approach

The Conceptual Core of Modern AML/KYC Compliance

The conceptual framework of contemporary AML/KYC compliance is the risk assessment and the risk-based approach. The principle is that compliance resources, time, technology, and human capacity should be commensurate with the level of risk, with more intensive measures applied to higher-risk customers and transactions.

- It provides theaRisk-based AML/KYC expectations from AUSTRAC remain a key focus for reporting entities in Australia. basis for the organisation's climate-related disclosures under AASB S2.

- The quality of the risk assessment and risk-based approach is the most important factor in deciding whether a compliance program will be up to the expectations of AUSTRAC - and, more fundamentally, whether it will be effective in detecting and preventing financial crime.

Assessing Inherent Risk Across Four Dimensions

The initial step in the rigorous risk assessment is to identify inherent risk – the money laundering and terrorism financing risk inherent in the business of the entity before the application of any controls. This is evaluated on four big dimensions.

- Customer risk: What kind of customers does the entity provide, and how risky are those customers?

- Product and service risk: To what extent are the entity's products and services vulnerable to money laundering or financing terrorism?

- Channel risk: What are the channels used by the entity to provide its services, and to what extent do the channels permit anonymity or hide the audit trail?

- Geographic risk: What jurisdictions is the entity exposed to in its operations and its customer base,e and to what extent is it exposed to high-risk or sanctioned geographies?

- This four-dimensional evaluation is the foundation for the calibration of the entity's controls: where standard CDD is suitable, where the entity must conduct more due diligence, and where the entity must not provide services at all.

The Risk Assessment as a Living Document

Risk assessment and risk-based approach should not be a one-time event but a living document. Several forms of change need to be reevaluated.

- Internal changes: The entity's risk profile can be significantly changed by the introduction of new products, new customer segments, new distribution channels, or new jurisdictional exposures, and the risk profile can be reviewed.

- External changes: New criminal typologies, new FATF guidance, new AUSTRAC regulatory expectations, and geopolitical changes that impact sanctions or high-risk jurisdiction designations should all be included.

- Organisations that update their risk assessment at the same frequency as their normal governance processes are better positioned to ensure their program aligns with their actual risk profile than organisations that only update their risk assessment at the independent review cycle.

Table 2: Risk Assessment Framework — Customer Risk Factors Entities

Risk Factor | Lower Risk Indicators | Higher Risk Indicators | Program Response |

|---|---|---|---|

Customer type | Home-based person; paid employee; well-established SME. | PEP; no face-to-face; complicated corporate structure; anonymous beneficial owner entity. | Standard CDD vs Enhanced Due Diligence; approval by the senior management. |

Source of funds | Regular salary; documented business income; known investment proceeds | Business with high cash needs; sells assets with high value; uncertain or unprovable source. | Documentation of source of funds and source of wealth; detailed EDD. |

Jurisdiction | Low risk FATF-compliant country; local customer. | FATF grey/blacklist country; high-corruption index; sanctions-adjacent jurisdiction | Improved screening, increased transaction monitoring, and geographic limits. |

Transaction behaviour | Aligns with the intended mission, foreseeable trends, and a complementary business portrait. | Building patterns; quick layering; at variance with customer profile; unaccounted variations. | Notification of alert escalation; review relationships; consideration of Suspicious Matter Report. |

Channel | In person; Confirmed online onboarding, including a biometric verification. | Online, intermediary presentation, agent network, anonymous online. | The improved identity verification, ECDD, and continuous monitoring uplift. |

Table 3: AML/KYC Compliance Program — End-to-End Process Flow

Phase | Key Activities | Responsible Party | Output |

|---|---|---|---|

1. Risk Assessment | Determine the inherent ML/TF risks by customer, product, channel, and geography; record the risk evaluation. | Compliance Officer + Risk | AML/CTF risk evaluation (Part A element) |

2. Program Design | AML/CTF program design Part A and Part B; document policies and procedures; get board approval. | Compliance + Legal + Board | Board-approved AML/CTF program |

3. CDD Implementation | Introduce customer identification and verification processes, CDD technology, and educate frontline personnel. | Compliance + Operations + IT | Operating CDD procedure; certified records of customers. |

4. EDD and Screening | Introduce EDD triggers and procedures; roll out PEP and sanctions screening; create a high-risk approval process. | Compliance + Technology | EDD framework; live screening ability. |

5. Ongoing Monitoring | Create a transaction-monitoring scenario, tune thresholds, create an alert-review process and an analyst team. | Compliance + Analytics + IT | Live transaction monitoring; alert workflow. |

6. SMR Process | Create a suspicious matter escalation pathway; educate train analysts on SMR quality; set up an AUSTRAC reporting portal. | Compliance + Legal | SMR process; ability to lodge. |

7. Record Keeping | Introduce 7-year retention of records, CDD, transaction, and compliance records. | Compliance + IT + Operations | Adhering to the record management system. |

8. Independent Review | Involve internal audit/external adviser; audit scope against requirements of AML/CTF Act; report to board; remediate. | External Adviser + Board/Internal Audit. | Remediation plan; independent review report. |

11 Challenges and Lessons Learned

Challenge 1 — The Gap Between Program and Operational Reality

The most endemic failure mode in AML/KYC compliance is the gap between the documented program and actual operational behaviour, and it has the most severe regulatory implications.

- A compliance program is not a properly written AML/CTF program in a shared drive, relationship managers onboarding customers without adequate CDD, compliance analysts clearing monitoring alerts without investigation, and the compliance officer having no visibility into what is actually going on. It is a liability.

- The organisations that escape enforcement action are not the ones with the most elaborate documentation; they are those that have succeeded in aligning the program with what people are actually doing.

- That alignment demands investment in training, in technology that embeds compliance requirements into business processes, in management information systems that provide the compliance function with real-time visibility, and in a culture that sees compliance requirements as a real business requirement, not an externally imposed cost.

Challenge 2 — Data and Technology Infrastructure

- The effectiveness of AML/KYC compliance is increasingly dependent on the quality of the underlying data and technology systems.

- Common outcomes of organisations with ageing technology architectures, multiple disconnected data sources, or poor data quality management include finding that monitoring systems raise alerts on incomplete or incorrect data, that CDD records are inconsistent across systems, and that generating accurate and complete AUSTRAC reports is a titanic manual task.

- These technological and data issues are expensive and time-consuming to fix, which is exactly why the organisations best prepared for AML compliance are those that invested in technology willingly, rather than being compelled to do so by regulatory pressure.

Challenge 3 — Talent and Capability

Professionals who are both highly competent in financial crime typologies, with the ability to perform sophisticated data analysis, and with the ability to apply investigative judgement are truly hard to locate and nurture, and are essential to effective AML/KYC compliance.

- The AML compliance professional market is competitive, and the impact of under-trained or under-supported personnel in key areas, especially in suspicious matter reporting and the continuous monitoring alert review role, is severe.

- The organisations that best navigate this dilemma are those that invest in structured professional development for compliance staff, are members of professional associations and training bodies, and have career structures that do not just reward compliance expertise but also make the function a cost to be minimised.

12 Conclusion and Actionable Insights

Why AML/KYC Compliance Is a Consequential Field

One of the most professional and socially important areas of the financial services and advisory environment is AML/KYC compliance. The network of obligations that arises from AUSTRAC’s risk-based AML/KYC expectations is not a liability to be reduced to a minimum, but a risk-management capacity to be invested in.

- The risk-based AML/KYC expectations of reporting entities in Australia are core to the Australian regulator, AUSTRAC's, audit of AML programs, and the requirements that derive from those expectations form an interdependent system.

- Organisations that view the system as a compliance cost are always at risk of being forced to comply, whereas those who view it as a genuine risk-management investment are not.

- The resiliency and credibility of those who invest in developing real capability safeguard the business and add to the integrity of the financial system as a whole.

Five Actionable Steps for Practitioners

The five steps below offer a systematic growth model to junior and mid-level professionals to develop expertise in AML/KYC compliance.

- Step 1 — Gain a comprehensive working understanding of the AML/CTF regulatory framework: the AML/CTF Act and Rules, the FATF Recommendations, and the AUSTRAC guidance documents and typology reports that operationalise those standards into the operational expectations. It is the basic knowledge on which all the more specialised skills are based.

- Step 2 - Learn risk assessment and risk-based strategy: identify and categorise risk factors across customer, product, channel, and geographic dimensions, and translate the risk assessment into corresponding, effective controls.

- Step 3: Build real skills in customer due diligence and enhanced due diligence,e not merely what documents to collect, but what the information collected tells us about the risk profile of a customer or relationship, and what the red flags are telling us.

- Step 4 — Develop professionalism in the quality of suspicious matter reporting: learn to recognise financial crime typologies, be able to effectively describe the basis of suspicion, and create reports that are actually of value to AUSTRAC and law enforcement - not merely technically correct.

- Step 5 — Find exposure to independent review engagements, as either a participant or a reviewer: objectively reviewing an AML program, uncovering actual weaknesses, and converting the results into plausible remediation strategies is one of the most marketable skills in the whole compliance advisory business.

The best AML compliance professionals are not only the most knowledgeable about the rules, but also those who are aware of the criminal behaviour the rules are meant to identify, and who construct systems resilient enough to detect it. Financial crime prevention is, however, about protecting people, not just against exploitation, but against the fruits of violence and corruption, and against a financial system that is used against them. |

AML/KYC compliance, when properly executed, is not a burden on the business but rather the effort to ensure that the financial system is more difficult for criminals to abuse and easier for all other parties to use. A career is worth developing if it aims