Impairment Testing Guide in Australia

Table of Contents

- 01 Introduction

- 02What Is Impairment Testing?

- 03 Why Do Clients Need Impairment Testing?

- 04 When Is Impairment Testing Required?

- 05 Key Concepts in Impairment Testing

- 06 Key Valuation Approaches

- 07 Key Drivers That Affect Impairment Results

- 08Common Mistakes in Impairment Testing

- 09Five Key Steps: The Impairment Testing Process

- 10Our Impairment Testing Process

- 11 Valuation Approaches by Asset and Situation

- 12 Indicative Timeline and Frequently Asked Questions

- 13 Challenges and Lessons Learned

- 14Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is Impairment Testing?

- 03 Why Do Clients Need Impairment Testing?

- 04 When Is Impairment Testing Required?

- 05 Key Concepts in Impairment Testing

- 06 Key Valuation Approaches

- 07 Key Drivers That Affect Impairment Results

- 08 Common Mistakes in Impairment Testing

- 09 Five Key Steps: The Impairment Testing Process

- 10Our Impairment Testing Guide in Australia Process

- 11 Valuation Approaches by Asset and Situation

- 12 Indicative Timeline and Frequently Asked Questions

- 13 Challenges and Lessons Learned

- 14Conclusion and Actionable Insights

01 Introduction

The Purpose of Impairment Testing

Impairment testing is a crucial component of financial reporting to ensure that a company’s assets are not valued above their recoverable value. It is, in essence, an expression of financial integrity: the value of assets in the financial statements should be based on their economic value, not the cost of acquiring or producing them.

- When the economic value of an asset is different to its book value - because markets are in decline, performance is in decline, or plans and expectations are too optimistic - the financial statements need to be adjusted to reflect the difference.

- Impairment testing is the formal process by which this is achieved.

The Mandatory Obligation Under AASB 136

When the carrying value of an asset is greater than the recoverable amount, an impairment loss is recognised in the financial statements. Recognition is mandatory under AASB 136 Impairment of Assets.

- The standard covers a wide variety of assets: goodwill, indefinite-life intangibles, property, plant and equipment, right-of-use assets under AASB 16, and the cash-generating units (CGUs) to which they are assigned.

- The impairment loss is recognised in the income statement as a deduction from profit, impacting the entity's profits, book value of equity and (for goodwill) its allocation of enterprise value among CGUs.

Who Needs to Understand Impairment Testing

Impairment testing is often necessary for companies preparing financial statements under Australian accounting standards – particularly at the end of the financial year or when there are signs of deterioration in performance.

- For public companies, the impairment charge is a public, and often market-moving, disclosure of the board and management's view of the economic value of key assets.

- For unlisted companies, the impairment test affects financial covenants with the bank, the calculation of management incentives, and the financial information provided to investors and lenders.

- For all corporate accountants, financial reporting practitioners, auditors, and advisors, it is essential to have a deep understanding of the impairment testing process.

Impairment testing is not a retrospective compliance exercise, but rather a prospective test of the economic value of the balance sheet. The quality of that assessment is critical to the financial statements. |

02 What Is Impairment Testing?

The Core Process and Calculation

Impairment testing is a procedure used to determine whether the value of an asset or a cash-generating unit (CGU) has fallen below its carrying amount in the financial statements. It involves the company estimating the asset’s recoverable amount (the greater of its fair value less costs to sell and its value in use) and then comparing that amount to the asset’s carrying amount in the balance sheet.

- If the carrying amount exceeds the recoverable amount, the impairment loss is the difference between the two, and the asset should be written down to the recoverable amount.

How Impairment Losses Are Recognised and Allocated

Where impairment occurs, the asset is written down to its recoverable amount. Where an individual asset is impaired, its carrying amount is written down to its recoverable amount, and the impairment loss is recognised as an expense in the income statement.

- For cash-generating units (CGUs) - especially those with goodwill - the impairment loss is allocated in a particular order: first, goodwill is written down, and then any remaining impairment is allocated pro rata to the other assets of the CGU.

- A loss on goodwill is irreversible in future periods, even if the reasons for the loss cease to exist. This characteristic of goodwill impairment losses makes the initial impairment test for goodwill especially important, both analytically and from a business perspective.

The Scope of Assets Covered by AASB 136

Impairment testing under AASB 136 applies to a wide range of assets, including most non-financial assets held by a corporation.

- Goodwill from business combinations: tested annually at the level of the CGU, even in the absence of impairment indicators.

- Intangible assets with indefinite useful lives: must be tested annually; intangibles with finite useful lives are tested when impairment indicators are identified.

- Property, plant and equipment (PPE): tested when there are indicators that the carrying amount may be greater than the recoverable amount.

- Right-of-use assets (AASB 16): subject to AASB 136 and tested when indicators suggest impairment.

- Investments in subsidiaries: tested at the parent entity level, with the carrying value of the investment compared to its recoverable amount.

03Why Do Clients Need Impairment Testing?

The events that give rise to the need for professional impairment testing are many and include all circumstances that impact asset values. Practitioners need to understand the full range of triggers when scoping engagements, and companies need to understand the range of triggers when managing their financial reporting responsibilities.

Financial Reporting and Audit Compliance

The most basic and persistent source of impairment testing is the statutory financial reporting requirement of AASB 136. At the end of the financial year, the financial statements of entities with significant amounts of goodwill, indefinite-lived intangibles, or other assets must be evaluated to determine whether the assets are supported at their carrying values.

- External auditors will test the impairment testing process, cash flow projections, discount rates, and sensitivity analyses as if they were any other significant accounting estimates.

- Fair value disclosures pursuant to AASB 13, where the recoverable amount is measured as fair value less costs of disposal, further complicate measurement and reporting.

- Meeting reporting standards is an active process that requires detailed analysis that can stand up to the scrutiny of a highly experienced external auditor - it is not a passive process.

Business Performance Assessment

Impairment testing is also triggered by particular business events and performance indicators, in addition to the annual reporting period.

- Falling revenues or margins - the most common real-world indicator of impairment - may reflect that the cash flows originally projected to justify the carrying value of goodwill or other assets are not being realised.

- Recessions in the entity's industry have a dual effect: income statement pressure (lower forecast cash flows) and discount rate pressure (higher cost of capital), thereby reducing the recoverable amount from both the top and the bottom.

- Restructuring events, such as the closure of a division or product line, or layoffs, may indicate a change in the intended use of the assets and may require a new value assessment.

- A change in business strategy due to a change in management, a change in competitive strategy, or a change in the long-term business plan may also trigger a review of the impairment triggers.

Mergers, Acquisitions and Post-Acquisition Review

Acquisitions are the main driver of goodwill on most company balance sheets, and the post-acquisition management Australia of that goodwill – including the annual impairment test – is one of the most significant recurring financial reporting activities for acquisitive businesses.

- The post-acquisition goodwill test involves not only the annual impairment test but also the review of the CGU structure to which the goodwill has been allocated, to ensure the allocation remains valid as the acquired business is integrated.

- Acquired assets may need to be revalued if acquired intangibles or other assets are not performing as expected in the purchase price allocation.

- Integration impact analysis - the impact of integrating the acquired business on the expected cash flows and risk of the relevant CGUs - is a critical but often overlooked aspect of post-acquisition impairment testing.

Regulatory and Board Reporting

For listed companies, impairment testing is subject to regulatory scrutiny by ASIC’s financial reporting surveillance program, which monitors the adequacy of impairment testing disclosures.

- ASIC has issued guidance on the most common areas of concern - such as the application of overly optimistic cash flow projections, discount rate inconsistencies and lack of sensitivity analysis.

- The governance reporting requirements ensure that boards are advised of the risk of impairment or an impairment charge, so the adequacy and timeliness of impairment testing are governance issues.

- For both listed and unlisted entities, the results of the impairment testing process need to be explained and justified to a range of stakeholders who may not have a deep understanding of its technical aspects.

04 When Is Impairment Testing Required?

The Two Testing Regimes Under AASB 136

The Australian Accounting Standards Board’s (AASB) standard on impairment testing, AASB 136, sets out two regimes: an annual test for some asset classes and a test based on indicators when certain events suggest that carrying amounts may exceed recoverable amounts. The key to understanding these two regimes – and the indicators that trigger the second regime – is fundamental to anyone involved in managing impairment testing.

- Goodwill and intangible assets with indefinite useful lives must be tested at least once a year - even when there are no indicators of impairment. The annual test must be performed in the same period each year, but can be conducted at any time within that period.

- For other assets covered by AASB 136, impairment testing must be conducted if there is an indicator that an asset is impaired.

External and Internal Impairment Indicators

AASB 136 includes a non-exhaustive list of external and internal indicators that need to be considered at each reporting period.

- External indicators: a significant decrease in the market value of the asset; adverse changes in the technological, market, economic or legal environment; an increase in the market interest rate used to discount the cash flows of the asset; and the carrying amount of the net assets of the entity is higher than the market capitalisation of the entity.

- Internal indicators: obsolescence or physical damage; significant adverse changes in the manner in which the asset is used; evidence from internal reporting that indicates the asset is not performing as expected; and plans to discontinue, restructure or sell the asset that are earlier than expected.

05Key Concepts in Impairment Testing

The four key concepts underpinning the impairment testing framework – carrying amount, recoverable amount, cash-generating unit (CGU) and goodwill allocation – are the starting blocks for all technical practice in this area. These terms are defined with great clarity in AASB 136, and the practitioner who understands their meanings and interactions will be better equipped to tackle the most challenging impairment testing engagements.

Carrying Amount

The carrying amount is the amount at which an asset is valued in the financial statements – the value after deducting accumulated depreciation, amortisation and impairment losses.

- For assets measured under the revaluation model (for example, some types of PPE and investment property), the carrying amount will include any revaluations recognised in equity.

- For goodwill and indefinite-life intangibles, the carrying amount is the original carrying amount (usually the purchase price in excess of the identifiable net assets in a business combination), less any impairment losses previously recognised.

- The comparison of carrying amount to recoverable amount is the core calculation in any impairment test, and the quality of both inputs affects the outcome.

Recoverable Amount

The recoverable amount is the greater of two amounts: the asset’s fair value less costs to sell (FVLCD) and its value in use (VIU). The “higher of” test represents the highest economic benefit the entity can receive from the asset, whether through disposal or continued use.

- If the recoverable amount of the asset under either measure is greater than the carrying amount, there is no need to impair the asset - even if the other measure results in a lower value.

- The implication: if the calculation of VIU is difficult or costly, it may be possible to skip the VIU calculation entirely if it can be shown that FVLCD exceeds the carrying amount.

Cash-Generating Unit (CGU)

The cash-generating unit (CGU) is the smallest group of assets that generates cash inflows independent of other assets or groups of assets. The cash flows from most individual assets are not independent, so impairment testing is not performed at the asset level.

- Determining CGUs is one of the most judgmental areas of impairment testing: CGU boundaries should reflect how management makes decisions about the business and the entity's organisational and reporting structure.

- Misidentification of CGUs, especially aggregating assets into a CGU that is too large, is a common audit issue since it can hide impairment at the sub-CGU level.

Goodwill Allocation

Goodwill from a business combination must be allocated to the CGUs (or groups of CGUs) that are likely to benefit from the synergies of the combination, and this allocation decision determines which CGUs need to perform the annual goodwill impairment test.

- Goodwill is tested at the CGU level (not as an isolated asset) and, therefore, the recoverable amount of the CGU as a whole (including allocated goodwill) is compared with the CGU's carrying amount.

- The allocation of goodwill to CGUs is a critical structural decision in the impairment testing process: a CGU with a large goodwill allocation and a downward performance trend is more likely to be impaired, and the quality of the allocation decision affects the structure of the impairment test in every subsequent period.

06 Key Valuation Approaches

The two most common measures of recoverable amount under AASB 136 – value in use and fair value less costs of disposal – involve different valuation methods and provide different evidence for the auditor to review. Knowing when to use each, how they are put together, and their limitations is critical for anyone involved in an impairment testing exercise.

Value in Use (Discounted Cash Flow Method)

Value in use is the present value of the future cash flows expected to be obtained from the use of the asset or CGU in its current state. It’s determined by a discounted cash flow (DCF) analysis of the cash flows expected from the CGU over a period of time (usually 5 years), with a terminal value reflecting the expected value after the explicit period.

- The discount rate used is a pre-tax rate based on current market expectations of the time value of money and the risks associated with the asset (usually the Weighted Average Cost of Capital (WACC) for the business, adjusted for the CGU's particular risks).

- The VIU calculation is subject to certain AASB 136 constraints: cash flows must be consistent with the asset in its existing state - no benefit from uncommitted restructurings, no synergies from future acquisitions, and a terminal growth rate not exceeding the long-run average for the relevant market.

- These constraints mean the VIU is often more conservative than a transaction-based DCF, and auditors will scrutinise the projections to ensure they meet them.

Fair Value Less Costs of Disposal

Fair value less costs of disposal (FVLCD) is the price that would be received to sell the asset or CGU in an orderly transaction between market participants at the measurement date, less the costs of disposal. It is measured in accordance with AASB 13 Fair Value Measurement.

- Where comparable listed companies for CGUs exist, market multiples from those companies can serve as a market check for the VIU.

- For CGUs that are discrete business units with a potential market of buyers, M&A market evidence provides more direct evidence of what a third party would pay for the same asset bundle.

Market Approach

The market approach (using comparable transactions and/or market multiples from comparable companies) is typically used to cross-check the VIU rather than as the primary valuation method.

- In industries with a robust M&A market and a rich set of publicly listed comparables, EV/EBITDA and EV/Revenue multiples serve as a test of whether the VIU value is consistent with value from the perspective of an arm's-length market participant for the CGU.

- When the market approach generates significantly lower value than the VIU, the difference should be investigated by reviewing the VIU's assumptions - especially the terminal growth rate and the expected cash flow stream.

- Market data can also be used to assess the discount rate and growth assumptions in the VIU.

07Key Drivers That Affect Impairment Results

The Most Consequential Inputs

The result of an impairment test depends on a relatively few key inputs, and it’s important for the practitioners performing the analysis to understand how changing those inputs will impact the bottom line, and for the auditors to understand the sensitivity of the result to those inputs. The key inputs are those that affect the numerator (cash flows) and the denominator (discount rate) in the VIU calculation.

Factors That Increase Impairment Risk

The most obvious and common factors that increase impairment risk are declining revenue trends.

- Declining revenue: a CGU whose revenue has declined for two or three years in a row has a strong presumption that the cash flow profile embedded in its original goodwill carrying value is not materialising.

- Higher discount rates: if the discount rate rises (due to rising interest rates, risk premiums, or credit risk), the size of the cash flow shortfall under the original acquisition scenario increases dramatically.

- Increasing discount rates (due to rising market interest rates and/or equity risk premiums, or worsening credit conditions) also reduce the present value of all future cash flows, while raising the bar for the CGU's performance to justify its carrying value.

- The combination of reduced cash flows and higher discount rates is the most common driver of a significant goodwill impairment charge.

Factors That Reduce Impairment Risk

The factors that reduce impairment risk are, for the most part, the reasons why a business is successful.

Predictable cash flows that offer a high degree of certainty in the forecast period.

- Competitive advantage that provides for long-term profitability.

- Multiple customers limit the impact of losing a single customer.

- Extended contracts that provide a guaranteed revenue stream for several years.

- Positive growth prospects with reliable market evidence.

- If these characteristics are indeed present and can be demonstrated, the impairment testing analysis will usually conclude that the carrying amount is recoverable, and the challenge is to ensure the VIU model accurately and fairly reflecting these positive characteristics.

Table 1: Impairment Risk Assessment — Key Indicators and Responses

Impairment Indicator | Category | Impact on Impairment Risk | Recommended Response |

|---|---|---|---|

Significant revenue decline (>10% year-on-year) | Internal performance | High — directly reduces VIU cash flows. | Trigger full CGU impairment test; update forecasts and sensitivity analysis. |

EBITDA margin compression | Internal performance | High — reduces cash flow generation below original acquisition case. | Reassess terminal margin assumptions; test downside scenario. |

Increase in market WACC / risk-free rate | External market | High — reduces present value of all future cash flows. | Update discount rate derivation; rerun VIU with current WACC. |

Loss of key customer or contract | Internal performance | Medium to High — depends on revenue concentration. | Assess revenue impact; update CGU cash flow forecast. |

Regulatory or legal adverse development | External environment | Medium — increases uncertainty and contingent liability exposure. | Assess financial impact; consider recognition of contingent liability. |

Market capitalisation below net assets (listed entities) | External market | High — explicit AASB 136 impairment indicator. | Mandatory trigger assessment; full impairment review required. |

Technology or product obsolescence | External environment | Medium to High — may compress useful life and future cash flows. | Reassess the useful lives of technology assets; update the CGU forecast. |

CGU outperforming budget with strong pipeline | Internal performance | Low — supports carrying amount recoverability. | Document evidence of strong performance; include in sensitivity upside case. |

08Common Mistakes in Impairment Testing

The Fundamental Challenge of Objectivity

The most frequent errors in impairment testing engagements reflect the difficulty of the exercise: it involves objective, forward-looking analysis in circumstances where the entity’s management has an incentive not to recognise an impairment charge. Impairment testing practitioners and auditors need to be aware of these errors, and the reasons why they occur.

Incorrect CGU Identification

The most fundamental error in impairment testing is incorrect CGU identification. CGUs that are too large – combining business segments with different risks, different cash flow generators or different management oversight structures – can conceal impairment at the sub-CGU level.

- A profitable division and a loss-making division, grouped in a single CGU, may have a combined recoverable amount greater than a combined carrying amount, even if the loss-making division would be impaired if evaluated separately.

- Auditors will question CGU definitions that appear to be structured to minimise impairment rather than align with the entity's operations.

Overly Optimistic Cash Flow Forecasts

Overly optimistic cash flow forecasts are the most common type of analytical flaw in impairment testing. The cash flows in the VIU must be management’s best estimate, not a base case intended to achieve a desired result, according to AASB 136.

- Bets on a sudden improvement in revenue after years of stagnation, on margin expansion without a plan for operational improvement, or on market share increases without a competitive strategy are all suspicious to auditors.

- The budget test - comparing the past three years' budgets to actual performance - is a very effective analytical tool: a company that has missed its budget by 20% for three years cannot reasonably expect to grow revenue by 15% in year four without compelling evidence to the contrary.

Other Critical Errors

Some other common errors exacerbate the effects of the basic errors listed above.

- Inconsistent discount rates: using a WACC that has not been updated to reflect current market conditions, or using a group-wide WACC for CGUs with significantly different risk profiles.

- Failure to consider market downturn indicators: not considering whether a market downturn is an impairment indicator, or waiting until after the reporting date to formally test for impairment.

- Poor documentation and sensitivity testing: while a well-designed VIU model is helpful, it is not much of an audit trail if assumptions are not documented with a justification, and if the sensitivity analysis does not show that the result is resilient to reasonable changes.

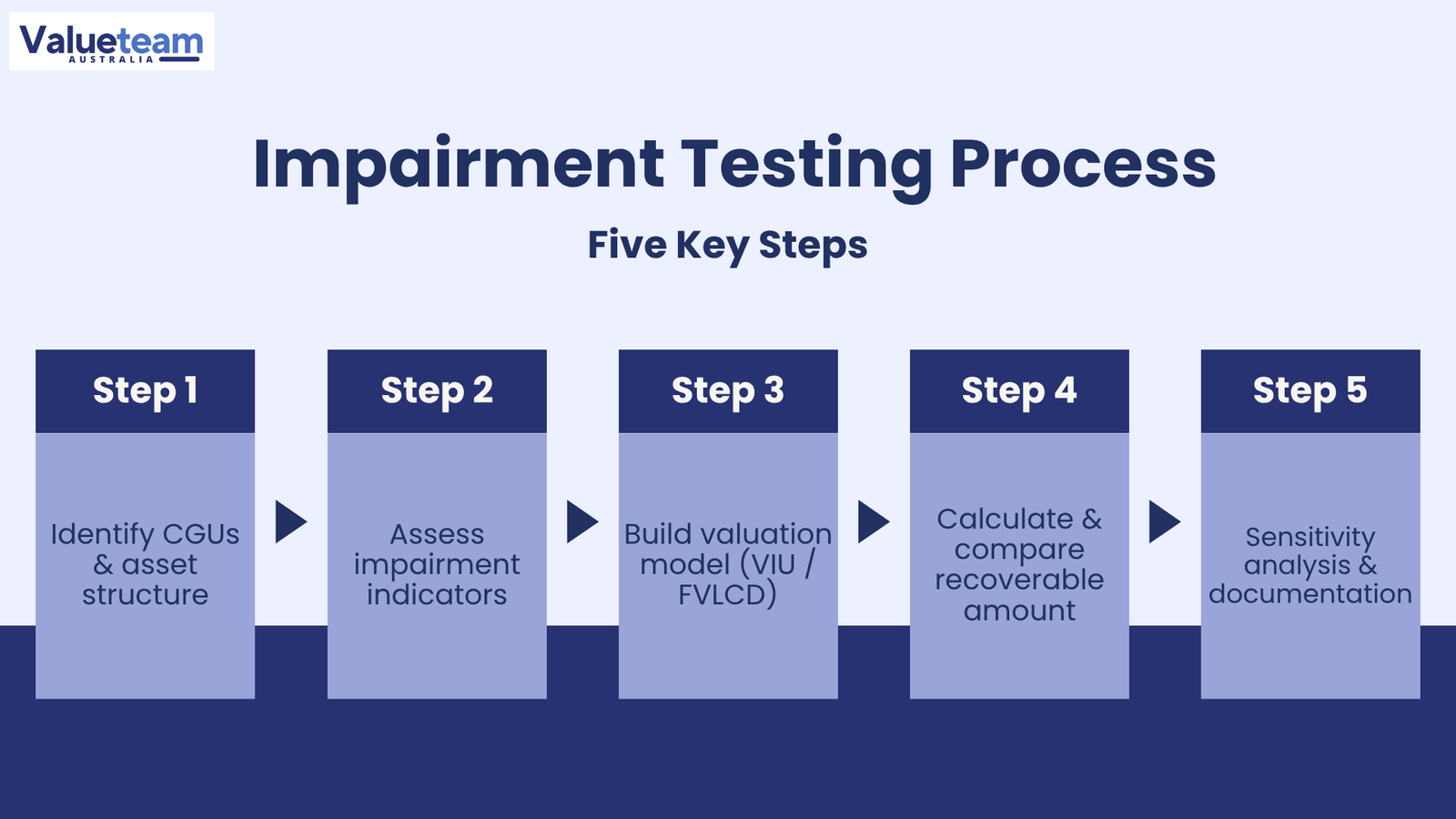

09Five Key Steps: The Impairment Testing Process

Impairment testing can be broken down into five steps: identifying the CGUs, assessing the impairment, determining the impairment amount, providing an audit report, and documenting the impairment. This process can help finance teams map their year-end close schedules, auditors understand the deliverables that will inform their audit procedures, and CFOs and financial controllers manage the integration of the finance, commercial, and valuation workstreams.

Step 1 — Identify CGUs and Asset Structure

The initial step is the identification of the CGU structure – the smallest identifiable groups of assets that generate independent cash flows – and the allocation of the entity’s goodwill, indefinite-life intangibles and other key assets to the CGUs.

- This process involves understanding the entity's management reporting, operational, and strategic planning structures, because the CGUs must be defined in line with how the entity's management monitors and evaluates operating performance and allocates resources.

- In some entities with complex divisional or geographical structures, the CGU identification process may involve considerable analysis to determine whether sub-divisional units have independent cash flows that justify separate CGU status.

Step 2 — Assess Impairment Indicators

Once the CGU structure is in place, the next step is to systematically evaluate whether any impairment indicators exist at the reporting date. This involves considering the external indicators identified in AASB 136, as well as the internal indicators evident in management and operational data.

- For entities with substantial balances of goodwill, the annual impairment test is performed regardless of whether indicators are present - but the scope and nature of the analysis performed is dependent on whether the test performed in the previous year provided considerable headroom, or whether there has been deterioration in the CGU's performance.

Step 3 — Build the Valuation Model

The valuation model Australia (usually a five-year DCF for the VIU, with a market multiples check) is the heart of the impairment test. It must be constructed using management’s best-estimate cash flow forecasts and tested for compliance with the constraints of AASB 136.

- The key AASB 136 constraints: no benefits from uncommitted restructurings, no future acquisitions, no speculative synergies, and a terminal growth rate capped by the long term average for the relevant market.

- The discount rate should be calculated from current market data (usually a WACC calculation that references current risk-free rates, equity risk premiums, industry betas, and leverage ratios) and applied as a pre-tax rate.

- Providing the model to audit quality - with clearly identified inputs, calculation logic, and a sensitivity analysis approach that is built into the model - is critical for audit efficiency.

Step 4 — Calculate Recoverable Amount and Compare

Once the VIU model is constructed and the parameters set, the recoverable amount is calculated as the higher of VIU and FVLCD, and compared with the carrying amount of the CGU (including goodwill).

- If the recoverable amount exceeds the carrying amount, no impairment is necessary, and the model can demonstrate this.

- If the recoverable amount is less than the carrying amount, the impairment loss is the difference and is allocated first to goodwill (until it is written down to zero), and then pro rata to the other assets in the CGU.

- A VIU that results in a recoverable amount significantly higher than the implied value of the CGU should be further investigated and subject to a more comprehensive cross-check.

Step 5 — Sensitivity Analysis and Documentation

Sensitivity analysis is a technical requirement of AASB 136 (for CGUs where the recoverable amount is close to the carrying amount), and a key audit evidence requirement for any impairment test conclusion.

- The sensitivity analysis must demonstrate the effect of reasonable variations to each of the key assumptions (the discount rate, revenue growth, EBITDA margin, terminal growth rate) and must determine the point at which the conclusion switches from no impairment to an impairment loss.

- For CGUs with low headroom, the sensitivity analysis is especially important - and the adequacy of the documentation explaining why management believes the base case assumptions are reasonable is a key part of the auditor's evidence gathering.

- The final impairment report should include all of these component, providings a full picture of the impairment testing process.

10Our Impairment Testing Guide in Australia Process

Why a Structured Process Matters

Our structured, repeatable engagement process serves as the operational framework for sound impairment testing practice. The following is a standard best-practice process for a professional impairment testing engagement, from the initial CGU structure review to the delivery of the audit-ready report. It can serve as a guide for finance teams, CFOs, and auditors.

The most successful impairment testing initiatives are integrated into the financial reporting cycle and not seen as a separate year-end event.

Firms that track the performance of their CGUs against the previous year’s VIU assumptions oevery quarter monitor the key value drivers identified in the sensitivity analysis, and commence impairment testing work as soon as year-end indicators become apparent tend to achieve more accurate, more defensible results with quicker audit cycles.

Table 2: Impairment Testing Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — CGU and Asset Identification | Define CGU structure; map goodwill and intangibles to CGUs; confirm asset register and carrying amounts. | Management reporting structure; asset register; acquisition documentation; audited financials. | CGU structure memo; goodwill allocation table; asset inventory by CGU. |

Step 2 — Impairment Indicator Assessment | Review external and internal impairment indicators; assess whether annual mandatory test or indicator-triggered test applies. | Management accounts; budget vs actual; market data; regulatory developments. | Impairment indicator assessment memo; triggering event documentation. |

Step 3 — Forecast Review and Assumption Assembly | Obtain and review management cash flow forecasts; assess budget accuracy; challenge key assumptions; derive WACC. | Cash flow forecasts; historical performance; WACC inputs; comparable market data. | Reviewed forecast; documented assumption register; WACC derivation. |

Step 4 — VIU Model Build | Construct five-year DCF model; implement terminal value; apply pre-tax discount rate; calculate VIU per CGU. | Reviewed forecasts; WACC; terminal growth rate; depreciation and capex schedules. | Value in use calculation per CGU; model documentation. |

Step 5 — FVLCD Cross-Check | Estimate fair value less costs of disposal using market multiples and comparable transactions where available. | Comparable listed companies; precedent transactions; market multiple databases. | FVLCD estimate; market multiples cross-check analysis. |

Step 6 — Recoverable Amount and Impairment Conclusion | Calculate recoverable amount (higher of VIU and FVLCD); compare to carrying amount; determine impairment loss if applicable. | VIU and FVLCD outputs; carrying amounts including allocated goodwill. | Recoverable amount per CGU; impairment loss calculation (if applicable). |

Step 7 — Sensitivity Analysis | Test key assumptions; identify impairment trigger points; present sensitivity tables for audit disclosure. | Model; assumption ranges; management commentary on downside risks. | Sensitivity tables, trigger point analysis, and headroom documentation. |

Step 8 — Final Report | Prepare audit-ready report; document CGU structure, methodology, assumptions, analysis, and conclusions. | All prior outputs; management factual review; auditor pre-engagement. | Final signed impairment testing report; AASB 136 disclosure support. |

11 Valuation Approaches by Asset and Situation

Matching Methodology to Asset Type and Context

AASB 136 calls for different approaches for different asset types and impairment testing. The table below outlines the main approaches and considerations for each major asset and context type.

- The methodology selected should be based on the asset type, availability of market evidence and the objective of the valuation - not the same approach for all assets.

- The preferred approach for most revenue-generating assets is to adopt value in use as the primary method, and verify with FVLCD using market evidence.

Table 3: Impairment Testing Approaches by Asset and Situation

Asset / Situation | Primary Approach | Key Considerations | Typical Audit Focus |

|---|---|---|---|

Goodwill (post-acquisition) | Value in use (VIU) — 5-year DCF + terminal value | CGU identification; budget accuracy; WACC; terminal growth rate within industry bounds. | Forecast assumptions vs prior year actuals; WACC derivation; sensitivity headroom. |

Indefinite-life intangible assets | VIU or FVLCD depending on market evidence | Annual mandatory test; royalty rate benchmarks for brands; cash flow attribution. | Consistency with PPA assumptions; useful life review; FVLCD market comparables. |

Finite-life intangibles (indicator-based) | VIU (incremental cash flow) or FVLCD | Triggered by performance decline, obsolescence, or contract loss; CGU-level test. | Whether indicator assessment was appropriately conducted; attribution of cash flows. |

Property, plant and equipment (PPE) | FVLCD (market value) or VIU | Physical condition; functional and economic obsolescence; replacement cost cross-check. | Consistency of carrying amount with market evidence; adequacy of depreciation policy. |

Right-of-use assets (AASB 16) | VIU (at CGU level) or FVLCD | Included in CGU to which they contribute; separable FVLCD only if asset can be sold separately. | CGU allocation; treatment of lease liability in carrying amount calculation. |

Investments in subsidiaries (parent entity) | VIU or FVLCD at parent entity level | Recoverable amount of investment equals higher of enterprise value less costs and VIU. | Consistency with consolidated goodwill test; intercompany loan implications. |

Multi-CGU groups with allocated goodwill | Combined VIU across CGU group; FVLCD cross-check | Goodwill allocation rationale; aggregation of CGUs for test within AASB 136 limits. | Whether aggregation is appropriate; individual vs group impairment risk identification. |

Near-impairment scenarios (low headroom) | Detailed VIU + extended sensitivity analysis | Sensitivity disclosures required; management assumptions must be robust and documented. | Reasonableness of base case; sensitivity of conclusion to key assumptions. |

12 Indicative Timeline and Frequently Asked Questions

Planning Around Realistic Timelines

When finance teams are planning year-end close and audit timelines, it’s useful to consider the realistic timeframe for an impairment testing engagement. The engagement can range from simple to complex depending on the number of CGUs, availability of management forecasts and the level of headroom above the impairment threshold.

Table 4: Indicative Impairment Testing Timelines

Assignment Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

Simple impairment review (single CGU, high headroom) | 3–5 business days | Completeness of cash flow forecasts and financial data. | Limited sensitivity required where headroom is substantial. |

Standard CGU testing (2–4 CGUs) | 1–2 weeks | Number of CGUs; forecast quality; WACC derivation complexity. | Most common scenario for mid-market acquisitive companies. |

Complex multi-CGU groups | 2–4 weeks | Number of CGUs; cross-CGU goodwill allocation; multi-entity structures. | Listed entities; complex acquisition histories; multiple operating segments. |

Low headroom situations (near-impairment) | 2–3 weeks | Extended sensitivity analysis; management commentary on assumptions. | More extensive auditor involvement; disclosure drafting support required. |

Post-acquisition goodwill test (first year) | 2–3 weeks | CGU allocation rationale; consistency with PPA assumptions; integration impact. | Typically tied to PPA completion timeline; auditor pre-engagement recommended. |

When is impairment testing required?

There are two triggers for impairment testing under AASB 136.

- Goodwill and indefinite-life intangible assets: tested at least annually, regardless of whether there are indicators of a decline in performance or impairment - a mandatory, routine test.

- Other assets in scope: tested if there are indicators of impairment at the reporting date - either external (market, interest rates, competitor activity) or internal (performance worse than budget, restructuring, damage or obsolescence of assets).

- Impairment testing is often required for companies that prepare financial statements under Australian accounting standards, particularly at the end of the financial year or when there are indicators of deteriorating performance.

What are the most important inputs?

Cash flow forecasts and the discount rate are the two most important inputs to the value-in-use calculation and the two most common areas of disagreement with the auditor.

- The cash flow forecasts must be management's best estimate, in line with the AASB 136 restrictions on uncommitted restructurings and future acquisitions, and consistent with the entity's past forecasting accuracy

- The discount rate (based on the business's WACC) must be consistent with current market-observable inputs and adjusted for the perceived risk of the particular CGU under test.

- These two inputs account for the bulk of the value-in-use output, and the accuracy of their derivation is the key factor in the impairment assessment.

Is impairment testing mandatory?

Yes – impairment testing is required under AASB 136 for all entities that prepare general purpose financial statements under Australian Accounting Standards if the entity has assets covered by the standard.

The requirement does not depend on the entity’s size, listing status, or profitability.

- Where an entity has goodwill on its balance sheet (which is the case for all entities that have undertaken an acquisition) the annual test for goodwill impairment is an ongoing, mandatory obligation.

- The omission of adequate impairment testing, or the failure to recognise an impairment loss supported by the impairment testing, constitutes a material departure from Australian Accounting Standards that external auditors must report.

13Challenges and Lessons Learned

The Management Incentive Problem

The impairment testing process is more than any other aspect of financial reporting; it is vulnerable to the “colouring” of management’s preferences. The VIU calculation is a forward-looking calculation that relies on management’s assumptions about future cash flows and the discount rate used to discount them, which presents many opportunities for technically correct but commercially biased assumptions.

- Auditors, independent reviewers and practitioners need to recognise this and the particular patterns evident, so they can conduct their analyses objectively and critically in a context where commercial pressures are in one direction.

Challenge 1 — The Budget Accuracy Analysis

The most common lesson from impairment testing practice is the value of the budget accuracy analysis. The most powerful refutation of an overly optimistic VIU budget is to look at its prior year results: did the company achieve its budget last year?

- If an entity has missed its revenue budget by 15% for three years in a row, a budget for the current year showing 20% revenue growth needs to be justified.

- Auditors who perform the budget accuracy analysis thoroughly - comparing the prior year VIU forecasts with actual results - always uncover the most significant flaws in impairment testing models.

- Professionals who incorporate budget accuracy analysis at the start of every audit, before they review forward-looking forecasts, are more likely to identify problems with forecast credibility and discuss them with management.

Challenge 2 — The Discount Rate Disconnect

The second key take-out is the risk of the disconnect between the discount rate used in impairment testing and the discount rate implied by the entity’s market capitalisation.

- For listed entities, the implied WACC can be calculated from the entity's market capitalisation and expected cash flows. If this rate is significantly higher than the rate used in the VIU, it is a market signal that the VIU's assumptions may not align with the market's assessment of the entity's risk and growth prospects.

- This disconnect is one of the most frequent issues identified in ASIC's financial reporting surveillance programme for listed entity impairment testing.

- The takeout: discount rates should be based on current, market-based information - not discount rates set at the time of the acquisition that have not been updated.

Challenge 3 — The Documentation Discipline

An impairment testing result that cannot be justified, supported and communicated via a coherent, comprehensive documentation package is not an accounting estimate – it is an opinion.

- The most frequent cause of late revisions and rework in the practice of impairment testing is not mistakes in the valuation models, it is a lack of documentation to support their assumptions.

- CFOs and financial controllers who implement a systematic documentation practice for impairment testing, documenting the rationale for the CGU structure, the indicator assessment, the forecast development, the WACC determination, and the sensitivity analysis in a single package, report shorter, less challenging and more efficient audits.

14Conclusion and Actionable Insights

Why Impairment Testing Matters

Impairment testing is a vital component of financial reporting – one that involves valuation, accounting standards, auditing and governance. It is a non-discretionary, mandatory requirement that cannot be managed through wishful thinking or poor record-keeping.

- If the recoverable amount of an asset is less than its carrying value, an impairment loss is recognised - period.

- It is a cyclical, operationally important task for any entity with significant goodwill, intangibles or PPE balances.

- The financial statements are as good as the impairment testing analysis.

For Companies Managing Significant Goodwill Balances

The key takeaway is the need to be more engaged in the impairment testing process throughout the year, rather than treating it as an annual year-end compliance exercise.

- Track CGU performance against the previous year's VIU assumptions, and track the key value drivers identified in the sensitivity analysis.

- Refine the discount rate derivation and begin impairment testing as early as possible once year-end indicators are identified.

- Establish a strong impairment testing framework (clearly defined CGU structures, WACC derivation processes, management forecast reviews), and reap the rewards many times over by minimising audit and regulatory costs, and improving financial statement quality.

Five Actionable Steps for Practitioners

For mid- to junior-level professionals looking to develop their impairment testing skills, the following priorities offer a development roadmap.

- Become familiar with AASB 136 and AASB 13 - the technical and conceptual underpinnings of impairment testing.

- Develop a strong understanding of DCF modelling and WACC calculations - because the value in use calculation is the key analytical technique used in the majority of impairment testing.

- Build a good CGU identification skill - the ability to identify appropriate CGU boundaries, appropriately allocate goodwill and determine when aggregation or disaggregation is appropriate.

- Build expertise in budget accuracy analysis as an analytical approach - how to compare last year's VIU assumptions to the actual results to assess the credibility of this year's assumptions.

- Look for opportunities to work on low-headroom impairment testing engagements - where the recoverable amount is close to the carrying amount - as these offer the most intense and most widely applicable training in rigorous impairment testing.

Our impairment testing advisory services offer comprehensive support to entities in meeting their AASB 136 obligations, including CGU structure development, impairment indicator testing, VIU model development, sensitivity analysis and audit-ready reporting. Our work is technically rigorous, market-informed and well-documented, as all financial reporting work must be. An impairment test is a test of integrity: does the balance sheet reflect the business’s value? Doing so in a rigorous, transparent and professionally honest way is the goal. |