Risk Management Guide in Australia

Table of Contents

- 01 Introduction

- 02What Is Risk Management?

- 03 Why Do Companies Need Risk Management?

- 04 Types of Business Risks

- 05 Risk Assessment Methods

- 06 Key Components of a Risk Management System

- 07 Risk Management and Business Value

- 08Five Key Steps: The Risk Management Framework

- 09Common Risk Management Challenges

- 10Our Risk Management Process

- 11 Risk Management by Business Context

- 12Indicative Timeline and Frequently Asked Questions

- 13 Challenges and Lessons Learned

- 14Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 What Is Risk Management?

- 03 Why Do Companies Need Risk Management?

- 04 Types of Business Risks

- 05 Risk Assessment Methods

- 06 Key Components of a Risk Management System

- 07 Risk Management and Business Value

- 08Five Key Steps: The Risk Management Framework

- 09Common Risk Management Challenges

- 10Our Risk Management Process

- 11Risk Management by Business Context

- 12 Indicative Timeline and Frequently Asked Questions

- 13 Challenges and Lessons Learned

- 14Conclusion and Actionable Insights

01 Introduction

The Reality of Business Risk

Risk management is an important element of corporate governance and business strategy in Australia. All businesses face uncertainty – about future revenues, competitors’ actions, the reliability of technology, the actions of regulators and so on.

- It's not a matter of whether a business is exposed to risk, but whether it has the processes, practices and cultures in place to manage risk effectively.

- Risk-managed organisations are more robust, more attractive to investors and creditors, and more likely to seize opportunities without being caught out by unexpected risks.

The Expanding Scope of Risk Management

Risk management is the process of identifying, measuring and managing risks that may affect a firm’s financial results, operations, brand or compliance. It has grown in recent years:

- Supply chains are more international and vulnerable.

- The use of technology has given rise to new cyber and technology risks.

- Regulation has grown in every industry.

- Damage to reputation can now spread faster than ever via social media, reducing the time an organisation has to respond to a crisis.

- Risk management is no longer an occasional exercise - it's a day-to-day operational practice that underpins decision-making.

Why This Guide Matters

Good risk management helps companies minimise uncertainty, enhance their decision-making and build resilience. For finance, accounting, operations, compliance, legal, or advisory services professionals, risk management skills are a key differentiator between those who are proficient and those who are technically competent.

This resource offers a reference guide to risk types, approaches and frameworks, and the issues organisations commonly face.

It is designed for junior to mid-career professionals looking to develop basic skills across the entire spectrum of risk management.

Risk management is not about removing uncertainty; it is about knowing it well enough to inform decisions. The aim is not to eliminate risk, but to understand it well enough to achieve organisational goals with the right level of confidence and caution. |

02 What Is Risk Management?

Definition and Core Discipline

Risk management is the systematic identification, assessment and mitigation of risks. It is a quantitative and qualitative discipline that takes into account an organisation’s strategic goals, risk tolerance, and resource allocation.

- At its most advanced, it is an offensive advantage - it allows companies to take more risks than their peers, and suffer less downside, because they know exactly what risks they are taking, and manage them accordingly.

- It is not a defensive practice aimed at avoiding bad outcomes - it is a practice that supports better risk-taking.

Sources of Risk

Risks come from all aspects of a business’s environment:

- Financial risks: credit risk, liquidity risk, interest rate risk, and foreign exchange risk.

- Operational risks: process breakdowns, system outages, supply chain disruptions, and human error.

- Regulatory risks - changes in law, compliance requirements or enforcement.

- Cyber risks are among the fastest-growing and most difficult to manage in the modern world.

- Market uncertainty, poor strategy, and employee or third-party errors or fraud.

The Fundamental Objective

Risk management is not about eliminating risk, but controlling it. All decisions involve risk and return:

- Market expansion, new product development, mergers and acquisitions, and even technology investment - all involve taking on certain levels of risk for certain levels of return.

- Risk management is about consciously making these trade-offs - knowing both the potential rewards and potential costs.

- Companies that view risk management as a compliance exercise that focuses on reporting rather than management simply miss the point.

03Why Do Companies Need Risk Management?

The commercial justification for investing in risk management is stronger than ever. The most damaging and embarrassing failures in organisations have almost always been preceded by either a lack of risk management capability or a culture that did not encourage realistic risk assessment.

Regulatory and Compliance Requirements

Risk management is not just best practice in Australia – it’s increasingly a regulatory requirement with enforcement implications:

- The ASX Corporate Governance Principles and Recommendations mandate listed companies to have an effective system of risk management and oversight, and ASIC's surveillance program assesses the board's compliance with its responsibilities.

- APRA-regulated entities have specific requirements under CPG 220 (Risk Management) and CPG 234 (Information Security) for the banking, insurance and superannuation industries.

- To be compliant, effective controls must be in place, tested, and monitored, and risks must be escalated through the audit and board reporting lines.

- All entities that prepare under ASRS must now disclose their governance and risk management of climate-related financial risks.

Financial Protection

The most obvious, tangible return on risk management is financial protection against losses:

- Limits financial losses resulting from operational failures, credit defaults, regulatory penalties and business interruption - a compounding return.

- Firms that have faced fewer adverse risk events have a lower cost of capital, higher credit ratings and access to insurance markets.

- Preserving cash flow stability through risk hedging, cash buffers, and contingency financing arrangements enables market shocks to be managed without panic.

- Portfolio- and counterparty-level credit and liquidity risk management is at the core of the financial stability of any organisation with substantial external financial relationships.

Operational Stability

In addition to the financial benefits, risk management enhances the operational effectiveness of the business:

- Enhancing processes by identifying and addressing operational risks often leads to process improvements and increased efficiency.

- Minimising operational downtime due to supply chain issues, IT downtime, and employee-related problems safeguards revenue, customer loyalty and brand reputation.

- Improving business continuity through recovery plans, backups,s and incident response exercises means that in the event of a disruption, the business resumes normal operations as soon as possible with minimal long-term impact.

Strategic Decision-Making

At the highest level, risk management offers the quantitative tools for improved decision-making:

- Enabling growth strategies - expanding into new markets, introducing new products, making major capital expenditures - by assessing opportunities and risks, including risk tolerance, objectively.

- Risk assessment for capital allocation ensures the expected returns of alternative opportunities are adjusted for risk and that the portfolio of strategic investments is diversified.

- M&A planning is one of the most critical due diligence processes; overlooking operational, regulatory, financial, or cyber risks inevitably leads to avoidable post-acquisition disappointment.

04 Types of Business Risks

The ability to identify the specific types of risk a business is exposed to, and the nature, causes, and management of those risks, is the fundamental analytical skill of a risk practitioner. The importance of each risk category varies greatly across industries, businesses, and countries.

Financial Risk

Financial risk covers risks to the financial position of an organisation from adverse movements in market factors, deterioration in credit quality, and mismatches in cash flows:

- Liquidity risk - the risk that the organisation cannot meet its obligations as they are due - is a particularly existential form of risk; companies that are economically viable but unable to access liquidity at the right time have failed.

- Credit risk exists wherever the organisation lends money - to its customers in the form of trade receivables, to its counterparties in the form of derivative exposures, to its investees in the form of loans and equity - and is managed through credit evaluation, credit limits and credit monitoring.

- Interest rate risk and foreign exchange risk are market risks that affect the cost of funding and the value of international revenues and assets. Treasury risk management specialists usually manage them.

Operational Risk

Operational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems, or from external events:

- Fails in manufacturing, service delivery or administrative processes result in direct losses and indirect reputational and customer impacts.

- System failures - technology outage, software failure, data loss - are increasingly significant as organisations rely on digital systems to support their operations.

- Human failure is a fact of life in complex organisations and can only be controlled (not eliminated) through process design, training and quality management.

- Supply chain risk from natural events, geopolitical events, supplier failure, or quality failure has become one of the most important operational commercial risks.

Compliance and Regulatory Risk

Compliance and regulatory risk is the risk of legal or regulatory enforcement action, financial penalty or reputational loss that could result from non-compliance with laws, regulations, rules and codes of conduct:

- Regulation of Australian business has grown in breadth, covering financial services, the environment, occupational health and safety, privacy and data protection, modern slavery, gender equality, and sustainability disclosure.

- Failure to comply with laws and regulations, and to report compliance breaches, can attract penalties that are far greater than the cost of compliance.

- Violations of industry regulations (such as in financial services, health care, and energy) can jeopardise an entity's right to operate.

- Governance failures - in the board, internal controls, or the management of conflicts of interest - draw the attention of regulators and investors, resulting in long-term reputational and financial harm.

Strategic Risk

When strategic risk – where the strategic decisions of an organisation are not consistent with market or competitive realities or stakeholder expectations – occurs, it is at the level of the organisation’s business model and its long-term value proposition:

- Sub-optimal business decisions - acquisitions at high premiums, investments in technologies that are rendered obsolete, market entries without sufficient competitive intelligence - result in losses that have a multi-period impact.

- Failed market entry and the risk that better-capitalised or better-positioned competitors erode the organisation's competitive advantages require open-minded, continuous evaluation of the strategic fit and competitive advantages.

- Product or service obsolescence - the risk that the company's product or service is made irrelevant by technological developments or changing consumer tastes - demands foresight that is absent from many conventional risk analyses.

Cyber and Technology Risk

Cyber and technology risk is one of the fastest-growing and hardest-to-fully-measure risks faced by Australian companies:

- Data breaches - unauthorised access, theft or disclosure of confidential customer, employee or commercial data - result in direct costs (regulatory fines, legal liability, remediation costs) and indirect costs (reputational loss, lost customers) that can be many times the initial cost of prevention.

- IT system outages - due to cyber attacks, hardware, software or human error - can impact revenue streams, customer service and supply chains all at once.

- Cybersecurity risks from advanced external threats, such as state-sponsored groups and highly resourced criminal groups that operate ransomware, constitute an ever-evolving threat environment that cannot be completely protected against without ongoing investment.

- Technology dependency risks - the increasing vulnerability from centralisation of key functions with single vendors, cloud providers or software systems - need to be managed through diversification, contingency and contractual arrangements.

05Risk Assessment Methods

Risk assessment methods differ in their level of sophistication, data demands and suitability for different types of risk. Knowing when to use which method is a fundamental skill for risk management professionals at all levels.

Qualitative Risk Assessment

Qualitative risk assessment is by far the most common method used – especially in organisations that are at a lower level of risk management maturity, or for risk types where quantitative information is sparse or unreliable:

- Involves categorising risks as low, medium or high based on an assessment of their likelihood and impact - usually through a facilitated workshop process with the relevant business owners.

- Typically produces a risk heat map - a matrix that shows the position of each risk according to the assessed likelihood and impact, allowing the most significant risks to stand out and provide a documented and consistent approach to prioritisation.

- Limitation: subjective - different people may assess the same risk differently, and the lack of quantitative inputs makes it hard to roll up risks across the organisation or track changes in risk over time.

Quantitative Risk Analysis

Quantitative risk analysis overcomes some of the shortcomings of qualitative analysis by attaching numerical estimates of probability and financial loss to risks:

- Allows for aggregating risks in the portfolio, calculating expected loss and value at risk, and comparing the cost of risk mitigation with the expected reduction in loss.

- Scenario analysis - the systematic analysis of specific adverse events and their financial consequences - is a useful approach to low-frequency events. In these high-impact risks, historical data is sparse, and outcomes are discontinuous with the organisation's experience.

- Stress testing involves testing the organisation's financial model or budget against specified extreme scenarios - a large increase in interest rates, a major disruption to its supply chain, a major data security breach - and determining whether the organisation can withstand the impact within its risk tolerance.

- Key risk indicators (KRIs) are leading indicators that give early warning of risk trends, enabling management to take preemptive action to mitigate risk rather than reactive action after the risk event has occurred.

06Key Components of a Risk Management System

The Integrated Architecture

A risk management system is not just a risk register and a policy – it is an integrated architecture of governance and control structures, risk analysis tools, control measures and reporting frameworks that collectively establish an enterprise-wide risk management capability to identify, manage and report risks.

Governance and Control Structure

The risk governance structure is the system’s underpinning – determining roles and responsibilities and accountability:

- The three lines of defence model - where the first line (business units) owns and manages risk, the second line (risk and compliance functions) oversees and challenges, and the third line (internal audit) independently assures - is the most common governance structure in Australian organisations.

- The internal controls system operationalises the risk management system through preventive and detective controls. The controls need to be tested and proven to be effective, not just assumed.

- Compliance policies establish the organisation's specific compliance obligations and the expected behaviour of employees and third parties to manage compliance risk.

Escalation, Reporting and Audit

The glue and audit that ensures the risk management system operates:

- Escalation processes ensure risk events and concerns flow through the governance process. In the absence of well-understood escalation processes, risks visible at the operational level do not reach the people who can make decisions.

- The risk reporting process provides periodic, structured insight to management and the board about the risk environment, mitigation status and concerns - the control process.

- Audit and monitoring activities independently confirm the effectiveness of controls and the veracity of risk information, assuring that the system is not reliant solely on self-reporting

Table 1: Risk Management System — Components and Functions

Component | Primary Function | Who Owns It | Key Failure Mode |

|---|---|---|---|

Risk governance structure | Define accountability, reporting lines, and oversight arrangements | Board + Executive | Unclear ownership; gaps between the first, second, and third lines |

Risk appetite statement | Define the amount and type of risk the organisation will accept | Board | Aspirational document disconnected from operational decisions |

Risk register | Document identified risks, ratings, owners, and mitigations | Risk Function + Business Units | Outdated; not actively maintained; not integrated with strategic planning |

Internal controls system | Reduce the likelihood and impact of risk events through preventive and detective controls | Business Units + Risk Function | Undocumented, untested, and circumvented under commercial pressure |

Key risk indicators (KRIs) | Provide early warning of emerging risk trends | Risk Function + Business Owners | Lagging indicators; not integrated with management decision-making |

Escalation procedures | Route risk events and emerging concerns to appropriate decision-makers | All levels of organisation | Not understood; not followed; disincentivised by blame culture |

Risk reporting framework | Provide structured risk information to management and the board | Risk Function + CFO | Too detailed; too infrequent; not decision-useful |

Audit and monitoring processes | Independently verify control operation and risk information accuracy | Internal Audit | Limited scope; insufficient frequency; inadequate follow-up on findings |

07Risk Management and Business Value

The Evidence Base

The link between risk management and business value is among the best documented in corporate finance. The evidence includes empirical studies linking governance quality to the cost of capital, event studies examining the effect of major risk events on market value, and empirical studies of the premium that private equity and institutional investors pay for businesses with superior risk management in mergers and acquisitions.

Channels of Value Creation

The value impact of effective risk management comes from reducing earnings volatility, cost of capital and investor uncertainty, and improving operational efficiency and compliance:

- Cost of capital channel: firms with lower earnings variability - through the reduction of financial, operational and compliance risk - are subject to lower risk premia on equity and to lower spreads on debt. Credit analysts and ratings agencies explicitly value risk management.

- Investor confidence channel: institutional investors with ESG mandates explicitly assess board oversight of risk as a governance factor. Effective risk management increases the investable universe and lowers equity costs.

- Operational efficiency channel: firms that anticipate and manage operational risk exposures (eliminating bottlenecks, strengthening controls, enhancing supply chain resilience) tend to enjoy cost efficiencies in addition to the risk-mitigation benefits.

- Ineffective risk management results in valuation discounts and greater business uncertainty - while organisations that invest in real risk management capability build a resilience premium that compounds in their competitive and capital market advantage.

Case Study: Supply Chain Resilience in Practice

Take the case of a multinational logistics company that heavily invested in supply chain risk mapping and contingency planning after a major supply chain disruption in the early 2010s:

- The company developed a risk management system over five years that mapped the risks associated with its top 500 suppliers and secured alternative-source agreements for all single-source critical components.

- It also established a business continuity plan that could reroute freight within 24 hours of a major event.

- During a geopolitical event in 2018 that affected key shipping lanes, the organisation diverted over 30% of its freight volume within 48 hours, resulting in a cost increase of about 8% on the volumes involved.

- Rivals lacking such resilience capabilities struggled for weeks with service outages and lost customers that took years to win back - a clear demonstration of the compounding value of risk management.

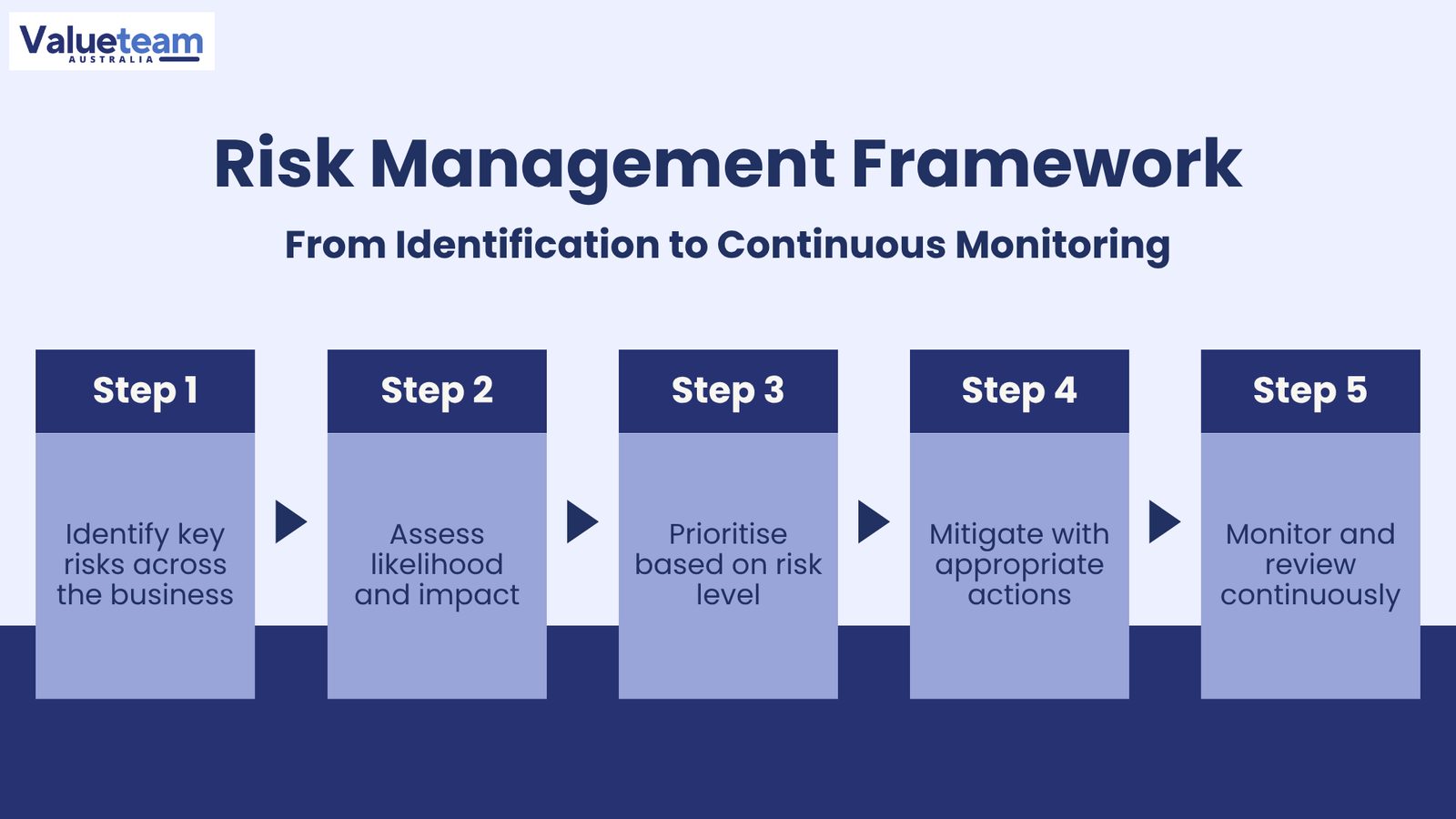

08Five Key Steps: The Risk Management Framework

The risk management framework can be broken down into five steps that take the organisation from initial risk identification to final monitoring and review, ensuring the framework is up to date and relevant. These are the steps of a management cycle – not a one-off process – that need to be integrated into the organisation’s operations to add value.

Step 1 — Risk Identification

The most fundamental step is to comprehensively identify all risks that may impact the organisation’s ability to achieve its objectives:

- Combines information from a range of sources: facilitated workshops with business unit managers and functional specialists, review of the strategic plan and business model, review of historical incident reports and near-miss reports, horizon scanning of the external environment, and benchmarking against similar organisations.

- The aim is broad coverage across the five key risk categories: financial risk, operational risk, compliance and regulatory risk, strategic risk, and cyber and technology risk.

- It's not enough to use generic risk descriptions like "regulatory risk" or "operational failure"; the risk register should include specific, context-specific risk descriptions that link each risk to the organisation's business operations.

Step 2 — Risk Assessment

Having identified the risks, this step assesses the likelihood and impact of each risk:

- Likelihood assessment estimates the likelihood that the risk event will occur over a specified time period (typically one to three years).

- An impact assessment estimates the financial, operational, reputational, and regulatory impacts of the risk event if it occurs.

- The best results are achieved by combining qualitative risk assessment (using rating scales) with quantitative risk analysis (if data is available).

- The risk heat map - a visual presentation of the likelihood and impact of each risk on a matrix - is a simple summary that can be easily shared with management and the board.

Step 3 — Risk Prioritisation

Not all risks are created equal – this step establishes where to focus the organisation’s scarce management resources:

- Risk prioritisation is mostly driven by risk assessment outcomes: risks with a high likelihood and high impact are the most important to manage.

- Risk appetite also comes into play: some low-likelihood, high-impact risks may be prioritised for considerable mitigation activity despite their low frequency.

- The result is a three-tiered risk register that identifies risks to be actively managed, those to be monitored with specific triggers for escalation, and those to be accepted as part of the business.

- This ranking needs to be periodically revisited - as business conditions evolve and mitigation measures are taken, the priorities will change.

Step 4 — Risk Mitigation Planning and Implementation

This step identifies the strategies, controls, and actions that will reduce each of the organisation’s priority risks to within its risk appetite. There are four categories of mitigation strategies:

- Avoidance - ceasing the activity that gives rise to the risk.

- Reduction - putting in place controls to mitigate the likelihood or consequences of the risk.

- Transfer - transferring financial responsibility for the risk to a third party, such as insurance or outsourcing.

- Acceptance - choosing not to mitigate the risk, either because the cost of mitigation outweighs the potential benefit.

- This step involves implementation with clear ownership, timeframes, resourcing, and integration into the operational management of the relevant business units. A major failure is the development of mitigation plans during risk workshops, but their failure to be implemented.

Step 5 — Monitoring and Review

The monitoring and review step completes the feedback loop that transforms risk management from an occasional event to an ongoing process:

- Key risk indicators (KRIs) - leading indicators that signal when a risk is moving towards its tolerance threshold - provide the timely insights that support proactive rather than reactive risk management.

- Periodic reporting of risk status to management and the board - the risk reporting framework - ensures that risk information is reported frequently and in a form that is relevant to the decision-making process.

- Periodic reviews of the risk register - usually annually or when there are changes in the business - ensure that risk identification and assessment are kept up-to-date as the business and its environment change.

- The inclusion of incident, near-miss, audit, and monitoring data ensures that operational experience feeds into the risk assessment.

09Common Risk Management Challenges

Structural Challenges

The most common challenges that organisations face in establishing and sustaining risk management capability are structural and cultural, and the solutions require as much focus on organisational culture as on the design of the risk framework:

- The absence of a formal risk framework is common in SMEs and organisations where risk has been managed informally through the experience and judgement of management.

- Moving from informal to formal risk management requires careful governance design, role and responsibility allocation, governance structure, and board sponsorship, which demonstrate the organisation's commitment to risk management.

- In the absence of sponsorship, formal risk management frameworks are often viewed as "compliance-driven" - producing reports but not changing behaviours.

- Poor internal controls are the operational consequence of poor risk management: processes that are not designed to prevent or detect errors and misconduct, or processes that are designed but not followed due to commercial pressures, lack of training and monitoring.

Data Quality and Cultural Awareness Challenges

Underlying many structural problems are data and cultural issues:

- Data quality is especially poor for operational risk and cyber and technology risk, where the lack of formal systems for reporting loss events means that data on loss events is either absent or incomplete, making risk assessments rely on judgment

- In the absence of historical data, the risk register is not a credible resource for allocating resources, and organisational buy-in on its findings is diminished.

- Poor risk awareness within teams is a cultural problem: risk management is best achieved when integrated into the decision-making of all business units, rather than being centralised in a risk management function.

- This awareness needs to be cultivated through continuous training, communication, and reward systems that incentivise the open reporting of risks and discourage their concealment.

- Changing regulatory requirements in the areas of ESG, privacy, cyber, and financial services regulation require constant vigilance and responsiveness.

10Our Risk Management Process

Why a Structured Engagement Process Matters

The engagement process is the engine room of risk management advisory work. The following process is typical of best practice for an engagement with a professional risk management practitioner, from the initial diagnostic through the delivery of the final risk management framework and reporting capability.

- The process encompasses the entire process from current-state assessment to risk identification workshops, risk assessment, risk appetite framework design, mitigation planning, controls review, KRI design, and board reporting.

- Each phase depends on the previous phase, and the effectiveness of its output depends on the quality of its inputs.

Table 2: Risk Management Advisory Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — Diagnostic Assessment | Assess current risk management maturity; review existing frameworks, registers, and control documentation; benchmark against industry standards | Existing risk policy; board reports, incident history, and regulatory correspondence | Risk management maturity assessment; gap analysis against the target framework |

Step 2 — Risk Identification Workshops | Facilitate structured workshops with business unit leaders; identify risks across all five categories; develop an initial risk register | Business strategy; operational model; regulatory environment; competitive landscape | Comprehensive risk register with identified risks across all categories |

Step 3 — Risk Assessment | Apply qualitative and/or quantitative assessment methodology; rate each risk for likelihood and impact; construct a risk heat map | Risk register; historical incident data; quantitative data where available | Risk-rated register; risk heat map; priority risk list |

Step 4 — Risk Appetite Framework | Develop risk appetite statement; define quantitative risk appetite metrics by risk category; align with board’s strategic objectives | Board strategy; financial model; regulatory requirements | Board-approved risk appetite statement; quantitative risk tolerance limits |

Step 5 — Mitigation Planning | Develop mitigation strategies for priority risks; assign accountability; define timelines; assess residual risk after mitigation | Risk-rated register; available resource and capability information | Risk mitigation plans; residual risk assessment; accountability matrix |

Step 6 — Controls Review | Assess adequacy and effectiveness of existing controls; identify control gaps; design additional controls where required | Internal control documentation, audit reports, process documentation | Controls gap analysis; enhanced controls design; testing framework |

Step 7 — KRI Development | Define key risk indicators for priority risks; establish monitoring thresholds; integrate into management reporting | Risk register; business data sources; management reporting systems | KRI register; monitoring dashboard design; escalation trigger framework |

Step 8 — Board Reporting Framework | Design board risk reporting pack; establish reporting cadence; prepare first report | All prior outputs; board governance structure | Board risk reporting template; first risk report; quarterly reporting cycle |

11 Risk Management by Business Context

Why Business Context Shapes Risk Management Priorities

Different industries, business models, and organisational maturity levels have distinct risk profiles and risk management priorities. Knowing the most prevalent risk landscape for different business contexts allows practitioners to tailor engagements and management teams to prioritise their risk management resources for maximum impact.

- Context-specific frameworks and industry standards add detail to the universal frameworks and should be considered where appropriate.

- Understanding the sector's materiality landscape is critical for practitioners and management teams when considering their risk management approach.

Table 3: Risk Management Priorities by Business Context

Business Context | Dominant Risk Categories | Most Critical Management Focus | Common Framework Gaps |

|---|---|---|---|

Early-stage startup | Strategic risk; financial risk (cash burn); operational risk (founder dependency) | Cash runway management; founder risk succession; regulatory registration compliance | No formal risk register; no governance structure; all risk held by founders |

Growth-stage (Series A–C) | Strategic risk; operational risk (scaling); cyber and technology risk; compliance risk | Supply chain management; technology platform resilience; compliance framework build | Informal controls, rapid growth outpacing governance, and ad hoc incident management |

Mid-market private company | Financial risk, operational risk, compliance and regulatory risk | Internal controls maturity, working capital management, and regulatory compliance program | Inconsistent framework documentation; limited board-level risk oversight |

Listed company (ASX) | All five categories: ESG risk is increasingly material | Board-level oversight; ASX CG Principles compliance; investor and regulator reporting | Insufficient risk heat map granularity; weak KRI framework; inadequate scenario analysis |

Financial services (APRA-regulated) | Financial risk; operational risk; cyber risk; compliance risk | APRA CPG 220 / 234 compliance; capital adequacy; operational resilience; cyber maturity | Technology risk governance; third-party risk management; stress test adequacy |

Resources and infrastructure | Operational risk; strategic risk; ESG / environmental risk; cyber risk | Asset integrity; supply chain resilience; environmental compliance; OT/IT convergence risk | OT cyber risk; climate physical risk; community and social licence risk management |

12 Indicative Timeline and Frequently Asked Questions

Planning Around Realistic Timelines

When finance and risk teams are planning governance and board reporting cycles, it is important to understand how long the risk management consulting engagement will take. The complexity depends on the organisation’s size, the maturity of the framework, and the scope of work.

Table 4: Indicative Risk Management Engagement Timelines

Engagement Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

Risk assessment (single business unit) | 2–3 weeks | Availability of management for workshops; documentation quality | Focused engagement for a specific division or operational unit |

Enterprise risk assessment (full organisation) | 4–8 weeks | Organisation complexity; number of business units; regulatory scope | Includes board-level risk appetite alignment and heat map development |

Risk management framework built (greenfield) | 2–4 months | Governance design requirements; controls documentation; board approval process | Includes policies, risk register, KRIs, and reporting framework |

Controls review and gap analysis | 3–5 weeks | Number of controls in scope; documentation completeness | Standalone engagement or a component of a broader framework built |

Annual risk register refresh | 2–4 weeks (ongoing) | Change in business environment; new risk events; management availability | Efficiency improves significantly with each annual cycle |

What is the main purpose of risk management?

The purpose of risk management is to allow organisations to achieve their strategic goals while understanding the risks they are exposed to – and having the governance, processes and monitoring in place to manage those risks to acceptable levels:

- Risk management is not about avoiding all risk, but about keeping it at manageable levels.

- The benefit of risk management is not the disasters it avoids (which, by definition, do not occur) but the improved decision-making it facilitates.

- Companies with effective risk management capacity are better at allocating capital, avoiding the worst of the operational and compliance disasters, and are more resilient in times of market stress.

Is risk management mandatory in Australia?

Risk management is highly encouraged under corporate governance and regulatory frameworks in Australia, and for certain types of organisations, it is mandated by regulation:

- Listed entities are subject to the ASX Corporate Governance Principles, which include having a sound system of risk oversight and management and reporting on risk to the board.

- Financial services entities regulated by APRA must comply with prudential standards.

- For all entities subject to ASRS, climate-related financial risks must be disclosed in their risk management.

- For smaller private entities not covered by these specific requirements, lenders, investors, and insurers effectively expect risk management.

How often should risk assessments be updated?

Risk assessment should be undertaken at least once per year – and more often in response to significant changes:

- Reasons for more frequent reviews include: new acquisitions, new markets, new technologies, or significant regulatory changes.

- The annual review cycle offers a formal opportunity to review the entire risk register, learn from incidents and near misses, and assess the effectiveness of the mitigations in place.

- In the interim, key risk indicators (KRIs) provide monitoring intelligence to detect emerging risks well before they reach the review cycle, enabling a proactive rather than reactive approach.

13Challenges and Lessons Learned

The Primacy of Culture Over Structure

The single most important lesson from risk management is that culture trumps structure:

- A company with a relatively simple risk management framework but a culture in which all employees feel it is safe to bring new risks to light, in which leaders respond to accurate risk reporting with a desire to learn rather than retribution, and in which the board is actively engaged with risk information will perform better than a company with a complex framework but a compliance culture.

- The framework is the vessel in which the culture is constructed - but without culture, it is an empty vessel.

- Creating the right culture is a long-term leadership project: leaders who demonstrate objective risk assessment, respond positively to bad news, and create a safe environment in which concerns can be escalated to prevent crises.

The Incident-Register Feedback Loop

The second key lesson relates to the feedback loop between incidents and the risk register:

- In many organisations, risk management and incident management are separate processes with little systematic integration - the result is a risk register based on management's preconceived ideas about risks, rather than an empirically based knowledge of risk events that would make it useful.

- Organisations that establish a systematic feedback loop between incidents and the risk register, by rigorously analysing incident data to understand root causes, incorporating the actual events into the risk register, and using historical loss events to inform the likelihood and impact estimates, consistently have more effective and useful risk registers.

- The risk register should be an operational document, not a planning document.

The Technology and Cyber Governance Challenge

Cyber and technology risk has changed too fast for the risk management processes of most organisations:

- The governance approach - quarterly reviews of risk by the risk committee, annual updates to the risk register - is too slow to keep up with a threat environment that is evolving in days and weeks rather than months and years.

- The organisations that are best at managing cyber and technology risk have closed the loop between their technical security experts and governance structures - ensuring cyber literacy at the board level, embedding cyber risk metrics in the existing risk reporting framework, and developing incident response plans that can operate at the right speed.

- It's too late to develop that capability once a live cyber incident has occurred - it needs to be in place before.

14Conclusion and Actionable Insights

Why Risk Management Matters

Risk management is an essential element of governance and strategy in Australia. Those that do so tend to be more resilient, able to access capital more easily and have greater long-term success than those that take a more ad-hoc approach to managing risk:

- Risk management is about identifying, measuring and managing risks that may affect the financial, operational, reputational or regulatory compliance aspects of a company - the whole gamut of activities.

- The cost of developing this capability is more than offset by the return on investment, in terms of crises defused, capital costs saved, and opportunities seized with the right level of confidence.

- For companies embarking on their journey to manage risk, the most practical first step is to understand who is responsible for managing which risks - the governance structure comes first, the tools and methodologies second.

For Companies Beginning Their Risk Management Journey

Before they start building a risk register or choosing a risk assessment method, they must first clarify who is responsible for managing each type of risk, how they are held accountable for it, and how risk information is communicated from the front lines to the boardroom. The most actionable priorities:

- Design governance first: roles, responsibilities, and escalation paths; then choose frameworks and build registers.

- Use the first risk assessment as a diagnostic: identify data and capability gaps to be addressed in future assessments.

- Populate the risk register from the reality of the business, not risk categories - actionability depends on specificity.

Five Actionable Steps for Practitioners

To support the development of risk management skills in junior to mid-level practitioners, the following priorities should be considered:

- Build a deep understanding of the risk management process - including risk identification, risk assessment methods, risk prioritisation, risk mitigation planning and the monitoring and review cycle - with the ISO 31000 and COSO ERM frameworks as the key guides.

- Acquire technical skills in risk assessment techniques - especially qualitative risk assessment using rating scales, the preparation of risk heat maps, scenario analysis, stress testing, and the design and interpretation of key risk indicators (KRIs).

- Become proficient in each of the five major risk categories (financial, operational, compliance and regulatory, strategic, cyber and technology) because the most useful practitioners are those who can assess and report risk across the spectrum.

- Make the effort to understand the governance aspect of risk management - in particular, the design of the risk management governance structure, the escalation process and the risk reporting framework that links operational risk and management to the board.

- Gain experience with the full engagement cycle - diagnostic assessment, workshop facilitation, framework design, internal controls review, and board reporting development - because the ability to manage and communicate the entire risk management process is what sets the practitioners apart from the analysts with knowledge of the frameworks, but not the process.

Our risk management advisory services help organisations manage the gamut of enterprise risk – from initial risk assessments and risk heat map development to the design of a risk management framework, internal control reviews, and development of board-level risk reporting. The services are delivered with an appreciation of business processes, regulatory requirements, and the governance discipline required of today’s risk management. Risk management, when it is good, is not a cost of compliance – it is a picture of where an organisation is vulnerable, how well protected it is, and where it needs to build its defences to achieve its goals. Risk managers are not those who stop organisations from taking risks – they are those who ensure that when risks are taken, they are understood, measured and managed in a way that the board knows and has chosen. That is the discipline. |