Valuation Requirements Under Australian Accounting Standards

Table of Contents

- 01 Introduction

- 02 When Is Valuation Required Under Accounting Standards?

- 03Key Accounting Standards That Require Valuation

- 04Common Valuation Approaches Used in Financial Reporting

- 05 Key Inputs Required for Valuation

- 06 Five Key Steps: The Financial Reporting Valuation Process

- 07 Common Challenges in Valuation Compliance

- 08 Importance of Valuation in Financial Reporting

- 09 Our Valuation Process

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Introduction

- 02 When Is Valuation Required Under Accounting Standards?

- 03 Key Australian Accounting Standards Require Valuation

- 04 Common Valuation Approaches Used in Financial Reporting

- 05 Key Inputs Required for Valuation

- 06 Five Key Steps: The Financial Reporting Valuation Process

- 07 Common Challenges in Valuation Compliance

- 08 Importance of Valuation in Financial Reporting

- 09 Our Valuation Process

- 10 Indicative Timeline and Frequently Asked Questions

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Introduction

The Growing Landscape of Valuation Requirements Under Australian Accounting Standards Obligations

Businesses are required to value assets, liabilities and equity instruments at fair value or recoverable amount under Australian Accounting Standards, depending on the transaction and accounting requirements. This requirement is not new – the need to reflect economic substance rather than cost has been a feature of the Australian accounting standards framework for many years.

- Australian companies are more active in mergers and acquisitions, more complex in equity-based remuneration, and more globally exposed to capital markets.

- Both ASIC and the audit profession have come under greater scrutiny.

- This has led to a world of valuation needs that encompasses almost every corporate transaction and many annual reporting cycles.

What Independent Valuation Means

This means that independent valuation is required for financial reporting and audit, mergers and acquisitions, and share-based payments. The word “independent” is important:

- Financial reporting valuation is not a management estimate or a price in a commercial transaction.

- It is a professional estimate based on recognised valuation methods, documented in a way that would pass the scrutiny of an external auditor.

- It is undertaken by an adviser with no significant conflict of interest.

- The professional standard set by the audit profession for fair value measurements, especially those that fall under Level 3 of the AASB 13 fair value hierarchy, has been raised considerably in recent years, resulting in professional risk for entities that use valuation work that falls short of that standard.

Purpose of This Guide

This guide provides an overview of when, why and how valuation is used, and how companies comply with the relevant standards. It is intended for early to mid-career accounting, finance, advisory, legal and audit professionals who need to be aware of the entire spectrum of valuation requirements driven by Australian accounting standards:

- Whether you are a CFO gearing up for your entity's first financial report after an acquisition,

- A newly qualified accountant helping with the annual impairment testing, or

- A consultant advising a start-up company on its employee share option plan,

- This article will provide you with the conceptual understanding and practical resources to meet the requirements.

Valuation for financial reporting is not an art; it is a measurement with technical requirements, standards, and documentation that determine whether the financial statements are accurate and auditable. |

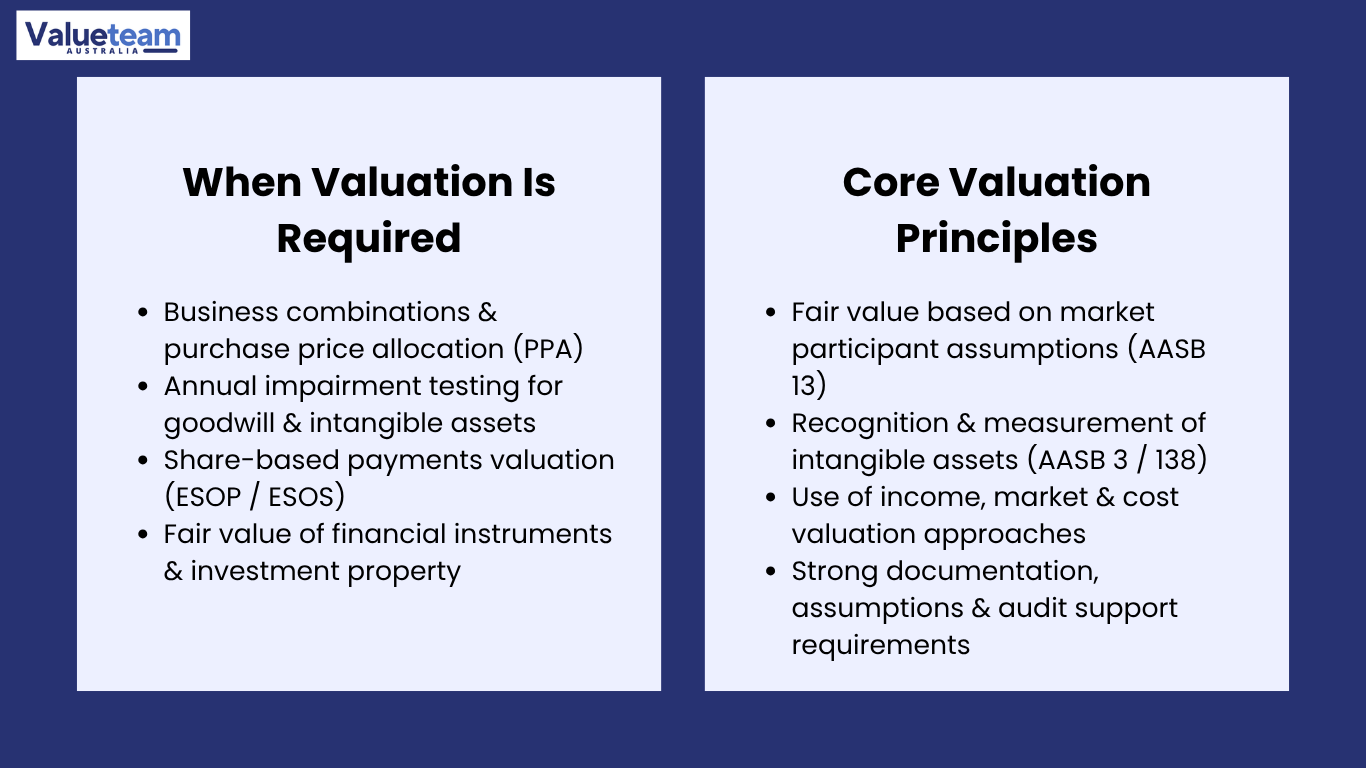

02 When Is Valuation Required Under Australian Accounting Standards?

Overview of Valuation Triggers

The triggers for a financial reporting valuation requirement are more frequent, more complex and more diverse than professionals often realise until they experience them first-hand. A complete understanding of the triggers (and the Australian accounting standards that apply to each) is the first thing any financial reporting, audit, or corporate transaction professional needs to know.

Primary Triggers

The most prominent trigger is business combinations and acquisitions:

- On the acquisition of another entity, AASB 3 requires the acquirer to recognise and measure at fair value all identifiable assets acquired and liabilities assumed, including assets that were not previously recognised on the target's balance sheet.

- This involves a purchase price allocation (PPA) calculation that usually requires the independent valuation of customer relationships, brands, technology assets and other intangibles that must be separately accounted for under the standard.

Impairment Testing

The most common triggers are impairment testing of assets and goodwill:

- The need to reassess at least annually whether goodwill and indefinite-lived intangibles can continue to be carried at their current book values.

- Impairment testing based on indicators for all other assets covered by AASB 136.

Share-Based Payments and Financial Instruments

Share-based payments (ESOP / ESOS) create a valuation obligation under AASB 2 that applies to every entity that issues equity-based compensation instruments (regardless of size, listing or profitability). Additional triggers include:

- Fair value measurement of financial instruments, such as derivatives, equity investments carried at fair value through profit or loss, and some debt instruments, which require periodic valuations under AASB 9 and AASB 13.

- Recognition of intangibles in acquisitions.

- Valuation of investment property for entities that adopt the fair value model for investment property.

- Valuation in relation to restructuring or transfers of assets between related parties at arm's length prices.

Table 1: Valuation Triggers Under Australian Accounting Standards

Trigger | Applicable Standard | Frequency | Typical Valuation Type |

|---|---|---|---|

Business combinations/acquisitions (PPA) | AASB 3 Business Combinations | On acquisition, 12-month measurement period | Intangible assets, CGU, contingent consideration |

Goodwill impairment testing | AASB 136 Impairment of Assets | Annually (mandatory); more frequently if indicators present | Value in use (DCF) or FVLCD of CGU |

Impairment testing (other assets) | AASB 136 Impairment of Assets | When impairment indicators are identified | Value in use or FVLCD of individual assets or CGUs |

Share-based payments (ESOP / ESOS) | AASB 2 Share-Based Payments | At the grant date, remeasured at each period for cash-settled | Black-Scholes, binomial, or Monte Carlo model |

Fair value measurement of financial instruments | AASB 9 / AASB 13 | At each reporting date for FVTPL instruments | DCF, option pricing, or market comparables |

Intangible asset recognition (post-acquisition) | AASB 138 / AASB 3 | At the acquisition date, annually for indefinite-life | Relief from royalty, MPEEM, cost approach |

Investment property (fair value model) | AASB 140 Investment Property | Annually, at each reporting date | Market approach: DCF for income-generating properties |

Restructuring / intercompany transfers | AASB 13 / ATO Transfer Pricing | When transfers occur, annually for ongoing arrangements | Arm’s length price; DCF; market comparables |

03Key Australian Accounting Standards Require Valuation

Understanding the Standards Framework

Each of the key Australian Accounting Standards (AASBs) that trigger valuation requirements has specific measurement purposes, techniques, and disclosure requirements that govern how the valuation must be performed and what information is needed to audit it. It’s essential to understand these standards, not simply as compliance requirements, but as conceptual models that reflect different economic measurement objectives, to underpin professional valuation practice in financial reporting.

AASB 13 — Fair Value Measurement

The Cornerstone Standard

The Australian Accounting Standards Board’s (AASB) Fair Value Measurement (AASB 13) is the “parent” standard for measuring fair value in financial reporting. It sets a single point of reference for the definition of fair value – the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date – and a three-part hierarchy:

- Level 1 inputs are quoted prices in active markets (the most reliable).

- Level 2 inputs are other observable inputs.

- Level 3 inputs are unobservable inputs, for which the entity must make its own assumptions about what market participants would use.

- The majority of valuations for financial reporting, such as recognition of intangible assets, impairment testing using the FVLCD approach, and valuations of unlisted equity instruments, fall under Level 3 and are subject to the most rigorous audit procedures and the most comprehensive disclosure requirements.

Practical Implications for Practitioners

Fair value measurement must be based on market participant assumptions – not entity-specific preferences, plans or synergies:

- Discount rates, growth rates and market risk premiums used in the fair value DCF must be calibrated to those used by a hypothetical market participant in an orderly sale.

- This issue - of entity value versus market participant value - is one of the most frequently misunderstood aspects of AASB 13.

- It is also one of the most common areas of challenge for auditors of valuations for financial reporting.

AASB 3 — Business Combinations

Purchase Price Allocation Requirements

Under AASB 3 Business Combinations, acquirers must measure the fair values of the assets acquired and liabilities assumed at the date of the business combination, and allocate the entire purchase consideration paid for the business to these assets and liabilities. The purchase price allocation (PPA) exercise is one of the most complex valuation exercises in financial reporting:

- It involves not only the valuation of tangible assets, but also the recognition and separate valuation of intangible assets that may not have been recognised on the target's balance sheet.

- As per AASB 3, an intangible asset must be recognised separately from goodwill if it satisfies either the contractual-legal criterion (stemming from legal or contractual right) or the separability criterion (separable and exchangeable).

- This results in the recognition of assets including customers, trade names, technology, order backlog and non-compete agreements.

Goodwill and Its Long-Term Consequences

The remaining value after allocating the fair value of all recognised assets and liabilities is goodwill, which is the portion of the value of the acquisition that cannot be separately identified and measured (such as synergies, the assembled workforce and market position):

- Goodwill is not amortised under AASB 3 and AASB 136; it must be annually tested for impairment at the cash-generating unit (CGU) level.

- This means that the allocation of goodwill to CGUs in the PPA is important not only for the initial balance sheet at the acquisition date but also for all subsequent impairment tests.

- So the AASB 3 PPA is a long-term financial reporting investment (or a disinvestment if not done well).

AASB 136 — Impairment of Assets

Scope and the Recoverable Amount Measurement

AASB 136 Impairment of Assets prescribes the annual impairment testing for goodwill and indefinite-life intangibles, and indicator-based testing for all other assets in its purview. The recoverable amount, the greater of fair value less costs of disposal (FVLCD) and value in use (VIU), is used to assess impairment. Value in use is subject to certain constraints:

- Cash flows must reflect the asset in its existing state (no unplanned restructurings or acquisitions).

- The terminal growth rate should not exceed the market's long-term average.

- The discount rate must be a pre-tax rate that reflects current market expectations of the time value of money and the asset's risks.

The Challenge of Management Subjectivity

The difficulty of complying with AASB 136 is the blend of technicality and management judgement required:

- The value in use is based on management's projections of future cash flows, which are necessarily uncertain and unavoidably influenced by management's optimism about the future.

- Auditors must assess the reasonableness of these projections, with the budget accuracy test (comparing the previous year's forecast to actual outcomes) being a very effective tool.

- The sensitivity analysis required by AASB 136 for assets with recoverable amounts close to their carrying amounts provides information that enables investors and auditors to determine whether the impairment decision is sustainable in reasonably foreseeable adverse scenarios.

AASB 138 — Intangible Assets

Recognition Criteria and Post-Acquisition Treatment

AASB 138, Intangible Assets, covers the recognition, measurement, and disclosure of intangible assets. It states that an intangible asset should only be recognised if it is identifiable, the entity has control over it, and it is expected to provide future economic benefits:

- Historical cost accounting rules do not allow internally developed intangibles, such as customer lists, brands, and technology, to be recognised on the balance sheet; they are written off as expenses.

- However, when the same intangibles are acquired in a business combination, AASB 3 requires them to be separately identified and measured at fair value, and the balance recognised on the post-acquisition balance sheet is amortised over the useful life of the intangible asset.

The Useful Life Assessment

Where the useful life of intangibles is finite, the annual amortisation charge is recognised in the income statement and impacts earnings:

- The determination of the useful life, which is the expected period over which the asset will be used to generate economic benefits, is a critical assumption in the financial reporting valuation process.

- It needs to be consistent between the valuation model (using the life to establish the cash flow projection period) and the accounting treatment (using the same life for amortisation).

- Auditors scrutinise this consistency, and differences between the implied useful life in the valuation model and the amortisation period in the accounting are a frequent issue in the audit of compliance with AASB 138 and AASB 3.

AASB 2 — Share-Based Payments (ESOP / ESOS)

Recognition and Scope

Under AASB 2 Share-Based Payments, entities that issue equity compensation instruments (such as employee stock options, restricted share units (RSUs), performance rights and management incentive plans) must recognise a share-based payment expense, equal to the fair value measurement of the instruments at the date of grant, over the vesting period:

- This recognition applies to all entities that grant equity compensation, whether listed, unlisted, profitable or pre-revenue.

- This expense is recognised in the income statement as a cost of personnel and impacts reported earnings, making the quality of the ESOP/ESOS valuation a financial statement issue.

Valuation Model Selection

The models used to comply with AASB 2 depend on the plan design:

- The Black-Scholes model is the most common for typical employee stock options with straightforward exercise rights and no complex performance hurdles.

- The binomial models are generally used for options with American-style exercise rights, multiple vesting conditions or non-market performance rights.

- Monte Carlo simulation is needed for market-based awards, such as total shareholder return (TSR) performance rights, where payouts are based on relative share price performance over a measurement period.

- For unlisted companies, the fair value of the underlying equity instrument (the current share price) must be determined through a business or equity valuation to apply the option pricing model.

AASB 140 / AASB 9 — Investment Property and Financial Instruments

Investment Property Under the Fair Value Model

Where an entity elects to use the fair value measurement model allowed by AASB 140 to measure investment property, the property needs to be remeasured to fair value at each reporting date, with any changes reflected in the income statement:

- This can be achieved through an annual independent valuation or an internal valuation with independent evidence.

- The auditor of an entity with significant investment property balances is likely to require at least annual independent valuations as evidence of the fair value measurement.

Financial Instruments Under AASB 9

AASB 9 Financial Instruments requires fair value measurements for:

- Equity investments that are designated at fair value through other comprehensive income.

- Financial instruments are measured at fair value through profit or loss.

- Certain debt instruments.

- The fair value of unlisted equity investments, in particular, requires the use of valuation techniques that match the nature of the investee company (typically DCF or market multiples) at each reporting date.

04 Common Valuation Approaches Used in Financial Reporting

Overview of the Three Principal Methodologies

The three main valuation approaches used for financial reporting purposes (the income approach, the market approach and the cost approach) are applied at the level of the individual asset. The choice of the most appropriate approach is a key element of the auditor’s review of valuations for financial reporting.

Income Approach

The income approach is based on valuing an asset as the present value of the future income expected to flow from it. The discounted cash flow (DCF) method is the main manifestation of this approach:

- It is widely used in impairment testing (as the value-in-use calculation under AASB 136), in valuations of businesses and CGUs for PPA and fair value reporting purposes, and in valuations of income-generating intangible assets.

- The AASB 136 value-in-use model is a specialised form of DCF with constraints designed to align with market participants.

- The excess earnings method - used mainly for recognising intangible assets, such as customer relationships and technology assets, in PPA exercises - separates the income attributable to the subject intangible from that attributable to other assets.

- The relief from royalty method values an intangible asset by reference to the royalty payments avoided by owning rather than licensing the asset - the main method used for brands and trademarks in AASB 3 PPA exercises.

Market Approach

The market approach relies on observable market evidence (from comparable listed companies or comparable transactions) to determine value by reference to market prices of similar assets or businesses:

- Market multiples from comparable listed companies provide Level 2 inputs under the AASB 13 hierarchy, where the companies are comparable to the subject entity.

- Acquisitions of comparable businesses provide evidence of the control premium and the multiples applied to different types of assets.

- Market data - such as royalty rate data for intangible assets and cap rates for investment properties - provide the market-based inputs that support the income approach.

- In financial reporting, the market approach is often used as a second approach to corroborate the income approach, especially when the adjustment to make the comparables comparable can be hard to justify under audit.

Cost Approach

The cost approach is based on the cost of replacing an asset with an asset of equal utility:

- It is most commonly used for assets where the most relevant basis of value is replacement cost (such as internally developed software or proprietary databases, or assembled workforces), and where the income approach produces valuations that are difficult to benchmark against independent data sources.

- The cost approach is adjusted for obsolescence: physical deterioration, functional obsolescence (functional inferiority to a new replacement), and economic obsolescence (external factors).

- The cost approach is often used for assembled workforce and technology infrastructure assets under AASB 3 PPA, as a floor test for income-based valuations, and as the only approach when the asset is not generating uniquely identifiable cash flows.

05Key Inputs Required for Valuation

The Importance of Input Quality

The inputs to a financial reporting valuation serve as the foundation for the valuation, and developing a structured, systematic process for collecting and documenting them is one of the key operational skills for someone producing or reviewing financial reporting valuations.

- Every input must be sourced, documented, and compared with other similar data (for reasonableness) before being used in a valuation model.

Financial and Forecast Inputs

Historical financial statements and management forecasts underpin the quantitative aspects of any income approach valuation:

- Historical financial statements - usually the past three to five years of audited reports - supply the quantitative foundation, showing the historical performance trend, profit margin profile, working capital requirements, and capital expenditure patterns that will inform the forward-looking projections and ensure they are rooted in real-world operational experience.

- Management forecasts - the forward-looking cash flow projections that feed the value in use calculation in AASB 136 and the income approach in AASB 3 PPA valuations - need to be assessed for reasonableness, consistency with the past and in accordance with the particular constraints of the applicable standard.

- The budget accuracy analysis - comparing prior year forecasts to actual outcomes - is the most effective means of gauging the credibility of the forecasts and is an essential part of an auditor's review.

Asset, Legal and Market Inputs

A full suite of asset, legal and market data is needed to complete the information package for a professional financial reporting valuation:

- Asset registers - the physical counts and carrying values of tangible assets - are the foundation for AASB 136 impairment testing and AASB 3 tangible asset valuations.

- Acquisition documents (the share purchase agreements, asset purchase agreements, and disclosure schedules) are the key legal documents that define the extent and nature of business combinations under AASB 3.

- Capital tables - reflecting the entire capital structure of the entity, including all common shares, preference shares, convertible securities and options - are required for ESOP / ESOS valuations.

- Discount rates, market comparables and contract and customer data for intangibles valuations complete the standard data package required for a professional financial reporting valuation exercise.

06 Five Key Steps: The Financial Reporting Valuation Process

Overview of the Process

The financial reporting valuation process is a five-step process that begins with identifying the reporting requirement and standard and ends with the provision of audit documentation. This process is important for finance teams to plan their reporting cycles, for auditors to understand the evidence available to support their audit procedures, and for valuation practitioners to appropriately scope their engagements.

Step 1 — Identify the Reporting Requirement and Applicable Standard

The first step in every financial reporting valuation is to identify the accounting standard that establishes the valuation requirement and the measurement objective it requires. Sounds easy, but it isn’t always – there can be multiple valuation requirements in play under different standards:

- For instance, an acquisition gives rise to a business combinations PPA valuation under AASB 3.

- It can give rise to a potential impairment test for pre-existing goodwill in the acquirer's balance sheet (if the acquisition alters the CGU structure).

- And possibly an ESOP / ESOS valuation requirement if management incentive schemes are amended as part of the acquisition.

- Identifying all of the standards and their associated measurement requirements up-front avoids the omissions that are the biggest source of audit issues later in the process.

Step 2 — Define the Scope and Asset Inventory

Once the relevant standards have been identified, the next step is to build a detailed inventory of all assets, liabilities and equity instruments that need to be valued:

- For a business combinations PPA exercise: a thorough review of the acquired business to identify all intangible assets that may qualify for recognition under AASB 3 - not just those reported in the target's pre-acquisition financial statements.

- For an impairment testing exercise: confirming the CGU structure, allocation of goodwill and intangibles to the relevant CGUs and the continued suitability of the CGU definitions in light of any changes in the organisation's structure or strategy.

- For an ESOP / ESOS valuation: confirming the full list of outstanding grants, their terms and conditions, and how they are accounted for (under AASB 2).

Step 3 — Data Collection and Documentation

The data collection step brings together the full information package needed to calibrate the valuation models – financial reports, management projections, asset registers, legal documents, market data and comparable company or transaction data:

- The documentation standard is higher for financial reporting valuations than for commercial valuations.

- All data must be sourced to a document, all calculations must be documented in sufficient detail to allow replication by a third party, and all assumptions must be justified either by management's rationale, or by other market evidence.

- The documentation produced in this step is the working paper package that the auditor will review, and the quality and completeness of the package affect the audit process itself.

Step 4 — Valuation Analysis and Methodology Application

Once the scope and data collection are complete, the valuation analysis applies the appropriate methodology to each item in scope. The methodology must be applied in line with the requirements of the accounting standard, as well as the nature of the asset being valued:

- For AASB 136 impairment tests, the value-in-use calculation must comply with the specific AASB 136 requirements regarding cash flow projections and terminal growth rates.

- For AASB 3 intangible valuations, the contributing asset approach must be applied to all intangibles to avoid double-counting or missing cash flows.

- For AASB 2 share-based payments (ESOP/ESOS), the model used must be suitable for the particular plan features (Black-Scholes for simple grants, binomial/trinomial for American-style and performance-conditioned grants, and Monte Carlo for market-linked awards).

- Several standards mandate sensitivity analysis of key assumptions, and it is good practice for all financial reporting valuations.

Step 5 — Audit Support and Final Report

The final step is preparing the documentation package and the valuation report that the auditor will use to review the financial reporting valuation. The report must document:

- The standard and measurement objective, the scope of the valuation and the information used.

- The valuation approach used, the reasons for its use, all significant assumptions, and the basis for benchmarking.

- The sensitivity analysis and the fair value conclusions.

- For valuations for financial reporting purposes that fall under the Level 3 category of the AASB 13 hierarchy, the report must also consider the specific disclosures required for unobservable inputs, as well as the sensitivity analysis disclosures required by the standard.

- Collaborating with the audit team early in the audit process - before the audit commences - to provide draft conclusions is the best way to control the timing and cost of the audit compliance process.

07Common Challenges in Valuation Compliance

Overview of Recurring Challenges

The most common issues encountered in financial reporting valuation compliance are technical and organisational, and being aware of these issues helps practitioners and finance staff resolve them in advance of an audit cycle.

Inconsistent Financial Forecasts

The most common source of financial reporting valuation problems is inconsistent financial forecasts:

- Companies that use different forecasts for impairment testing, for their ESOP/ESOS valuations, and in their investor communications will create inconsistencies that auditors will detect and require explanation.

- All valuations for financial reporting in the same period should be based on a set of management assumptions.

- Any variations from the assumptions should be supported by documentation and explanation.

- A DCF applied in an AASB 136 impairment test assuming 8% revenue growth. In comparison, a business combination PPA applied to an acquisition in the same reporting period assumes 15% growth, which will be of considerable interest to the auditor - and rightly so.

Lack of Supporting Documentation

The failure to document key assumptions is the most frequent cause of late-stage audit issues and additional audit fees:

- Discount rates that are not linked to a WACC calculation, royalty rates that are not benchmarked to comparable licensing arrangements, and volatility rates for ESOP/ESOS valuations that are not derived from benchmarking to listed companies all require additional work by auditors.

- The up-front costs of investing in a structured approach to documentation - a fully completed assumption register, a benchmarking document and a version-controlled working paper package - are invariably offset by the benefits of reduced audit time and increased audit efficiency.

Incorrect CGU Structure

The increasingly prevalent failure of incorrect CGU structure is a governance failure with financial statement implications that can extend beyond the current period:

- Setting CGUs too broadly to mask impairment at the sub-CGU level.

- Not adjusting CGU structure after an acquisition or restructuring.

- This structural error can lead to impairment not being reported for several periods before an auditor spots tit

08Importance of Valuation in Financial Reporting

Beyond Technical Compliance

The value of financial reporting valuation is not just about compliance – it’s critical to the integrity of the financial statements that investors, lenders, boards and regulators rely on. Accurate valuation supports compliance with Australian accounting standards, financial statement accuracy, auditability, and investor confidence.

The True Purpose of the Standards

Adherence to Australian accounting standards is the minimum standard – but not the only one:

- A valuation that is compliant with the letter of the applicable accounting standard but that presents an incorrect economic view of the entity's financial position does not fulfil the purpose of the Australian accounting standards.

- The purpose of AASB 13 fair value measurement is to provide investors with an economically meaningful, transparent picture of the value of assets - not to generate a number that "checks the box" for an auditor.

- The purpose of AASB 136 impairment testing is to ensure that the balance sheet does not overstate the value of assets that have lost value - not to produce a VIU calculation that, by making optimistic assumptions, never results in a write-down.

- Those who grasp the economic purpose of the standards (not just the technicalities) produce financial reporting valuations that are more useful to their clients.

Consequences of Poor Valuation Practices

Inadequate valuation practices can lead to audit qualifications or restatements. This is not a theoretical outcome:

- ASIC's financial reporting surveillance program has frequently highlighted insufficient impairment testing, overly aggressive business combinations PPA allocations, and lack of documentation of assumptions in ESOP / ESOS valuations in the financial reports of listed entities.

- The tangible cost of a qualified audit or financial restatement (in management and external audit resources, investor confidence, and reputation) far outweighs the cost of establishing a satisfactory valuation process in the first place.

- The reputational impact of a high-profile financial restatement can be significant for years to come, impacting the entity's cost of capital, institutional investor confidence, and auditor relationship.

- The cost of audit readiness through quality financial reporting valuation is not a compliance expense - it is a risk mitigation investment with a strong return.

09Our Valuation Process

A Structured, Repeatable Engagement Framework

A repeatable engagement process is the key to high-quality financial reporting valuations. The following is a typical best practice process for a professional engagement – from identifying the reporting requirements to delivering the audit-ready report.

- The process has clear inputs, actions and outputs for each stage, providing a full engagement workflow.

- The process is an interactive one - leveraging the internal expertise of the finance team, and applying professional advisory rigour to the structure, analysis and reporting.

- The workflow is interactive with the audit team.

Table 2: Financial Reporting Valuation Engagement Process Flow

Step | Activity | Key Inputs | Output |

|---|---|---|---|

Step 1 — Reporting Requirement Identification | Identify all applicable Australian accounting standards for the reporting period; map each to the specific assets, liabilities, or instruments requiring valuation | Transaction documents; financial statements; management briefing on reporting obligations | Standards mapping; valuation requirement schedule; scope memo |

Step 2 — Scope and Asset Inventory | Define scope; build complete asset and instrument inventory; confirm CGU structure for impairment testing | Asset register; acquisition documents; ESOP scheme documents; cap table | Complete asset inventory; CGU structure map; goodwill allocation confirmation |

Step 3 — Data Collection | Collect all required financial, legal, and market data; review historical forecasts vs actuals; assemble documentation package | Financial statements; management forecasts; contracts; comparable market data; discount rate inputs | Documented assumption register; benchmarking file; working paper package |

Step 4 — Valuation Analysis | Apply appropriate methodology to each asset/instrument; build models; run sensitivity analysis; cross-check conclusions | All collected data; management discussions; methodology selection rationale | Valuation models; sensitivity tables; fair value conclusions per asset/instrument |

Step 5 — Audit Support and Review | Share draft conclusions with audit team; respond to queries; provide additional documentation as required | Draft valuation conclusions; audit team queries; management factual review | Audit evidence package; responded queries; disclosure draft support |

Step 6 — Final Report | Prepare final valuation report with full methodology, assumptions, analysis, and conclusions; issue signed final opinion | All prior outputs; management sign-off; audit team confirmation | Final signed financial reporting valuation report; AASB disclosure support |

10Indicative Timeline and Frequently Asked Questions

Planning Your Financial Reporting Valuation Timeline

For finance professionals working on year-end financial reporting and audit compliance timelines, it is important to understand the expected engagement time for the various types of financial reporting valuation. The timelines can vary greatly depending on:

- The nature of the valuation need and the volume of assets or instruments involved.

- The quality of information such as management forecasts and market data.

- The coordination needed with the auditor and auditor pre-engagement.

Table 3: Indicative Financial Reporting Valuation Timelines

Valuation Type | Typical Timeline | Primary Determinant | Notes |

|---|---|---|---|

ESOP / ESOS valuation (standard options) | 1–2 weeks | Completeness of grant documentation; equity valuation currency (unlisted) | Requires underlying equity valuation if company is unlisted |

Impairment testing (single CGU, high headroom) | 1–2 weeks | Forecast quality; WACC derivation; data availability | Limited sensitivity required where headroom is substantial |

Impairment testing (multiple CGUs / low headroom) | 2–4 weeks | Number of CGUs; forecast complexity; auditor pre-engagement | More intensive auditor involvement; sensitivity disclosure drafting |

Business combinations PPA (standard) | 2–4 weeks | Number of intangibles; forecast availability; contract documentation | Coordination with audit team required before first post-acquisition report |

Complex PPA (multiple intangibles, cross-border) | 4–8 weeks | Intangible identification complexity; cross-border tax implications | Listed entities; complex capital structures; multi-jurisdiction acquisitions |

Investment property / financial instruments | 1–3 weeks per asset | Property type; financial instrument complexity; market data availability | Ongoing annual requirement; efficiency improves with each cycle |

Frequently Asked Questions

When Is Valuation Required Under Australian Accounting Standards?

Valuation is required when an asset, liability, or equity instrument is to be measured at fair value or at recoverable amount under the accounting standard. The most common triggers are:

- Acquisitions under AASB 3 (requiring PPA).

- Impairment under AASB 136 (requiring annual testing for goodwill and indefinite-life intangibles, and indicator-based testing for other assets).

- Share-based payments (ESOP / ESOS) under AASB 2 (requiring grant-date fair value for all equity-settled plans).

- Fair value of financial instruments under AASB 9 and AASB 13 at each reporting date.

Is Valuation Mandatory for Private Companies?

Yes – if the private company prepares general purpose financial statements in accordance with Australian Accounting Standards, then all of the measurement requirements outlined in this guide will apply, whether the entity is listed or unlisted:

- Australian Accounting Standards require businesses to measure certain assets, liabilities and equity instruments at fair value or recoverable amount - and this is true for all entities preparing financial statements under the Australian Accounting Standards, including small and medium-sized private companies.

- In reality, private companies that are not required to have their financial statements audited by an external auditor may have greater flexibility in preparing their financial statements.

- However, any entity required to prepare audited financial statements under Australian Accounting Standards, or that has external investors or lenders relying on those financial statements, will be subject to the full gamut of financial reporting valuation requirements.

What Are the Most Common Valuation Requirements?

For the vast majority of Australian companies with active M&A programs, the combination of business combinations PPA (AASB 3), annual impairment testing (AASB 136) and share-based payments (ESOP / ESOS) valuation (AASB 2) constitutes the core of their financial reporting valuation requirements:

- Business combinations PPA is the most complex, involving the identification and measurement of several intangible assets within the short timeframe of the post-acquisition financial close.

- Impairment testing is the most common - resulting in an annual recurring valuation task for any entity with significant goodwill.

- ESOP/ESOS valuation is the most ubiquitous, impacting all entities that issue equity-based compensation, regardless of maturity, size, or profitability.

11 Challenges and Lessons Learned

Lessons Consistent Across Financial Reporting Valuation Practice

Financial reporting valuation practice under Australian Accounting Standards produces a uniform set of lessons that seasoned practitioners bring to each assignment – and that junior practitioners learn, often in the heat of an audit cycle that brooks no lack of preparation.

Lesson 1: The Importance of Early Engagement

The most common lesson is the importance of early engagement. The most frequent and most expensive mode of failure in financial reporting valuation is starting late:

- The tight timeframe for completing a post-acquisition AASB 3 PPA (within the measurement period, while the entity is also managing the integration, preparing its first set of post-acquisition financial statements, and managing audit procedures for the combined entity) cannot be shortened by delaying the start of the work.

- The best way for entities to manage this challenge is to engage the AASB 3 PPA work before the acquisition closing - to access the transaction data room materials, to start to identify intangible assets, and to build the financial model using pre-close data.

- Beginning the work after the deal is done and the audit clock has started is one of the most common and costly errors in financial reporting valuation.

Lesson 2: Managing Concurrent Valuation Obligations

A second key lesson concerns the interconnections among the valuation obligations under the Australian accounting standards that may arise from a transaction. When an entity acquires another entity, several simultaneous valuation obligations arise:

- The AASB 3 PPA obligation.

- Potentially an AASB 136 impairment test for any goodwill in the acquirer's balance sheet (if the acquisition alters the CGU structure).

- Potentially an AASB 2 share-based payments (ESOP / ESOS) valuation if the management incentive plans are changed as part of the deal.

- These obligations have different requirements and audit evidence requirements, but also common data inputs (the financial projections, the discount rates, the equity valuation) that need to be consistent across all three valuations.

- The CFO and financial controller who develop an integrated information-collection process that feeds all the simultaneous valuation obligations will consistently produce better results, in a shorter time and at a lower overall cost.

Lesson 3: The Documentation Imperative

The last lesson is the documentation imperative. There is a degree of external scrutiny of financial reporting valuations, by auditors, by regulators, and perhaps by the courts in contentious transactions, that does not apply to management estimates:

- The documentation standard for a Level 3 fair value measurement under AASB 13 is rigorous. All unobservable inputs must be identified and justified with reference to market evidence, and disclosed in the financial statements in sufficient detail for an advanced user to comprehend the nature of the measurement.

- Organisations that design financial reporting valuations around this documentation standard from the beginning - rather than "dusting off" documentation in response to audit inquiries - enjoy faster and smoother audits and audit opinions.

- The discipline of documentation magnifies the incremental improvement in financial reporting quality over time.

12 Conclusion and Actionable Insights

Summary

Australian Accounting Standards require companies to value some assets, liabilities and equity instruments at fair value or recoverable amount – a reality that affects every major corporate transaction, every financial year-end close and every entity that issues equity-based compensation. Specialist valuations are frequently needed for financial reporting, audit purposes, M&A transactions and share-based payments.

- Mapping the standards at the start of the financial year (and before any major transactions) is the best way to enhance the quality of valuations for financial reporting, and audit efficiency.

- All relevant requirements under AASB 3, AASB 136, AASB 2, AASB 13, AASB 138 and AASB 140 should be mapped out before the audit starts, with a plan developed around a centralised information collection process.

- This pre-emptive strategy has been proven to lead to faster audits, reduced fees, and fewer audit qualifications.

Key Principles for CFOs and Financial Controllers

- Develop an integrated valuation plan that meets all requirements through a single information-collection process.

- Use the same, "official" set of management assumptions for all financial projections used for valuations for the same reporting period.

- Bring in valuation advisers early - preferably before deals close - to avoid rushed work.

- Prioritise documentation rigour: assumption registers, benchmarking files, version-controlled working paper packages and Level 3 evidence from the start.

Actionable Development Path for Junior and Mid-Level Professionals

- Understand the six core standards (AASB 13, AASB 3, AASB 136, AASB 138, AASB 2, AASB 140) well, both in terms of their economic measurement objectives and technical provisions.

- Develop a high degree of technical competency in the three main valuation approaches: income approach (DCF, value in use, excess earnings method), market approach (trading multiples, precedent transactions), and cost approach - and the circumstances under which each is preferred.

- Learn a workpaper discipline - the practice of producing complete, traceable, assumption-documented workpaper packages that provide the evidence standard required for audit purposes.

- Gain exposure to the breadth of financial reporting valuation contexts - AASB 3 PPA, AASB 136 impairment testing and AASB 2 ESOP / ESOS valuations - as those who are comfortable with all three are more valuable.

- Understand the auditor's perspective - what the auditor needs to test, what evidence they need to have, and how the timing and quality of the valuation work impacts on the auditor's work.

Financial reporting valuation is all about one thing: ensuring that the financial statements present users with an accurate, technically sound, and well-documented view of the business’s economic realities. That’s worth striving for – and worth a career. |