Sustainability Reporting in Australia

Table of Contents

- 01 Sustainability Reporting Services in Australia Overview

- 02 AASB S1 and S2 Framework

- 03Materiality Assessment

- 04 Governance Disclosures

- 05 Strategy and Climate Risks

- 06 Scope 1, 2 and 3 Reporting

- 07 Scenario Analysis

- 08Targets and Metrics

- 09Data Collection and Management

- 10 ASIC Lodgement and Assurance

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

Table of Contents

- 01 Sustainability Reporting Services in Australia Overview

- 02 AASB S1 and S2 Framework

- 03Materiality Assessment

- 04 Governance Disclosures

- 05 Strategy and Climate Risks

- 06 Scope 1, 2 and 3 Reporting

- 07 Scenario Analysis

- 08Targets and Metrics

- 09Data Collection and Management

- 10 ASIC Lodgement and Assurance

- 11 Challenges and Lessons Learned

- 12 Conclusion and Actionable Insights

01 Sustainability Reporting in Australia Overview

The Shift from Voluntary to Mandatory

An Australian boardroom, finance team and accounting practice turning point is underway. Preparing Sustainability reporting in Australia has traditionally been more of a voluntary add-on to an annual report, a well-meaning side-note to a marketing-intuitive model that lacks rational structures. That era is ending.

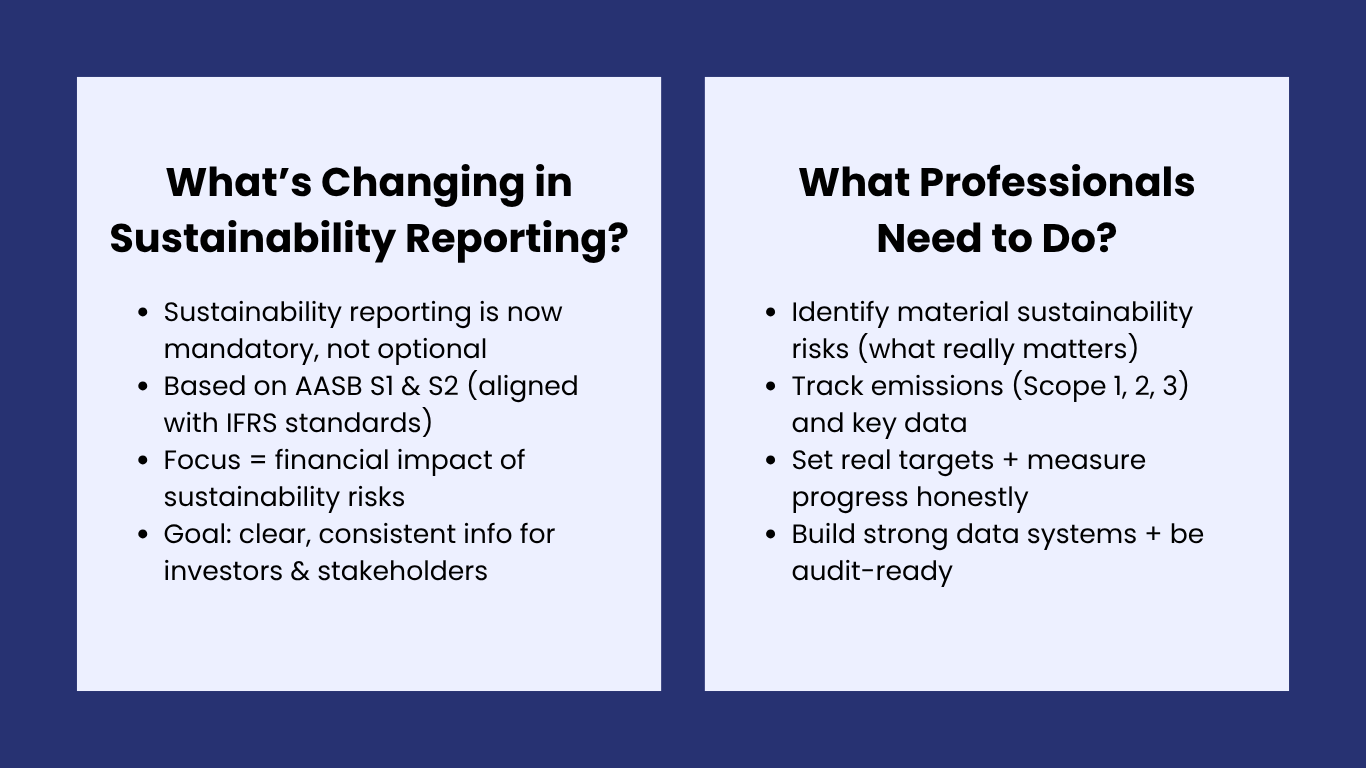

- Sustainability reporting is becoming mandatory, standardised and as rigorous as financial statements in Australia.

- Whether companies will report or not is no longer the issue; the issue is whether they can report credibly.

- This change is a real turning point for the professions of sustainability, finance, audit, law, and corporate advisory.

The Regulatory Driver

A mix of regulation and international harmonisation is driving this change, which is being accelerated by one of the biggest milestones in global sustainability standards-setting.

- In June 2023, ISSB issued IFRS S1 (general sustainability-related disclosures) and IFRS S2 (climate-related disclosures), establishing a universal framework.

- Australia reacted swiftly: the AASB adopted AASB S1 and AASB S2, which were closely aligned with their IFRS equivalents.

- AASB S2 climate-related disclosures are mandatory in-scope entities and are analogous to IFRS S2.

- Knowledge of the architecture of these standards has already become a professional competency for anyone who works in or around this space.

Who This Guide Is For

This guide is intended as a working guide for professionals at the junior to mid-level of their careers. It discusses every aspect of the reporting structure in a logical order.

- Discusses materiality assessment, governance disclosures, scope emissions, scenario analysis, targets and metrics, and ASIC lodgement.

- Does more than just explain what is needed, why it is important and how plausible organisations go about each challenge in practice.

- Intends to provide the reader with terms, structures, and on-the-job experience to play an important role in sustainability reporting within their organisation.

Sustainability is no longer a communications activity. It is a financial reporting requirement and must be carried out with the same discipline, documentation, and professional scepticism as any other section of a company’s audited accounts. |

02 AASB S1 and S2 Framework

Who This Guide Is For

To understand the AASB S1 and S2 framework, it is necessary to know its purpose. It does not aim to measure corporate goodness or rank businesses by environmental practices.

- The rationale is to provide investors, lenders, and other capital market participants with consistent, comparable, decision-useful information on sustainability-related risks and opportunities.

- It pays special attention to climate-related exposures and opportunities that can reasonably affect a company's cash flows, access to finance, or loss of capital.

- The time horizon covers short-, medium-, and long-term.

The Two Standards Explained

AASB S1 and AASB S2 have different yet complementary functions within the framework, with AASB S2 bearing the bulk of the technical burden.

- AASB S1 covers general requirements on financial disclosure on sustainability - including materiality concepts, reporting limits, and integration with financial reporting.

- AASB S2 is the climate-specific standard that mandates disclosure across four thematic pillars known to TCFD practitioners: governance, strategy and climate risks, risk management, and targets and metrics.

- The TCFD alignment is not accidental - organisations that have already committed resources to TCFD-aligned reporting have a significant head start. Still, AASB S2 requirements are even more thorough in several key ways.

Phased Implementation and Career Opportunity

The development strategy implemented in Australia is incremental, recognising that not all organisations are equal in terms of reporting capacity, and it creates a structured rollout that benefits professionals at all levels.

- Group 1 entities - the largest listed and unlisted entities with substantial public interest must report first, with smaller groups reporting in later years.

- This progressive implementation offers a learning experience for professionals working in smaller organisations based on the initial experiences of larger reporting organisations.

- The need to hire professionals with expertise in sustainability reporting will remain high over the next three to five years, with considerable career opportunities across different fields.

Table 1: AASB S1 and S2 — Framework at a Glance

Standard | Scope | Key Requirements | IFRS Alignment |

|---|---|---|---|

AASB S1 | Any risks and opportunities associated with sustainability. | Materiality, reporting limit, comparability, and reliability. | IFRS S1 – close to conform. |

AASB S2 | Risks and opportunities related to climate (compulsory for in-scope entities) | Governance, Strategy, Risk Management, Targets and Metrics. | Very similar to IFRS S2. |

IFRS S1 | International overall sustainability reporting. | General requirements for IFRS reporters throughout the world. | Standard of source of AASB S1. |

IFRS S2 | Global climate disclosures | Scope 1/2/3, physical and transition risk, scenario analysis. | AASB standard of the source of S2. |

03 Materiality Assessment

What Materiality Means in This Context

The only concept that supports the whole sustainability reporting framework is materiality. Its definition in AASB S1 and IFRS S1 is thoughtfully designed as a test of financial consequence to investors – not a social impact test.

- A sustainability-related issue is material when its absence, misstatement, or obscuration is likely to affect the decision-making of the primary users of general-purpose financial reporting.

- An environmental effect can or can be financially material - a seemingly small physical climate risk can be extremely material when it affects a critical supply chain or the carrying value of a material asset.

- It is measured in terms of financial impact and not the magnitude of environmental or social impact per se.

How the Materiality Assessment Process Works

The materiality test is usually conducted at the beginning of each reporting cycle as a systematic, methodical review process that relies on various inputs.

- The process involves in-house workshops, stakeholder consultation, value chain analysis, and benchmarking against sector-specific guidance.

- The outcome is a documented materiality matrix that cross-tabulates the issues identified by their potential financial implications and probability of occurrence within a given time period.

- This matrix then becomes the guiding force behind subsequent disclosures - it is a reporting tool and a strategic risk management input.

Financial Materiality vs Double Materiality

One difference that may be disappointing to practitioners is the distinction between financial materiality under IFRS standards and Australian and the broader concept of double materiality in Europe.

- Under AASB S1 and IFRS S1, the test to be applied is financial materiality - the impact of sustainability risks on the financial position and performance of the company.

- Under the European Sustainability Reporting Standards (ESRS), there is double materiality: companies are required to report both on financial impacts and on their environmental and societal impacts.

- Multinational organisations operating in Europe might need to contend with both regimes simultaneously, so it is important to be aware of both frameworks.

04 Governance Disclosures

Why Governance Disclosures Are Required

The question, which has been gaining increasing urgency among investors and regulators and is answered by the governance disclosures pillar of AASB S2, is: who in this organisation is ultimately answerable for matters of climate-related risk?

- Sustainability has been too long run by the board and the executive team, in a distinct operation, reported separately from financial performance.

- The governance disclosure requirements will help change this by forcing entities to disclose the specific bodies and individuals responsible for managing climate-related risks and opportunities.

- It is a paradigm change: climate is no longer a reputational management practice - it is a strategic governance requirement.

What AASB S2 Requires

AASB S2 establishes certain governance disclosure requirements that address how climate considerations are integrated across the board, executive team, and incentive frameworks.

- Report on the manner in which the board manages and tracks climate-related risks and opportunities, and how that management is carried out.

- Demonstrate how the role of management in evaluating and managing climate risks is embedded within the organisation's wider governance frameworks.

- Demonstrate how climate considerations are encoded in executive compensation and performance frameworks, a concrete accountability mechanism that investors and proxy advisers are scrutinising.

- Organisations that have demonstrated they have integrated climate issues into their incentive systems are better positioned to demonstrate credibility in their overall sustainability reporting.

Common Starting Points and What Needs to Change

In practice, the majority of organisations are finding that their existing governance documentation needs to be enhanced considerably to meet AASB S2. Board skills matrices without climate experts are a typical weakness that needs to be fixed.

- Risk committees without an explicit climate requirement should have formal terms of reference.

- ESG reports, which the audit committee has not audited, need to be changed not only the document but also the governance process.

- To close such loopholes, real behavioural change is needed at the board and executive levels - the most effective sustainability reporting programmes are always top-down and never assigned wholesale to the sustainability function.

05 Strategy and Climate Risks

Connecting Climate to Business Strategy

The strategy and climate risks pillar is the most direct link between sustainability reporting and the essence of a business’s value creation and preservation. AASB S2 is much more than a mere risk register entry.

- Entities should disclose how they determined climate-related risks and opportunities to their business model and value chain.

- Disclosures should include how climate considerations are incorporated into the organisation's strategic and financial planning.

- This should be an evidence-based narrative, not just a statement, of how climate is affecting the entity's actual direction of movement.

Physical and Transition Risks

AASB S2 and IFRS S2 identify two broad types of climate risks that organisations need to evaluate and report in a systematic and particular manner.

- Physical risks include acute events such as extreme weather, floods, and cyclones, as well as chronic changes such as rising temperatures, rising sea levels, and altered precipitation patterns.

- Transition risks are associated with the shift to a less carbon-intensive economy and include policy and regulatory changes (such as carbon pricing and emissions legislation), technological disruption, and market changes.

- An effective strategy and climate risk disclosure map both categorise individual assets, sources of revenue, and supply chains, and quantify potential financial impacts where data sets exist on which they can be reliably determined.

Real-World Example: From Narrative to Quantified Disclosure

One of the first to go TCFD-aligned in reporting was a European logistics company. Its initial strategy was narrative-driven and qualitative – a tale of risks without a reasonable estimate of financial effect.

- Response to investor feedback: The company did a physical risk assessment of its warehouse and distribution network.

- The evaluation found that in a 2-degree warming scenario, about 18% of its physical property was in high-flood-risk areas.

- This finding led to certain capital allocation decisions, including site upgrades and insurance restructuring, as mentioned in later annual reports.

- The moral of the story: disclosures are most beneficial when they are specific, quantified, and demonstrably related to real business decisions.

06 Scope 1, 2 and 3 Reporting

The GHG Protocol Foundation

The quantitative foundation of climate-related disclosure is greenhouse gas emissions measurement. Companies are required to disclose emissions in accordance with the Greenhouse Gas Protocol, a universally recognised standard under AASB S2 and IFRS S2.

- Scope 1: Direct greenhouse gas emissions of sources owned or controlled by the entity - combustion in company-owned boilers, vehicles, and industrial processes.

- Scope 2: Indirect emissions of electricity, steam, heat, or cooling purchased by the entity.

- Scope 1 and Scope 2 are relatively easy to measure because the data sources, such as energy bills, fuel records, and operational data, are usually available within the organisation.

Scope 3 — Complexity and Importance

The third scope is more complex than the first two scopes in terms of categories. It captures all other indirect emissions across the entity’s value chain, both upstream and downstream.

- Scope 3 includes upstream emissions from suppliers and the manufacturing of purchased goods, as well as downstream emissions from the use and disposal of sold products.

- Scope 3 emissions are larger than Scope 1 and Scope 2 combined in many entities, so they provide the fullest picture of an organisation's actual climate exposure.

- Scope 3 reporting can be challenging in practice: primary data on suppliers is not always available, and organisations often need to use estimates based on spend or industry-average emission factors.

- The 15 types of Scope 3 emissions outlined in the GHG Protocol must be mapped to the entity's business model with care; not all types of emissions will be material to all organisations.

Why Scope 3 Investment Matters

Nevertheless, despite the difficulties, investors are becoming more concerned with Scope 3 as the most informative indicator of the organisation’s actual climate exposure and transition risk.

- Investors and regulators consider scope 3 data the primary indicator of an organisation's actual climate impact across its entire value chain.

- Scope 3 reporting capability is a compliance requirement and a competitive edge for demonstrating climate credibility.

- Organisations that develop this capability early - before it becomes compulsory - will be much better placed than those who see the phase-in window as a licence to procrastinate.

07 Scenario Analysis

What Scenario Analysis Is — and Is Not

The most intellectually difficult aspect of the AASB S2 disclosure requirements is, perhaps, scenario analysis – and, of course, the most strategically useful when effectively executed.

- AASB S2 states that entities should use scenario analysis to assess the strength of their business model and strategy in various plausible future climate conditions.

- This should at least cover one scenario aligned with keeping global warming under 1.5 degrees Celsius, and another aligned with a higher warming trajectory (2.5 to 4 degrees).

- Scenario analysis is not a future-looking exercise, but a stress test of the present, under structured, plausible alternative futures.

Why It Matters for Strategy

Organisations can identify material blind spots by constructing ordered stories of how the world could appear under different climate paths and overlaying them onto the organisation’s financial exposures.

- An agribusiness that has not considered the yield implications of continuing drought is operating with a significant strategic blind spot.

- A real estate developer who has not simulated the effect of a 3-degree scenario on the insurability of coastal properties is also at risk.

- Scenario analysis outputs directly inform capital allocation decisions, strategic planning, and the targets and metrics framework.

Practical Starting Advice for First-Time Practitioners

For any professional starting scenario analysis, a systematic, progressive approach is the most viable means of generating credible outputs.

- Begin with qualitative stories, then go on to quantification - the form of the story precedes the numbers.

- Choose reputable, credible climate scenarios from the IPCC, IEA, or NGFS rather than developing proprietary scenarios.

- Start with the most significant risks found during the materiality assessment and proceed to greater depths with each reporting period.

- It is impractical and unrealistic to achieve perfection on the first try - the features of a plausible scenario analysis practice include improvement, openness about constraints, and progress over the years.

08 Targets and Metrics

The Accountability Layer of Climate Disclosure

The accountability layer of climate-related disclosure targets and metrics. They provide the answer to the question of greatest immediate concern to investors and stakeholders: what has this organisation undertaken, and how is it doing?

- Under AASB S2, the entities are required to disclose the climate-related measurements that they use to quantify and manage material climate risks and opportunities.

- Entities should also report the objectives they have set for those measures and how they have been achieved, both currently and in the past.

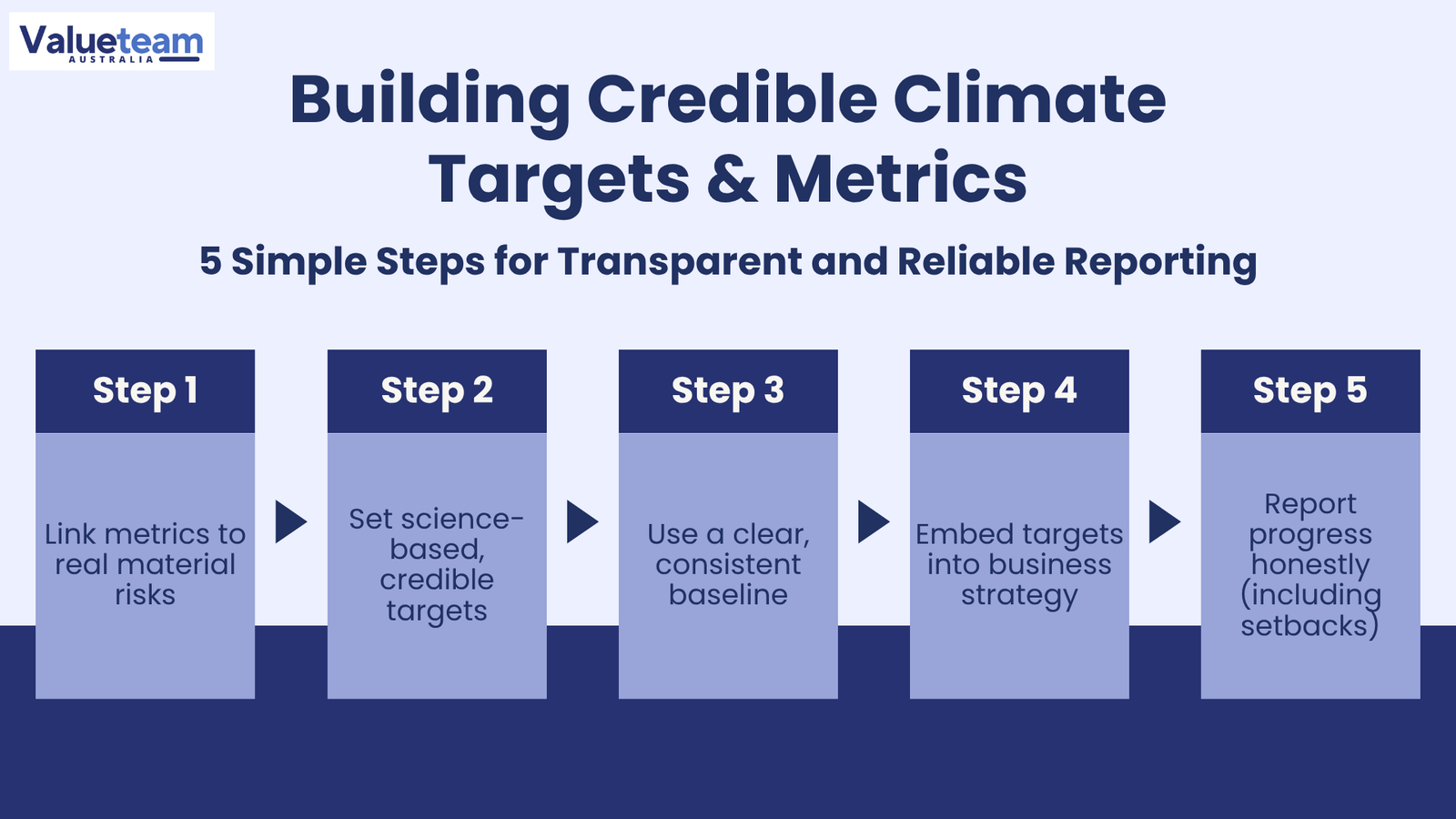

- The five steps below are best practices in the development of a credible targets and metrics framework - one that will withstand audit, investor, and regulatory scrutiny.

Step 1 — Align Metrics to Material Risks

Check the materiality evaluation and select metrics. The identified material climate risks and opportunities should be directly reflected in the metrics revealed.

- A company primarily exposed to transition risk (e.g., a carbon-based manufacturer) should track the intensity of its emissions, its exposure to the cost of carbon, and its investment in clean technologies.

- Non-material-risk metrics create noise and no signal.

- Sophisticated investors will immediately realise the disclosure gap between reported metrics and material risks, thereby weakening credibility.

Step 2 — Set Science-Based Targets

In organisations that have set objectives to minimise their emissions, AASB S2 requires disclosure on whether and how the objectives have been measured against a recognised scientific method.

- Science-Based Targets Initiative (SBTi) validation gives the targets external credibility and ensures they align with the objectives of the Paris Agreement.

- Goals that are not based on a recognised scientific framework or are formulated in a manner that allows wide latitude in scope or base year are increasingly questioned as possible greenwashing.

- SBTi validation is becoming a requirement for institutional investors and sustainability-linked financing structures as the least ambitious standard.

Step 3 — Establish a Reliable Baseline

Each target requires a baseline. In the case of emissions targets, it implies a well-defined base year, a recorded emissions inventory, and a uniform methodology in all subsequent periods.

- Changing the base year or methodology without making historical data transparent and recalculating it is one of the most common practices that erode credibility.

- Stability and consistency over time are even more important than the target's ambition.

- The minimum documentation should be stringent enough to enable external assurance - not internal reporting.

Step 4 — Integrate Targets into Business Planning

Aspirations and not commitments. The targets contained in the sustainability report are not linked to capital allocation, procurement decisions or operational planning.

- The most plausible organisations show that climate objectives and measures are incorporated into business plans, budgeting plans, and executive compensation plans.

- Auditors are also paying closer attention to how sustainability disclosures align with financial statements, especially when decarbonisation commitments may affect asset lives, impairment testing, or capital expenditure planning.

- Integration will make targets more of a management tool rather than a reporting exercise.

Step 5 — Report Progress Transparently, Including Setbacks

The performance against targets and metrics is not a disclosure requirement alone; it is the practice of accountability and the process of gaining credibility.

- It is easy to lose investor confidence in organisations that report only when they are doing well and downplay the reality of failure to meet targets.

- Advanced stakeholders need an honest explanation of what went wrong, the corrective actions implemented, and whether the deadline should be changed.

- Honesty about failures, along with an honest remediation plan, is far more helpful than performative optimism.

09 Data Collection and Management

Why Data Is the Hardest Part

Ask any professional who has prepared the first sustainability report of their organisation what the most difficult part of it was, and the answer is nearly always the same: data. Narrative does not comply with the disclosures required under AASB S2 and IFRS S2.

- They demand definite, measurable information about emissions, energy consumption, financial impacts on climate and goal performance.

- One of the biggest operational challenges of the shift to mandatory reporting is creating a data-collection and management infrastructure that ensures this information is audit-quality and reliable.

- The fact that sustainability data is usually distributed across different systems, functions, and geographies adds to this challenge.

Mapping the Data Landscape

The key initial step in developing a strong data collection and management framework is mapping the data landscape. This gap analysis typically identifies readiness categories.

- Energy consumption data may be in facilities management software; fleet emission data may be in a logistics system; supplier emission data may not be in any structured form.

- Gap analysis identifies information that exists but is not yet merged, information that must be gathered through new processes, and information that must be estimated using proxies or industry benchmarks.

- Every category requires a different response, and the general picture defines the extent of infrastructure investment required before the first compliant report can be generated.

Technology and the Role of Purpose-Built Platforms

Technology is becoming a very central part of the sustainability data collection and management. Dedicated platforms are emerging as the standard of operation for organisations with serious reporting requirements.

- Special ESG data management systems - like Workiva, Sphera, and Persefoni - provide centralised data collection, calculation, audit trail and reporting features that are hard to duplicate in spreadsheets.

- The payback period of purpose-built tooling is typically short due to reduced manual labour, higher-quality data, and the ability to demonstrate to auditors that controls are in place.

- The internal controls dimension is particularly relevant when the assurance requirements are mandatory: any data that cannot be traced to a verifiable source with documented controls will not pass the independent assurance test.

Table 2: Sustainability Data — Sources, Challenges, and Solutions

Data Type | Typical Source | Common Challenge | Practical Solution |

|---|---|---|---|

Scope 1 — Direct emissions | Records of fuel purchases and logbooks. | Several locations, incompatible designs. | Centralised energy control system; auto meter reading. |

Scope 2 — Electricity | Energy agreements, utility bills. | Market-based vs. location-based. | Organised the request of energy providers; RECs documentation. |

Scope 3 — Value chain | Supplier information, spend database, logistics. | Poor supplier response; uncertainty in estimations. | Supplier engagement program; spend-based proxy, disclosure of methodology. |

Physical risk exposure | Asset registers, GIS records, insurance records. | Incompetence of the geospatial capability in-house. | Third parties provide surveillance tools of climate risk (e.g. ClimateWise, Jupiter Intel). |

Transition risk/opportunity | Carbon pricing models, strategic plans, R&D pipeline. | Subjectivity; discrepancy between business units. | Formalised scenario exercises; Library of central assumptions. |

Table 3: Data Collection and Management — Process Flow

Phase | Key Activities | Responsible Party | Output |

|---|---|---|---|

1. Scope Definition | Confirm reporting boundary, materiality results, and standards to apply. | Sustainability Lead + Finance | Reporting scope memo |

2. Data Mapping | Find all the needed data points; map to existing systems and owners. | Sustainability Team + IT | Inventory and gap analysis of data. |

3. Collection Design | Construct data templates; determine calculation approaches. | Sustainability Analyst | Methodology and templates are used. |

4. Data Gathering | Gather information on internal and subsidiary teams, as well as major suppliers. | Owners of the data in the business units. | Raw data submissions |

5. Validation and QA | Check completeness, reasonableness; clear up anomalies. | Sustainability Lead + Finance | Validated data; query log. |

6. Calculation and Aggregation | Use GHG Protocol calculations; add up between entities and scopes. | Sustainability Analyst | Emissions inventory; metrics dashboard. |

7. Disclosure Drafting | Prepare narrative and quantitative disclosures that align with the AASB S2 pillars. | Sustainability Lead + Comms | Draft sustainability disclosures |

8. Internal Review and Sign-off | CFO, Board Audit/Risk Committee and legal reviews. | CFO / Board | Disclosures that have been approved and are ready to be lodged. |

10 ASIC Lodgement and Assurance

The Final Mile: From Internal Document to Regulated Disclosure

ASIC lodgement and assurance is the last step in the sustainability reporting process – when disclosures are no longer internal documents but controlled statements to the public.

- As part of their annual report, in-scope entities are required to prepare a sustainability report as a compulsory annual report under the Australian compulsory climate reporting regime.

- This report should be filed with ASIC under the Corporations Act - it is not a supplementary publication or a marketing document.

- It is a legally required disclosure on the same level as the financial statements, and directors are personally liable for its accuracy and completeness.

Assurance Requirements and Their Trajectory

The assurance requirements introduce a new dimension for many organisations, and requirements are likely to increase over time to a higher standard.

- In the initial years of compulsory reporting, limited assurance, which gives moderate confidence that disclosures are free of material misstatement, is needed.

- Over time, reasonable assurance (the higher standard used in financial statements) will be the standard, at least for Scope 1 and Scope 2 emissions and the most material disclosures.

- There are long-term implications for this path of data collection, data management infrastructure design, and control.

Career Opportunity at the Intersection

The ASIC lodgement and assurance procedure is changing the competitive environment of the professional services market, providing real career prospects to early-investing practitioners.

- The ability to assure sustainability is emerging as a major investment for audit firms, the Big Four and specialist sustainability consultancies.

- Sustainability reporting professionals who are aware of sustainability reporting standards and the process of assurance are in demand - and this set of skills is not yet well supplied.

- Early investment in learning about the ASIC lodgement and assurance processes is not only professionally helpful but also a smart career move.

11 Challenges and Lessons Learned

Challenge 1 — The Gap Between Aspiration and Infrastructure

The most generalised problem is the disjuncture between infrastructure and desire. Many organisations have presented plausible climate ambitions without establishing the data infrastructure to report on them.

- Net-zero, science-based emissions-reduction, and supply-chain decarbonisation pledges have been made without data collection and management systems.

- The lack of a connection between the commitment story and quantifiable, verifiable facts becomes particularly acute when the first compulsory sustainability report is due.

- Lesson: It is a simple lesson that is easily forgotten: Have the reporting infrastructure in place before the promise to the people. Each target should have an accountability mechanism, a collection process and a measurement methodology.

Challenge 2 — Organisational Ownership

Sustainability reporting is an awkward fit between various functions, such as finance, legal, risk, operations, communications, and investor relations. When ownership is not well shared, it is likely to be left at the crossroads.

- The most successful programs possess an explicit executive sponsorship, a specific reporting position with explicit authority, and are formally part of the CFO's responsibilities.

- The CFO's involvement is particularly crucial because AASB S2 disclosures will be part of the statutory financial report.

- The discipline and audit-readiness that finance has brought to financial reporting should now be extended to sustainability disclosure; the two should not be handled independently.

Challenge 3 — The Need for Authentic Engagement

Sustainability reporting done well is not a compliance exercise conducted in a vacuum, but a process of fact-based research into the risks and opportunities of the business in relation to climate.

- Building credible reporting capacity is most effectively done by the organisations that engage in materiality assessment and scenario analysis to have substantive strategic discussions.

- These involve conversations about the most exposed assets to physical risk, the business lines most affected by transition risk, and the low-carbon opportunities worth pursuing.

- When reporting is an aftereffect of a genuine strategic process, not a document written under deadline pressure, the quality difference will be obvious, even to advanced investors and auditors.

12 Conclusion and Actionable Insights

Key Takeaways

The adoption of mandatory sustainability reporting in Australia is a structural shift in the requirements and expectations on companies, boards and their advisers.

- AASB S2 climate-related disclosures apply to in-scope entities and are consistent with IFRS S2 - this is not a trend that will turn back.

- The regulatory trend, investor demands and international standards are all shifting towards tougher, more similar, and more confident sustainability reporting each year.

- Professionals who invest in the present to become truly skilled in this framework will be well-positioned to secure jobs that did not exist five years ago.

Five Actionable Steps for Practitioners

The steps that follow provide a viable point of departure for professional development in sustainability reporting under AASB S2.

- Step 1: Read the AASB S2 standard, not just summaries. It is structured into four TCFD pillars: governance disclosures, strategy and climate risks, risk management, and targets and metrics.

- Step 2- Develop substantive knowledge of the GHG Protocol and its three scopes- Scope 1, Scope 2, and Scope 3- the mainstay of emissions accounting of any climate disclosure.

- Step 3 — Exposure to real materiality testing. One of the most marketable skills in the field is the capacity to recognise financially material climate risks and to document that distinction rigorously.

- Step 4 - Interact with publicly available IPCC, IEA, and NGFS scenario analysis frameworks to learn about the spectrum of plausible future climate pathways and how they are implemented in practice.

- Step 5 — Research how early reporters are moving towards ASIC lodgement and assurance. Look at their published sustainability reports, evaluate the quality of their disclosures and see what makes organisations that have actually invested in capability stand out.

It is not the organisations with the most impressive targets that will be in the lead on sustainability reporting, but those with the most rigorous data, the most truthful disclosures, and the most comprehensive incorporation of climate risk into strategic decision-making. |

At best, sustainability reporting is an area where an organisation is brought face-to-face with the world it operates in. Rigour, honesty and long-term thinking are the foundations of professional practice, which are established during a career.