Table of Content

1. Introduction to Prepare a Sustainability Report in Australia

Sustainability Reporting Australia has become a compliance task, rather than a “best-practice” voluntary exercise. As mandatory reporting for climate-related issues under AASB S1 and S2 comes into play for large companies, and expectations from stakeholders increase for companies of all sizes, preparing a Corporate Sustainability Report is one of the most critical annual activities for a business.

The skill for those new to the field is not a lack of frameworks to follow, but understanding the multiple standards, which the ESG Disclosure Framework is relevant to your business, and how to set up a process that delivers data-driven, defensible disclosures that can be verified. When well prepared, a sustainability report isn’t just a regulatory compliance exercise, but a key communication strategy to earn the trust of investors, customers and regulators.

This how-to guide outlines the process, the relevant frameworks, how Data Collection ESG works, and what makes reports that stand the test of time different from those that don’t. This guide is based on the way many experienced practitioners work, whether you are producing your organisation’s first report or enhancing an established process.

2. Understanding the Frameworks Before You Start

Why framework selection matters

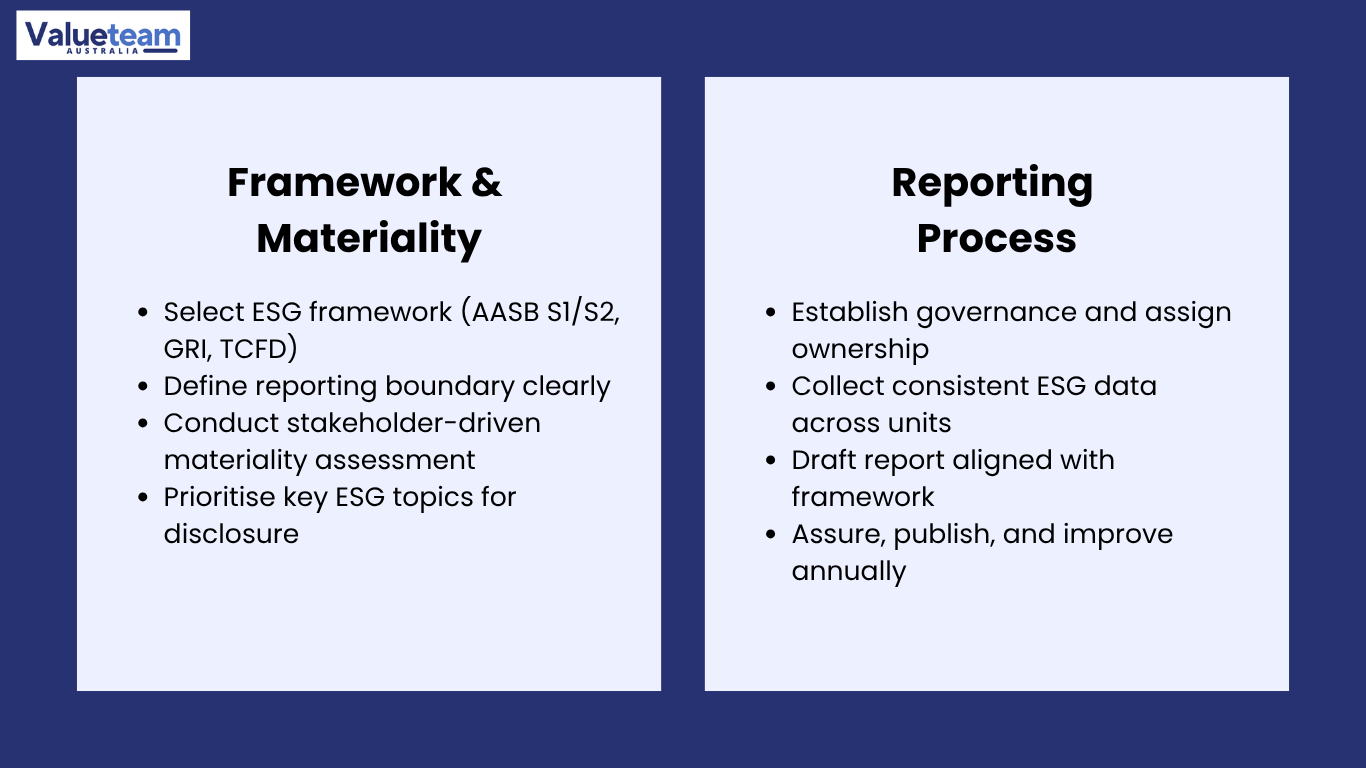

The reporting team must decide on which ESG Disclosure Framework the report will be based on before reporting any data. In Australia, the major frameworks are AASB S1 / S2 (required for large entities), the GRI Standards Australia (the most comprehensive and widely used voluntary framework worldwide) and the TCFD recommendations for climate-related reporting. Many will align to more than one.

- GRI Standards Australia – the most comprehensive voluntary framework; covers economic, environmental and social performance; recognised by institutional investors and customers.

- AASB S1/S2 – required for entities above Group 1, 2 or 3 thresholds; climate-centred; includes scenario analysis and Scope 1, 2 and 3 emissions reporting.

- TCFD – the climate-focused reporting framework that serves as the basis for both AASB S2 and many investor expectations; includes governance, strategy, risk management, and metrics.

- UN SDGs – often used to provide context of a business’s contribution to sustainability; not a reporting framework, but a useful narrative for businesses.

Choosing the right standard for your organisation

If you’re mandatory, you have no choice – it’s AASB S1 and S2. For others, the decision should be guided by your target audience: institutional investors like TCFD; customers and procurement teams often want GRI; and boards looking to get ahead of mandatory requirements in the next Group should adopt AASB S2. Choosing a framework that you will use year in and year out – and not the one that offers the best first-time view – is a critical Reporting Best Practices choice.

3. Materiality Assessment and Report Scoping

What does materiality mean in practice

A Materiality Assessment identifies which sustainability issues should be reported in the report. Under GRI Standards Australia, double materiality means looking at the financial materiality – the impact of ESG issues on the organisation – and the environmental and social materiality – the impact of the organisation on the environment and society. Under AASB S1, it is financial materiality – what matters to investors considering the entity. Getting materiality right drives the report: it defines what you report on, what you disclose and what you set targets for.

- Conduct stakeholder surveys (including employees, investors, customers and community organisations) to determine ESG topics of greatest interest.

- Evaluate each topic against two criteria: importance of the business’s impact on the topic; importance of the topic’s impact on the business’s bottom line.

- Plot the results in a materiality matrix; the topics in the top-right quadrant are the report’s focus.

Defining the report boundary

The report boundary defines which entities, locations and activities are included in the Corporate Sustainability Report. It should be the same as the financial reporting boundary unless there is a justification for it. The reporting boundary impacts which Sustainability Metrics are reported and should be clearly stated to ensure that readers understand the information. A common pitfall: omitting subsidiaries or joint ventures that have a major environmental or social footprint because they are difficult to manage.

Materiality Approach | Required Under | Focus | Stakeholder Lens |

Financial Materiality | AASB S1, AASB S2, TCFD | Risks and opportunities relevant to investors and financial performance | Investors, lenders, regulators |

Double Materiality | GRI Standards Australia, EU CSRD | Both the financial impact on the business AND the business’s impact on society and the environment | Investors, customers, employees, NGOs, and the community |

Impact Materiality only | Emerging voluntary frameworks | How the organisation affects people and planet, regardless of financial significance | Community, civil society, employees |

4. Five Steps to Preparing Your Sustainability Report

After the framework and the scope of materiality are set, the reporting process has a universal five-step framework. No step can be missed without problems arising later – usually during data review, assurance or stakeholder review.

Step | What It Involves | Key Output | Common Pitfall |

1. Establish governance and assign ownership | Designate a cross-functional reporting team (sustainability, finance, legal, HR, operations); assign executive sponsor; define the board’s review and sign-off role for ESG Report Preparation | Governance charter, responsibilities matrix, and board approval process documented | Sustainability team works in isolation without finance or legal input; board sees the report for the first time at sign-off without having been involved in content decisions |

2. Conduct Materiality Assessment | Engage stakeholders via surveys, interviews, and workshops; map material topics against financial and impact materiality axes; validate with board and senior management | Materiality matrix; prioritised topic list; documented stakeholder engagement process | Materiality is copied from prior year or peer benchmark without genuine stakeholder engagement; topics are rated as material without connecting them to specific disclosure content |

3. Data Collection ESG | Assign data owners for each material topic; establish data collection templates aligned to the chosen framework; gather Sustainability Metrics for the current year and prior year comparatives; verify data quality | Populated data set with source documentation; prior-year comparatives; variance explanations for significant changes | Data is collected late and without source documentation; inconsistent methodologies across business units; no prior-year baseline, making trend analysis impossible |

4. Draft and review the Corporate Sustainability Report | Write narrative sections contextualising the data; draft performance disclosures against framework requirements; conduct internal review for accuracy, consistency, and alignment with Reporting Best Practices | Complete draft report with all GRI, AASB, or TCFD required disclosures; internal sign-off | Narrative overstates performance relative to data; cherry-picking favourable metrics while omitting underperforming areas; legal review of claims not conducted before publication |

5. Assurance, publication, and continuous improvement | Engage an independent assurance provider for limited or reasonable assurance on selected metrics; finalise report; publish with clear methodology notes; debrief and identify improvements for next cycle | Assured report; published Corporate Sustainability Report; process improvement plan for next year | Assurance is treated as a rubber stamp rather than a quality check; findings from the assurance process are not used to improve data collection systems for the following year |

The greatest practical challenge for most reports occurs at step 3: Data Collection ESG. Organisations often don’t appreciate the time and system resources needed to gather robust, repeatable Sustainability Metrics across business units and geographical locations. Typical issues include non-financial data being recorded in spreadsheets rather than in a managed system; a lack of ownership for non-financial data categories; and different calculation methods across sites. Establishing a data collection process that is fit for purpose – preferably integrated with financial reporting systems – is the most important system improvement most organisations can make to their Sustainability Reporting Australia process.

5. Data Collection, Environmental Metrics, and Reporting Quality

Building a robust data collection process

Data Collection ESG for a sustainability report is not a once-a-year rush. The best reports are produced by organisations that collect data for Sustainability Metrics every month or quarterly – they treat ESG data the same as their financial data. This involves appointing data owners, creating data collection templates, setting internal deadlines and conducting a review of the data before it’s published in the report.

- Greenhouse gas emissions (Scope 1, 2 and if material, Scope 3) calculated with NGA emission factors for Australia operations.

- Energy usage by type (electricity, gas, fuel) and intensity measures (per FTE, per sqm or per unit of production).

- Water use and waste (by disposal type) – relevant for operations with material Environmental Impact Reporting obligations.

- Social data: employee demographics, gender pay gap, safety (days lost to injury), training hours and, if relevant, modern slavery due diligence.

Environmental Impact Reporting specifics

For Environmental Impact Reporting, the quality of the reporting is only as good as the measurements. Greenhouse gas emissions data should mention the emission factors used; water data should note whether it is consumption or withdrawal; and waste data should specify the landfill, recycling, and other disposal methods used. Reports that present a figure without a methodology note do not meet Reporting Best Practices and may be challenged in an assurance or stakeholder review.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Framework & Scope | Data Collection ESG | Draft & Internal Review | Assurance & Publication |

Select ESG Disclosure Framework; confirm materiality topics; define reporting boundary; assign governance and data owners for Sustainability Reporting Australia | Collect Sustainability Metrics by topic and business unit; apply consistent methodologies; gather Scope 1, 2, and 3 emissions data; compile prior-year comparatives for Environmental Impact Reporting | Write narrative and performance disclosures; align to GRI Standards Australia or AASB S2 requirements; conduct cross-functional review for accuracy; legal review of material claims | Engage independent assurance provider; respond to findings; finalise Corporate Sustainability Report; publish with methodology notes; plan data quality improvements for next cycle |

6. Real Cases, Challenges, and Lessons Learned

Case 1: When materiality is misapplied

A mid-sized logistics company developed its first Corporate Sustainability Report from a materiality process that included only internal stakeholders, senior management and the board. The report excluded fleet emissions and fuel consumption, which was the company’s largest Environmental Impact Reporting category, while emphasising governance and human capital data. When a key customer asked for a copy of the report as part of a due diligence procurement exercise, the gap was quickly detected. The customer was concerned to see a logistics company issue a sustainability report without reporting its main environmental impact. The company had to issue an additional disclosure before the contract was signed – this could have been avoided if the Materiality Assessment had involved external stakeholders, especially customers.

Case 2: Data quality driving credibility

A professional services business in its third year of Sustainability Reporting Australia partnered with an ESG data platform, which linked to its financial reporting platform. The platform automatically downloaded building electricity use from the building management system and travel data from the expense management system, and calculated emissions using the latest NGA emission factors. The assurance provider was able to easily trace the data from meter readings to the reported Sustainability Metrics during its limited assurance. The assurance took half the time as last year and found no material issues. The company’s Corporate Sustainability Report received the top data quality score in a peer benchmarking exercise among similarly sized firms in its industry.

Common challenges and how to address them

Challenge | Why It Occurs | Practical Resolution |

Inconsistent data across business units | Different sites use different methodologies for measuring the same metric; no central coordination of Data Collection ESG | Establish a single data collection template with a prescribed methodology for each metric; appoint site-level data owners with training on the template |

Narrative overstates performance | Marketing or communications teams write sections without reference to the underlying data; no data verification before publication | Cross-reference every quantitative claim in the narrative to a specific data point; require the finance or sustainability team to sign off on all claims before publication |

No prior-year comparatives | First-year report has no baseline; subsequent years show inconsistent boundaries or methodology changes | Establish a base year in year one; document methodology clearly; disclose and explain any restatements in subsequent reports — this is a requirement under GRI Standards Australia |

Scope 3 gaps | Supply Chain Emissions are excluded because supplier data is unavailable | Disclose which Scope 3 categories are included and excluded with documented rationale; use spend-based proxies with stated uncertainty ranges as a starting point; build a supplier engagement programme over time |

7. Conclusion: Actionable Guidance for Owners and Advisors

To produce a credible Corporate Sustainability Report in Australia, it is important to align with the right framework, undertake a genuine Materiality Assessment, implement robust ESG Data Collection processes, and follow Reporting Best Practices that favour substance over style. For those organisations that succeed in this endeavour, sustainability reporting is not a yearly exercise in compliance, but a continuous process of data collection and governance, one that improves each year as processes and systems are refined and ownership is enhanced.

For practitioners, there are three key steps. First, build data infrastructure in the beginning – the data collected into Sustainability Metrics is the foundation for all decisions. Second, work with stakeholders to identify the issues you won’t get right in the Materiality Assessment – they will see the things that you don’t. Third, use the assurance process as an opportunity to improve the quality of the report, not to add cost and complexity – the insights from the assurance process are the most specific guidance for improving the next year’s Sustainability Reporting Australia process.

Frequently Asked Questions

Q1. What is a sustainability report?

A sustainability report communicates an organisation’s environmental, social, and governance (ESG) performance, sustainability initiatives, and long-term business impacts.

Q2. Why are sustainability reports important?

They improve transparency, strengthen stakeholder confidence, demonstrate corporate responsibility, and support compliance with emerging reporting requirements.

Q3. What information is typically included in a sustainability report?

Reports commonly include environmental performance, emissions data, governance practices, social initiatives, risk management, and sustainability goals.

Q4. Who should prepare sustainability reports?

Listed companies, large organisations, and businesses with ESG reporting obligations or sustainability commitments should prepare sustainability reports.

Q5. How do sustainability reports benefit businesses?

They enhance corporate reputation, attract investors, improve stakeholder engagement, and demonstrate commitment to sustainable business practices.

1 thought on “How to Prepare a Sustainability Report in Australia: Step-by-Step Guide”