Table of Content

1. Introduction: Startup Valuation in Australia

Startup valuation is one of the most challenging tasks in finance. Where a profitable SME with three years of audited accounts or a listed company with a market price is easily valued, a startup has little or no revenue, no operating history, and a value proposition that is almost entirely dependent on its future potential. Yet investors are making these kinds of judgements every week in the Australian startup ecosystem – and while their valuations are not always 100% accurate, they are systematic, predictable and teachable. What is now known about Startup Valuation Australia is not simply a theoretical exercise for potential founders and business owners: it is a practical skill for those who provide advice, investment capital, or financing to others, in particular, the burgeoning cohort of early-stage investors.

Over the last ten years, the Australian startup ecosystem has evolved. Local venture capital activity has intensified, government initiatives have helped expand early-stage financing, and a generation of successful founders has created a virtuous circle of mentoring, syndication, and market intelligence that enhances the success of subsequent early-stage businesses. In this environment, Startup Valuation Australia is no longer simply a question of hammering out a price between a founder and an individual angel investor. It is now a process of negotiating a term sheet, syndicated investment rounds, and investors who draw on robust approaches from their local and global deal flows.

This article is intended for founders gearing up for their first institutional funding round, early-career professionals interested in investors’ perspectives, and those looking to develop their knowledge in Early-Stage Investment advisory roles. It presents the key valuation approaches investors use at the early stage, the five most critical factors influencing valuation in the context of Early-Stage Investments, the types of issues that arise, and the lessons learned from actual investment rounds.

2. Why Early-Stage Valuation Is Fundamentally Different

The traditional methods of valuing businesses – multiples of earnings before interest, taxes, depreciation and amortisation (EBITDA), discounted cash flow (DCF) analysis, asset-based valuations – are designed to value companies with a financial track record. When applied to a pre-revenue or early-revenue startup, such approaches either yield meaningless results or require assumptions so uncertain that the value cannot be justified. A discounted cash flow (DCF) model for a pre-revenue SaaS business isn’t technically incorrect. Still, the result is nearly entirely dependent on the terminal value, which in turn is driven by untestable projections. Hence, the Venture Capital Valuation methodology takes an outcome-based approach, uses market-based benchmarking, and emphasises a clear understanding of Risk vs. Return Analysis rather than simply applying a multiplier to earnings.

The fundamental value that investors acquire in early-stage companies is the right to participate in an event that, if it occurs, will yield a return sufficient to compensate them for the risk of many investments that will fail. This is the basis of the Venture Capital Valuation methodology: the success rate for startups is low, so the returns from successful investments need to be commensurately large. For an investor who invests her capital at a Pre-Money Valuation of $5 million in a startup that fails, she loses 100% of her capital. To have a balanced portfolio, they need successful investments that return 10x, 20x, or more. This is not greed – it is the maths of early-stage investing, and having a clear understanding of it enables founders to have a more constructive, realistic discussion with prospective investors about price.

There are particular realities of the Australian market that affect Startup Valuation Australia, which differ from, say, the Silicon Valley scale-up benchmark many founders use. The UK market is smaller, exit opportunities are narrower, the late-stage follow-on market is shallower, and the lack of large IPO outcomes in the UK means that M&A (mergers and acquisitions) – rather than IPOs – is the preferred exit path for funded startups. These factors contribute to Australian Pre-Money Valuation benchmarks typically being lower than those for US startups at the same stage, reflecting both the size of the market and the cost of capital for Australian founders looking to build their companies globally from Australia.

3. The Methods Investors Use to Arrive at a Number

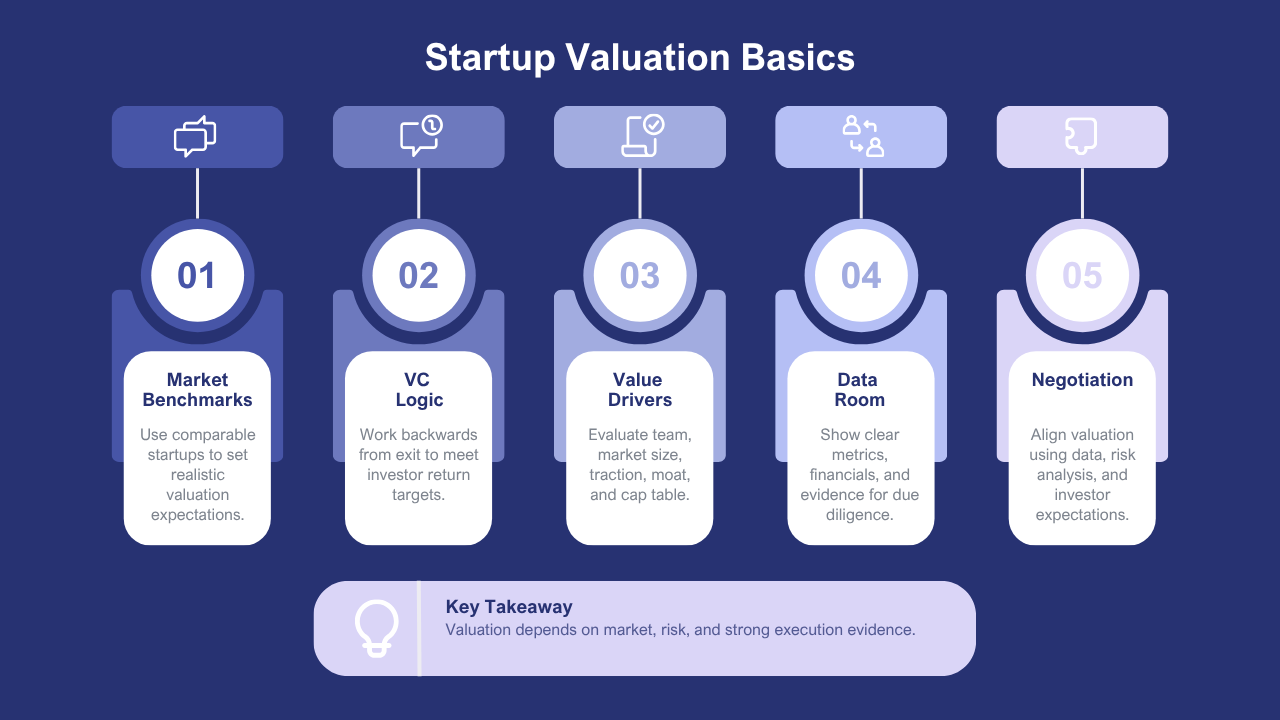

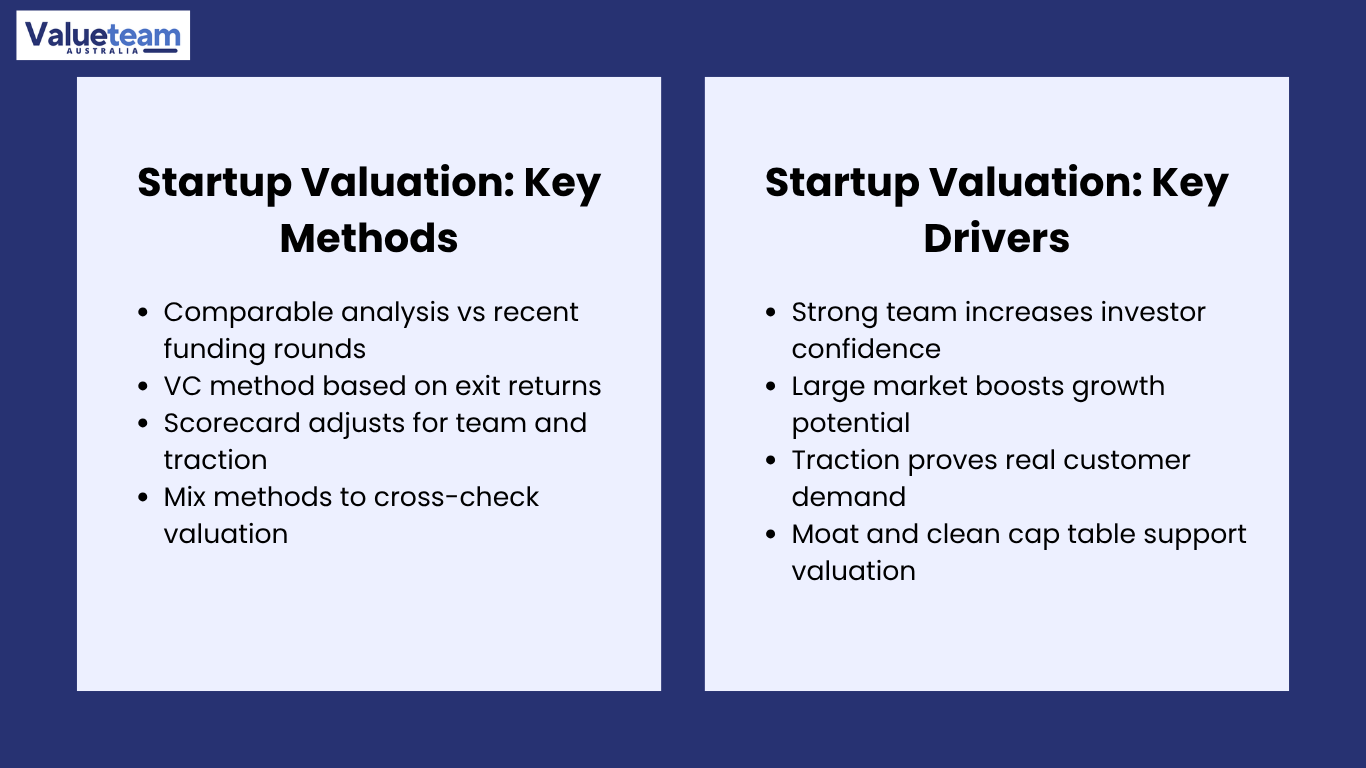

Seasoned early-stage investors do not rely on one particular method for Pre-Money Valuation. They apply multiple frameworks to determine what’s fair for a particular company and stage of development. The most popular methods in the Australian Venture Capital Valuation context are outlined in the table below.

Valuation Method | How It Works | Best Applied When | Key Limitation |

Benchmark the target’s stage, metrics, and sector against recent comparable funding rounds to establish a market-referenced valuation range | Sufficient comparable transaction data exists in the same sector and geography, for angels and early VC rounds | Australian private round data is limited; US benchmarks may overstate domestic market pricing | |

Venture Capital Method | Work backwards from a target exit value and required return multiple; determine the implied Pre-Money Valuation that the investor can accept, given dilution and timeline | Institutional VC rounds where the investor has a defined fund return requirement and exit assumption | Output is highly sensitive to exit multiple and timeline assumptions; it encourages circular negotiation |

Scorecard / Berkus Method | Assess Growth Potential Assessment factors (team, market, product, traction, IP) relative to a baseline; adjust a reference valuation up or down accordingly | Pre-revenue or seed-stage companies, where financial metrics are insufficient for quantitative methods | Subjective weighting of a factor produces different outputs depending on which investor applies it |

Innovation Valuation (Real Options) | Treat the startup as a bundle of real options on future outcomes; value each option using probability-weighted scenario analysis. | Deep tech, biotech, and platform businesses with distinct development milestones and binary outcomes | Technically complex; rarely applied in practice outside specialised deep tech and life sciences investors. |

Most early-stage investors use a mix of Comparable Startup Analysis and the Venture Capital Method as their primary framework, and a scorecard methodology to sanity-test the qualitative aspects of their analysis. The Comparable Startup Analysis provides a market anchor: what comparable startups are raising, for what stakes, and at what point in their development? The Venture Capital Method provides an investor economics anchor – given our target return and the expected exit date, what is the highest Pre-Money Valuation we would be prepared to pay and still achieve our portfolio performance targets? Where the two anchors agree, a deal can be closed. Where they don’t, either investors will have to change their return expectations or the founder will have to change his/her Pre-Money Valuation expectations.

4. Five Key Factors That Drive Startup Valuation

Regardless of the methods investors use or the discussions founders have with prospective investors, there are five key factors in Pre-Money Valuation for an Early-Stage Investment. Knowing what they are and how to demonstrate that they are as strong as possible is the fastest way to achieve a valuation that meets the founder’s goals and the investor’s demands.

|

Valuation Driver |

Why Investors Weight It Heavily |

How Founders Can Strengthen It |

|

Team quality and depth |

The founding team is the single most important predictor of early-stage outcome; investors are effectively backing people before they are backing a product or market |

Demonstrate relevant domain expertise, prior startup experience, and the ability to attract and retain strong talent; address obvious capability gaps through advisors or early hires |

|

Growth Potential Assessment: market size and trajectory |

A large, growing market provides the headroom for the returns investors require; a small or declining market caps upside regardless of product quality |

Use credible, independently sourced market size data; distinguish between addressable market and serviceable market; show why the window of opportunity is open now |

|

Startup Funding Metrics: traction and revenue quality |

Demonstrated market pull — paying customers, revenue growth, retention rates, NPS — reduces investor risk more than any financial model can; evidence beats assertion |

Prioritise quantifiable traction metrics over anecdotal customer feedback; recurring revenue and strong retention rates are weighted more highly than one-off or project revenue |

|

Competitive Moat and Innovation Valuation |

Investors price the durability of competitive advantage; a business that a well-funded incumbent can easily replicate commands a lower premium than one with genuine IP, network effects, or switching costs |

Articulate the specific sources of defensibility — proprietary data, regulatory moats, switching costs, network effects — and explain why they compound over time rather than eroding |

|

Founder Equity Dilution structure and cap table cleanliness |

A messy cap table — excessive dilution from prior rounds, poorly structured option pools, or informal shareholder arrangements — creates friction in due diligence and can deter institutional investors |

Maintain a clean, well-documented cap table from day one; engage a startup-specialist lawyer for early structuring decisions; model dilution across funding scenarios before entering negotiations |

The fifth factor – Founder Equity Dilution and cap table structure – is often underappreciated by first-time founders and overplayed in its importance to early-stage fundraising. A well-organised cap table alone does not lead to a higher valuation. Still, a messy cap table can create enough friction to limit the number of potential investors, increase the time required to complete due diligence, or create the risk of renegotiations at deal closing. The key takeaway for founders in the early stages is to spend money on legal structure – shares’ agreements, vesting and ESOP documents – up front, rather than afterwards. It’s usually cheaper to do it right at the beginning than to fix things in the middle of a fundraiser.

5. Process, Challenges, and What the Market Teaches You

It’s helpful to understand how the Venture Capital Valuation process works. Knowing how it works – and where the potential misalignment can occur – helps create better results for founders and their advisors. The four phases below illustrate how an Early-Stage Investment round,from first contact with investors to signing the term sheet and closing, plays out and where the real-world problems lie.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Preparation & Positioning | Investor Outreach & Pitch | Due Diligence | Term Sheet & Close |

Establish Pre-Money Valuation range using Comparable Startup Analysis; assemble Startup Funding Metrics deck; clean cap table; define use of funds and 18-month milestone roadmap | Present Growth Potential Assessment, team, and traction to target investors; manage parallel processes to create competitive tension; respond to initial due diligence information requests | Support investor Risk vs Return Analysis; provide financials, customer evidence, IP documentation, and cap table; address Founder Equity Dilution structure and legal due diligence requirements | Negotiate Pre-Money Valuation, option pool, liquidation preferences, and board composition; manage Founder Equity Dilution against investment objectives; execute subscription documents |

It’s in Phase 1 that founders often fail to invest enough time. Getting into discussions with investors without a firm grasp of a Pre-Money Valuation reference point – ideally benchmarked against the latest Comparable Startup Analysis data for comparable Australian and international rounds – leaves founders at a disadvantage from the start. Investors who work with founders who lack a clear idea of their pre-money valuation typically either dictate deal terms or, in a more dire case, infer the founders’ sophistication. Addressing the question, “What have similar companies raised at and why is our company deserving of a certain place in that spectrum?” in the two to three weeks before starting outreach is time well spent.

Phase 3 – due diligence – is always described as the most difficult and emotionally taxing time for first-time founders. Investors conducting Risk vs. Return Analysis will question the business on customer churn, market share, unit economics, and the assumptions underlying the financial model. These questions are not hostile – they are professional – but founders who perceive them as critical rather than evaluative are likely to react defensively and can create a breakdown in the relationship when it is critical to maintain rapport. Having answers to the most common questions and data to back them is a high-ROI investment founders should make in the lead-up to due diligence. Mentors who encourage founders to identify and explore their risks before investors raise them are more successful than those who merely help founders put their best foot forward.

The Risk vs Return Analysis that investors use in Phase 3 is really about understanding the probability distribution of the venture’s outcomes – not just the scenario that the founder puts forward. Investors want to know the credible downside scenarios as well as the upside, and founders who talk with them about this analysis (investors will want to know what the key risks are, and what your plans are to manage them) are more likely to build trust with investors than those who simply present the upside case. The most fundable founders are not those who “ignore” the risks; they are those who recognise them and have a strategy for dealing with them.

6. Real Cases and What They Teach Founders and Advisors

A most telling feature of Startup Valuation Australia is the mismatch between founders’ valuation expectations based on US precedents and the Australian market. A B2B SaaS business with annual recurring revenue of $400,000 and 85 per cent gross margins launched a seed round process with a Pre-Money Valuation expectation of $8 million, pointing to similar-sized rounds in the US. Local institutional investors showed interest but could not agree on the same valuation; instead, they offered term sheets between $4 million and $5 million, based on the local market, fund size, and a lower exit multiple assumption. After six weeks of unsuccessful negotiations, the founders adjusted expectations. The round closed at $5.5m Pre-Money Valuation, with a solid syndicate of investors. The takeaway: Comparable Startup Analysis needs to be benchmarked to the market you are raising in, not the best-case scenario overseas.

Another example highlights the importance of being ready for the Startup Funding Metrics presentation. A deep-tech company with a proprietary materials science platform had good Innovation Valuation metrics – three issued patents, a university research collaboration agreement, and a clear path to multiple applications in several industries – but little business revenue. The founders engaged an advisor to develop a milestone-driven Venture Capital Valuation model that linked the company’s growth plan to a series of value inflection points, each with its own independent technical validation. Rather than proposing a single Pre-Money Valuation figure and having to argue with investors, the team presented a scenario model that illustrated how the valuation would change as milestones were reached. This type of Innovation Valuation approach, rather than the traditional profit-based valuation, resonated with deep-tech investors and brought about a term sheet at a Pre-Money Valuation higher than anticipated. It was the valuation narrative that won the day.

7. Conclusion: Actionable Insights for Founders and Advisors

A prime example of the consequences of poor M&A Valuation Timing is a professional services organisation that went to market with only a broker’s indicative report. The vendor had been told that a formal report was not needed because the business was simple. The prospective preferred buyer’s due diligence team, working with a Big Four advisory firm, conducted an earnings quality analysis and found that normalisation adjustments reduced the investable EBITDA by 22 per cent compared to the broker’s assessment. Without the vendor having a “Formal Valuation Report” prepared at market entry, they tended to accept the price adjustment. The price of a report at the start of the process (about $14,000) would have given an independent analytical basis for contesting at least some of the adjustments. The final sale price was significantly lower than what it would likely have been based on an earlier independent valuation.

Another example illustrates the benefits of early involvement in a Shareholder Disputes Valuation. The owners of a manufacturing company were unable to resolve a dispute and agreed that one owner would purchase the other’s share at fair value. The parties used independent valuers at around the same time, before a lawsuit was commenced. The two reports, prepared to a similar standard and using the same method, had estimates that differed by 12 per cent, a difference that could readily be resolved. The overall cost of the valuations was around $28,000. If litigation had been necessary, it would have certainly cost 10 times this figure and taken much longer. The moral: in dispute matters, the competency and integrity of the Independent Valuation are key factors in determining whether the matter is settled commercially or litigated, which is costly.

8. Conclusion: Actionable Insights for Owners and Advisors

Startup Valuation Australia is not an exact science, and if an advisor thinks it is, they are either overconfident or deceiving their client. It is a formal dialogue between a founder who has a passion for what they are creating and an investor who is undertaking a systematic Risk vs. Return Analysis of a portfolio of risks. The most valuable forms of that conversation take place when the parties understand each other’s approaches, have done enough homework to frame their positions in evidence rather than opinion, and have the right mindset – namely, a genuine interest in whether there is a win-win solution – rather than a win-lose mindset.

The advice for founders is straightforward: Shape your Pre-Money Valuation expectations based on an Australian Comparable Startup Analysis. Build the Startup Funding Metrics – the quality of revenue, retention and unit economics – that minimise investor risk before you go out to raise. Sanitise your Cap Table and Founder Equity Dilution early in the game, with legal guidance. And anticipate the Risk vs Return Analysis conversations that will come with due diligence as an opportunity to show investors you are commercially savvy, not a threat.

For advisers and young professionals adding capacity in this area, the best thing you can do is to learn about the industry. The Venture Capital Valuation models can be learned from textbooks and journal articles, but the ability to apply them – to know whether the Growth Potential Assessment for a particular startup warrants a premium or a discount compared to similar rounds; to help founders with the inevitable conflict between aspirations and reality – comes from on-the-job experience. The Australian startup community is big enough to offer plenty of opportunities to learn and small enough for networks to form quickly. The best way to develop the intuition at the heart of successful early-stage advice is to work with it, at whatever level your role allows.

Frequently Asked Questions

Q1. Why is startup valuation important?

Startup valuation helps founders determine business value for fundraising, equity allocation, investment negotiations, and long-term strategic planning.

Q2. What factors affect startup valuation?

Revenue growth, market opportunity, intellectual property, customer traction, management capability, scalability, and competitive advantage all influence startup value.

Q3. Which valuation methods are commonly used for startups?

Common methods include the Venture Capital Method, Scorecard Method, Berkus Method, Discounted Cash Flow (DCF), and Market Approach.

Q4. Why is startup valuation more complex than valuing mature businesses?

Startups often have limited financial history, requiring greater reliance on future growth expectations and qualitative business factors.

Q5. How does professional startup valuation benefit founders?

Professional valuation strengthens investor confidence, supports fundraising, and provides a credible basis for negotiating investment terms.

1 thought on “Startup Valuation in Australia: How Investors Value Early-Stage Companies”