Table of Content

1. Introduction to Scope 1, 2, and 3 Emissions

When it comes to meeting Emissions Reporting Australia reporting obligations in 2026, businesses cannot afford not to understand the three-scope framework – it is the underlying basis for all credible climate reporting. Scope 1 Emissions, Scope 2 Emissions, and Scope 3 Emissions are the categorisations used for greenhouse gas emissions under the GHG Protocol Corporate Accounting and Reporting Standard and have become the global measurement framework adopted by mandatory and voluntary Carbon Disclosure Standards. In Australia, both the mandatory AASB S2 climate reporting standard and the National Greenhouse and Energy Reporting (NGER) scheme adopt this framework as their measurement standard, so any business with disclosure obligations must understand how to measure, classify and report emissions across the three scopes.

The real problem faced by most businesses is not the definitions – they are clear-cut. It is knowing how to manage the measurement of each of the three scopes, the data sources and validation of the data required to measure, and the relationships between the three scopes to provide an accurate, non-duplicated view of the business’s Carbon Footprint Measurement (also referred to as its Carbon Footprint). Scope 1 Emissions and Scope 2 Emissions are usually under direct operational control of a business and are easily measured with a high degree of accuracy. In contrast, Scope 3 Emissions relate to the full value chain and involve working with suppliers, customers and external data sources with whom most businesses have not yet had to work together in an organised and structured manner. It is Scope 3 that usually represents the bulk of a business’s Carbon Footprint Measurement – and is the most challenging to measure accurately.

This article is aimed at sustainability professionals, finance, and entry-level advisors interested in understanding the three-scope approach and its application in Australian businesses. It explores the definitions, measurement and challenges that each scope presents, and the measures businesses need to adopt to establish a Greenhouse Gas Accounting framework that is robust, repeatable, and able to support compliance with regulation and drive a Net Zero Strategy to success. The concepts presented here are relevant to all sectors and businesses, and the insights are based on the experiences of organisations at different stages of maturity in their greenhouse gas measurement.

2. Scope 1 and Scope 2: Measuring What the Business Directly Controls

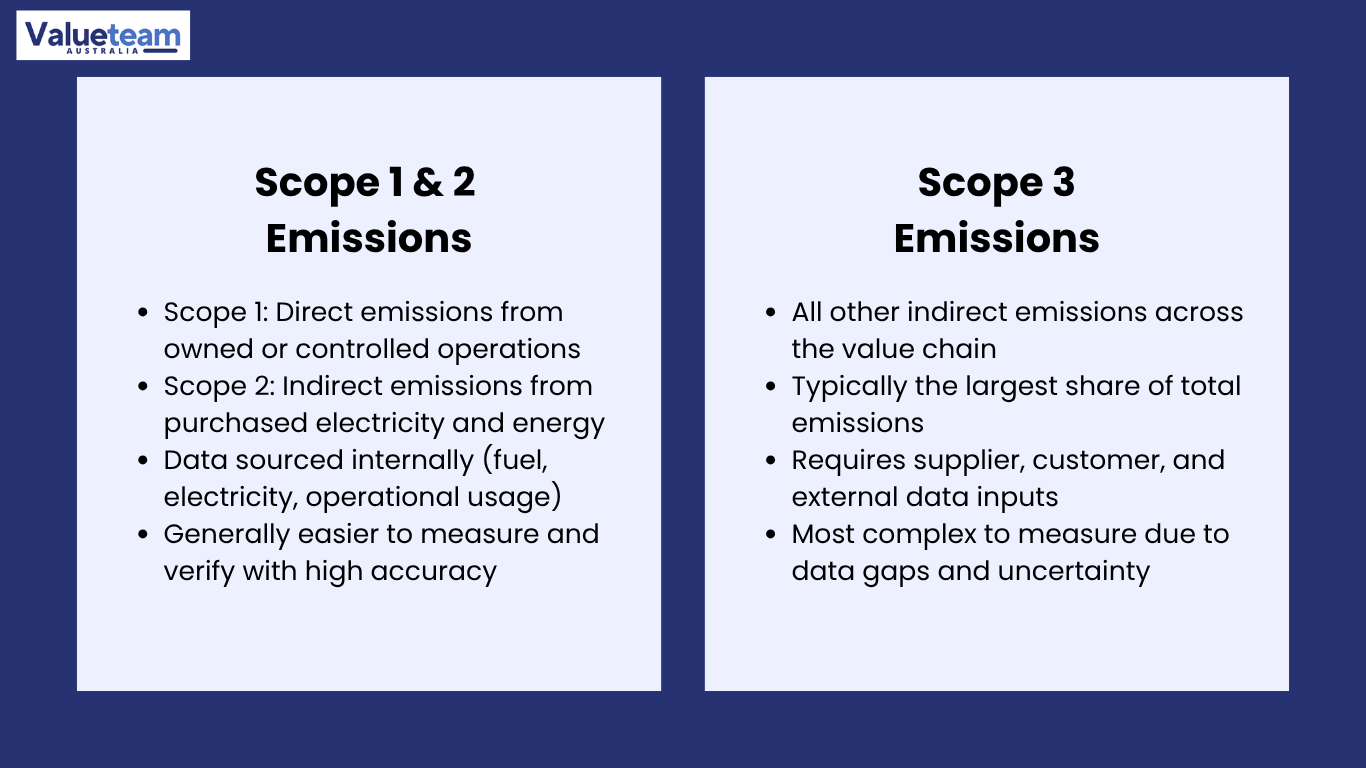

Scope 1 Emissions are direct greenhouse gas emissions from sources that the organisation owns or controls. These comprise fossil fuel combustion in owned vehicles, boilers, furnaces, and generators; emissions from industrial processes (cement, steel, chemicals); and fugitive emissions from refrigerants, air conditioners and gas supply. In Australia, Scope 1 Emissions are typically a relatively small source of overall emissions for most service-sector businesses, limited to fuel combustion from fleet vehicles and natural gas use in buildings owned by the business. For industrial, agricultural, and resources sector businesses, Scope 1 Emissions can be the largest emissions category and the most significant for operational and reputational purposes.

Scope 1 Emissions are the technically easiest aspect of Greenhouse Gas Accounting because all data comes from sources within the business and is under their direct control. Fuel use data from fleet management, gas meter data, and process engineering reports can all be used as activity data for calculating Scope 1 emissions using the Australian government’s National Greenhouse Accounts (NGA) emission factors. For businesses already impacted by the NGER scheme, Scope 1 and 2 emissions data is already being reported to the Clean Energy Regulator (CER) – a great starting point for compliance with AASB S2. For those exempt from NGER, the first step towards compliance is to implement processes for collecting data from Operational Emissions sources.

Scope 2 Emissions are indirect emissions from the production of purchased electricity, steam, heat or cooling used by the reporting entity. They are indirect because they are emissions associated with the power generation facility where the electricity is generated, rather than at the business; however, the business’s purchase of electricity creates a causal link with the generation facility and therefore indirectly drives emissions. In most Australian businesses, the largest component of Operational Emissions is Scope 2 Emissions from purchased electricity, reflecting our historically grid-dominated energy system. The GHG Protocol provides two options: a location-based measurement (using the average grid emission factor of the grid to which the business is connected) and a market-based measurement (using the emission factor of an electricity contract or certificate purchased). The method used can significantly impact reported emissions, and the decision to purchase green energy instruments that reduce market-based Scope 2 Emissions to zero is one of the most critical emissions management choices for most service-sector companies.

3. Scope 3 Emissions: The Value Chain Challenge

Scope 3 Emissions represent all other indirect emissions that take place in a company’s value chain, upstream (in the supply chain) and downstream (in the use and disposal of products and services). The GHG Protocol breaks down Scope 3 into 15 categories, including purchased goods and services, capital goods, upstream transportation and distribution, downstream transportation and distribution, business travel, employee commuting, use of sold products and services, end-of-life treatment of sold products, and others. The majority of Australian businesses have Scope 3 Emissions as the largest component of their Carbon Footprint Measurement – typically five to ten times the combined total of Scope 1 and Scope 2 for service companies and even greater for companies whose products have high emissions in use.

Scope 3 measurement of Supply Chain Emissions is the most complex practical element of Greenhouse Gas Accounting for most businesses. Whereas Scope 1 and Scope 2 measurements are based on internal data sources under the business’s control, Scope 3 measurements rely on the responsiveness, data accuracy, and emissions measurement competence of hundreds or thousands of suppliers, logistics providers, and customers. For most companies, the measurement of Scope 3 Emissions starts with spend-based modelling, where emission intensity factors are applied to supplier spending data from Environmental Input-Output (EIO) databases, which can provide a high-level indication of emissions but with significant uncertainty. The next step is to use supplier-specific data, obtained from suppliers via a verified method. This is a significant improvement in measurement precision but requires supplier engagement programs that are in their infancy for most organisations.

According to AASB S2, entities must disclose their Scope 3 Emissions if they are material to the entity’s climate risk and opportunity profile. The materiality assessment here is based on both the absolute magnitude of the Scope 3 category and its relevance to the entity’s transition risk, where the entity’s products or supply chains are exposed to carbon pricing, regulatory, or technological change. For banks and other financial institutions and investment managers, the most strategically important disclosure is that of financed emissions (emissions associated with the bank’s loan and investment portfolios, Category 15 of Scope 3), which is emblematic of the role that the financial sector plays in allocating capital toward or away from emissions-intensive activities.

4. Understanding the Three-Scope Framework: A Practical Reference

The table below provides a reference guide to the three-scope classification, key data sources, the measurement standard for each scope under the Emissions Reporting Australia framework, and the common measurement issues for each scope.

Scope | Definition & Key Sources | Primary Data Required | Measurement Challenge |

Scope 1 Emissions | Direct emissions from owned/controlled sources: vehicle fleet combustion, natural gas, industrial processes, fugitive refrigerant emissions | Fuel consumption records, gas meter data, process engineering data, refrigerant recharge logs; apply NGA emission factors | Completeness: smaller or distributed sources (e.g. site refrigerants, minor plant) are often missed; NGER methodology may differ from GHG Protocol |

Scope 2 Emissions | Indirect emissions from purchased electricity, steam, heat, or cooling; location-based (grid average) or market-based (contract-specific) method | Electricity meter data (kWh); emission factors from NGA or electricity retailer; any Large-Scale Generation Certificates (LGCs) or PPAs held | Method choice: location vs. market-based produces materially different results; market-based requires documentation of contractual instruments that many businesses do not currently maintain |

Scope 3 Emissions | All other indirect Supply Chain Emissions: 15 GHG Protocol categories covering upstream supply chain, business travel, employee commuting, use of sold products, and end-of-life | Supplier spend data, supplier emissions disclosures, logistics data, product lifecycle assessments, employee travel records, portfolio data (financial sector) | Data availability and quality: spend-based proxies carry high uncertainty; supplier-specific data requires engagement programmes; Category 15 (financed emissions) requires sophisticated portfolio-level analysis |

An essential consideration for those developing Greenhouse Gas Accounting programs is that the three scopes are mutually exclusive and collectively exhaustive. Every emission should be categorised in only one scope, without overlap between scopes. In reality, the line between Scope 1 and Scope 3 Category 3 (fuel and energy-related activities not included in Scope 1 or 2) is often blurred: the emissions upstream (extraction and processing) associated with purchased fuels are Scope 3, not Scope 1, even though the combustion of fuels is Scope 1. Likewise, the boundary between Scope 2 (purchased electricity) and Scope 3 Category 4 (upstream transportation) must be maintained when measuring leased buildings or shared services arrangements. Establishing an organisational boundary and emissions boundary – and documenting boundary decisions – is fundamental to the Carbon Footprint Measurement being auditable and comparable over time.

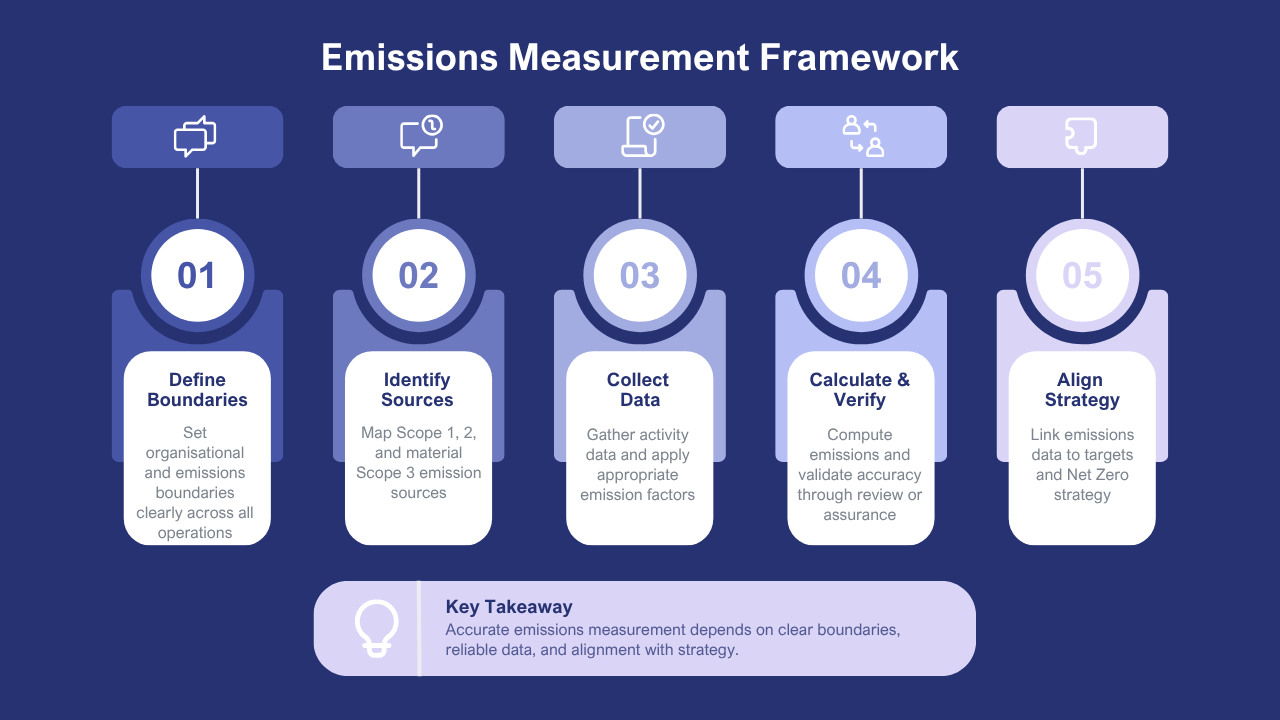

5. Five Key Steps to Building a Credible Emissions Measurement Programme

Across the spectrum of business types and sizes, those organisations that build the most robust and credible Greenhouse Gas Accounting capability follow a common set of steps. The following five steps outline the practical steps in developing an Emissions Reporting Australia programme that is compliant with the mandatory standard and meets the expectations of discerning investors, customers and auditors.

Step | What It Involves | Most Common Gap |

1. Define organisational and emissions boundaries | Determine which entities, operations, and emission sources are included in the inventory (equity share, financial control, or operational control approach); document all boundary decisions and exclusions explicitly | Boundaries are adopted from a peer company without a genuine analysis of the reporting entity’s own structure; leased assets and outsourced operations are excluded without a documented rationale, understating actual emissions |

2. Identify and categorise all emission sources | Map all Scope 1 Emissions, Scope 2 Emissions, and material Scope 3 Emissions categories; conduct a materiality screen to prioritise the Scope 3 categories most relevant to the business model and risk profile | Scope 3 materiality is assessed too narrowly, excluding categories that are large in absolute terms but difficult to measure; Category 11 (use of sold products) is frequently omitted by product businesses with significant product-in-use emissions |

3. Collect activity data and select emission factors | Establish systematic data collection for each identified source; select the most appropriate emission factors (NGA Factors for Australian operations; IPCC or sector-specific factors where NGA factors are unavailable); document data sources and estimation methods | Activity data is incomplete for minor sources; emission factors are not updated annually to reflect NGA revisions; spend-based Scope 3 estimation uses outdated EIO databases without disclosure of the uncertainty range |

4. Calculate, verify, and quality-assure the inventory | Calculate gross and net emissions for each scope; cross-check against prior year data and investigate significant variances; engage an independent third party for limited or reasonable assurance before disclosure | Assurance is deferred to a later reporting period; internal quality review is insufficient to catch systematic errors in data collection methodology; year-on-year restated figures are not disclosed with adequate explanation |

5. Integrate with Net Zero Strategy and set science-based targets | Connect the emissions inventory to the entity’s decarbonisation strategy; set targets aligned with the Science Based Targets initiative (SBTi) where applicable; report progress against targets consistently under Carbon Disclosure Standards | Targets are set as percentage reductions from a base year without verifying that the reduction rate is consistent with a credible Net Zero Strategy pathway; absolute reduction targets are avoided in favour of intensity metrics that can show improvement even when absolute emissions increase |

Step 5 – linking the emissions inventory with the entity’s Net Zero Strategy – is arguably the most challenging step for businesses. An effective Net Zero Strategy must deliver absolute emissions reduction across the three scopes, not just intensity-based reduction (tonnes of CO2 per unit of output or turnover). Enterprises that adopt intensity-based targets (such as tonnes of CO2 per unit of production) can show improved performance on the metrics. At the same time, total emissions do not change or even grow as the enterprise expands. Regulators, investors, and the Science Based Targets initiative are more rigorous: businesses should set absolute emissions-reduction targets that will limit global warming to 1.5°C. For companies that have not yet set science-based targets, it is important to understand the differences between these approaches and accurately disclose which target type is being met when reporting to investors and regulators.

6. Process, Challenges, and What the Market Teaches You

Greenhouse Gas Accounting is a multi-year commitment, and businesses that have advanced furthest in the process recognise that the initial year’s inventory is a work in progress. The four-part processing workflow below shows how companies with well-developed emissions measurement capability have built their capability and where the major practical difficulties lie.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Boundary & Source Mapping | Data Collection & Estimation | Inventory Calculation & Review | Disclosure & Target Setting |

Define organisational and operational boundaries; map all Scope 1 and Scope 2 Operational Emissions sources; screen Scope 3 categories for materiality; document boundary decisions for Carbon Disclosure Standards consistency | Collect activity data from internal systems; apply NGA emission factors for Scope 1 and Scope 2; apply spend-based or supplier-specific methods for Supply Chain Emissions; document data quality and estimation uncertainty | Calculate gross emissions by scope and category; conduct internal quality review; compare to prior year and benchmark against sector peers; prepare for third-party assurance as required under Emissions Reporting Australia | Prepare Carbon Footprint Measurement disclosure aligned with AASB S2 and Carbon Disclosure Standards; disclose Scope 1, 2, and 3 with methodology notes; set or update targets consistent with Net Zero Strategy commitments |

A common issue in Phase 2 is the limited availability and quality of supplier data for measuring Scope 3 Emissions. A large professional services company may have hundreds of suppliers, ranging from IT equipment and cloud computing to office facilities and travel. For most of them, emissions data is not available in a structured, verified format, so spend-based estimates are required. The uncertainty associated with spend-based estimates (which can differ by 50-100% from actual supplier emissions across industries, depending on the version of the EIO database used) means that caveats must be applied to Scope 3 emissions disclosures, which are primarily based on spend-based methods. Companies that explicitly disclose this uncertainty and have a plan to enhance data quality as suppliers are engaged are more trusted in the Carbon Disclosure Standards environment than companies that simply report spend-based Scope 3 data.

Assurance of Scope 3 Emissions data is a recent practice with evolving standards and expectations. Under the first mandatory reporting cycles of AASB S2, there is a requirement for limited assurance over Scope 3 disclosures when they are material. Assurance practitioners providing this service need to consider not only the accuracy of the numbers but also the reasonableness of the methodology, the inclusivity of the categories, and the suitability of the emission factors employed. Companies that have meticulously documented their Scope 3 methodology, including the reasons for category inclusion and exclusion, data sources and limitations of the measurement approach, will have a much easier time with the assurance process than those who view documentation of the methodology as optional.

7. Real Cases and What They Reveal

A case study that demonstrates the strategic importance of measuring Scope 3 Emissions is that of a consumer goods manufacturer that had made substantial headway with its Scope 1 Emissions and Scope 2 Emissions over the past five years, cutting operational emissions by over 40 per cent by replacing its fleet of vehicles with electric vehicles and sourcing renewable electricity. When the business undertook its first Carbon Footprint Measurement that included the Scope 3 emissions, it found that its Supply Chain Emissions from the raw materials purchased and its product-in-use emissions accounted for more than 85 per cent of the total emissions footprint – an aspect that it had not considered at all in earlier reporting. The Scope 1 and Scope 2 Emissions reductions – while real and significant – had only reduced less than 15 per cent of the business’s total emissions footprint. This shift in perspective radically realigned the business’s Net Zero Strategy to prioritise investments in supplier engagement, product reformulation, and circular-economy projects that address upstream and downstream emissions the operational focus had previously overlooked.

The second case illustrates the benefits of early investment in supplier emissions data. A large financial institution, which falls under the Group 1 category of the mandatory Emissions Reporting Australia (ERA) regime, was required to report financed emissions – the Scope 3 Emissions Category 15, which are the emissions from its loan and investment portfolio. In the first year of disclosure, the institution relied on emission intensity factors, which were sector averages, multiplied by the loan balances to arrive at a top-down estimate of the emissions with an acknowledged range of uncertainty. In the second reporting cycle, the institution had made the necessary investment in data partnerships with industry groups and specialist data providers that provided entity-level emissions data for a large share of its portfolio. This data quality improvement reduced the uncertainty range of the financed emissions estimate by 60 per cent, and the institution had a much more credible basis for its Carbon Disclosure Standards disclosure. The institution also leveraged this improved data to understand concentration risk in high-emissions sectors – a critical insight for its risk and portfolio management strategies.

8. Conclusion: Building Emissions Measurement Capability That Lasts

Knowing the three-scope definitions is the first step towards a credible Emissions Reporting Australia programme, but it’s not enough on its own. The hard work of developing a Greenhouse Gas Accounting capability that complies with mandatory Carbon Disclosure Standards, can be independently assured, and supports a credible Net Zero Strategy,y is about investing in data collection infrastructure, supplier engagement initiatives, and in-house expertise that many businesses are only now beginning to build. Businesses that will be best prepared as mandatory reporting standards are developed are those that have recognised their emissions measurement as a business tool (and not a compliance activity) from the beginning.

For sustainability and finance teams around the world, the most critical initial investment is in data quality and documentation of methodologies, not in measurement complexity. A documented and consistently applied spend-based estimate of Scope 3 Emissions with documented uncertainty ranges is more credible – and more useful to stakeholders – than a poorly documented supplier-by-supplier estimate which cannot be reproduced or verified by another party. As measurement capability improves, the shift to higher-quality data needs to be based on materiality: the Scope 3 categories that account for the largest percentage of the business’s total Carbon Footprint Measurement and the greatest transition risk exposure should be prioritised for data quality improvement.

For professional services advisers to businesses fulfilling their Emissions Reporting Australia obligations, the most valuable service is helping their clients understand the links between emissions measurement and emissions management. An inventory that measures and reports Scope 1 Emissions, Scope 2 Emissions and material Scope 3 Emissions is not a compliance exercise; it is a guide to where the material climate-related risks and opportunities lie in a business, and a resource that will inform the management decisions that will make a business’s Net Zero Strategy credible or just aspirational. Those who understand both the technicalities of Greenhouse Gas Accounting and the strategic consequences of the information it reveals will be among the most valuable resources for Australian businesses in the transition they are undertaking in 2026 and beyond.

Frequently Asked Questions

Q1. What are Scope 1, 2, and 3 emissions?

Scope 1 emissions come from direct business operations, Scope 2 covers indirect emissions from purchased energy, and Scope 3 includes emissions across the value chain.

Q2. Why is understanding emissions important?

Understanding emissions helps businesses measure their environmental impact, improve sustainability performance, and comply with evolving climate reporting requirements.

Q3. Which emissions are typically the most challenging to measure?

Scope 3 emissions are often the most complex because they involve suppliers, customers, transportation, and other indirect activities throughout the value chain.

Q4. Which organisations should monitor these emissions?

Businesses of all sizes, particularly those subject to ESG reporting or mandatory climate disclosures, should monitor and manage their greenhouse gas emissions.

Q5. How can businesses reduce their emissions?

Organisations can improve energy efficiency, engage sustainable suppliers, optimise operations, and implement emission reduction strategies across their value chain.