Table of Content

1. Introduction to Documents Required for Professional Business Valuation in Australia

When it comes to business valuations, you get what you put in. However skilled the valuer, however advanced the valuation techniques. However, to date, the market data and benchmarks used are up to date; the value of any valuation is limited by the quality, completeness, and accuracy of the documentation upon which it is based. For business owners facing the prospect of a sale, a dispute, a restructure or a financing event, knowing exactly what documents will be required in the valuation exercise and ensuring they are available in a reconciled, well-organised format is one of the fastest, cheapest and most effective ways to manage cost, time and risk in the engagement process, and to improve the quality and credibility of the final valuation report.

In reality, the process of gathering and reviewing underlying documents is the most common source of delays, costs, and quality risks to the valuation report, according to professional valuers. In many Australian SMEs, financial documentation is technically correct but functionally unhelpful: management accounts that don’t reconcile with tax returns, asset registers that haven’t been updated for a decade, and customer contracts that are in various states of execution across different file systems and email accounts. When faced with this reality, a valuer must spend considerable time re-arranging and reconciling information that could have been prepared by the business owner – time that is billed but not used for analytical purposes.

This article is for business owners looking to understand what information a professional valuer needs and why, and for young to mid-level advisory practitioners looking to build their skills in helping business owners prepare documents. It outlines the 10 most significant document categories in a professional business valuation, how they are used in the valuation, and the preparation guidance that has the best record of delivering the best outcomes for the owner and advisors. The preparation tips provided here are relevant regardless of the purpose of the engagement (trade sale, shareholder dispute, tax, financial reporting, etc).

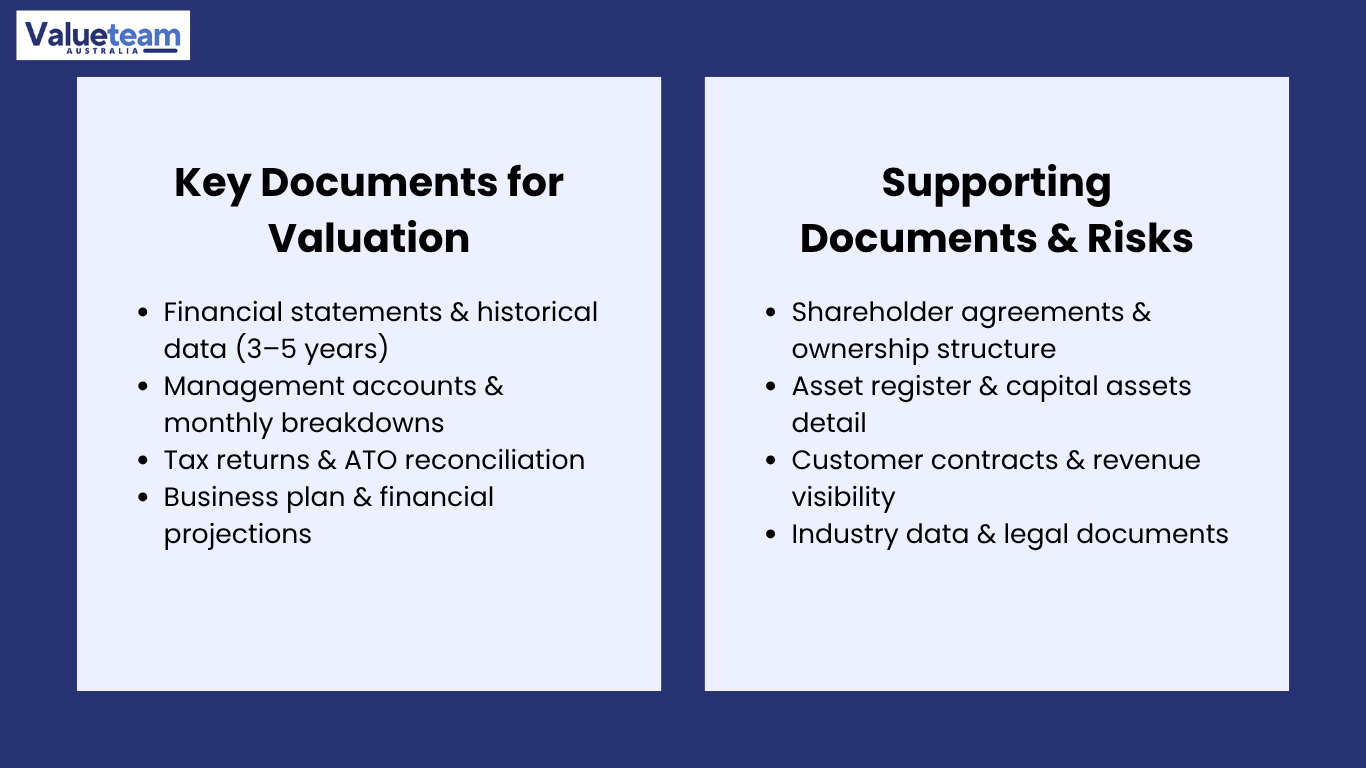

2. Financial Records: The Foundation of Every Valuation

The most significant document category in a business valuation is the financial records, and within those records, the consistency over time is key. Financial Statements Review is the analytical foundation of the valuation process: it is the process by which a valuer determines the true earnings of the business, identifies the add-backs and one-offs made by the owner, and sets the normalised EBITDA figure that will serve as the primary driver for valuation methodologies. Without “clean” (i.e., properly adjusted) financial statements for at least three years of prior trading, there can be no normalisation exercise – and without normalisation, the valuation exercise is open to scrutiny.

The norm in Australia for a professional valuation exercise is three to five years of Historical Financial Data. That is, profit and loss statements, balance sheets, and cash flow statements for each annual period, prepared using a common methodology and supported by working papers that enable the valuer to track the key line items back to their original entries. If the business has been audited or reviewed by an independent accounting firm, those audited or reviewed financial accounts are given greater weight than internally prepared accounts, both because an independent firm has reviewed them and because the accounting methodology is likely to be consistent from year to year. It is worth considering a review engagement for those businesses that have not had their accounts reviewed before commencing a valuation, especially if the valuation is to be used by a sophisticated purchaser or in litigation.

Management Accounts are an important and related document type. Statutory financial statements are annual summaries of business activity. Still, management accounts are monthly or quarterly summaries that enable a valuer to detect seasonality, revenue timing problems and other anomalies that an annual summary may obscure. A company whose statutory financial statements show steady revenue for the past three financial years might well show, in its monthly management accounts, that revenue is very seasonal and that the current year is lagging well behind the previous year – information that has a direct bearing on the valuation. Valuers without access to management accounts work with annual summaries and therefore have a less detailed picture than those with access to monthly management accounts.

3. Tax Returns, Projections, and Forward-Looking Documents

Tax Returns Documentation has two functions in a valuation engagement. Firstly, it serves as an independent reconciliation of the financial statements: the revenue and profit figures reported to the ATO can be compared with those reported in the management accounts to identify any reconciliation differences that, in some cases, represent legitimate one-offs but, in others, suggest inconsistencies in the preparation of the accounts. Secondly, the tax returns provide explicit information (on related-party transactions, employee benefits, loans to directors, and so on) that may not be reflected in the statutory financial statements but is relevant to the EBITDA normalisation process. Those businesses that are up to date with their ATO obligations and can produce signed tax returns for the previous three years are significantly better off than those with outstanding returns and/or disputes with the ATO.

Business Plan Projections are necessary not as a key input to valuation in most SME valuations – where the EBITDA multiple method is the most common valuation approach – but as a contextual document that permits the valuer to see management’s expectation for the future performance of the business, and to compare that expectation with the historical performance of the business. A business plan that assumes 40 per cent market growth, given the business’s historical 8 per cent per annum growth rate, needs to be justified and explained before being used as an input to a forward-looking valuation. On the other hand, an explanatory business plan that outlines a growth plan, customer backlog, and investment opportunities is the kind of contextual information that supports a higher valuation. Valuers do not take business plans as gospel, but a carefully constructed plan is an important element in the story that supports the valuation.

Where valuations involve a discounted cash flow analysis – which is usually the case for higher growth, capital-intensive or pre-profitable businesses – the financial model used to produce the Business Plan Projections is an essential document. The valuer will need to scrutinise the model, benchmark assumptions against past results and industry averages, and alter or rebuild the model as required to generate a projection that can be supported as a base case. Business owners who have taken the time to build a modelled financial projection (as opposed to a spreadsheet projection) as part of their business plan stand to save a great deal of time at this stage, while putting themselves in a better position to address the valuer’s queries and model revisions.

4. Legal, Operational, and Structural Documents

Shareholder Agreements and other governance documents are necessary for a professional valuation for two reasons. Firstly, they define the nature of the ownership and control being valued: any transfer restrictions, drag-along and tag-along rights, pre-emptive purchase rights or buy-sell arrangements in a shareholders’ agreement impact on the marketability and transferability of the equity interest being valued, and these must be understood and communicated in the valuation report. Secondly, the Shareholder Agreements often include valuation provisions (for instance, a formula or approach for discounting the value of a shareholder’s interest who is exiting a shareholding in the entity) that are binding on the valuer and must either be followed or the valuer must explain why they are not. Not supplying this document risks a valuation inconsistent with the business’s governance structure.

The Legal and Corporate Documents category is a catch-all category that includes the company’s ASIC records, constitution, any licences or permits required to operate and records of any current or past proceedings. The items of most interest for valuations in this category are anything that might impact the business’s continuity: licences that are transferable or non-transferable, leases that are assignable or subject to landlord consent, and any threatened or pending litigation that is a contingent liability not disclosed on the business’s financial statements. The buyer will scrutinise all of these items, and their due diligence advisors, and a valuer who uncovers them as early as possible (rather than leaving them until the buyer’s due diligence) will deliver a valuation that is less susceptible to post-offer price adjustment.

The Asset Register Details are important for businesses with significant physical assets that contribute to their value, as is typically the case in manufacturing, hospitality, logistics, and property-related businesses. An up-to-date, well-cultivated asset register provides the valuer with a complete list of physical assets, the dates of their acquisition, their written-down book values, and their condition – information required to perform both an asset valuation and to quantify the capital expenditure required by any forward-looking financial model. An asset register that has not been updated for two or three years, or that reflects assets that have been disposed of but remain on the list, creates work to reconcile the asset register and, consequently, uncertainty in the valuation conclusion.

5. The Top 10 Documents: A Professional Preparation Framework

The table below outlines the ten most common categories of documents required in a professional business valuation in Australia, the specific documents in each category required by the valuers, and the most frequent preparation issue that delays the engagement. Business owners can use this framework to prepare for the valuation process (and for advisors to prepare their clients) to speed it up, reduce its cost, and strengthen its defensibility.

Document Category | Specific Items Required | Most Common Preparation Gap |

1. Financial Statements Review | Profit and loss, balance sheet, cash flow — three to five years; audited or reviewed where available; working trial balances for key years | Statements prepared on inconsistent bases across years; prior-year comparatives not reconciling to signed accounts |

2. Historical Financial Data | Month-by-month revenue and EBITDA breakdowns; year-on-year trend analysis; gross margin by product or service line | Annual summaries only, with no monthly detail; inability to explain year-on-year variances without reference to internal systems |

3. Management Accounts | Monthly P&L and balance sheet for the current financial year; comparison to prior year and budget; aged debtor and creditor schedules | Management accounts are not prepared regularly; significant differences from statutory accounts, with no documented reconciliation |

4. Tax Returns Documentation | Signed income tax returns — three years; BAS lodgement history; notice of assessments; any ATO correspondence or outstanding obligations | Outstanding lodgements; undisclosed ATO disputes; differences between tax returns and management accounts not explained |

5. Business Plan Projections | Three-to-five year financial model with documented assumptions; narrative business plan covering strategy, market, and growth initiatives | No formal projection model; projections based on aspirational growth without historical substantiation or market evidence |

6. Shareholder Agreements | Current shareholders’ agreement; any buy-sell provisions or valuation formulae; cap table with full shareholding and option schedule | Informal or unsigned arrangements; outdated agreements that do not reflect current ownership; undisclosed option grants |

7. Asset Register Details | Full fixed asset register with acquisition dates, cost, accumulated depreciation, and condition notes; any recent independent asset appraisals | Asset register not updated for years; assets written off in accounts still appearing on register; no condition assessment for key assets |

8. Customer Contracts | Top 10 to 20 customer contracts by revenue; contract terms, renewal dates, exclusivity provisions, and any concentration risk disclosures | Informal customer arrangements without written contracts; inability to demonstrate contracted versus at-risk revenue |

9. Industry Benchmark Data | Sector reports, industry association data, or market research relevant to the business’s competitive position and growth outlook | No independent market data; reliance on management’s characterisation of market size and competitive dynamics without external substantiation |

10. Legal and Corporate Documents | ASIC current and historical extracts; licences and permits; lease agreements; any current or historical litigation records | Licences not in the entity’s name; leases with change-of-control clauses undisclosed; pending litigation not disclosed until late in the process |

The most under-estimated items in this list are items 8 (Customer Contracts) and 9 (Industry Benchmark Data). Business owners often assume that valuers will take their word for the customer list (and in a low-stakes internal planning scenario, they might). If the output of the engagement is to be reviewed by a knowledgeable buyer, a court, or an auditor, the lack of formal Customer Contracts for the major sources of revenue raises questions about the quality of reported revenues that cannot be addressed solely by a narrative. In the same way, Industry Benchmark Data obtained from independent sources – IBISWorld sector reports, industry association data, or independent market research studies – offers an objective benchmark against which the valuations’ assumptions regarding growth, profitability and market position can be tested. Valuers who rely solely on management’s assertions about market conditions are relying on a single (and perhaps biased) view of an issue critical to the business’s pricing.

6. Process, Real Cases, and Lessons for Advisors

Gathering documents for a valuation is a multi-stage process that, when well handled, leads to an efficient and reliable valuation. Knowing the four steps of this workflow – and the potential issues that may arise along the way – is valuable information for any advisor who supports a client with a valuation engagement.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Document Request & Scoping | Receipt & Initial Review | Gap Resolution & Clarification | Validation & Normalisation |

Issue structured document request list tailored to business type and valuation purpose; identify Financial Statements Review standard; clarify Management Accounts format and availability; set data room or submission timeline | Conduct completeness check against document request; reconcile Financial Statements Review to Tax Returns Documentation; identify gaps in Historical Financial Data, Asset Register Details, and Customer Contracts | Issue targeted follow-up requests for missing items; reconcile Management Accounts to statutory accounts; obtain Industry Benchmark Data where not provided; review Legal and Corporate Documents for continuity risks | Cross-reference all document categories; build normalisation schedule supported by documentation; confirm Business Plan Projections consistency with historical record; finalise data set for valuation modelling |

A recent example of the consequences of poor document preparation involved a distribution business that appointed a valuer some six weeks before a sale process. When the valuer issued the standard document request, the business owner produced three years of management accounts. Still, these had been prepared by different bookkeepers over the years, and the treatment of several key cost items was inconsistent. The Financial Statements Review took an additional three weeks than expected because, in reconciling with Tax Returns Documentation, the valuer had to rebuild the accounts from the original entries. The Asset Register Details submitted were three years old and included equipment that had been sold since then. And most of the revenue from customers was based on informal agreements with no formal Customer Contracts, so the valuer had to provide a supplementary analysis of revenue concentration that would not have been required if formal contracts were in place. The delay cost the client about $8,500 in valuer fees (nearly half of the total valuer fees charged) and delayed the sale’s commencement by 30 days.

Another example shows what the best practice preparation of documents looks like and the results. A professional services firm engaged its accountant six months before a planned management buyout to audit the previous two years’ financial statements and review the current year’s financial statements. Monthly Management Accounts were audited and reconciled with the statutory accounts. A schedule of Asset Register Details was prepared and updated by an appraisal of equipment. All Customer Contracts for the top 15 clients – 82% of revenue – were gathered, assessed for assignability and dated for renewal. The client’s lawyer reviewed the Shareholder Agreements and prepared a summary of the terms and conditions for the valuer. When the valuation engagement began, the document review stage was completed in three days, rather than the two to three weeks required for an unprepared engagement. The valuer’s normalisation analysis was completed with a few questions, assumptions supported the Business Plan Projections, and the report was provided on time. The overall cost of the engagement was less than the market average for such a business, and the report passed management due diligence review with limited challenge.

7. Conclusion: Actionable Guidance for Owners and Advisors

The outcome of a professional business valuation in Australia is heavily dependent on the quality of the documents submitted to inform it. Review of Financial Statements, Historical Financial Data, Management Accounts, Tax Returns Documentation, Business Plan Projections, Shareholder Agreements, Asset Register Details, Customer Contracts, Industry Benchmark Data, and Legal and Corporate Documents – the ten categories of documents provide the “proof” for all credible valuations. Business owners who view document preparation as a compliance exercise to be completed with minimal effort invariably receive a lower-quality outcome (in terms of time, cost and defensibility) than those who view it as an investment in the value of the outcome.

For the business owner, the key takeaway is to start gathering the documents 3 to 6 months before the planned valuation date. This leaves time to resolve inconsistencies in the financial books and records, formalise informal arrangements with customers, update out-of-date asset registers, and commission any independent reviews and appraisals that will add to the evidence base. For Industry Benchmark Data in particular, searching for a sector report or paying an industry research provider to provide such data early on ensures that the valuer understands the market analysis in context, rather than later in the engagement.

For other advisors, the document preparation framework in this article offers an effective framework for discussions with clients at the beginning of a valuation engagement. Explaining to a client which documents are important, why, and how the typical preparation deficiency manifests itself – before the engagement has started, rather than after the first document request – is precisely the kind of proactive advisory service that inspires confidence and delivers value. The difference between a well-prepared and a poorly-prepared document set is not just one of convenience: it is one of quality, credibility, defensibility, and confidence in the resulting valuation and in the ability of both the client and the advisors to defend it.

Frequently Asked Questions

Q1. What is a professional business valuation?

Business valuation in Australia is a process of estimating the economic value of a business, ownership interest or a particular asset. It is important because it forms the basis of key business decisions such as purchasing, selling, raising funds and solving conflicts, which gives it a fair and objective basis that everyone can depend on.

Q2. Why is a professional business valuation important?

A business valuation is the analytical process of establishing the value of a business or ownership interest. A separate expert opinion is a step further as it is a formal, objective opinion on whether a particular transaction is fair and reasonable, usually in the interest of shareholders or other interested parties who are considering the proposed transaction.

Q3. Which valuation methods are commonly used?

An independent expert report is usually needed when a fair and objective opinion of a transaction is vital, especially when various parties are involved, and an independent opinion is needed to support transparency, confidence, and informed decision-making in the final outcome.

Q4. Who should obtain a professional business valuation?

The timeframe depends on business complexity, valuation purpose, and data availability. The less complex interactions can be accomplished in a few weeks, whereas more elaborate or formal assignments can take longer. Anticipated schedules are negotiated and agreed upon at the beginning of any engagement.

Q5. How does an independent valuation benefit businesses?

Typically, we require historical financials, recent management reports, and any available forecasts or business plans. Background information on operations, ownership, and governance is also helpful. To ensure that the process is as simple as possible, a clear information checklist is provided at the start of each engagement.