Table of Content

1. Introduction: Goodwill vs Intangible Assets

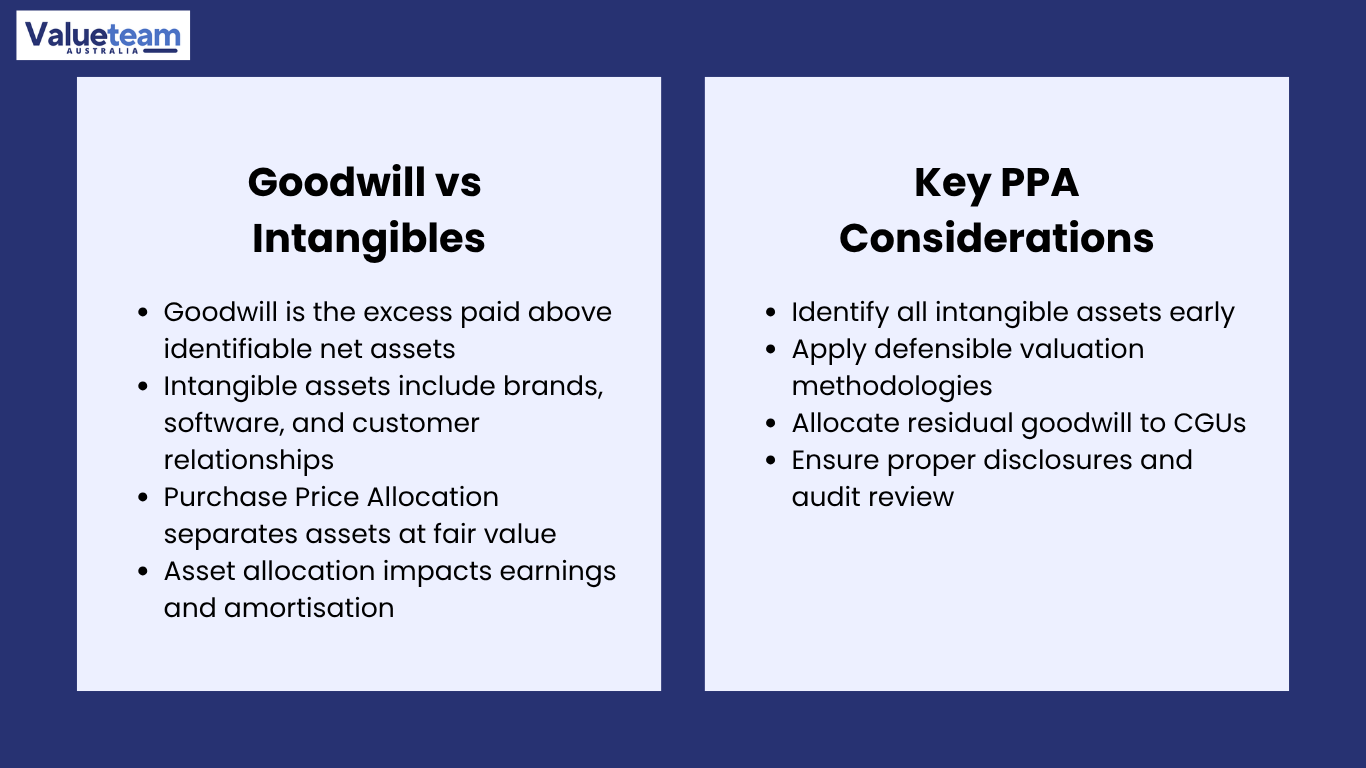

When a buyer purchases a business at a price above the fair value of the business’s identifiable net assets, the excess is reported in the financial statements as goodwill. It is among the most prominent line items on the balance sheets of most acquirers – but is also among the least understood, especially by those new to the M&A and advisory arena. The difference between Goodwill vs Intangibles is not necessarily an accounting technicality: it can determine how the acquisition is reported, how future earnings are impacted by amortisation, how annual impairment testing works, and what the Deal Value Breakdown actually says about what the buyer believed they were purchasing.

Purchase Price Allocation (PPA) is the process by which acquirers allocate the total price paid to the individual assets and liabilities acquired at their fair values. In accordance with AASB 3 (Business Combinations), it is the responsibility of this exercise to identify and separately recognise all Identifiable Intangible Assets that meet the recognition criteria of the standard – even though those assets were not listed on the balance sheet of the seller before the acquisition. The part of the price which cannot be ascribed to any particular identified asset, tangible or intangible, passes on to Residual Goodwill Value. Goodwill in this context is not a valuation concept – it is an accounting residual.

This article is aimed at junior professionals in the accounting, corporate finance, and M&A functions who wish to know the practical difference between Goodwill vs Intangibles, how the process of Purchase Price Allocation works, why both buyer and seller have strong interests in how the value is allocated across these categories, and what the lessons of real transactions tell us about the accounting and commercial implications of getting it right – or wrong.

2. Understanding Goodwill vs Identifiable Intangibles

What is Residual Goodwill Value, and what does it represent?

The amount of Goodwill Value remaining in an acquisition is the economic benefits of assets that cannot be identified separately and recognised separately. In theory, it reflects the synergies between the combined entities, the assembled workforce, the strategic positioning created by the acquisition, and the premium paid to unlock future growth potential not pegged to a specific identified asset. In practice, the difference between the purchase consideration and the total fair value of all Identifiable Intangible Assets, tangible assets, and liabilities recognised at the date of acquisition is known as goodwill.

- Unlike Identifiable Intangible Assets, goodwill is not amortised under IFRS; it is subject to annual impairment testing under AASB 136, which means it can only be written down, not written back up.

- The presence of a large goodwill balance relative to the total acquisition price is an indicator that the buyer paid a substantial premium that cannot be attributed to any specific identified asset, either because the identified intangibles were really few or because they were not identified in the PPA exercise to any satisfactory extent.

- M&A Accounting Goodwill Differences in how goodwill is treated in IFRS (no amortisation; annual impairment test) and in US GAAP (right of the company to amortise) – an aspect practitioners working on cross-border transactions must not ignore.

What qualifies as an Identifiable Intangible Asset?

Under AASB 3, an intangible asset can be identifiable (and therefore required to be separately recognised) either because it meets the separability criterion (it can be separated from the entity and sold, licenced, rented or exchanged) or the contractual-legal criterion (it arises out of contractual or other legal rights, whether or not those rights are transferable or separable with the entity). The purpose of this definition is to capture a wide spectrum of assets that would not be included in the pre-acquisition balance sheet of the seller because they were either internally generated (not capitalised under the AASB 138) or had never been formally valued.

3. The Purchase Price Allocation Process in Practice

How Acquisition Accounting distributes the purchase price

The AASB 3 requirement for Acquisition Accounting is that the acquirer should complete the Purchase Price Allocation within 12 months of the acquisition date, the measurement period. It starts with a determination of all assets obtained, and liabilities incurred, then valuing each one of them at their acquisition-date fair value. The most critical technical issue is the identification and valuation of Identifiable Intangible Assets: brand names, customer relationships, technology platforms, non-compete agreements, and order backlogs, which must be separately valued and recognised.

- The multi-period excess earnings (MEEE) technique of Fair Value Allocation is typically used to value customer relationships after adjusting the earnings of all other contributing assets.

- The relief-from-royalty method is typically used to value brand names: the present value of the royalty payments the business would hypothetically pay to license the brand if it did not own it.

- Technology and software platforms can be valued using the relief-from-royalty method (where other similar royalty rates apply) or the cost-to-recreate approach, adjusted for obsolescence.

The Intangible Asset Recognition decision and its consequences

The recognition between Identifiable Intangible Assets and Residual Goodwill Value directly affects financial reporting. Any identified intangible asset with a finite useful life will be amortised over its finite useful life, decreasing reported earnings in each period following the acquisition. An intangible customer relationship with a 7-year life and a fair value of 2 million generates annual amortisation of 286,000. A brand with a fair value of $1.5 million and a 10-year life yields annual revenue of $150,000. These amortisation expenses are included in the income statement and reduce the bridge between EBITDA and net profit, which affects reported earnings, earnings per share, and, in some cases, debt covenant calculations.

Asset Category | Typical Valuation Method | Typical Useful Life | Intangible Asset Recognition Criterion |

Customer relationships | Multi-Period Excess Earnings (MEEM) | 5–12 years | Separability: can be valued and transferred independently of the entity |

Brand names/trademarks | Relief-from-Royalty | Finite (5–15 years) or indefinite, depending on brand durability assessment | Contractual-legal: trademark registration confers legal rights |

Technology / proprietary software | Relief-from-Royalty or Cost Approach | 3–7 years | Separability or contractual-legal, depending on the protection mechanism |

Non-compete agreements | Income approach: probability-weighted loss if competition occurred | Equal to contractual term (typically 2–5 years) | Contractual-legal: exists by virtue of the agreement |

Order backlog | Direct income approach to contracted revenue at the acquisition date | Short (6–18 months); reflects backlog duration | Contractual-legal: arises from specific customer orders or contracts |

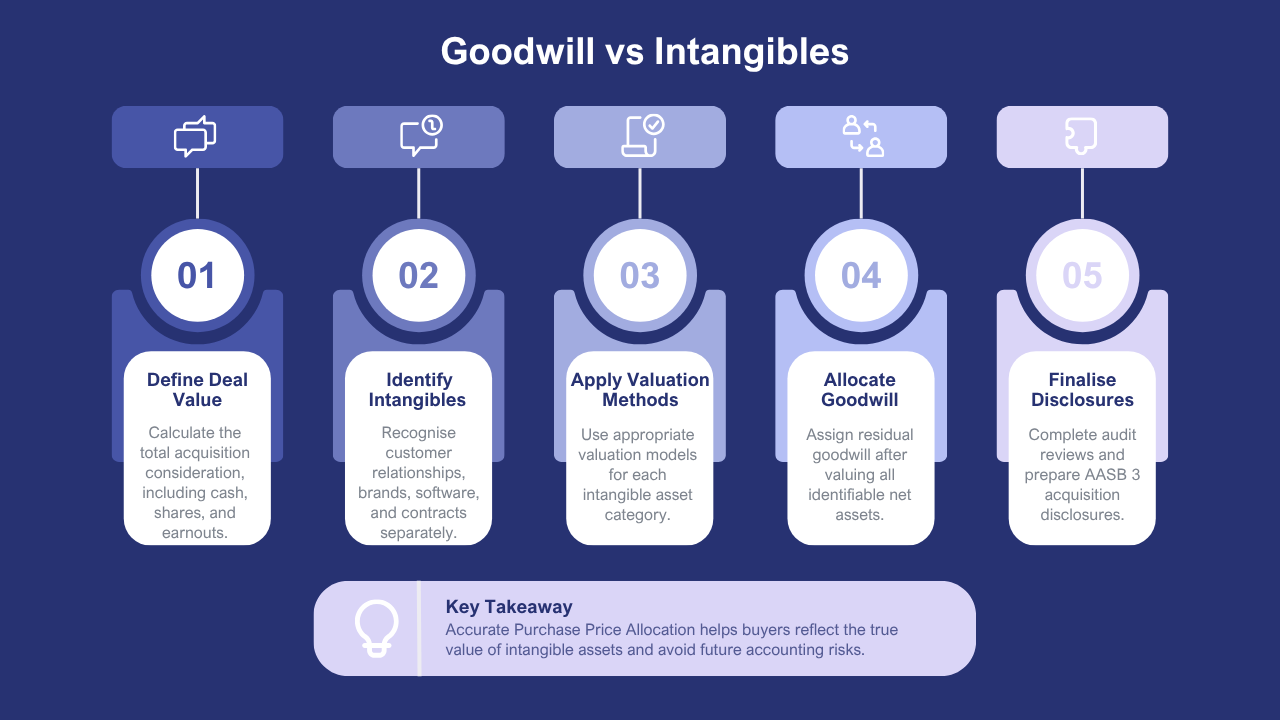

4. Five Key Steps in a Rigorous Purchase Price Allocation

A properly prepared Purchase Price Allocation is not just an after-completion accounting exercise. It has actual commercial, tax and financial reporting implications – and the quality of the process defines whether they are pre-empted and dealt with or they are found out afterwards. The five steps below outline how experienced practitioners approach the exercise.

Step | What It Involves | Why It Matters | Common Failure Mode |

1. Determine total consideration | Measure all forms of consideration at acquisition-date fair value: upfront cash, deferred consideration, contingent consideration (earnouts), and any equity instruments issued | The opening balance of goodwill depends on the total consideration figure; earnouts must be fair-valued at the acquisition date, not at their maximum contractual amount | Using the maximum earnout amount rather than the probability-weighted fair value, not including non-cash consideration at fair market value |

2. Scope the Identifiable Intangible Assets | Apply the AASB 3 recognition criteria systematically to all potential intangibles; use sector benchmarks to identify the intangible categories typically present in comparable transactions | Comprehensive scoping prevents the under-identification of intangibles that auditors will challenge; it sets the work plan for the valuation phase | Scoping only the obvious intangibles (brand, patents) without examining all potential categories, and not using sector-specific comparables to identify what the auditor will expect |

3. Apply Fair Value Allocation methodologies | Engage specialist valuers for each identified intangible category; document the methodology, assumptions, and sensitivity analysis for each asset; cross-check results against the implied acquisition multiple | Documented, defensible methodologies withstand audit scrutiny; cross-checks against the deal multiple identify methodological inconsistencies before the auditor does | In-house estimates without specialist support; insufficient sensitivity analysis; no cross-check of the implied return on intangibles against deal economics |

4. Calculate Residual Goodwill Value | Subtract the fair value of all identified net assets (tangible and intangible) from the total consideration; allocate goodwill to cash-generating units (CGUs) for annual impairment testing purposes | A proper CGU allocation structure is essential for manageable annual impairment testing; poor CGU design creates complexity and audit friction in subsequent years | Treating goodwill allocation to CGUs as an afterthought, the CGU structure is not aligned with how management actually monitors the business post-acquisition |

5. Disclose and assure | Prepare the AASB 3 required disclosures in the acquisition notes; ensure the external auditor reviews the PPA as part of the year-end audit; and document all significant judgments and estimates. | Transparency in disclosures protects the acquirer from restatement risk; audit review catches errors before they compound into future periods. | Boilerplate disclosures without specific facts; not engaging the auditor during the measurement period; discovering material errors after the measurement period closes |

Step 4 – assigning Residual Goodwill Value to CGUs – is consistently underweighted relative to its continued significance. All subsequent annual impairment tests under AASB 136 are determined by the CGU structure adopted at the time of acquisition. A CGU structure does not reflect the way in which management monitors and reports on the business, creating complexity in each successive year thereafter. Whether it is necessary to reallocate goodwill or to subject a structure that does not reflect economic reality to impairment tests. The cost can pay off once by investing time in thoughtfully designing the CGU structure at the acquisition, with input from not only the finance function but also the operations team.

5. Real Cases and What They Teach Practitioners

The PPA workflow in practice

Acquisition Accounting and Purchase Price Allocation have a predictable workflow between deal close and finalised financial statements. Knowledge of the timing and location of significant decisions taken is a practical skill for any practitioner in the field of M&A, advisory, or corporate finance.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Deal Close & Scoping | Fair Value Assessment | Goodwill Calculation & CGU Allocation | Audit, Disclosure & Finalisation |

Confirm acquisition date and total consideration; scope Identifiable Intangible Assets by sector; brief specialist valuers; establish provisional accounting entries; agree measurement period milestones | Apply Fair Value Allocation methods to tangible and intangible assets; model deferred tax on all step-ups; prepare a provisional Purchase Price Allocation schedule; address auditor queries on methodology | Calculate Residual Goodwill Value; allocate to CGUs aligned with management reporting; document CGU structure for ongoing Acquisition Accounting; prepare AASB 136 impairment testing framework | Support auditor review of all Fair Value Allocation assumptions; finalise Purchase Price Allocation within measurement period; prepare AASB 3 acquisition note disclosures; document Deal Value Breakdown for investor and analyst communications |

Case 1: Under-identification leading to restatement

The business being acquired was in the financial services industry, and the price implied a considerable premium over the seller’s net tangible assets. The acquirer’s internal accounting team prepared the original Purchase Price Allocation with little or no expert intangible valuation advice, and most of the consideration was allocated to Residual Goodwill Value. The external examiner, as part of the review of the Intangible Asset Recognition exercise at the end of the year, identified that the customer relationship base, which was clearly the main factor that had caused the premium to be paid, had not been recognised separately to the extent required by AASB 3. The time frame was over. The outcome was that the opening balance sheet was restated. There was a large increase in the customer relationship intangible and a similar decrease in the goodwill, introducing amortisation charges which the acquirer had failed to model in its post-acquisition earnings projections. The Accounting Treatment error in M&A Accounting was found too late to be corrected during the measurement period, and the restatement process entailed costs, complexity, and audit friction in the next reporting period.

Case 2: Competing interests in the Deal Value Breakdown

A public company whose analysts were interested in reported EBITDA growth after the acquisition of a technology business. The acquirer had a clear preference: to maximise the Residual Goodwill Value in the Purchase Price Allocation, as goodwill is not amortised, so a higher goodwill allocation minimised the annual amortisation expenses that would otherwise lower reported earnings. The seller’s advisors, whose client was receiving share-based consideration, had a presence in the technology platform, which was separately recognised as an Identifiable Intangible Asset at fair value that supported the acquisition economics. The auditor questioned the preferred allocation that the acquirer wanted to make and required a more comprehensive Intangible Asset Recognition exercise, which identified a technology asset and a customer relationship asset that, together, decreased goodwill by about $4.2 million and introduced annual amortisation charges of about $560,000. The Buyer Value Perception of the technology was, in reality, the Fair Value Allocation exercise; it was just made apparent in the financial statements.

6. Conclusion

Goodwill vs Intangibles is no abstract accounting distinction – it is a commercially relevant decision that impacts annual earnings, impairment risk, tax treatment, and transparency of the Deal Value Breakdown that investors and analysts will interpret. Purchase Price Allocation done in good faith, with a full scope of Identifiable Intangible Assets and a defensible methodology of Fair Value Allocation, would produce financial statements that truly represent what the purchaser is actually buying and why. The accounting liability that multiplies in each successive reporting period is the accumulated Goodwill Value, inflated by under-identifying intangibles.

To practitioners: have a specialist valuer on board at the earliest stage, and conceive the CGU structure during acquisition rather than retrofitting it later. In junior professionals developing capability in Acquisition Accounting, the Purchase Price Allocation exercise is where the commercial logic of the acquiring is converted into the accounting language of the financial statements. Knowing how to read that translation and what it can tell you about what buyers actually valued is one of the most practically useful tools in the M&A and corporate finance toolkit.

Frequently Asked Questions

Q1. What is the difference between goodwill and intangible assets?

Intangible assets are identifiable non-physical assets, while goodwill represents the excess purchase price paid above the fair value of identifiable net assets during an acquisition.

Q2. What are examples of identifiable intangible assets?

Examples include trademarks, patents, software, customer relationships, copyrights, and proprietary technology.

Q3. When is goodwill recognised?

Goodwill is recognised after a business acquisition when the purchase price exceeds the fair value of identifiable assets and liabilities.

Q4. Why is the distinction important?

Separating goodwill from identifiable intangible assets improves financial reporting accuracy and supports accounting compliance.

Q5. How do valuation professionals determine goodwill?

Professionals first value identifiable assets and liabilities before calculating goodwill as the remaining acquisition value.

2 thoughts on “Goodwill vs Intangible Assets: What Buyers Really Pay For”