Table of Content

1. Introduction to ESG Framework Design

Designing a legitimate ESG Framework Design is more important than ever for Australian mid-sized companies, and more complicated. You are working in an environment where the ESG mandatory disclosure requirements of large entities are filtering through supply chains, where institutional customers and lenders are increasingly asking for evidence of your ESG credentials, and where your regulatory obligations, in some cases, are soon to be upon you and your organisation may not be quite ready for them.

The Mid-Sized Company ESG challenge is not the same as that for large, listed entities with sustainability managers and many years of reporting. Resources are constrained. The company may not have an ESG starting point. The board may be unfamiliar with the frameworks. And the need to “do something” – develop a policy, a report, some targets – often comes before governance and data systems are established to sustain it.

This guide is here to help. It outlines the nature of a real ESG Framework Design for a mid-sized Australian company, the order in which it is implemented, the governance required, and the typical pitfalls. By setting out the work in this way, we reflect the best practice for a sustainability officer starting from scratch, a CFO who has been asked to take charge of the ESG function, or an advisor helping a client navigate the process.

2. What an ESG Framework Actually Is and What It Is Not

More than policy documents

An ESG Policy Framework is not a file of policies stored in a network directory. It is a holistic approach that links the board’s oversight role to the organisation’s operations via governance arrangements, ESG Performance Metrics, and an ESG Implementation Roadmap that allocates accountability and monitors progress. The difference is that most organisations that have “ESG policies” without the overall governance and measurement framework soon find that their policies are unenforceable, unprovable, and ultimately a risk to reputation rather than a strength.

- ESG Strategy Development provides the purpose: the material issues, targets and integration with the business strategy.

- Sustainability Governance Model provides the governance: the roles and processes for board and management decisions and reporting.

- ESG Performance Metrics deliver the measurement: the key indicators used to measure progress against each material issue, measured annually.

- Implementation Roadmap ESG outlines the execution timeline for capability building, process integration, and compliance.

Why mid-sized companies need a different approach

Large entities can develop ESG capability with dedicated resources, long time frames, and companies’ and data management systems in place. Mid-sized companies’ ESG work needs to get there with fewer resources and in less time. The solution is not a watered-down version of the large-entity approach, but a more sequenced and pragmatic approach that prioritises building the essential elements and adds complexity as they are developed. A mid-sized company must first establish its governance model, then build its measurement and reporting capability.

3. Building the Governance and Strategy Foundation

Establishing the Sustainability Governance Model

Before collecting data or developing policies, the organisation must establish a governance model that assigns ESG responsibility at all levels. This does not mean a mid-sized firm needs a dedicated sustainability committee. Still, it does need clarity at the board level, a management owner, and a process for reporting ESG risks and opportunities to the board.

- Designate a board owner of ESG (either a dedicated committee or through the audit and risk committee, with terms of reference that cover ESG).

- Assign a management owner (often the CFO, COO or sustainability manager) who has access to the executive team and reports to the board.

- Set up an inter-functional working group with representatives from finance, operations, human resources, legal and communications (ESG is not a finance-only initiative).

Connecting ESG Strategy Development to business strategy

Other business priorities will always trump a stand-alone ESG Integration Strategy. The most sustainable frameworks link ESG goals to the business’s value drivers – the supply chain, the ability to attract and retain talent, customer needs, and capital. When the board and executive see ESG in this way, the cost of investing in an ESG framework is justified as a business investment, not a cost centre.

Corporate Sustainability Planning at this point should result in a written ESG strategy development document that captures the two to four ESG priorities most relevant to the business, why they are important to business success, the three-to five-year ambition for each, and board approval. This document will guide all ESG governance, measurement and reporting decisions.

Governance Element | What It Requires | |

Board mandate | Explicit board resolution or committee terms of reference assigning oversight of Risk and Compliance, ESG and sustainability performance | No formal mandate; ESG is discussed at the board level informally but never formalised in governance documents |

Management ownership | Named individual with clear accountabilities, budget, and direct access to the board or a board committee | ESG responsibility spread across multiple functions with no single owner; no budget allocated; sustainability sits below the executive line |

Cross-functional working group | Representatives from finance, operations, HR, legal, and communications meet on a regular cadence to progress ESG Framework Design deliverables | Working group formed but meets irregularly; no terms of reference; no connection between working group outputs and board reporting |

Reporting mechanism | Regular (quarterly minimum) board reporting on ESG Performance Metrics, risks, and Implementation Roadmap ESG progress | ESG is reported to the board annually as part of the sustainability report; no in-year performance reporting; the board has no visibility of progress between reporting cycles |

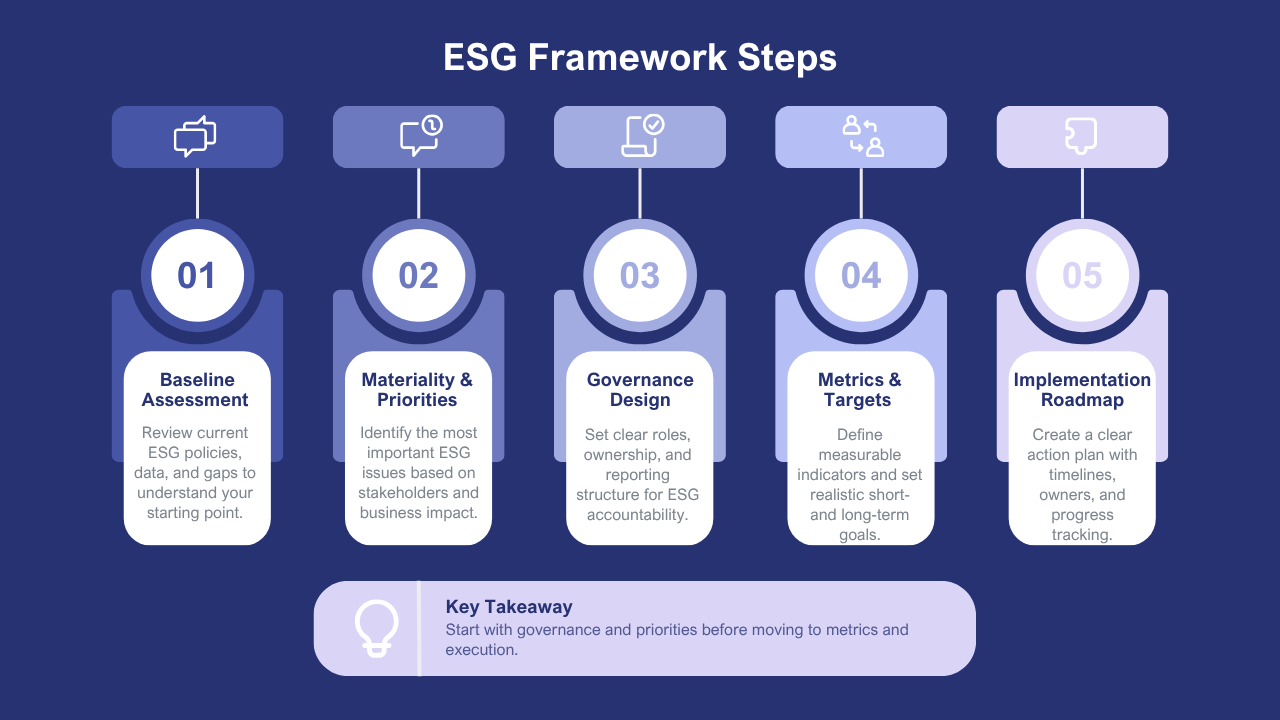

4. Five Steps to Build an ESG Framework That Works

There is a specific sequence for designing a functional ESG Framework for a mid-sized company. A common source of ESG frameworks that are good on paper but ineffective in practice is skipping steps or doing them in the wrong order. The five steps outlined below are the steps experienced professionals follow.

Step | What It Involves | Key Output | Sequencing Note |

1. Baseline assessment | Audit current state: what ESG policies exist, what data is already collected, what commitments have been made publicly, and where the governance gaps are. Identify the ESG risk and compliance obligations applicable to the business now and over the next two years. | Current-state gap analysis; compliance obligation register; inventory of existing commitments | Must come first — without a baseline, the ESG Strategy Development process lacks a foundation and risks duplicating or contradicting existing commitments |

2. Materiality and priority setting | Engage key stakeholders (board, management, customers, investors) to identify the ESG issues most material to the business. Distinguish between regulatory requirements (non-negotiable) and strategic priorities (where the business chooses to lead). | Materiality matrix; prioritised ESG topic list validated by the board | Informs every subsequent step — materiality determines which metrics to collect, which policies to develop, and what targets to set |

3. Design the Sustainability Governance Model | Formalise the governance structure: board mandate, management ownership, cross-functional working group, reporting cadence. Draft or update the ESG Policy Framework documents for each material topic. | Governance charter; updated board committee terms of reference; ESG Policy Framework document suite | Governance before metrics — the most common mistake is to invest in measurement before accountability structures are in place to act on what is measured |

4. Set ESG Performance Metrics and targets | For each material topic, define the specific metrics that will track performance, the baseline figure for the current year, and the targets for the next one, three, and five years. Align targets to the ESG Integration Strategy and, where applicable, to science-based or industry benchmarks. | Metrics register; target schedule; data collection methodology for each metric | Metrics should be set after governance is established — metric selection without accountability is data collection without purpose |

5. Build the Implementation Roadmap ESG | Translate the strategy and targets into a sequenced action plan with owners, timelines, and resource requirements. Identify the capability gaps to be addressed in year one vs. years two to three. Build in review points aligned with the board reporting cadence. | Twelve-month action plan; three-year Corporate Sustainability Planning roadmap; progress review schedule | The roadmap is a living document — it should be reviewed quarterly by the ESG management owner and presented to the board annually alongside the sustainability report. |

In Step 4, setting ESG Performance Metrics and targets, organisations face their most practical limitation: they lack a baseline for the Metrics they want to measure. The solution is to start collecting data for the current year in the framework built and to set targets at year-end. Trying to set targets when we don’t have a baseline leads to untestable and unmeasurable commitments, a key indicator of a poorly developed ESG Framework Design.

5. Process, Challenges, and Real Cases

The Implementation Roadmap ESG in Practice

For a medium-sized enterprise, the typical time frame of the Implementation Roadmap ESG is 12-18 months for the initial build and 2-3 years for full maturity. The phased approach below is how senior practitioners would manage the work.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Foundation (Months 1–3) | Framework Build (Months 3–6) | Measurement & Targets (Months 6–12) | Reporting & Maturity (Year 2+) |

Baseline assessment; governance mandate; materiality engagement; ESG Strategy Development document drafted and approved; compliance obligation register established | Sustainability Governance Model formalised; ESG Policy Framework documents drafted; ESG Performance Metrics defined; data collection for base year commenced | First full year of ESG Performance Metrics data collected; targets set against base year; Implementation Roadmap ESG progress reviewed quarterly; ESG Integration Strategy embedded in business planning | First Corporate Sustainability Report prepared; assurance engaged; Risk and Compliance ESG obligations met; annual review cycle established; framework refined based on first-year learnings |

Case 1: Governance before metrics

A medium-sized industrial services firm began its ESG Framework Design by investing in measuring emissions and sustainability metrics, then set up governance. After the first year, the company had a year’s worth of quality data, but no Board direction on what to do with it, no approved targets, and no ESG reporting to the executive team. The data sat unused. When an important customer asked for a questionnaire on the company’s sustainability data, it could not be completed because the metrics lacked a formal commitment and accountability framework. It took another six months to rebuild from governance to the framework. The lesson: Sustainability Governance Model, then measurement

Case 2: Materiality anchoring the strategy

This professional services firm engaged 80 employees, 20 clients, and 10 investors in a six-week materiality assessment as the first step in its ESG Strategy Development. The firm identified the most material topics as talent attraction and retention, client data privacy, and supply chain labour standards – none of which were included on the draft list prepared by managers. The firm then focused its entire ESG Policy Framework on these topics, including budget and executive support. Sixteen months later, the firm’s employee engagement score had improved substantially, and two institutional clients gave the sustainability strategy as a reason for renewing the contract. The materiality assessment had shifted focus from where the firm thought it was important to where stakeholders thought it was.

Common challenges and how to address them

Challenge | Why It Occurs | Practical Resolution |

ESG seen as a cost, not an investment | Board and executives view ESG Framework Design as compliance overhead; the commercial connection is not articulated. | Map each ESG priority to a specific commercial value driver: talent retention costs, customer contract requirements, financing conditions, or risk reduction. Present the business case in financial terms. |

No internal data capability | ESG Performance Metrics cannot be collected because systems are not configured to capture non-financial data | Start with the metrics that can be measured from existing data (energy bills, HR records, waste invoices); build system capability progressively rather than waiting for perfect infrastructure before starting |

Framework paralysis | The organisation tries to address all ESG topics simultaneously; progress stalls because the scope is unmanageable | Use materiality to ruthlessly prioritise two to four topics for year one; explicitly defer lower-priority topics to the Implementation Roadmap ESG for years two and three |

Targets without baselines | Pressure to announce targets before the first year of data is collected | Set directional commitments (“we will measure and disclose”) in year one; set quantified targets in year two once a reliable base year is established |

6. Conclusion

The ESG Framework Design for a mid-sized Australian company should be developed in four steps: governance, materiality, metrics and reporting. Doing it in the wrong order is the #1 cause of failure. Those companies that best manage this process are those that link ESG Strategy Development Integration to business value from the start, build the accountability framework before the measurement framework, and recognise that an Implementation Roadmap ESG is a tool, not a plan.

Three practical tips for starting: ask for an assessment before writing a policy; ask external stakeholders for feedback during the materiality process before choosing priorities; and build the governance structure before building the measurement systems. Australian businesses in 2026 will thrive on the commercial and regulatory advantages of capability building, and perish on the rocks of paper generation.

Frequently Asked Questions

Q1. What is an ESG framework?

An ESG framework provides a structured approach for managing environmental, social, and governance priorities across an organisation.

Q2. Why is an ESG framework important?

It helps businesses identify sustainability priorities, manage risks, improve governance, and align operations with stakeholder expectations.

Q3. What are the key components of an ESG framework?

An effective framework typically includes governance structures, environmental objectives, social initiatives, performance metrics, reporting processes, and continuous improvement plans.

Q4. Which businesses benefit from ESG framework design?

Organisations of all sizes seeking stronger sustainability performance, regulatory compliance, and long-term value creation benefit from ESG frameworks.

Q5. How does ESG framework design support business success?

A well-designed framework strengthens decision-making, improves accountability, enhances reporting quality, and supports sustainable growth.

1 thought on “ESG Framework Design: A Practical Guide for Mid-Sized Australian Companies”