Table of Content

1. Introduction: Purchase Price Allocation

Any business acquisition at a price exceeding the fair value of identifiable net assets triggers an accounting requirement that most buyers do not fully expect until they are in the middle of it: the Acquisition Accounting PPA process, technically known as Purchase Price Allocation. Under AASB 3 (the Australian equivalent of IFRS 3), the acquirer is required to apportion the total purchase consideration among all the assets acquired and liabilities taken, at the acquisition-date fair value. The most difficult and material aspect of this exercise is the identification and valuation of PPA Intangible Assets – assets that generally do not appear on the seller’s balance sheet, yet must be recognised separately from goodwill if they meet the recognition criteria of the standard.

The stakes are high either way. The under-identification of PPA Intangible Assets inflates the Calculation of Goodwill and understates the amortisable intangible base, reducing the annual amortisation charges flowing through the income statement but creating a larger, more vulnerable goodwill balance that will be subjected to annual impairment testing. Over-identification or inappropriate Fair Value Allocation results in amortisation charges that reduce reported earnings over the years, affect debt covenant calculations, and trigger audit scrutiny that can be not only costly but also disruptive. It takes a combination of technical knowledge and business acumen to get the Purchase Price Split correct.

This paper explains the implications of PPA Intangible Assets on the general Purchase Price Split, why the Intangible Recognition Process is important to everyone, from the CFO to the external auditor, and what practitioners entering the corporate finance and M&A accounting environment need to know about the Valuation of Intangibles in a post-acquisition setting. The structures and teachings here reflect both the technical needs of IFRS 3 Compliance and the realities of how this is done.

2. The PPA Framework and How Intangibles Fit Within It

How the Purchase Price Split is structured

The Purchase Price Split starts with the amount of consideration paid, upfront cash, deferred consideration, contingent payments (earnouts measured at fair value at the acquisition date), and any equity instruments issued. The latter is then divided into: tangible assets and financial instruments at fair value; Identifiable Asset Valuation of separately recognisable intangibles; liabilities assumed at fair value; and the residual – Goodwill Calculation – which includes everything that cannot be separately identified.

- Identifiable Asset Valuation of intangibles is not optional, but a requirement of any intangible asset that satisfies the AASB 3 separability criteria (can be separated and sold, licensed, or transferred) or the contractual-legal-requirement (arises out of contractual or legal rights).

- The Goodwill Calculation is a residual: it declines as more intangibles are recognised and valued. A strict Intangible Recognition Process results in reduced goodwill and increased amortisable intangible balances.

- The IFRS 3 Compliance means that the measurement period – the period during which the PPA will be finalised – should close within 12 months of the date of acquisition. Provisional values can be made during that time, but no material revisions can be made after it is closed.

Why PPA Intangible Assets require specialist involvement

The Valuation of Intangibles in a PPA setting is technically different from business valuation in general. Each intangible category has a suitable methodology that should be used consistently with the assumptions of market participants, not with the specific post-acquisition plans of the acquirer. Market data, industry standards, and documented assumptions that most corporate finance teams do not maintain as standard are required for the relief-from-royalty method for brand names, the Multi-Period Excess Earnings Method (MEEM) for customer relations, and the income method for patented technology. That is why material PPA exercises are conducted using the services of specialist intangible valuers – and why their reports are the main source to be audited.

3. The Intangible Categories and How They Are Valued

Common PPA Intangible Assets and their Fair Value Allocation approaches

The Intangible Recognition Process under AASB 3 is extensive in scope. The standard specifically identifies five categories of intangible assets that are to be determined in any business combination: marketing-related (brands, trademarks), customer-related (customer lists, relationships, contracts), artistic-related (copyrights), contract-based (licences, franchises, non-compete agreements), and technology-related (patents, software, trade secrets). In practice, customer relationships, brand names, and technology platforms are the most widespread and material categories in Australian private M&A transactions.

PPA Intangible Assets Category | Valuation of Intangibles Method | Typical Useful Life | Post-Acquisition Reporting Impact |

Customer relationships | Multi-Period Excess Earnings Method (MEEM): isolates earnings attributable to the customer base after contributory asset charges for all other assets | 5–12 years based on attrition analysis | Annual amortisation reduces reported EBIT; the customer attrition assumption is the most contested input |

Brand names/trademarks | Relief-from-royalty: present value of royalties avoided by owning the brand, based on comparable licensing rates | Finite (5–15 years) or indefinite, where the brand is assessed as durable; indefinite life brands require an annual impairment test rather than amortisation | Amortisation is finite; the annual impairment test is indefinite; the auditor will challenge the finite/indefinite judgment |

Technology / proprietary software | Relief-from-royalty (where comparable rates exist) or cost-to-recreate adjusted for functional and economic obsolescence | 3–7 years reflecting the technology cycle and competitive obsolescence | Annual amortisation is typically significant relative to carrying value; there is an accelerated obsolescence risk if technology evolves rapidly |

Non-compete agreements | Income approach: probability-weighted loss if former management competed, discounted over the agreement term | Equal to contractual term (typically 2–5 years) | Fully amortised over contract life; relatively straightforward audit treatment once fair value is established |

Order backlog | The direct income approach is applied to specific contracted revenue at the acquisition date. | Short (6–18 months); represents backlog duration only | Rapid amortisation in months following acquisition; material to revenue recognition disclosure in the first post-acquisition period |

At any rate, Fair Value Allocation of customer relationships continues to be the source of the greatest audit scrutiny, as the assumption of an attrition rate is both the most influential input and the most subjective. Auditors would expect the attrition assumption to be based on three or five years of historical customer-level data, expressed not as a simple count of accounts but as a revenue-weighted annual attrition rate. In cases of missing or inconsistent historical data, analysts need to apply sector benchmarks, which auditors will evaluate for comparability. Developing a plausible, historically substantiated attrition schedule before the measurement period expires is one of the most crucial practical steps in conducting a defensible Acquisition Accounting PPA exercise.

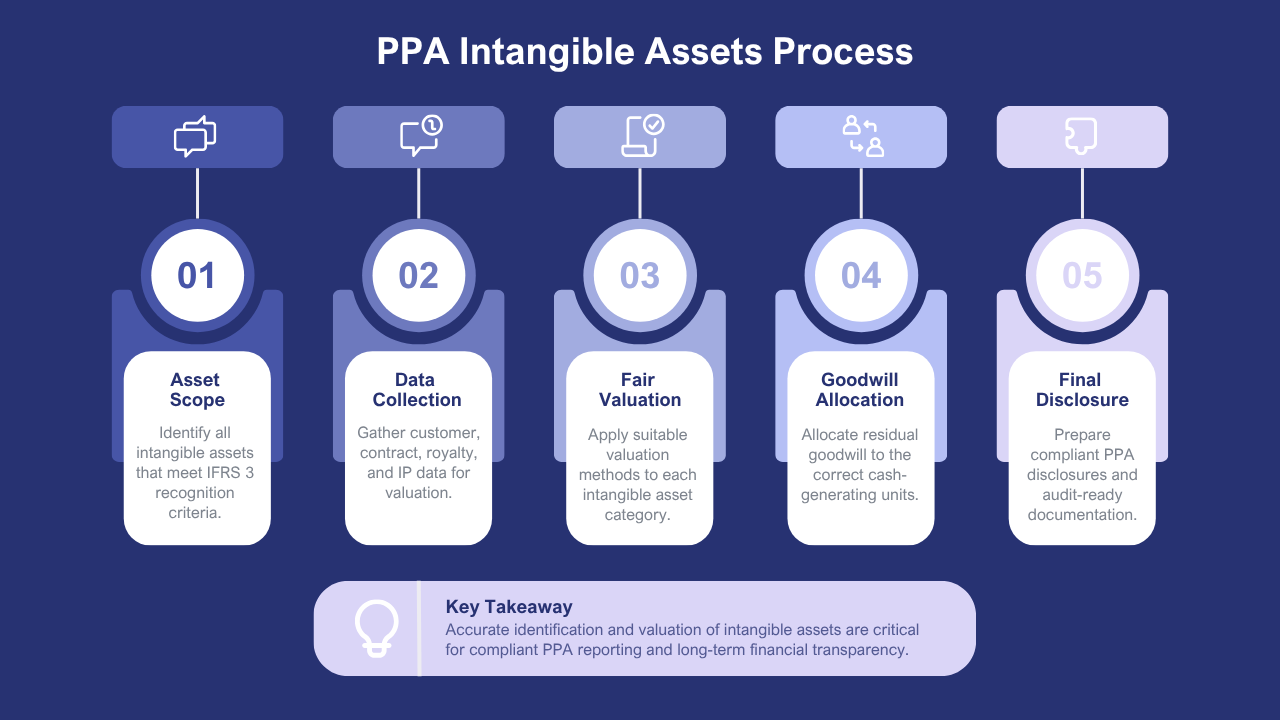

4. Five Key Steps in the PPA Intangible Asset Process

An effective Acquisition Accounting PPA has a structured series of steps. The following five steps outline how seasoned practitioners would approach the exercise to deal with the finalised financial statements that are in compliance with IFRS 3 Compliance requirements.

Step | What It Involves | IFRS 3 Compliance Requirement | Common Failure Mode |

1. Scope the PPA Intangible Assets universe | Apply the separability and contractual-legal criteria to every potential intangible category in the acquired business; use sector benchmarks to identify what types of intangibles are typically present in comparable acquisitions | All identifiable intangibles meeting AASB 3 criteria must be recognised; failure to scope comprehensively is the primary source of audit challenge and restatement risk | Scoping only the obvious intangibles (brand, registered patents) without examining the full AASB 3 category list, and not benchmarking against sector comparables to identify what auditors will expect |

2. Collect and organise data for Identifiable Asset Valuation | Gather three-to-five years of customer-level revenue data for MEEM; source comparable royalty rates for brand and technology; obtain IP registration documentation; compile contract schedules for backlog | Identifiable Asset Valuation requires market participant data, not just internal management estimates; assumptions must be observable or derived from market evidence | Relying on management estimates without independent market benchmarks, data gaps in customer records that undermine the attrition analysis |

3. Apply Fair Value Allocation methodologies | Engage specialist valuers to apply the appropriate methodology for each identified intangible; document all assumptions, sensitivity analyses, and data sources; model deferred tax on all fair value step-ups | Each methodology must use market participant assumptions; the Valuation of Intangibles must reflect what a willing buyer and willing seller would agree, not the acquirer’s specific synergy expectations | Using acquirer-specific synergy assumptions rather than market participant assumptions, incomplete sensitivity analysis leaves the valuation vulnerable to challenge |

4. Calculate the Goodwill Calculation and allocate to CGUs | Subtract the sum of all identified net assets (tangible and intangible at fair value) from total consideration; allocate goodwill to cash-generating units (CGUs) aligned with management’s internal reporting structure | Goodwill Calculation residual must be allocated to CGUs for annual AASB 136 impairment testing; CGU allocation must reflect how management monitors the business | Treating CGU allocation as an afterthought; CGU structure not aligned with operational reality; goodwill concentrated in a single CGU, creating a fragile impairment position |

5. Finalise disclosures for Post-Acquisition Reporting | Prepare AASB 3 acquisition note disclosures covering each class of intangible, the methodology used, the significant assumptions, and the sensitivity of the fair value to those assumptions | Post-Acquisition Reporting disclosures are mandatory and audited; they must be specific to the acquisition, not generic boilerplate | Generic disclosures without transaction-specific detail; not engaging the auditor during the measurement period; material errors discovered after the measurement period closes, requiring restatement |

The step with the most protracted continuing ramifications of any choice in the PPA process is allocating the Goodwill Calculation to cash-generating units. The framework for all annual impairment tests to be reported under AASB 136 at the point in time when goodwill is on the balance sheet is determined by the CGU structure established at the time of acquisition. When a CGU structure is not reflective of how the management actually monitors and manages the business, it creates two risks: the impairment test is conducted at a level of aggregation that is not reflective of how the management actually monitors and manages the business; or the test produces anomalous results because the carrying value of the CGU reflects the value of assets that are generating returns at a different rate than the goodwill allocated to it. The time to thoughtfully design the CGU structure, including the operations team, not just the finance function, is a once-in-a-lifetime investment that pays dividends in audit efficiency over the years.

5. Process, Real Cases, and Lessons for Practitioners

The Acquisition Accounting PPA workflow in practice

The workflow of the Acquisition Accounting PPA process starts at deal close and runs through four phases. This is a realistic preparation for any practitioner in a post-merger accounting, audit, or advisory role.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Deal Close & Scoping | Fair Value Assessment | Goodwill & CGU Allocation | Audit Support & Disclosure |

Confirm acquisition date and total consideration; scope PPA Intangible Assets by sector; brief specialist valuers; establish provisional Purchase Price Split; confirm measurement period milestones with audit team | Apply Fair Value Allocation methods to tangible assets, Identifiable Asset Valuation for intangibles, and liabilities; model deferred tax on step-ups; build sensitivity analysis; document all assumptions | Calculate Goodwill Calculation residual; design CGU structure aligned with management reporting; allocate goodwill to CGUs; establish AASB 136 impairment testing framework for Post-Acquisition Reporting | Respond to auditor queries on methodology and data sources; finalise Acquisition Accounting PPA within measurement period; prepare AASB 3 and IFRS 3 Compliance disclosures; file final accounting entries |

Case 1: The cost of an insufficient Intangible Recognition Process

It acquired a healthcare services company at a high premium based on the quality of the contracted patient relationships and the proprietary clinical protocols it had developed. The internal finance team of the acquirer completed the first PPA without specialist valuation advice, with the majority of the premium being recognised as goodwill and only a small customer relationship intangible is recognised. When the external auditor reviewed the Acquisition Accounting PPA, they understood that the clinical protocols – which met the AASB 3 separability criterion and were the primary source of the business’s competitive advantage – had not been separately recognised. The unrecognised technology intangible fair value overstated the Goodwill Calculation. The measurement period was closed. It needed restatement, along with the extra specialist valuation fees, longer audit time, and corrections to the previous disclosures of the acquisition note. The lesson: full scoping of the PPA Intangible Assets at the beginning of the measurement period is categorically less costly than doing it afterwards.

Case 2: IFRS 3 Compliance and the Competing Interests in the Purchase Price Split

A consumer goods company bought a premium brand. The management team of the acquirer was preoccupied with minimising amortisation charges that would reduce reported earnings during the post-acquisition period and had a structural preference for allocating as much of the premium as possible to indefinite-life goodwill rather than to finite-life amortisable intangibles. The specialist valuer engaged to support the Valuation of Intangibles prepared an independent brand valuation using the relief-from-royalty method and identified a separately recognisable brand intangible with a finite useful life of 12 years. The auditors of the acquirer, who had access to the specialist report, required the brand intangible to be recognised at its fair value assessed, and not subsumed within goodwill. The annual amortisation cost was about 420,000 and had not been included in the management team’s post-acquisition earnings estimates. The outcome of IFRS 3 Compliance was accurate; however, the cost of the oversight of planning was high. The moral: simulate the effects of amortisation of a realistic PPA Intangible Assets scope before the acquisition, not after.

6. Conclusion

Some of the most technically challenging and commercially significant aspects of post-acquisition accounting are PPA Intangible Assets. The Intangible Recognition Process required by IFRS 3 Compliance is comprehensive; the methodologies for Valuation of Intangibles are specialised; and the Goodwill Calculation, resulting from an intensive Fair Value Allocation, has long-term implications for annual impairment testing, reported earnings, and the transparency of Post-Acquisition Reporting disclosures. Businesses that navigate this process most effectively are those that seek expert support early, map the universe of PPA Intangible Assets by sector, and design the CGU structure at the time of acquisition rather than retrofit it later.

For practitioners venturing into the M&A accounting and advisory arena, the PPA process is one of the most illustrative examples of how accounting standards integrate commercial transactions into financial statements. The basic understanding of the Purchase Price Split, which drives the allocation between identifiable intangibles and residual goodwill, why the Acquisition Accounting PPA has continuing earnings implications, and what IFRS 3 Compliance specifically requires, in particular, is fundamental knowledge that applies to all post-acquisition reporting situations. Develop this ability early: it is technically challenging and in high demand.

Frequently Asked Questions

Q1. Why are intangible assets important in Purchase Price Allocation (PPA)?

PPA requires identifiable intangible assets to be recognised separately from goodwill at their fair values after a business acquisition.

Q2. Which intangible assets are commonly recognised in PPA?

Customer relationships, trademarks, patents, software, licences, technology, and non-compete agreements are commonly identified during PPA.

Q3. Why is accurate valuation important in PPA?

Accurate valuation supports compliance with accounting standards and improves the reliability of post-acquisition financial statements.

Q4. Who requires PPA valuation services?

Acquiring companies, accountants, auditors, finance teams, and valuation professionals commonly require PPA valuations.

Q5. How does professional valuation support acquisition accounting?

Professional valuers identify intangible assets, apply recognised valuation methodologies, and provide reliable fair value measurements for financial reporting.

1 thought on “How Intangible Assets Affect Purchase Price Allocation (PPA)”