Table of Content

1. Introduction: Strong Brands and Recurring Customers

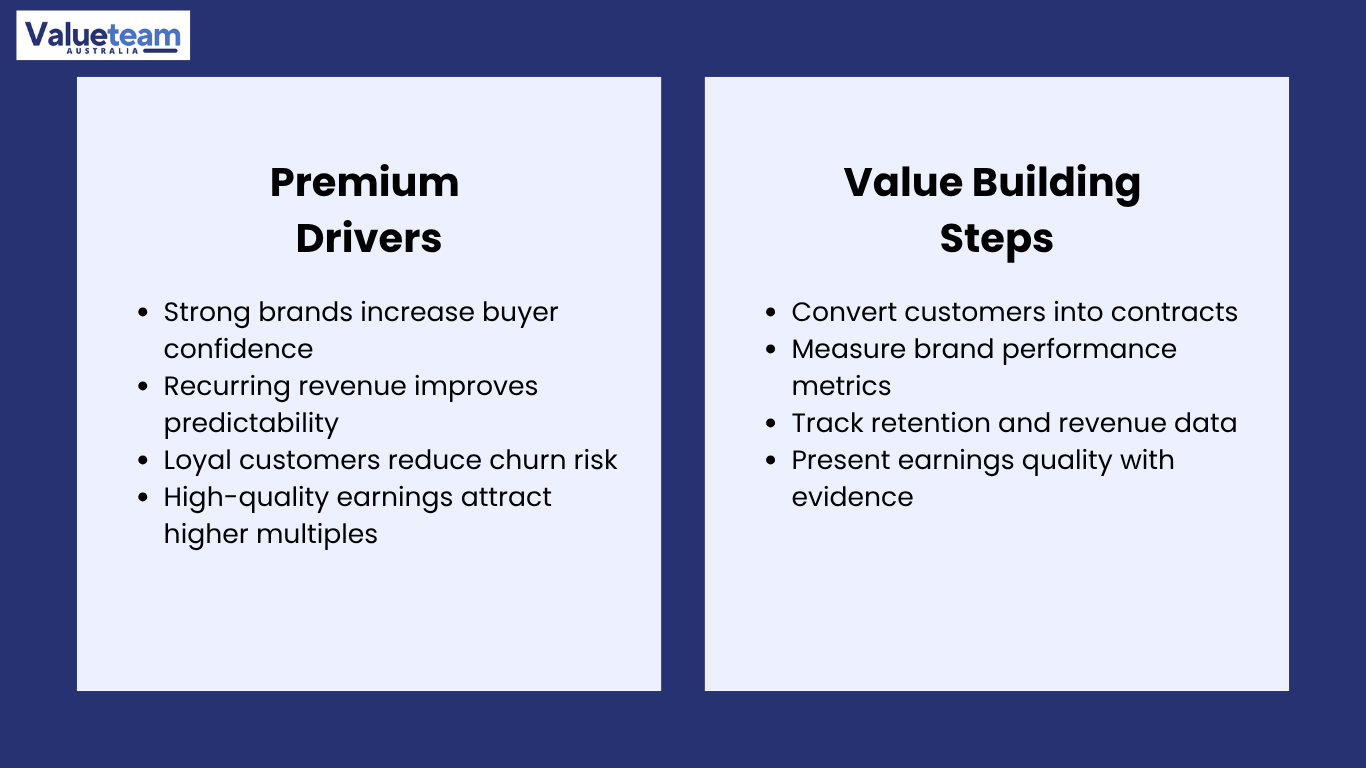

When the question is posed to experienced M&A practitioners about what they seek first in a target business, the answers can be divided into two themes: the strength of the brand and the quality of the customer base. These are not some mushy considerations that will be made after the financial analysis is well done – they are key determinants of the valuation multiple a business will attract. The combination of Brand Premium Value and Recurring Revenue Importance explains why two businesses with the same EBITDA can sell at dramatically different multiples, and why buyers will always pay more for predictability than for the absolute size of earnings.

The business rationale is very simple. Buying a business is buying a future stream of earnings. The multiplier a buyer puts in is actually a gamble on how sure they are that those incomes will be sustained. A business with a strong, trusted brand and a loyal, contracted customer base provides much greater assurance of continuity than one that relies on constant new customer acquisition, undifferentiated positioning, and transactional relationships. Stable, recurring, and defensible High-Quality Earnings that are both stable, recurring and defensible are more valuable, in any market, and of any size, than volatile earnings of the same or greater absolute magnitude.

This article explains why Brand Premium Value and Recurring Revenue Importance are directly proportional to transaction multiples, how buyers evaluate and quantify these attributes, and what business owners and advisors should do to build and document them before going to market. These frameworks can be applied across sectors and business sizes, and lessons learned in practice can be used to apply them to the challenge.

2. The Commercial Logic Behind Valuation Premiums

Why Predictable Cash Flow commands a higher multiple

A buyer who buys a business whose revenue is generated by active selling effort every month is underwriting a fundamentally different risk profile than a buyer who buys a business whose revenue is generated by active selling effort every month. Foreseeable Cash Flow lowers the discount rate used in any income-based valuation, increases the buyer’s confidence in the acquisition model’s assumptions, and reduces the amount of capital and management investment required after the acquisition to support the earnings base. All these are, separately and individually, valid reasons why a higher multiple should be used; however, together they explain why the spread between high- and low-multiple businesses operating in the same industry might be as wide as three or four turns of EBITDA.

- Revenue Stability Premium: buyers are paying an explicit price based on the difference between contracted recurring revenue and transactional revenue; a business with 60%+ recurring revenue is likely to attract a multiple premium of 0.5x to 1.5x above an equivalent earnings business whose revenue is primarily project-based.

- Increasing the discount rate with greater revenue predictability reflects the fact that the more predictable the revenue, the lower the discount rate used in a DCF or risk-adjusted return analysis should be.

Brand Strength Metrics and the competitive moat premium

A good brand is not just a marketing tool – it is a competitive advantage. Brand Strength Metrics, such as unprompted awareness, Net Promoter Score, and the cost of customer acquisition and retention versus unbranded alternatives, all speak to the same underlying commercial fact: the brand lowers the cost of acquiring and retaining customers. To buyers, this directly translates into a reduced risk assessment of the post-acquisition income foundation. A business to which the customers will actively go out to, as opposed to one that competes on price in a commodity market.

3. Recurring Revenue and Customer Loyalty as Value Drivers

How Customer Retention Value accumulates over time

Customer Retention Value: The total economic value of customers who will remain part of the business over a period of time. The cost of serving a customer they have retained declines each year they retain them, and their contribution to the bottom line increases (cross-sell, price increases, increased product engagement). The outcome is a customer relationship that gets more profitable over time – and a customer base that is truly more than the amount of its annual contribution to the bottom line.

- Impact of customer Loyalty on the economics of acquisition: a business with a 95 per cent retention rate loses 5 per cent of its customer base per year; a business with an 80 per cent retention rate loses 20 per cent of its customer base per year to maintain the same customer base revenue.

- Subscription Business Model features – predictable annual or monthly revenue, auto-renewal mechanisms, and high switching costs are the structural mechanisms that entrap retention and create the Predictable Cash Flow, which buyers pay a premium to obtain.

High-Quality Earnings vs. High-Volume Earnings

One of the most significant analytical models in M&A valuation is the difference between High-Quality Earnings and high-volume earnings. Two businesses can produce the same EBITDA: one is based on a diversified, contracted, long-tenure customer base with minimal churn; the other on a large volume of small, transactional customers with high churn and the need to actively sell to them. There is High-Quality Earnings in the first business; high-volume earnings in the second business. Buyers who recognise this difference will pay radically different multiples on each, although the headline profit will be equal.

Revenue Characteristic | Buyer’s Risk Assessment | Valuation Premium Drivers Effect | Example Premium |

Contracted multi-year agreements, auto-renewal, 95%+ retention | Very low churn risk; Predictable Cash Flow highly confidence-inspiring; minimal post-acquisition sales investment required | Revenue Stability Premium applied; multiple premium of 1.0–1.5x above sector average | Subscription Business Model tech company at 8–10x EBITDA vs. 4–5x for non-recurring peer |

Informal recurring relationships, no contracts, 80–85% retention | Moderate risk; renewal depends on relationship management quality; post-acquisition risk if seller is the relationship holder | Partial Customer Retention Value credit; premium applied but discounted for informality | Mid-market services business at 4.5x vs. contracted peer at 6x |

Primarily transactional, low repeat rate, high volume | High: constant new customer acquisition required; revenue does not compound; earnings quality is lowest | No recurring revenue premium; standard or below-average multiple applied | Distribution business at 3–4x EBITDA regardless of absolute earnings size |

Mixed: 40% contracted, 60% transactional, growing contracted proportion | Moderate and improving: trajectory matters; buyer will ask why conversion is slow and whether it is sustainable | Partial premium reflecting trajectory; buyer may propose earnout if growth in contracted proportion continues | Professional services at 5x with earnout to 6x if contracted revenue reaches 65% within 24 months |

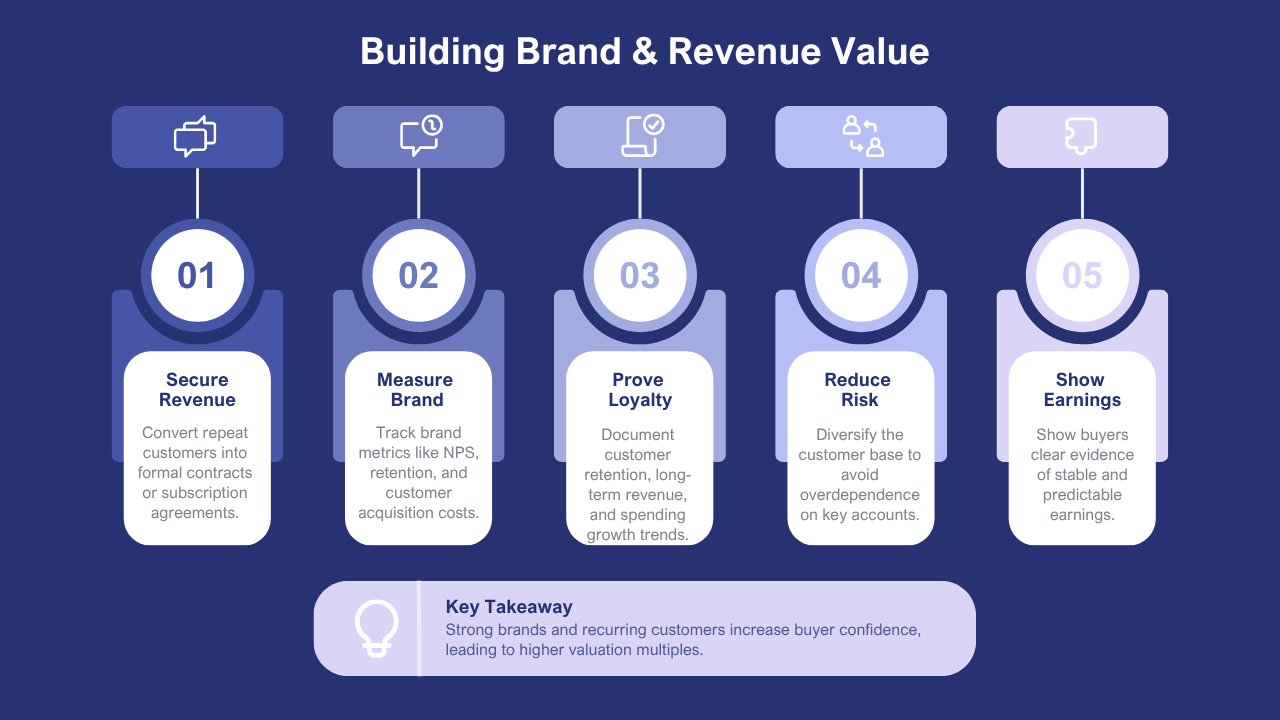

4. Five Steps to Build and Evidence Premium-Worthy Characteristics

Drivers of Valuation Premiums are developed over the long term as a result of conscious commercial and operational investment. The following five steps are the highest-return actions business owners can take before entering the market to create genuine Brand Premium Value and Recurring Revenue Importance.

Step | What It Involves | Multiple Impact | Timeframe |

1. Convert informal customer relationships to a Subscription Business Model or formal contracts | Identify the customers with informal recurring relationships and convert to annual or multi-year agreements; implement auto-renewal provisions; document switching costs | Converts partial Customer Retention Value credit into full credit; reduces buyer’s perceived churn risk; directly supports a higher Revenue Stability Premium | 6–18 months; must begin early enough to generate at least one full year of contract-based revenue |

2. Measure and document Brand Strength Metrics | Commission NPS research; compile unprompted awareness data; calculate pricing premium over unbranded alternatives; document customer acquisition cost trends over time | Converts qualitative brand claims into verifiable evidence; buyers who can independently assess Brand Premium Value are more confident paying for it | 3–6 months; research commission and data compilation |

3. Build the Customer Retention Value data record | Compile three years of customer-level revenue data showing retention, tenure distribution, and spend growth; calculate cohort-level retention rates; prepare a formatted retention schedule | The attrition assumption in any customer relationship valuation is the most contested input; documented historical retention data neutralises the buyer’s ability to apply conservative assumptions | Ongoing: requires a customer data system; 12 months of formatted records is the minimum useful preparation |

4. Reduce Customer Loyalty Impact concentration risk | Where any customer exceeds 15–20% of total revenue, develop and execute a diversification plan; add new customer segments; deepen relationships with mid-tier accounts | Removes the concentration discount buyers apply; enables the Customer Retention Value to be fully valued rather than discounted for key customer departure risk | 12–18 months; diversification requires deliberate new customer investment, and results take time to establish |

5. Present the High-Quality Earnings narrative with evidence | Prepare a revenue quality analysis segmenting earnings by contract type, customer tenure, and renewal pattern; connect each quality metric to a specific financial outcome; and integrate into the information memorandum | Frames the buyer’s assessment from the outset; buyers who receive a structured earnings quality analysis early in the process apply fewer conservative adjustments | 3–6 months before going to market; builds on all preceding data collection steps |

The action that has the greatest direct and measurable effect on the quality of earnings assessment of the buyer is Step 1, which is the conversion of informal relationships into formal agreements. An informal, recurring relationship is considered to contribute to the seller’s claimed normalised revenue, though the buyers provide a discount to compensate for the absence of contractual commitment. A signed multi-year contract eliminates that discount and transforms the relationship into a Predictable Cash Flow that buyers can model with confidence. The conversion dialogue with existing customers is nearly always simpler than the owners think: customers who have been returning already often welcome the formalisation as a mutual commitment rather than resisting it as an imposition.

5. Process, Real Cases, and Lessons for Practitioners

The premium-building workflow

The structured programme is called Building Brand Premium Value and Recurring Revenue Importance, and it operates in tandem with preparing to leave the company with money. The four-step workflow below represents how the experienced advisors can fit this work into the overall pre-sale preparation timeline.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Assessment & Baseline | Conversion Programme | Evidence Building | Sale Narrative |

Measure Brand Strength Metrics; compile Customer Retention Value data; segment revenue by type (contracted, informal recurring, transactional); identify the highest-return conversion and documentation opportunities | Implement Subscription Business Model conversions for top accounts; build NPS and brand measurement infrastructure; begin Customer Loyalty Impact documentation; address concentration risk | Compile 12+ months of contract-based Predictable Cash Flow evidence; prepare retention cohort analysis; document Brand Premium Value with independent research; build Revenue Stability Premium case | Prepare High-Quality Earnings analysis for information memorandum; integrate Brand Strength Metrics; present Valuation Premium Drivers case to buyers; defend recurring revenue position through due diligence |

Case 1: From transactional to recurring — a multiple transformation

The business was a managed IT services business that had been providing ongoing support to about 80 clients over several years with no formal service contracts. Revenue was very predictable in practice yet not in structure, as it was very informal. When the owner started a Subscription Business Model conversion programme 16 months before a planned exit, 62 of the 80 clients signed 12- to 24-month managed service agreements at fixed monthly rates. As the conversion continued, annual recurring revenue increased to about $1.4 million, almost zero at the start of the conversion. The Revenue Stability Premium that could be offered to a buyer when the business went to market could be demonstrated, documented, and verified against signed contracts. The last transaction multiple that it had was 1.4x of what an advisor had been estimating would be possible through the same business, with its original billing structure, representing an estimated additional sale value that could have been achieved using a conversion programme, which cost less than 20,000 in legal and advisory fees to implement.

Case 2: Brand Strength Metrics that changed the negotiation

A consumer services company had developed a well-known brand for over 11 years, which it had never formally measured. When the owner commissioned an NPS study and customer acquisition cost analysis as part of the sale preparation, the results were striking: NPS of 72 (significantly higher than the industry average), and customer acquisition cost of about 40 percent lower than the industry standard due to word-of-mouth referral driving most of the new customer acquisition. These two measurements, neither of which would have been reflected in any financial statement, were incorporated into the information memorandum as quantified Brand Premium Value evidence. As a strategic buyer challenged the multiple in the initial negotiation, the advisor to the seller was at liberty to respond with specific, independently gathered data demonstrating that the brand established a structural competitive cost advantage. The Brand Premium Value claim that had been negotiated, and the final price that was offered was a multiple at the upper end of the original range.

6. Conclusion

Strong brand names and repeat customers pay premiums because their characteristics reduce the risk of the investment they are making. Brand Premium Value creates a defensible competitive position that can sustain revenue without the perpetual need to reinvest. Recurring Revenue and Predictable Cash flow minimise the uncertainty in the earnings projections on which the acquisition price is based. Customer Loyalty Impact and Customer Retention Value reduce the investment required at the post-acquisition stage to ensure the business remains operational. Collectively, these Valuation Premium Drivers explain why High-Quality Earnings will always command higher multiples than equivalent-volume earnings with weaker commercial foundations.

To business owners: the cost to create these features – converting informal relationships to formal agreements, measuring brand strength, documenting retention data – is nearly always paid back many times over in the ultimate price of the transaction. To advisors: The businesses that implement premium exits are those where the owners have grasped the commercial rationale of the Revenue Stability Premium and have acted on it with sufficient lead time to create the evidence buyers need. The premium is not awarded based on claim – it is won based on documentation, consistency and time.

Frequently Asked Questions

Q1. Why do buyers value recurring customers?

Recurring customers provide predictable revenue, improve cash flow stability, and reduce business risk, making the business more attractive to buyers.

Q2. How do recurring customers affect valuation?

Businesses with stable recurring revenue often receive higher valuations because they demonstrate sustainable future earnings.

Q3. Which industries commonly benefit from recurring revenue?

Software, subscription services, maintenance businesses, healthcare, and professional services frequently benefit from recurring customer relationships.

Q4. How can businesses strengthen recurring customer value?

Businesses can improve customer retention, service quality, long-term contracts, and subscription-based offerings.

Q5. Why is recurring revenue important during acquisitions?

Reliable recurring income provides buyers with greater confidence in future financial performance and long-term business sustainability.

1 thought on “Why Buyers Pay Premiums for Strong Brands and Recurring Customers”