The majority of business owners work several years – in some cases decades – to create something that will eventually be worth selling. But shockingly, many come to the exit table unprepared and end up with a lot of value in their hands simply because they failed to take the right cues early enough. Knowledge of what adds value to the sale of a business before exit is not the prerogative of an experienced M&A advisor or corporate financier. It is a pragmatic science that everyone involved in business valuation processes, business valuation strategy, and/or ownership can study and implement, irrespective of their position in the organisation.

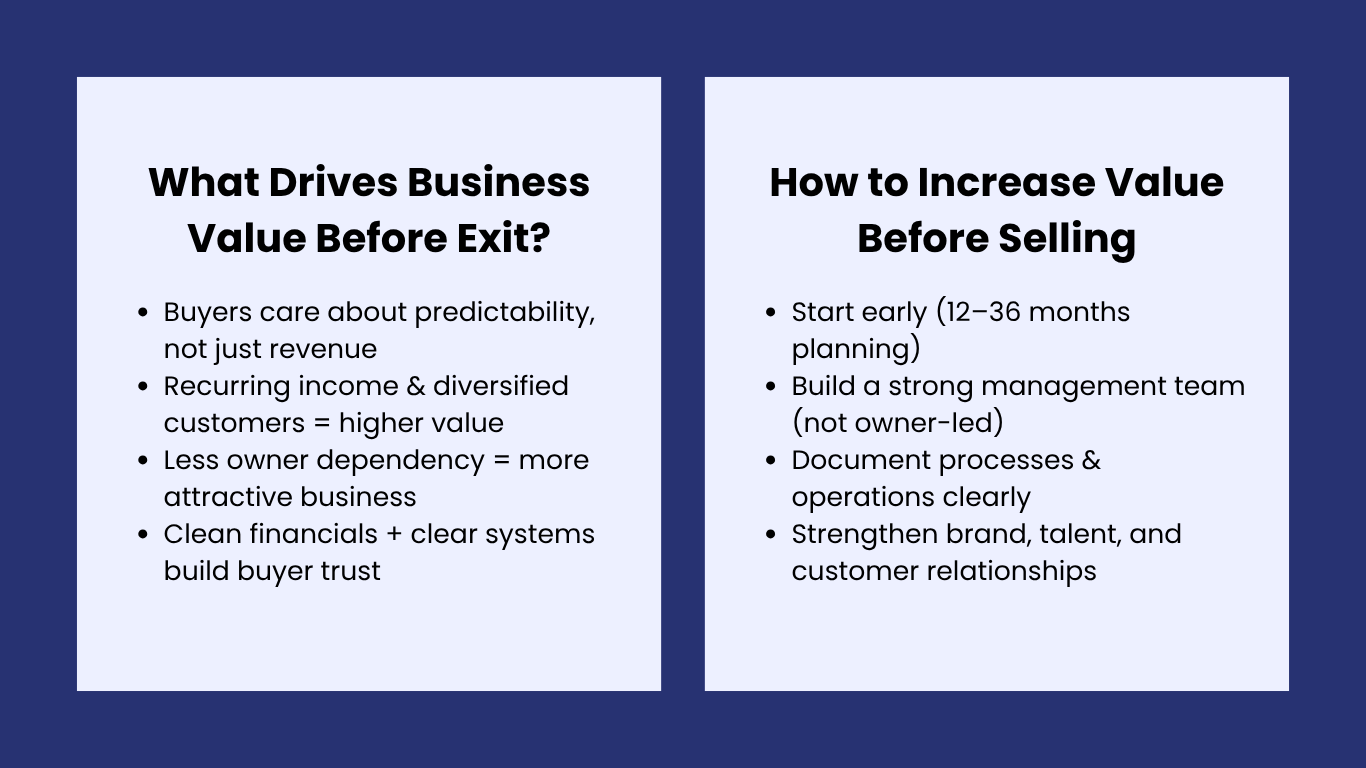

Stakes are high. Studies have consistently shown that consumers are willing to pay a premium for a business that exhibits predictability, clear structure, and justifiable growth. Sellers who take time to plan an exit (12-36 months before a deal) tend to see significant changes in their final business valuation multiple compared to those who make a decision and list within weeks. It is not a coincidence. It is pre-planning, and it starts with learning what buyers really consider when they peek under the hood.

Table of Content

1. Sale Value of a Business: Why Valuation Is Not Simply about Revenue

The belief that higher revenue automatically leads to higher sale prices is one of the most widespread myths professionals face when they first enter the M&A space. In practice, customers value businesses on the quality of earnings – a notion which looks outside the top line to determine the extent to which the income is sustainable, recurring and transposable. A company with 5 million dollars in revenue, low margins, a high concentration of customers, and a model that relies on its owner may have the same multiplier as a company with 3 million dollars in revenue, high margins, a varied clientele, and a leadership team that works.

It is here that the business-value-adding work starts, before selling, not in the financial statements themselves, but in the operational and business underpinning behind the figures. The buyers are purchasing the future and not the past. They desire a business valuation that will keep doing the job even when the founder takes a seat on the doorstep, and they value that in the number of multiples they are willing to pay. alks out the door, and they price that confidence into the multiple they are willing to apply.

TABLE 1 — REVENUE VS. VALUE: WHAT BUYERS ACTUALLY ASSESS

Factor | Low Value Signal | High Value Signal |

|---|---|---|

Revenue Quality | One-off, project-based income | Recurring, contracted revenue |

Customer Base | Top 3 customers = 70%+ of the money earned. | Diversified; none of the clients exceeding 15%. |

Owner Dependency | The owner does all the key relationships. | The team operates independently. |

Documentation | The activities of the head of a founder. | SOPs, systems, and playbooks in place |

Financial Reporting | Cash-basis, inconsistent records | Audited, accrual-basis financials |

2. The Five Drivers That Move the Needle in Earnest

In any industry, some of these levers always enhance the perception of that business to the acquirers and its price. They are not fast solutions. They are structural advantages that are time-consuming but compound returns for the business valuation when it enters the market. To enhance the business valuation before exit, it is important to focus on the following five drivers and ensure they are disciplined and learned early enough to be considered credible.

TABLE 2 — FIVE KEY VALUE DRIVERS BEFORE AN EXIT

# | Driver | What It Means in Practice |

|---|---|---|

1 | Recurring Revenue Architecture | Substitute transactional revenue with subscription or retainer-based revenue wherever feasible. Buyers will place higher multiples on a business whose revenue can be accurately predicted today. |

2 | Management Layer Independence | Develop a team of leaders who can manage the business without the owner present. Outsource important customer relationships and institutionalise knowledge. |

3 | Clean, Audited Financial Records | Professionalism is indicated by three years of audited or reviewed financial statements. The seller’s number is not at risk during negotiations, as clear records, such as the separation of personal and business expenses, are maintained. |

4 | Documented Operational Systems | A job is a business because of standard operating procedures, technology infrastructure and repeatable processes. A documented operation sells easily and smoothly and has a premium price. |

5 | Customer and Market Defensibility | Competitive moats based on strong brand positioning, IP, long-term contracts, and actual switching costs are minimising buyer risk and promoting high multiples. |

3. Real-World Practices: What the Preparation is Like in the Field

Take a European mid-sized software consultancy that had steadily increased to about 80 employees during a period of eight years. The business was performing well financially when the founder initially engaged an M&A advisor. 60 per cent of the revenue was attributed to two customers; the founder himself handled the biggest account, and none of the entities consistently reported their financials. The first indicative business valuation was lacking.

The founder chose 18 months of restructuring over entering the market at once. They employed a head of client delivery, diversified the client base through focused business valuation development, streamlined the entity structure, and engaged a reputable accounting firm to conduct a quality-of-earnings review. At the time the business was reintroduced to the market, it was sold at a multiple of almost 40 per cent of the original indicative figure. This is how to increase business valuation value before selling looks like in practice: disciplined, patient and commercial.

An opposite example is a consumer goods brand in North America that has established a high level of D2C revenue through digital marketing. The founders believed that their growth path would be sufficient in itself to receive a premium offer. They entered the market without addressing their reliance on a single paid media platform, low gross margins relative to category competitors, or limited proprietary product IP. During the due diligence process, buyers put red flags on every issue and reduced their offers. The last sale was made, but at a considerable discount to what similar businesses with cleaner profiles had sold for at the same time.

“Buyers are not paying me what a business has done; they are paying me what the business will consistently do tomorrow. The task of the seller is to ensure that tomorrow is as much a given as possible.”

4. The Exit Preparation Process: A Workflow

Preparation for leaving is not a one-time thing. It is a process performed in stages, and when done properly, it accumulates value at each stage. As a junior/mid-level professional who will be working with owners or executives on this path, knowing the flow will enable you to play a significant role in it, regardless of your role in finance, operations, marketing, or commercial.

TABLE 3 — EXIT PREPARATION: FOUR-STAGE PROCESS FLOW

Stage | Timeline | Key Actions | Common Challenge |

|---|---|---|---|

1. Diagnostic | 24–36 months out | Gap analysis of value, comparisons with comparables, and structural weaknesses. | Overvaluing present value; being emotional about it. |

2. Restructure | 18–24 months out | Construct a management team, clean financials, less concentrate on customers, and document systems. | Increased costs in the short run; leadership resistance to change. |

3. Positioning | 6–12 months out | Development of craft, strategic buyer identification, CIM and data room set-up. | Lack of congruence between what can be established by the business valuation and what the seller would like to assert. |

4. Transaction | 0–6 months | Control the buyer process, due diligence, negotiations, and deal structuring. | Due diligence surprises are issues that had not been previously addressed; deal fatigue. |

Among the most instructive lessons for M&A practitioners is that issues identified during due diligence are always more costly than those addressed in advance. One of the issues the seller mentioned in advance and is being addressed through a mitigation plan is a footnote. The identical problem identified by the buyer’s accountants during due diligence triggers a renegotiation. This imbalance is why an honest, early diagnosis is the most valuable thing a business can achieve during its exit process.

5. What Goes Overboard Often — and Why

Most business owners put nearly all their efforts into financial metrics in the process of exit preparation and underinvest in what can be broadly described as the intangible value stack – the brand, culture, talent retention and technology infrastructure that a sophisticated buyer will subject to due scrutiny. The risk profile of a business with a strong employer brand, low voluntary turnover, and a modern, scalable technology stack is very different from that of a business with a high turnover rate, outdated systems, and a culture that relies entirely on a founder.

Special attention should be paid to talent retention. One of the quickest ways to destroy value and erode buyer confidence is key employee turnover during a sale. The risk is greatly mitigated by businesses that have structured retention programmes (via equity participation, long-term incentives or multi-year employment contracts with key employees). Buyers can see when a management team is interested in the business’s future, and they charge a premium for that stability.

TABLE 4 — INTANGIBLE VALUE: BUYER EXPECTATIONS VS. SELLER BLIND SPOTS

Factor | What Buyers Look For | What Sellers Often Miss |

|---|---|---|

Brand Equity | Differentiation positioning, customer retention, and low turnover. | Supposing that the growth of revenues is the only indicator of brand strength. |

Talent & Culture | Well-established leadership, documented organisation, succession. | Founder or single-manager key-person risk. |

IP & Technology | Trade secrets, scalable technology, proprietary knowledge. | Underestimating or not reporting internal systems and tools. |

Customer Relationships | Breadth of relationships on the team, transferable contracts. | Relationships are based on the owner, not the business. |

6. In summary: The Paying Work

The realisation of what adds to a business’s sale value before exit finally depends on one field of study: making the business’s future as predictable and independent as possible to someone who has never operated it. That is, creating systems, not outcomes. It involves building a group not only based on income. And the financial and operational story presentation of the business valuation should be handled with the same attention given to the day-to-day running of the business.

To those in the supporting profession, be it finance, operations, HR or commercial strategy, the implication on the ground is as follows: any effort to decrease reliance on an individual, any process to be documented, any customer relationship to be expanded, any financial records to be tidied up, adds to the exit value of the business where you are employed. Rarely are the most effective methods of enhancing business valuation before an exit dramatically effective. They are gradual, planned and are usually unknown until a buyer places a price on the table.

Begin with the diagnostic stage: should you be advising an owner, be in an exit-bound business, or just be developing skills in this area? Determine the differences between the current position of the business and the one that a respectable buyer would want to see. Next, develop a strategy to seal those holes – not during the last months before sale, but years earlier, when there is yet time to ensure the improvements count.

Frequently Asked Questions

Q1. What is the sale value of a business?

The sale value of a business is the estimated price a buyer is willing to pay based on its financial performance, assets, market position, growth potential, and future earning capacity.

Q2. Why is a business valuation important before selling?

A professional valuation helps business owners set a realistic asking price, strengthen negotiations, and provide buyers with confidence in the company’s estimated value.

Q3. What factors influence the sale value of a business?

Key factors include profitability, cash flow, customer base, industry outlook, market conditions, tangible and intangible assets, and business risks.

Q4. Who should obtain a business valuation before selling?

Business owners, shareholders, investors, and companies preparing for mergers, acquisitions, or succession planning should obtain an independent valuation.

Q5. How does a professional valuation improve the selling process?

An independent valuation supports informed negotiations, reduces pricing disputes, and helps maximise the likelihood of achieving a fair market value.

2 thoughts on “What Increases the Sale Value of a Business Before Exit”