Table of Content

1. Introduction: Purchase Price Allocation (PPA)

The acquisition of a business by another is not just a matter of one entity acquiring control over another. It unleashes a complex accounting process that will determine how the purchase consideration is allocated in the acquiring entity’s financial statements – and that process, called Purchase Price Allocation, is one of the most important and challenging post-transaction accounting tasks. When done correctly, Purchase Price Allocation results in financial statements that reflect the underlying economic reality of the assets purchased and provide a basis for valuable Post-Acquisition Reporting. Done badly, it leads to financial errors, audit complexity and those nasty batches of goodwill impairments that still surprise investors and management years later.

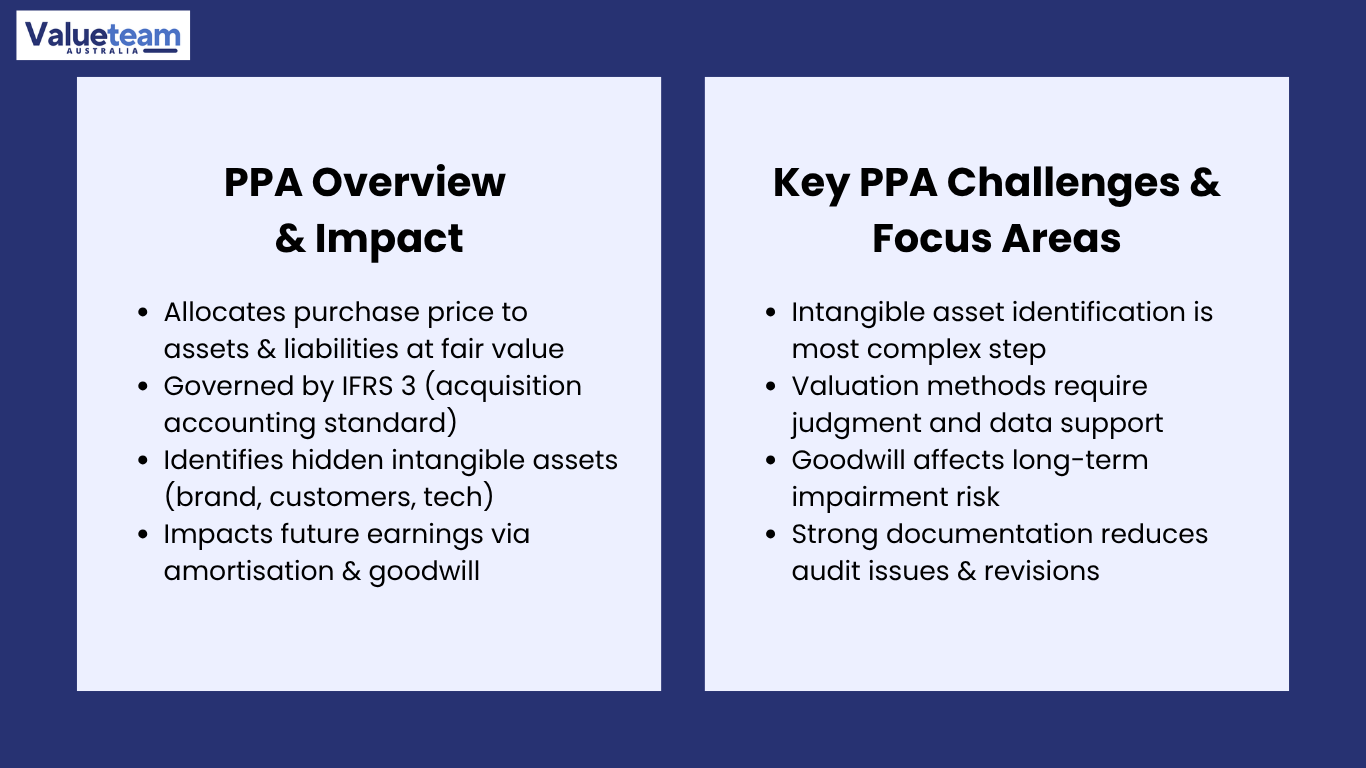

PPA Accounting Australia is primarily regulated by IFRS 3 (Business Combinations), adopted by the AASB, for Australian companies that report under IFRS (including all ASX-listed companies and many large unlisted groups). The standard requires an acquirer to measure and recognise, at their acquisition date, the fair values of all identifiable assets acquired and liabilities assumed – including a wide variety of Identifiable Intangible Assets that might not be reflected on the target’s books at all. This raises the possibility and challenge of capturing real value in the acquirer’s financial statements, as well as the need to document the methodology used to calculate all fair values.

This article is aimed at corporate finance, accounting, valuation and M&A professionals at the junior and intermediate levels who are interested in how Purchase Price Allocation (PPA) is conducted, what the main steps and challenges are, and how the quality of the PPA process ultimately affects financial reporting beyond the transaction’s close. So whether you’re gearing up to assist with your first set of post-acquisition financial statements, working with a client in the wash-up of a transaction, or simply acquiring the technical expertise to participate knowledgeably in conversations about Acquisition Accounting, the models and examples presented in this article should serve you well.

2. What Purchase Price Allocation Is and Why It Matters

Simply put, Purchase Price Allocation is how the overall price paid for an acquisition (the purchase price) is allocated to the individual assets and liabilities of the target, each at its fair value as of the acquisition date. The details follow from this apparently straightforward formula: the purchase price minus the fair value of net identifiable assets is the Goodwill Calculation. However, the simplicity of the equation belies the complexity of the process, since the fair value of all the identifiable assets must be accurately measured, which, for most intangible assets that have never been valued, requires expertise, process and documentation.

The M&A Accounting Treatment under IFRS 3 Compliance requires the acquirer to allocate within one year of the acquisition date (a measurement period). During this period, the acquirer can retrospectively revise provisional fair value estimates based on new information. However, after the measurement period has expired, the acquirer can only make adjustments to the opening balance sheet to correct accounting errors, not update fair value estimates. This provides a significant incentive to undertake detailed and well-documented fair value estimates during the measurement period, rather than provisional estimates that need to be refined.

The ramifications of PPA Accounting Australia do not end with the opening balance sheet. Depreciable assets’ fair values set in the Asset Recognition Process are carried as amortisation charges on the income statement of every subsequent reporting period. Identifiable Intangible Assets, such as customer lists, brands, and technology systems, are usually amortised over their useful lives (typically 3 to 15 years, depending on the asset and the industry in which it is used). The greater the fair value of an amortisable intangible asset, the greater the amortisation charge and the lower the net income. This relationship between Purchase Price Allocation and future earnings means that it is not a simple accounting compliance exercise – it impacts the way investors, analysts, and the board view the financial performance of an acquisition.

3. Identifying and Valuing Intangible Assets Under IFRS 3

The most complex part of a Purchase Price Allocation project is the recognition and valuation of Identifiable Intangible Assets. For IFRS 3 Compliance, an intangible asset is separable from goodwill if it is either separable – it can be separated or divided from the entity and sold, licensed, or transferred – or contractual-legal – it arises from contractual or other legal rights. This is a very broad definition, and in reality, it encompasses a great many assets that would not be found on the target’s pre-acquisition balance sheet because they were either internally developed (and therefore not capitalised under AASB 138) or simply not identified and valued at all.

The table below illustrates the most common types of Identifiable Intangible Assets encountered in Australian M&A deals, the valuation methods used for each, and the range of useful lives commonly used for subsequent amortisation. This is an area in which those practitioners who familiarise themselves with these categories – and the specific methodological requirements associated with each – are much better placed to contribute to and review the output of Purchase Price Allocation exercises than those who do not have this knowledge.

Intangible Asset Category | Primary Valuation Method | Typical Useful Life | Common in Sector |

Customer relationships | Multi-Period Excess Earnings Method (MEEM): isolates earnings attributable to the customer relationship after charges for all other contributing assets | 5–12 years (based on churn and attrition analysis) | Professional services, technology, healthcare, and financial services |

Brand names and trademarks | Relief-from-Royalty: estimates the royalty the business would pay to license the brand if it did not own it; discounts projected royalty savings to present value | Indefinite or 3–15 years, depending on brand durability assessment | Consumer goods, retail, hospitality, FMCG |

Technology and software platforms | Relief-from-Royalty or Cost Approach: either royalty savings or cost-to-recreate, adjusted for obsolescence | 3–7 years (technology cycle and competitive lifecycle) | SaaS, fintech, medtech, industrial technology |

Non-compete agreements | Income approach: estimates the reduction in earnings that would result if the counterparty competed; probability-weighted and discounted over the agreement term | Equal to contractual term (typically 2–5 years) | Owner-operated businesses, professional services, and distribution |

Order backlog and contracts in place | MEEM or direct income approach applied to the specific contracted revenue stream as of the acquisition date | Short (6–18 months); reflects backlog duration at acquisition | Construction, project-based services, and manufacturing |

4. Goodwill Calculation and Its Post-Acquisition Implications

Goodwill Calculation is the numerical result of the Purchase Price Allocation: it is the balance remaining after the fair value of all identifiable assets acquired and liabilities assumed has been deducted from the purchase price. From an accounting perspective, goodwill is the economic benefit derived from the assets that are not capable of being individually identified and separately recognised – such as the value of an assembled workforce, synergies of the combined entities and the value paid for a strategic position or market entry. Under IFRS 3 Compliance, goodwill is no longer amortised: it is tested for impairment each year under AASB 136.

The annual impairment test on goodwill is one of the most important long-term effects of Acquisition Accounting, and it’s where the original Purchase Price Allocation can have a lasting impact. AASB 136 requires that goodwill be allocated to cash-generating units (CGUs) or groups of CGUs at the level at which management monitors it for internal reporting purposes – and the carrying value of each CGU be compared to its recoverable amount at least once a year, or more frequently if there is an indicator of impairment. If the Fair Value Allocation at the time of the acquisition correctly identified and separately valued the fullest possible set of intangible assets, the goodwill allocated to each CGU will be lower, and the risk of goodwill impairment will be smaller. If intangibles are not properly identified and a larger proportion is allocated to goodwill, the CGU will be overvalued and at a higher risk of impairment if the business does not perform as expected at the time of acquisition.

For those involved in Post-Acquisition Reporting processes, the association between the quality of the PPA and the risk of goodwill impairment is a reason (besides compliance) to focus on thorough intangible asset recognition at the time of acquisition. An effective Asset Recognition Process that allocates value to amortisable intangibles will lower the goodwill balance, provide transparent amortisation charges and leave the acquirer with a CGU balance that is less vulnerable to earnings volatility in future periods. This is not a niche value proposition of good accounting; it is a significant issue for any acquirer whose financial statements will be audited, reviewed by institutional shareholders, or reviewed by debt providers subject to financial covenant tests.

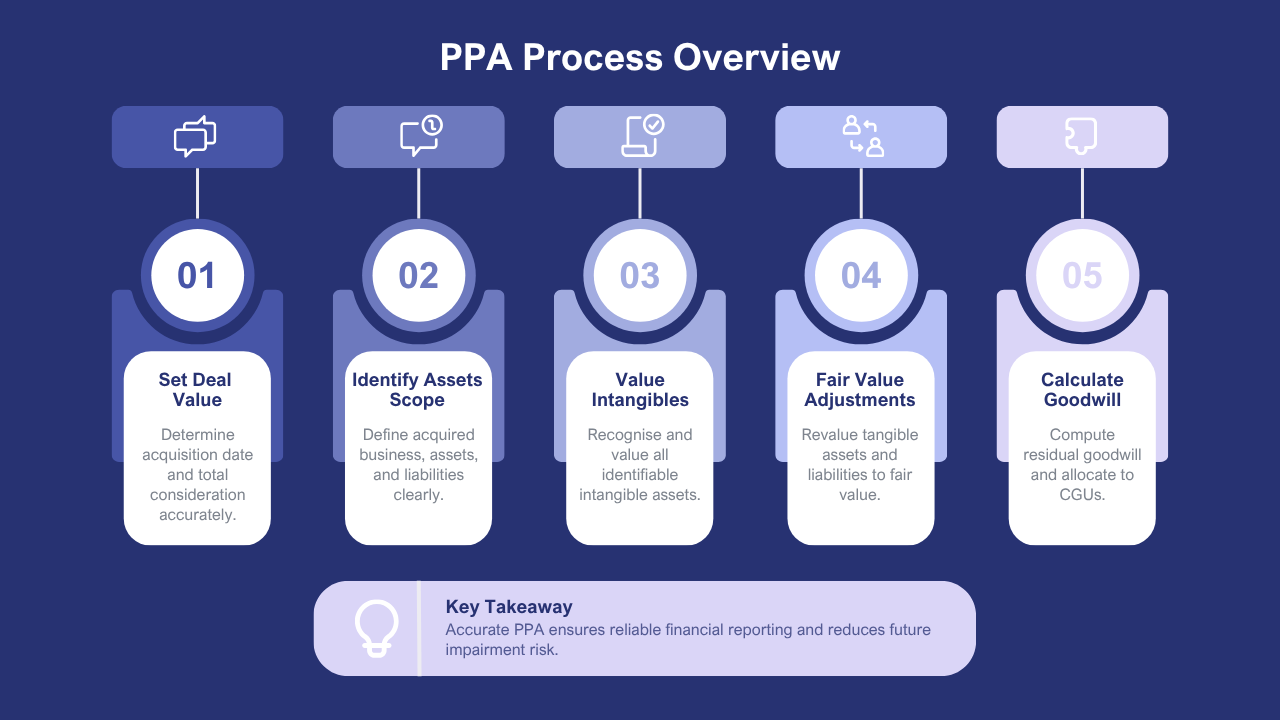

5. Five Key Steps in the Purchase Price Allocation Process

The steps in a robust Purchase Price Allocation apply to deals of all sizes and across all industries. The five steps outlined below reflect the Asset Recognition Process in practice, in Australia, from deal closing through to completed Post-Acquisition Reporting.

Step | What It Involves | Common Challenge |

1. Determine the acquisition date and total consideration | Establish the precise acquisition date under IFRS 3 Compliance; calculate total consideration, including cash, deferred payments, contingent consideration (earnouts), and equity instruments issued | Contingent consideration must be measured at fair value at the acquisition date, not at its maximum contractual amount; earnout structures require probability-weighted scenario modelling |

2. Identify the acquired business and its components | Map all entities, operations, and asset categories included in the acquisition; distinguish between business combinations (AASB 3) and asset acquisitions (AASB 116/138); establish opening balance sheet scope | Incorrectly classifying a business combination as an asset acquisition avoids the PPA Accounting Australia requirements but creates audit risk and potential restatement obligation |

3. Recognise and measure Identifiable Intangible Assets | Apply separability and contractual-legal criteria under IFRS 3 Compliance; engage specialist valuers for each identified intangible category; document methodology, assumptions, and sensitivity analysis for each Fair Value Allocation | Acquirers frequently under-identify intangibles, either from cost considerations or unfamiliarity with the standard; auditors will challenge allocations where the intangible universe appears incomplete relative to sector norms |

4. Measure all tangible assets and liabilities at fair value | Restate property, plant, equipment, inventory, and financial instruments at acquisition-date fair value; identify any contingent liabilities meeting recognition criteria; assess deferred tax implications of all fair value adjustments | Deferred tax accounting on fair value step-ups is technically complex and frequently misapplied; tax specialists should be engaged alongside the valuation team for all material adjustments |

5. Calculate Goodwill Calculation and allocate to CGUs | Compute residual goodwill; allocate to CGUs for annual impairment testing under AASB 136; document the basis of allocation and ensure it reflects management’s internal reporting view of the business | Goodwill allocation to CGUs is often treated as an afterthought; poorly structured CGU allocations create ongoing complexity in the annual impairment test and increase audit friction in subsequent reporting periods |

It is at Step 3 – identification and valuation of Identifiable Intangible Assets – that expertise is most critical and quality differences between service providers are most apparent. Practitioners who bring to this step a list of categories of intangibles relevant to the business they are dealing with, and who commission independent specialist valuations for the most significant assets, can be expected to produce far more defensible allocations than those who under-identify intangibles or rely on in-house estimates without demonstrating methodology. The purpose of the 12-month measurement period for the work to be done is to give acquirers who use the new measurement period as an opportunity to do this good work, rather than a deadline to be met with as little effort as possible, generally better outcomes in the subsequent impairment testing cycle.

6. Process, Challenges, and What the Market Teaches You

M&A Accounting Treatment and PPA Accounting in Australia are two areas with steep learning curves. It’s good to know from a textbook what is required for IFRS 3 Compliance; it’s essential to know from practice how a typical PPA engagement performs, where the difficulties lie, and how they are addressed. The four-phase process below is a typical workflow for a formal PPA engagement between deal close and the issuance of financial statements.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Deal Close & Scoping | Fair Value Assessment | Goodwill & CGU Allocation | Audit & Finalisation |

Confirm acquisition date and total consideration; scope Identifiable Intangible Assets by sector; assemble deal documents; brief specialist valuers and tax advisors; set measurement period milestones | Conduct Fair Value Allocation for tangible assets and liabilities; apply specialist valuation methods to each intangible category; model deferred tax on all step-ups; prepare provisional PPA schedule | Calculate Goodwill Calculation as residual; allocate to CGUs aligned with internal reporting structure; document allocation basis; prepare AASB 136 impairment testing framework for ongoing Post-Acquisition Reporting | Support external auditor review of all Fair Value Allocation assumptions; respond to queries on methodology and comparables; finalise PPA within measurement period; disclose in acquisition notes per IFRS 3 Compliance |

Most of the real challenges in the PPA Accounting Australia exist in Phase 2. Accurately valuing Identifiable Intangible Assets requires information that may not be available in a structured format immediately post-close – for example, customer attrition rates, royalty rates for brand licencing, the cost of replacing certain technologies and the revenue schedule for the order book – all need to be collected, verified and documented before they can be incorporated into a valuation model. In many deals, the quality of the data available in the first few weeks after close is significantly lower than what will become available later, once the acquirer has had time to reconcile systems and records. Practitioners who anticipate data needs and requests in their pre-close planning – rather than identifying data gaps in Phase 2 – tend to provide more accurate provisional allocations and avoid revisiting measurement period adjustments.

A recurring issue during the Phase 3 and Phase 4 periods is a conflict between the acquirer’s desire to allocate as much value as possible to goodwill and the auditor’s duty to question if the maximum recognisable intangible asset universe has been identified. Acquirers may be reluctant to allocate value to amortisable intangibles because amortisation expenses will affect earnings. Auditors, in accordance with IFRS 3 Compliance, will challenge allocations that appear inconsistent with the “size of the intangible pie” identified in the transaction. This is particularly the case when the acquisition premium is substantial (indicating significant intangible value), but the PPA shows relatively small intangible amounts. Young professionals who recognise this are better equipped to anticipate the auditor’s concerns and can present their analysis in a way that pre-emptively addresses them.

7. Real Cases and What They Reveal

A prime example of the impact of poor Purchase Price Allocation is that of a financial services company’s acquisition of a complementary advisory company. The acquirer’s in-house accountants undertook the initial PPA without the assistance of a specialist intangible valuator. They allocated most of the consideration to goodwill, with only a small amount of customer relationship intangibles recognised. During the year-end audit of the Fair Value Allocation, the external auditor detected that the customer relationship base of the acquired entity – clearly the main driver for the purchase of the firm – had not been separately recognised as an Identifiable Intangible Asset with a justified fair value. This was after the measurement period was closed. This led to a reopening of the opening balance sheet, a substantial lift in the customer relationship intangible, and a commensurate decrease in goodwill, with annual amortisation charges that had not been factored into the acquirer’s post-acquisition earnings projections. The cost of this rectification, in terms of specialist valuation fees, time for the auditors to undertake the work, and management time to oversee it, was significantly higher than the cost of the specialist valuer engaged at the time of the original Asset Recognition Process.

A positive example is a technology firm that purchased a SaaS platform and ensured a proper PPA Accounting Australia exercise. The acquiring management team engaged a specialist intangible valuation firm within two weeks of closing the deal and identified the Identifiable Intangible Assets based on a benchmarking of the industry – technology platform, customer relationships, brand and a non-compete agreement with the founders. The Fair Value Allocation for each intangible was documented with a methodology, benchmarked royalty rates and a projected customer attrition rate based on an analysis of the target’s historic CRM data. The external auditor’s review of the allocation was well documented, and the audit was not an issue, nor was the reporting delayed. The Goodwill Calculation residual was small relative to the total consideration as a result of the intangible identification exercise, and the CGU structure reflected how the integration was managed. So the annual impairment test was a simple exercise rather than an orgy of reconstruction.

8. Conclusion: Actionable Insights for Practitioners and Advisors

Purchase Price Allocation is not a backroom compliance process to be done after the deal is done – it is an accounting and valuation exercise with significant financial reporting implications that should be given the same consideration as the transaction itself. The Fair Value Allocation of Identifiable Intangible Assets, the Goodwill Calculation (residual) and the CGU structure of the acquirer at the time of the transaction flow through to the financial statements and impairment indicators for the foreseeable future. Those who view this step as a compliance exercise rather than an opportunity to capture the economic substance of the acquisition and accurately reflect it in the financial statements tend to do more harm than good in the long run.

For young professionals looking to build technical skills in M&A Accounting Treatment, it’s important to understand the criteria for recognising Identifiable Intangible Assets under IFRS 3 Compliance, the most common valuation methods applied to each type, and the deferred tax implications arising from fair value adjustments. These are practical tools that enable a practitioner to provide value beyond merely “checking off” the PPA process. Learning from real-life transactions – examining the notes disclosing acquisition accounting in financial statements, questioning senior practitioners on the decisions made in real engagements and observing the performance of goodwill allocated in significant transactions through impairment testing – is the best way to develop the pattern recognition skills that separate the seasoned PPA practitioners from the mechanistic.

The best advice for an advisor supporting an acquiring client is simple: seek specialist support. The 12-month measurement period for IFRS 3 Compliance gives plenty of time to complete a Purchase Price Allocation, provided it begins as soon after deal close as possible. Draft allocations prepared without the specialist input of an intangible valuator often need substantial adjustment, and the adjustment cost (in both consulting fees and management time) always outweighs the cost of doing it right in the first instance. Post-Acquisition Reporting that reflects a credible, well-documented Asset Recognition Process is not just a compliance goal – it is a message to auditors, investors, and boards that the acquisition has been managed with the same care that was justified by the price paid for it.

Frequently Asked Questions

Q1. What is Purchase Price Allocation (PPA)?

Purchase Price Allocation allocates the purchase price of an acquired business to identifiable assets, liabilities, and goodwill based on their fair values.

Q2. What is a business valuation and an independent expert report?

PPA ensures accurate recognition of acquired assets and liabilities while supporting compliance with accounting standards and transparent financial reporting.

Q3. What are the circumstances in which an independent expert report is needed?

Common assets include customer relationships, trademarks, patents, technology, property, equipment, and other identifiable intangible assets.

Q4. What is the average length of a business valuation engagement?

Businesses involved in mergers and acquisitions, accountants, auditors, finance teams, and valuation professionals commonly require PPA services.

Q5. What information is needed to start a valuation engagement?

Professional valuation produces reliable fair value measurements, supports regulatory compliance, and improves the accuracy of post-acquisition financial statements.

2 thoughts on “Purchase Price Allocation (PPA) Explained for Australian M&A Transactions”