Table of Content

1. Introduction AUSTRAC Compliance Requirements

Businesses expanding are often found to have their AUSTRAC Compliance Guide obligations at the worst possible time: during a growth period when expansion is accelerated, when a new product is launched, or when a compliance audit reveals gaps that have quietly been building over months. The Australian financial intelligence regulator and supervisor of money laundering (as well as the regulator of other money services) is the Australian Transaction Reports and Analysis Centre (AUSTRAC), and its AML/CTF Regulations Australia framework applies to the very first designated service transaction, not to a revenue level or to a licensing level. In the case of rapidly growing businesses, AUSTRAC compliance requirements can grow at the same rate, as they do not need to be built into the growth plan initially.

The Reporting Entity Obligations in the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 are based on a principle familiar to those with experience in compliance systems. Still, many business leaders do not know it when their business grows into a regulated service category. The difference is important, as the AUSTRAC’s enforcement focus is on the quality of the compliance program, not necessarily on whether any particular incident of money laundering was detected.

The article targets founders, senior managers, and compliance professionals of growing businesses who need to understand what AUSTRAC Compliance Requirements really means, how the obligations scale with business growth, and the practical steps to building a program robust enough to withstand regulatory scrutiny as the business expands. The frameworks herein apply to the fintech, payments, lending, digital asset, and professional services sectors, which most frequently fall within the AUSTRAC’s supervisory jurisdiction.

2. Who AUSTRAC Regulates and What Triggers Obligations

The designated service trigger and Reporting Entity Obligations

The jurisdiction of AUSTAC extends to any individual or organisation that provides a designated service as stipulated in the AML/CTF Act. The list of designated services is long and includes: accepting or making electronic funds transfers, currency exchange, remittance services, providing accounts or loans, digital currency exchange, gambling services, and, under expanding reforms, professional services, including conveyancing, legal, and accounting services, when they facilitate financial transactions on behalf of clients.

- Reporting Entity Obligations apply to the initial transaction in a specified service class; there is no minimum transaction size or volume threshold.

- A business that introduces a new product feature that triggers a designated service status, such as adding a payment account or currency conversion feature to an existing platform, becomes subject to new obligations as of the date of the first transaction using that feature.

- The obligation to enrol under the AML/CTF Regulations Australia applies to the provision of the given service; operating without enrolment is also a violation of those Regulations.

How obligations scale with business growth

The most practically significant fact about AUSTRAC Compliance Guide for growing businesses is that obligations increase with complexity and transaction volume, among other factors. The introduction of a new customer segment, a new geographic market, a new product with a new risk profile, or the acquisition of a business that brings its own regulated services all trigger a need to reassess and modify the Risk-Based AML Framework and the supporting compliance program. Companies that treat their AML/CTF program as a stagnant document prepared at inception, rather than a living framework that evolves, gradually accrue gaps in their compliance program.

3. The Core Obligations and How They Work in Practice

Customer Identification Procedures and the KYC Foundation

The operational basis of all AML Program Implementations is Customer Identification Procedures. The business should gather and verify the customer’s identity using a reliable, independent source before providing any designated service. For individual customers, this normally involves a check against a government-issued document or an accredited electronic verification service. For corporate customers and trusts, the requirements are extended to include beneficial ownership identification: tracing the ownership chain to identify the natural persons who ultimately own or control the entity.

- The Customer Identification Procedures should be used before the first service transaction; in rare, documented cases, deferred verification can be used.

- Higher-risk customers: politically exposed persons (PEPs), customers in high-risk jurisdictions, and non-face-to-face customers demand extra measures beyond those that are typical.

- Ongoing Customer Identification Procedures are applicable throughout the relationship; if the customer’s risk profile changes materially, the identification and verification procedures should be updated.

Regulatory Reporting Duties: what must be reported and when

The AML/CTF Act Regulatory Reporting Duties include three main types of reports. Any physical currency transaction of $10,000 or more, or its foreign currency equivalent, must be reported as a Threshold Transaction Report (TTR), which is why they are called threshold transactions. International Funds Transfer Instructions (IFTIs) should be reported within 10 business days of when they are sent or received. Suspicious Transaction Reporting – Suspicious Matter Reports (SMRs) – must be submitted as soon as practicable, and no later than 24 hours in the case of terrorism financing, or three business days in the case of other suspicious matters.

Report Type | Trigger | Deadline | Key Compliance Risk |

Threshold Transaction Report (TTR) | Physical currency transaction of AUD $10,000 or more | Within 10 business days of the transaction | Failing to identify reportable transactions and not monitoring cash transactions against the threshold |

International Funds Transfer Instruction (IFTI) | Electronic transfer of funds to or from Australia | Within 10 business days of being sent or received | Automated systems not configured to capture all IFTI-eligible transfers; delays in processing transfer data |

Suspicious Transaction Reporting (SMR) | Reasonable grounds to suspect proceeds of crime, terrorism financing, or other AML/CTF-relevant activity | 24 hours for terrorism financing; 3 business days for other matters | Suspicion formed but not reported; staff not trained to recognise and escalate indicators; tipping off the customer |

Annual Compliance Report | Annual reporting to the board or governing body on the program’s effectiveness | No fixed statutory deadline, but expected as part of program maintenance | No formal annual review process; board not informed of compliance status; deficiencies not escalated or addressed |

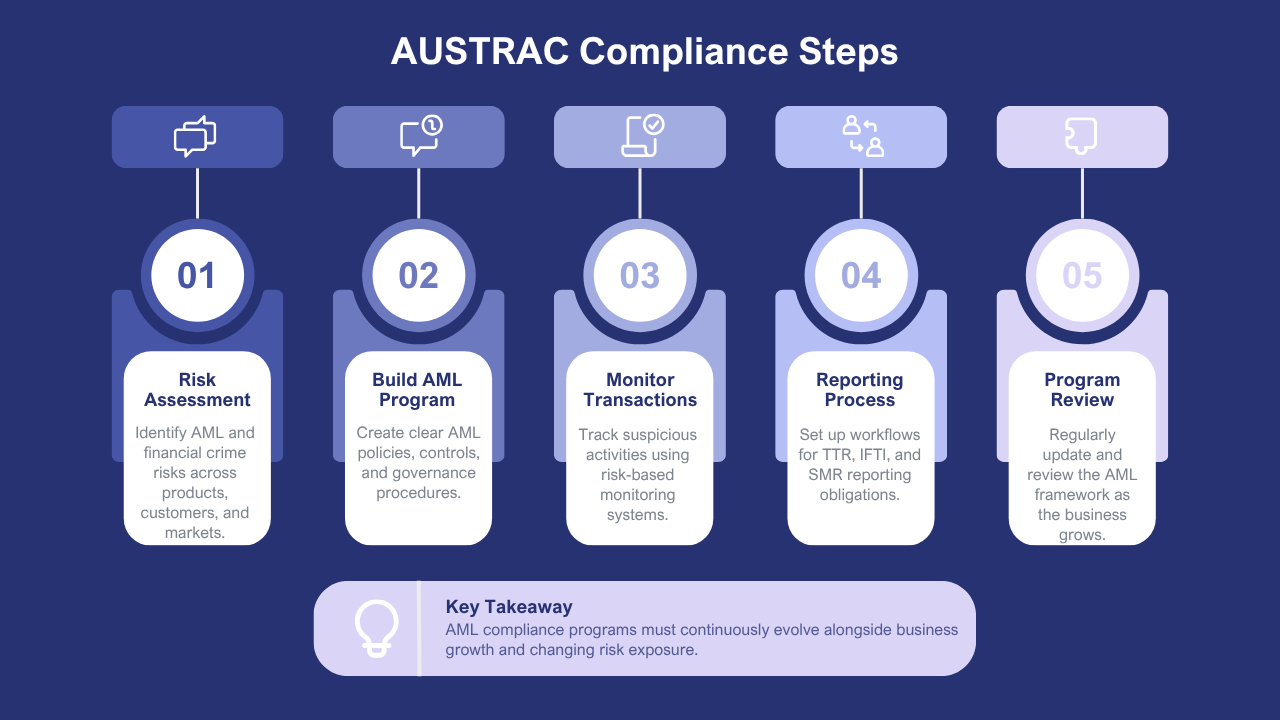

4. Five Key Steps for Growing Businesses: Building an AML Program

The implementation of an AML Program for a growing business does not just involve drafting a policy document. It necessitates a systematic approach that embeds the Risk-Based AML Framework in the business and keeps it up to date as the business continues to develop. The following five steps illustrate how experienced compliance professionals construct programs that are fit for purpose at every stage of growth.

Step | What It Involves | AUSTRAC Compliance Requirements | Common Gap for Growing Businesses |

1. Conduct an ML/TF risk assessment | Identify and document the money laundering and terrorism financing risks specific to the business’s products, services, customers, delivery channels, and geographies; update when new products or markets are introduced | The risk assessment must precede all other program elements and must reflect the entity’s actual risk profile, not a generic industry template | Risk assessment is conducted once at program launch and not updated as the business grows; new products and customer segments are not assessed for ML/TF risk |

2. Build the AML/CTF Regulations Australia program | Draft Part A (governance, oversight, controls framework) and Part B (Customer Identification Procedures, ongoing due diligence, enhanced due diligence for higher-risk customers); have the program approved by the board or senior management | The program must be documented, approved at the senior level, and kept current; AUSTRAC can request a copy during supervisory activities | The program is a document rather than an operational reality; procedures in the document are not reflected in actual business processes; no governance structure for ongoing maintenance |

3. Implement Ongoing Compliance Monitoring and transaction monitoring | Deploy systems or manual processes to monitor transactions for suspicious activity; set monitoring thresholds calibrated to the entity’s specific risk profile; document the methodology and the process for reviewing and actioning alerts | Ongoing Compliance Monitoring must be proportionate to the assessed ML/TF risk; higher-risk products and customers require more intensive monitoring | Generic monitoring thresholds not calibrated to the business’s specific products; no documented process for reviewing alerts; monitoring system not updated when new products are launched |

4. Establish the Regulatory Reporting Duties workflow | Build internal processes for identifying and filing TTRs, IFTIs, and SMRs within the required timeframes; appoint an AML/CTF Compliance Officer with clear accountability for report filing | Reports must be filed within statutory deadlines; late reports are themselves contraventions. Suspicious Transaction Reporting requires staff training to identify indicators | No designated owner for report filing; manual processes creating risk of missed deadlines; staff not trained to identify suspicious activity indicators that trigger SMR obligations |

5. Maintain and review the program under the Risk-Based AML Framework | Conduct independent reviews of the program at least every three years; update the program when the business changes materially; maintain records for 7 years; file an annual compliance report to the board | The Risk-Based AML Framework requires the program to be current and effective, not just documented; AUSTRAC expects evidence of ongoing management and review | Program last reviewed at launch; no scheduled review cycle; independent review not commissioned; records not maintained in a retrievable format |

Step 3 — The component most likely to fail when the business is expanding rapidly is the implementation of calibrated Ongoing Compliance Monitoring. When a business adds new products, enters new geographies, or changes its customer mix, the risk profile changes – and the monitoring that was suitable in the original product mix may no longer be able to detect the risk patterns that the new profile presents. The payments business that introduces a cryptocurrency exchange feature must rebalance its monitoring system to reflect the specific typology of digital assets, rather than simply applying the same thresholds as its existing fiat payment monitoring. The best compliance programs include a formal product launch procedure that must be monitored and calibrated, and evaluated and recorded before the launch of any new designated service.

5. Process, Real Cases, and Lessons for Compliance Professionals

The AML Program Implementation growth workflow

Expanding businesses require a compliance workflow that grows with the business without becoming outdated as the risk profile changes. The four-phase programme below indicates how functionally mature compliance functions structure their AML/CTF Regulations Australia obligations across the business growth cycle.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Foundation | Operational Embedding | Growth & Reassessment | Continuous Improvement |

Complete ML/TF risk assessment; enrol with AUSTRAC; draft and approve AML/CTF program (Parts A and B); appoint AML/CTF Compliance Officer; implement Customer Identification Procedures for new customers | Deploy Ongoing Compliance Monitoring systems calibrated to the risk profile; train all customer-facing and compliance staff; establish Regulatory Reporting Duties workflows for TTRs, IFTIs, and Suspicious Transaction Reporting | Update risk assessment when new products, markets, or customer segments are introduced; revise program and monitoring thresholds accordingly; conduct compliance reviews for all material business changes under the Risk-Based AML Framework | Commission independent program review every three years; maintain 7-year record retention; file annual board compliance report; monitor AUSTRAC guidance updates; respond to any supervisory inquiries under AUSTRAC Compliance Guide |

Case 1: The product launch that created an undisclosed obligation

One of the software companies introduced a peer-to-peer payment option into its existing platform as part of its product development. The option enabled users to send money between accounts within the platform and between bank accounts. Before launching the feature, the development team had not evaluated the feature against the AML/CTF Regulations Australia designated services list. A compliance audit six months after the launch of the feature revealed that the payment functionality had triggered Reporting Entity Obligations that had not been identified. The business had been offering specified services without enrolment, without Customer Identification Procedures and without any Ongoing Compliance Monitoring of the said transactions. The remediation programme encompassed retroactive enrollment, a catch-up KYC exercise for all affected users, and a major investment in monitoring infrastructure. The moral: any product development process should have an AML/CTF regulatory assessment checkpoint at the gateway of any new feature before it goes live.

Case 2: Monitoring thresholds that missed a growth-phase risk

The AML Program Implementation at the launch of a digital lending business was compliant, and its monitoring was calibrated to the risk profile of the business’s first consumer loan product. When the business expanded and introduced a small-business lending product with transaction volumes far greater, the compliance team failed to re-examine the monitoring thresholds. The customer risk profile of the business lending product differed from that of the consumer product, yet the monitoring system treated both the same. The supervisory review of the monitoring system by AUSTRAC revealed that several Suspicious Transaction Reporting obligations were not met due to the monitoring system’s thresholds being calibrated to consumer transaction patterns and to the business lending book, and the system did not identify anomalous patterns in the business lending book. The entity had to perform a retrospective examination of three years of business lending activities and submit a large number of late SMRs. The principle of the Risk-Based AML Framework, which states that you should calibrate to your real risk, not your original risk, applies to the entire product lifecycle rather than just the program launch.

6. Conclusion

Not a one-and-done project is the AUSTRAC Compliance Guide to growing businesses. The AML/CTF Regulations Australia framework demands that a program be living, risk-responsive, and actually operational, and that it evolves with the business, and relates effectively to new products, customers, and markets. AUSTRAC Compliance Requirements are substantive obligations subject to substantial civil penalties in the event of non-compliance, and the enforcement record reflects that when programs are not up to standard, then AUSTRAC is willing to act against entities of all sizes.

- Any product rollout, market entry, or other significant business change must result in a formal re-evaluation of the Risk-Based AML Framework and the supportive monitoring thresholds – a compliance checkpoint that is embedded into the development process, as opposed to an afterthought.

- Regulatory Reporting Duties, such as Suspicious Transaction Reporting, must be owned by a named person with definitive accountability, supported by staff training that enables frontline staff to recognise and report indicators that trigger reporting obligations.

- To junior compliance professionals working in this space, the published enforcement outcomes, typologies reports and industry guidance published by the regulator are the most useful available learning materials – they describe the particular failure patterns identified by the regulator and the standard of program it anticipates seeing.

Frequently Asked Questions

Q1. What is AUSTRAC compliance?

AUSTRAC compliance refers to meeting Australia’s Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) obligations established by the national regulator.

Q2. Why is AUSTRAC compliance important?

Compliance helps businesses detect suspicious activities, prevent financial crime, and avoid regulatory penalties.

Q3. What are common AUSTRAC compliance requirements?

Requirements include customer due diligence, risk assessments, transaction monitoring, record keeping, employee training, and reporting suspicious matters.

Q4. Who must comply with AUSTRAC regulations?

Financial institutions and other designated reporting entities covered by Australia’s AML/CTF legislation must comply with AUSTRAC requirements.

Q5. How can businesses strengthen AUSTRAC compliance?

Businesses should implement effective compliance programs, regularly review internal controls, provide staff training, and monitor regulatory updates.