Table of Content

1. Introduction to Closing the Valuation Gap Australia

The same disillusionment seems to befall most business owners who have been through a sale process: the price the buyer offered does not seem to reflect the value of the business they had. And in most instances, they were correct, not because the purchaser had done unfairly, but because the vendor had not done the work to bring the real value into view. This, in a nutshell, is the nature of the Valuation Gap Analysis challenge: a difference between the amount of value that a seller believes exists in his or her business and the amount of value that a buyer is willing to pay based on what he or she can actually see, verify, and underwrite.

The gap is not merely about financial performance. A business may be earning a good income and yet remain undervalued when its customer relationships seem weak, its growth story is unclear, or its competitive advantages are not presented in terms acceptable to the investment committee of a buyer. This gap needs to be bridged with a conscious Seller Value Strategy – one that initiates long before the information memorandum is written and continues through all the phases of the deal process.

The article is a practical guide for anyone involved in preparing a business for sale, advising business owners, or developing the financial and commercial skills required in an M&A advisory or corporate finance role. The structures here are applicable regardless of whether the transaction is a trade sale, a private equity recapitalisation, or a management buyout, because in all cases the fundamental challenge is the same: to demonstrate to buyers what the business is actually worth.

2. Understanding the Valuation Gap Analysis and Why It Persists

What creates the gap between seller expectations and buyer offers

Valuation gaps are almost always disputes over the figures on the page. It is nearly always a dispute over what those figures imply concerning the future. Buyers risk-adjust for what they cannot themselves ascertain, and discount opportunities they cannot model with confidence. A strict Valuation Gap Analysis identifies three primary causes of this discount: information asymmetry (the seller knows more than the buyer), narrative absence (the value story has not been told), and presentation risk (the way information is packaged creates doubt rather than confidence).

The most practical lesson sellers and their advisers can learn from this analysis is that a large share of the gap is not inherent in the business; the management of the sales process creates it. Work done systematically over the 12 to 24 months before a transaction, in the form of Pre-Sale Positioning, continues to reduce the gap by decreasing the information asymmetry and the risk adjustments buyers make.

- Anything that buyers cannot confirm on their own is subject to risk discounts by the purchaser; uncertainty is directly proportional to the price that the buyer is willing to pay.

- Businesses whose value is not immediately apparent but is real are the most undervalued, such as those with strong customer loyalty, proprietary processes, or a defensive market position that has never been formally documented.

- The quality of information itself signals: well-structured, clearly presented information conveys to buyers that management is competent and the business is properly managed.

The role of hidden assets in widening the gap

Most valuation gaps are increased by the inability to surface what professionals refer to as Hidden Asset Identification – the systematic process of listing the value-generating assets that do not appear on the balance sheet. These include customer relations and retention levels, brand equity, proprietary technology or processes, significant supplier relationships, and the quality of the management team below the founder level. All these are actual contributors to Negotiation Value Drivers, and can be quantified and communicated, though only when someone has gone to the effort of identifying them in the first place.

A company that has never formally mapped its intangible resources is structurally disadvantaged in any selling procedure. The buyer’s due diligence team will find the same assets. Still, they will evaluate them through a prism of doubt rather than confidence, and their valuation will reflect that doubt with broader risk adjustments and more conservative growth profiles.

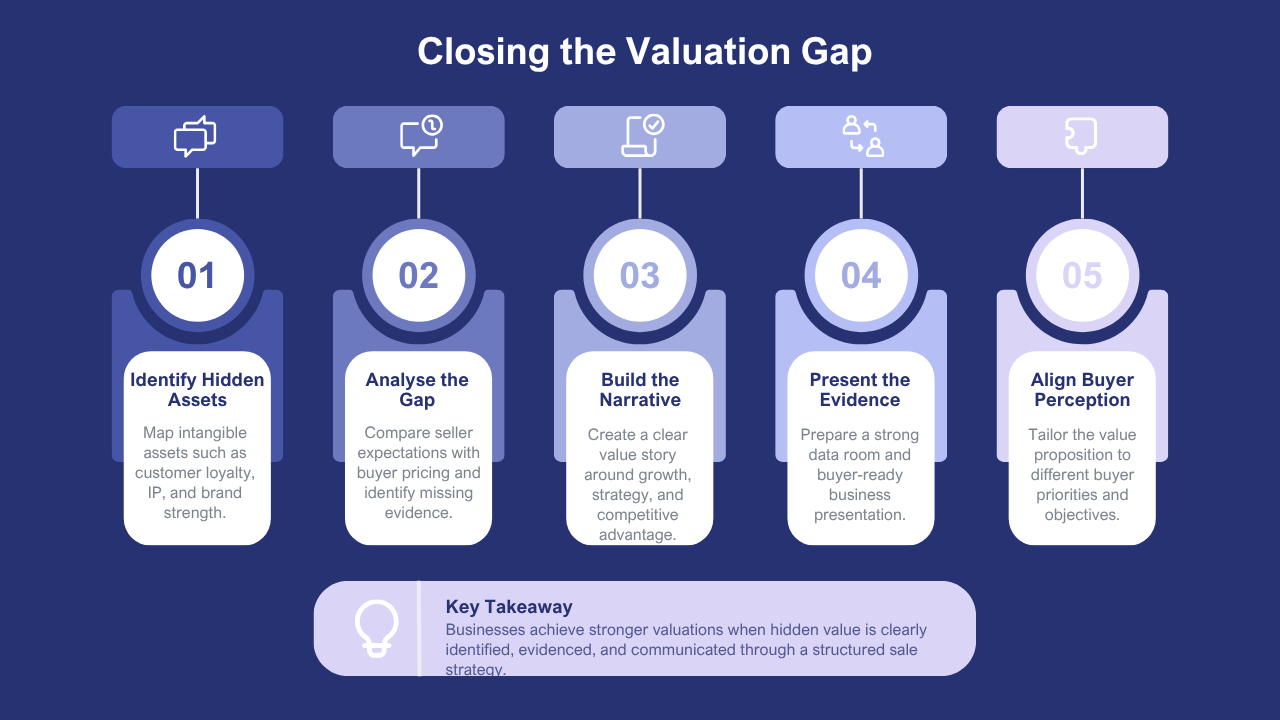

3. Five Steps to Showcase Hidden Business Value Australia

A well-defined Seller Value Strategy adheres to a well-defined sequence. The five steps below outline how experienced M&A advisers approach Pre-Sale Positioning for businesses across a spectrum of deal sizes and sectors.

Step | What It Involves | Key Deliverable | Timing |

|---|---|---|---|

1. Hidden Asset Identification | Systematically map all intangible and off-balance-sheet assets: customer retention data, brand strength, IP, proprietary processes, key contracts, management depth | Intangible asset register with supporting evidence for each item | 12–18 months pre-sale |

2. Valuation Gap Analysis | Compare the owner’s valuation expectations against likely buyer pricing; identify the specific value drivers that are not currently visible or credible to an external buyer | Gap report identifying which value drivers need evidence-building before going to market | 12 months pre-sale |

3. Value Communication Strategy | Develop the narrative architecture: how the business’s history, competitive position, customer relationships, and growth opportunities will be framed for buyers | Information memorandum outline, management presentation structure, and key messages for each buyer type | 6–9 months pre-sale |

4. Business Value Presentation | Build the data room and management presentation to evidence every claimed value driver; ensure financial model quality, data integrity, and commercial narrative alignment | Investment-grade information memorandum and verified data room | 3–6 months pre-sale |

5. Buyer Perception Alignment | Tailor the value story to each buyer archetype — strategic acquirer, financial sponsor, management team — so that the most relevant value drivers are front and centre for each audience. | Buyer-specific presentation variants and targeted due diligence support materials | During the sale process |

The area where several seller-side processes fall short is Step 3, which involves building the Value Communication Strategy. The financial information is well presented, but the context that puts it into perspective is either missing or unsatisfactory. Buyers do not base their decision on numbers alone; they base it on whether the narrative behind the numbers is coherent, credible, and compelling enough to justify the premium. Financial Storytelling is no spin; it’s the art of telling the truth and nothing but in the order, form, and language that would enable a buyer to make the right decision and no other.

4. Process, Real Cases, and Lessons Learned

How the pre-sale process works in practice

The pre-sale positioning process is an organised programme of actions, not a document in itself. In reality, it operates through four stages, from an initial readiness test to execution of the deal. It is crucial to understand where the most important decisions are made and where most of the value remains untapped. This is essential for anyone advising sellers or preparing businesses to transact.

Phase | Focus Area | Key Activity | Primary Risk If Skipped |

|---|---|---|---|

Phase 1: Readiness Assessment | Business Value: Presentation readiness, data quality, and financial reporting reliability | Audit financial statements; assess management reporting depth; identify gaps in intangible asset documentation | Buyer due diligence uncovers issues first — destroys confidence and creates re-pricing risk |

Phase 2: Value Building | Hidden Asset Identification: evidence construction for each value driver | Document customer retention history; formalise supplier contracts; complete IP registration; reduce key-person dependency | Value drivers exist, but cannot be evidenced — buyers apply maximum risk discount |

Phase 3: Narrative Construction | Financial Storytelling; Value Communication Strategy; Buyer Perception Alignment | Build information memorandum; develop management presentation; model deal scenarios for each buyer archetype | Business is undervalued because its competitive advantages are never articulated in terms that buyers find credible |

Phase 4: Deal Execution | Deal Value Optimisation; Negotiation Value Drivers; managing competitive tension | Run a competitive process; manage buyer interactions; leverage competing interests to maintain price discipline and protect key terms. | Single-buyer process reduces negotiating leverage — price and terms deteriorate without competitive tension |

Real cases: where the strategy made the difference

Case 1 — Industrial distribution business (UK): An industrial distribution company owned by a family had earned a steady EBITDA of about £3.2 million over five years and was in the process of selling at an average of 6x earnings. The opening indicative bids from the buyers were at 4.55x, indicating concerns over customer concentration and the centrality of the owner to key relationships. An organised Pre-Sale Positioning programme was incorporated 14 months before the official process was initiated. The data on customer retention (91% revenue retention over five years) were compiled and validated independently. Three top managers were promoted to external customer relationship roles, thereby reducing perceived key-person risk. The company’s 30-year supplier relationships and its proprietary inventory management system formed a Value Communication Strategy. First-round bids when the formal process was launched were 6.8x EBITDA on average, and the final deal closed at 7.4x – a 65% increase on the original range of offers – and all this work was done by Deal Value Optimisation before the process was even launched.

Case 2 — Healthcare technology platform (Canada): A Canadian digital health company with rich clinical outcomes data had positioned itself mainly on its technology capabilities—a common sector approach —but this was yielding poor results with strategic acquirers because of its own technology platforms. An analysis of Buyer Perception Alignment revealed that the company had the most valuable asset of its kind, the clinical validation data that lay behind it: three years of outcomes data across 14,000 patient episodes, which none of the competitors possessed. Repositioning the Business Value Presentation around this data set and framing it as a regulatory and commercial moat, rather than a technical feature, shifted buyers’ interest. The two other strategic acquirers entered the process after the repositioning, and the final valuation was 34 per cent above the pre-repositioning indicative range.

Challenges and lessons for practitioners

Timing is the most stable challenge of the Seller Value Strategy work. Proprietors who shop the advisers by the time they are going to market have already lost most of their opportunity to build value. The facts that count: the company’s retention history, the depth of management, and formalised contracts that take 12 to 24 months to be credibly built out. Late entry implies making claims without evidence, and buyers will highly discount it.

- Financial Storytelling is only effective when the data behind the story is factual and verifiable on its own – when a compelling narrative is being told using weak evidence.

- The most frequent cause of value destruction in sales processes is the owners themselves, who do not create competitive tension but instead negotiate directly with buyers. Always have a structured process with more than two parties.

- Value Drivers of negotiation have to be identified and prepared in advance, and introducing new value arguments into the negotiation process at the very last moment is to lose credibility rather than gain it.

Where value is commonly lost in the sale process

Stage | Common Mistake | Value Impact | How to Prevent It |

|---|---|---|---|

Pre-market preparation | No formal Hidden Asset Identification — intangibles exist but are not documented or evidenced | Buyers apply maximum risk discount to undocumented value claims | Build intangible asset register 12–18 months before going to market |

Information memorandum | Financial focus without narrative — strong numbers but no coherent Business Value Presentation | Buyers cannot construct a compelling investment thesis — process generates limited interest | Invest in professional Financial Storytelling; lead with strategy, support with numbers |

Buyer engagement | Same pitch to all buyers — no Buyer Perception Alignment to different strategic priorities | The most relevant value drivers are buried — buyers miss the upside that would justify a premium | Develop tailored presentations for each buyer archetype before first meetings |

Negotiation | Single-buyer process — no competitive tension to support price discipline | Price and terms deteriorate progressively as the single buyer extracts concessions | Always run a competitive process with at least two to three credible bidders |

5. Conclusion: Actionable Insights for Sellers and Advisers

The valuation gap is not invariable. In most instances, it is the outcome of detectable breaches in the evidence, narrative, and process, which can be addressed through structured preparation. Companies that invest in Pre-Sale Positioning, develop a strict Value Communication Strategy, and implement a competitive deal process continue to achieve prices that reflect the actual quality of their businesses, rather than a buyer’s risk-adjusted estimate. The distinction between a 5x and a 7x exit is not always the business per se; it is the preparation that went into presenting it.

Practitioners in the M&A advisory, corporate finance, or business strategy sectors are among the most commercially valuable skill sets available on the market. These are not passively acquired skills; they need to be actively studied in how transactions are framed, how buyers think, and how value is communicated across the table.

Key takeaways

- Start Hidden Asset Identification at least 12 months before going to market – it takes time to build the evidence that buyers require to underwrite a premium price, and it cannot be retrospectively built.

- Buyer Perception Alignment is not a choice; a generic pitch leaves value on the table. Customise the story to each buyer’s strategic priorities, and the premium will follow.

- The most certain tool for Deal Value Optimisation is the competitive process itself. No preparation can substitute for the discipline that rival bids provide at the bargaining table.

Sellers who treat the sale process as a transaction and handle it at the last minute consistently underperform. Those who treat it as a strategic programme – starting with a strict Valuation Gap Analysis and ending with a strict competitive process – always close the gap between what their business is worth and what a buyer is willing to pay.

6. Conclusion

A balance sheet is less than the business’s value because a balance sheet was never intended to capture economic value; it was created to reflect historical cost. Off-Balance Sheet Value, in the form of Intangible Value Drivers, Growth Potential Valuation, Market Position Strength, and Business Moat Strength, is the actual driver of premium pricing in most private business transactions.

- The documented and evidenced Enterprise Value Drivers always attract higher multiples than the same drivers that are asserted but not documented and with no supporting evidence -the evidence gap is almost always higher than the underlying value gap.

- Things that are non-financial in the sense that they are presented as non-financial value factors, which must be presented alongside the financial data in such a way that ties each driver to a particular commercial outcome; those buyers who receive such an analysis would be more prone to price the business at the top of the valuation range.

- To owners: now is the time to start naming and documenting Off-Balance Sheet Value; to advisors: the information memorandum that unlocks a premium is the one that tells the complete story – financial and non-financial – with evidence that can be verified independently by the buyer.

Frequently Asked Questions

Q1. What is the valuation gap?

A valuation gap is the difference between what a business owner believes the company is worth and what potential buyers are willing to pay.

Q2. Why does a valuation gap occur?

It often results from unrealistic expectations, weak financial performance, insufficient documentation, or unrecognised business risks and intangible assets.

Q3. How can businesses reduce the valuation gap?

Businesses can improve profitability, strengthen financial reporting, document intangible assets, reduce operational risks, and obtain an independent valuation.

Q4. Who benefits from closing the valuation gap?

Business owners, investors, buyers, and advisers benefit from realistic valuations that support smoother negotiations and successful transactions.

Q5. How does professional valuation help?

Professional valuation provides an objective assessment of business value, helping owners justify pricing and improve buyer confidence.

2 thoughts on “Closing the Valuation Gap: How Sellers Can Showcase Hidden Business Value”