Table of Content

1. Introduction: How Buyers Use EBITDA Multiples When Acquiring a Business

If you ask any seasoned M&A advisor how the majority of private businesses in Australia are valued for sale, the answer will be: EBITDA multiples. Not because this is the only way to do it, not because it is the only way to get the right answer, but because it is the most familiar, most succinct and most comparable way to value private businesses. EBITDA Multiples Explained is simply: normalise the business’s earnings before interest, tax, depreciation, and amortisation (EBITDA) and multiply by a factor that represents what, in this market, and in this industry, and during this economic cycle, buyers are prepared to pay for those earnings. This gives you the enterprise value.

For early- and mid-career professionals in the M&A advisory world, the challenge is understanding EBITDA multiples. It involves understanding how and why multiples differ across industries and transaction sizes, how buyers choose which multiple to use, what the key element – the normalised EBITDA – measures, and how the Enterprise Value Calculation leads to an offer price that the buyer can justify to their management and the seller can accept as reasonable. These are the skills that distinguish transaction advisors from clerks.

This article explains how buyers use EBITDA Multiples Explained in a real deal, from the market benchmarking to the offer price. It explores how Earnings Normalisation works, what factors can move a multiple up or down within an industry range, the importance of using Comparable Transactions to ground the analysis, and the lessons learned from deals where multiples worked and where they didn’t.

2. The Mechanics: How EBITDA Multiples Work in Practice

From EBITDA to Enterprise Value Calculation

It seems so easy: Enterprise Value = Normalised EBITDA × Multiple. However, all parts of the formula must be carefully crafted. The normalised EBITDA must strip out any one-off items, owner add-backs, non-arm’s-length transactions, and any other items that skew the real, transferable earnings the buyer is buying. The multiple must be adjusted to the business’s attributes, not a sector average. And the Enterprise Value Calculation must then be adjusted for net debt, working capital, and other balance sheet items that impact the Equity value the seller will receive.

- Enterprise Value = Normalised EBITDA x Multiple (a Market-Based Valuation of the business operations, regardless of how financed).

- Equity Value = Enterprise Value – Net Debt +/- Working Capital (cash received by the seller after repaying any debt the business owes).

- $800,000 of normalised EBITDA x a multiple of 5x equals an enterprise value of $4 million; if the business has $300,000 of net debt, the equity value is $3.7 million.

Why Earnings Normalisation is the most important input

What matters most to the EBITDA multiple approach is not the multiple – it’s the earnings to which it is applied. Earnings Normalisation is the process of recasting the business’s EBITDA to reflect the post-acquisition earnings likely to be achieved, after allowing for all owner-specific and one-off items. Each dollar of defensible normalisation increases the price by the entire multiple. Likewise, every dollar of normalisation that can’t be documented or justified will be tested by the buyer’s advisors – and if it fails the test, the effective EBITDA base (and hence the price) reduces.

Examples of normalisation adjustments include remuneration to the owner at a rate above or below replacement cost, personal expenses paid through the company’s P&L, non-recurring legal or restructuring fees, rent charged by a related party at non-Arm’s-Length value, and revenue/cost items that are historical and relate to a specific period. The principle of Earnings Normalisation is to include only one-off adjustments that can be documented, not all adjustments that boost EBITDA.

3. How Buyers Select and Justify the Multiple

Valuation Benchmarking against market data

When a buyer uses a multiple, but lacks external justification, they have a number but not a price. Valuation Benchmarking against Comparable Transactions in the same sector is the key mechanism buyers use to determine what the market is currently valuing a business at with similar characteristics. This benchmarking process is more difficult in Australia than in other markets because there is less publicly available data on private transactions, but it can be done. Transaction data disclosed by brokers or publicly announced deals in related sectors all offer benchmarks.

- Industry Multiples Australia differ by sector: technology-enabled businesses and healthcare businesses trade at higher multiples than distribution, manufacturing or labour-hire businesses of the same size.

- Comparable Transactions need to be comparable: sector, size, earnings quality and how the deal is structured all affect the multiple, and adjustments should be made when the comparisons are not perfect.

- Buyers who have participated in several transactions in a sector gain expertise in building a database of Comparable Transactions and thus an information advantage over sellers and their advisors.

What moves the multiple within a sector range

Understanding the sector average multiple is not enough. The multiple of any given business will be higher, the same, or lower than the sector average, depending on a series of qualitative and quantitative factors that buyers evaluate. Knowing these factors helps buyers and sellers predict where a specific business will sit within the range and justify their position with facts.

Factor | Multiple Impact | Buyers’ Assessment Lens |

Revenue quality: recurring vs. transactional | High recurring revenue → premium multiple; purely transactional revenue → discount | Renewal rates, contract tenure, churn data, subscription/retainer proportion of total revenue |

Customer concentration | Any customer >20% of revenue → discount; diversified base → at or above average | Revenue by customer for the top 10; percentage attributable to the single largest customer; trend of concentration over time |

Management depth and owner independence | Strong team with demonstrated independence → premium; owner-dependent → material discount | Evidence that the business operates without the owner, management tenure and capability, key-person risk assessment |

EBITDA scale | Larger EBITDA typically commands higher multiples (lower absolute risk per dollar of earnings) | Buyers apply a size premium: a business with $3M EBITDA typically trades at a higher multiple than an identical business with $500K EBITDA |

Growth trajectory | Consistent growth → premium; declining or flat → discount or conservative multiple on trough earnings | Three-year revenue and EBITDA trend; explanation of any decline; forward pipeline evidence if growth is claimed |

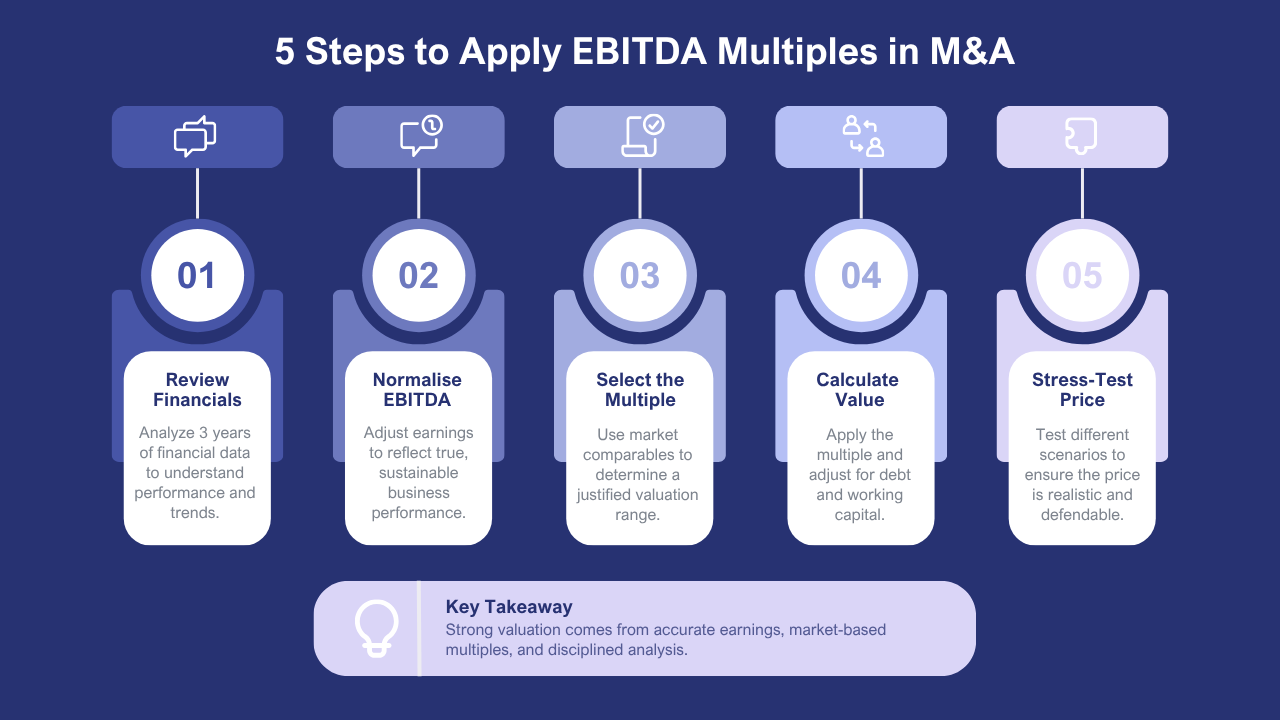

4. Five Steps Buyers Follow to Apply EBITDA Multiples Rigorously

The EBITDA multiple-based Acquisition Pricing Strategy is a disciplined, consistent process. The five steps outlined below are how disciplined buy-side teams use Deal Valuation Tools in the acquisition journey from screening to the final sale price.

Step | What It Involves | Why It Matters | Common Shortcut to Avoid |

1. Establish the Financial Metrics Analysis baseline | Obtain three years of financial statements; review management accounts; identify the current-year trading position; flag any unusual items for the normalisation process | Creates the raw data on which the entire valuation is built; without this, the EBITDA multiple is applied to an unverified number | Accepting management-provided financials without independent review; using the most recent year only, without examining the trend |

2. Earnings Normalisation | Reconstruct EBITDA from source documents; identify and adjust for owner add-backs, one-offs, and non-arm’s-length items; establish the sustainable, transferable earnings base | Every normalisation adjustment has a dollar-for-dollar impact on the price; the buyer’s independent normalisation is the most important financial due diligence step | Accepting the seller’s normalisation schedule without independent verification; applying the multiple before normalisation is complete and agreed |

3. Valuation Benchmarking and multiple selection | Research Industry Multiples Australia through sector reports and Comparable Transactions; identify the specific quality characteristics that position this business above or below the sector average; establish the buyer’s justified multiple range | Grounds the multiple in market evidence rather than buyer preference; allows the buyer to defend their price position under pressure from competing bids or seller pushback | Using benchmarks from non-comparable markets (e.g., US multiples for an Australian SME) without adjustment, applying a single point multiple rather than a range |

4. Enterprise Value Calculation and equity bridge | Apply the justified multiple to the normalised EBITDA; adjust for net debt, cash, and working capital to arrive at the equity value; present the implied offer price with the bridge clearly documented | Translates the Market-Based Valuation into a specific offer price that the buyer can submit and defend; ensures net debt and working capital are correctly captured | Applying the multiple to revenue or gross profit rather than EBITDA, failing to account for normalised working capital in the equity bridge |

5. Sensitivity and stress-test | Run the Enterprise Value Calculation under base, downside, and upside EBITDA assumptions; test the implied returns under each scenario; confirm the price works within the buyer’s return criteria. | Prevents buyers from overpaying based on optimistic assumptions that do not materialise post-acquisition; establishes the buyer’s walk-away price | Sensitivity analysis limited to a single variable; no testing of the impact if normalised EBITDA is challenged during due diligence |

It is at step 2 – Earnings Normalisation – that the multiple method is often misused. By relying on the seller’s normalisation without independent reconstruction, buyers are using the seller’s price anchor rather than analysing to determine whether it is valid. In practice, the independent normalisation process routinely reveals adjustments that lower the reported EBITDA by 10-30% – adjustments that have an immediate effect on the justified offer price. Independent Earnings Normalisation: Earnings normalisation is not only a risk management process; it is also the price-holding process.

5. Process, Real Cases, and Lessons for Practitioners

The buyer’s EBITDA multiple workflow

In a managed sale, the EBITDA multiple process runs from screening through the binding offer. It is updated through the flow of information from due diligence, rather than being fixed in advance. The following four-stage workflow reflects the buy-side best practice.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Screening & Initial Valuation | Due Diligence & Normalisation | Multiple Calibration | Final Offer & Negotiation |

Preliminary Financial Metrics Analysis of IM; initial Earnings Normalisation from available data; Valuation Benchmarking against Industry Multiples Australia; indicative Enterprise Value Calculation; submit non-binding indicative offer | Independent Earnings Normalisation from source documents; challenge seller’s add-backs; identify any downward adjustments; update Enterprise Value Calculation; assess Market-Based Valuation against current Comparable Transactions | Revise multiple positioning based on due diligence findings; document specific quality factors supporting premium or discount vs. sector average; stress-test price under multiple scenarios using Deal Valuation Tools | Submit a binding offer with documented Acquisition Pricing Strategy; present Valuation Benchmarking evidence; negotiate normalisation adjustments and any working capital mechanism; finalise price within the established return criteria |

Case 1: When normalisation determines the deal

A manufacturing company was put on the market at a price that implied a 5.5x multiple on the seller’s claimed normalised earnings before interest, taxes, depreciation and amortisation (EBITDA) of $1.1 million. The buyer’s advisors undertook an independent Earnings Normalisation. They identified three adjustments made by the seller which could not be fully justified: a rental add-back where the below-market rent was paid to a related party who would not be transferring the property to the buyer, a “one-off” legal cost that had been incurred in two of the three years considered and an owner remuneration adjustment which was in excess of the market value for a management role. The normalised EBITDA was $920,000 following these adjustments. The buyer then applied the same 5.5x multiple to the adjusted base, resulting in an offer of $5.06 million, not the $6.05 million the seller had anticipated. The Earnings Normalisation process, with its attention on the source documents, saved the buyer more than $990,000 – purely by rebuilding a number the seller thought finalised.

Case 2: Industry Multiples Australia calibration

A business services business with a speciality in compliance was initially valued by the seller-broker at 4x EBITDA, in line with industry multiples for generic business services entities. The buyer’s broker recognised that the business’s sub-sector (compliance software with embedded workflows) was trading at 7x to 9x in recent Comparable Transactions, reflecting high switching costs, recurring revenues, and the business’s product differentiation. The buyer made an offer at 7x, backed by a Valuation Benchmarking report that showed five disclosed transactions in the compliance software sector. The seller accepted the buyer’s bid at a multiple well above the broker’s indicative range, and the buyer’s return model remained valid at the higher multiple because the business’s quality (96 per cent gross retention, 3.2-year average contract length) justified the higher price. The example highlights a longstanding theme: Industry Multiples Australia ranges are guides, not absolutes, and the value of the particular business drives the appropriate multiple within the range.

6. Conclusion

EBITDA multiples are the most widely used Deal Valuation Tools in private M&A in Australia because they are efficient, transparent, and grounded in the market through Comparable Transactions and Valuation Benchmarking. However, their potential is only unleashed with rigorous inputs. Normalised EBITDA inputs that are independently verified, Industry Multiples Australia benchmarks that are comparable, Enterprise Value Calculation that correctly values the entire balance sheet – these are the technical inputs that distinguish an offer price that can be justified from a number that can’t.

For practitioners: spend money on the normalisation process, not on multiple discussions; a 10% error in EBITDA is equivalent to a 100% difference in the multiple. For buyers: know your Industry Multiples Australia range for your target sector before starting a process, and ensure you have the Comparable Transactions data to back up your position if the seller or their advisor questions your multiple.

Frequently Asked Questions

Q1. What is an EBITDA multiple?

An EBITDA multiple is a valuation metric that compares a company’s enterprise value to its Earnings Before Interest, Taxes, Depreciation, and Amortisation (EBITDA).

Q2. Why are EBITDA multiples used in acquisitions?

They provide a simple and widely accepted method for comparing businesses and estimating market value during acquisition transactions.

Q3. What factors influence EBITDA multiples?

Industry conditions, business size, profitability, growth prospects, market demand, competitive position, and transaction risks all influence EBITDA multiples.

Q4. Are EBITDA multiples suitable for every business?

No. While widely used, EBITDA multiples should be considered alongside other valuation methods to produce a comprehensive valuation.

Q5. How do professional valuers use EBITDA multiples?

Valuers analyse comparable companies, market transactions, and company-specific factors to determine an appropriate multiple and support reliable acquisition pricing.

1 thought on “How Buyers Use EBITDA Multiples When Acquiring a Business”