Table of Content

1. Introduction: Business Valuation Multiples

The highest noted premium in private market M&A deals is the technology premium. Businesses that have built Proprietary Technology Value into their operations, whether through purpose-built software, proprietary data assets, or secured intellectual property, trade at significantly higher multiples than comparable businesses generating equivalent earnings without those digital foundations. The gap is not simply accidental: it reflects a basic calculus for buyers that technology-enabled businesses can offer higher growth prospects, greater scalability, more defensible competitive positions, and lower marginal expansion costs than their non-technological counterparts.

To a business owner, it is a commercial imperative long before the thought of selling a business arises. Technology assets developed and reported as part of the regular operation of the business, but with no particular sale preparation in mind, will always generate the most plausible valuation premiums since they were developed not out of any particular sale preparation in mind, but rather because it was necessary to do so at some point in the regular operation of the business. Buyers differentiate between technology that actually supports the business model and technology characterised as proprietary to justify a higher asking price.

The article is directed at junior and mid-level professionals in advisory, technology strategy, and M&A roles who would like to understand why software, data, and IP create Tech Business Valuation premiums, how buyers examine and price these assets and what business owners ought to do to ensure their technology investments are properly recognised and valued in a transaction. These frameworks extend to software-enabled service businesses, SaaS and platform businesses, as well as traditional businesses that have developed technology-driven competitive advantages.

2. Why Technology Assets Command Premium Multiples

The scalability premium in Tech-Driven Valuation

Scalability is the primary reason technology assets attract higher multiples. Scalable Digital Assets portfolio enables a company to increase revenue without a corresponding rise in cost – the marginal cost of serving an extra customer via a software platform is a fraction of the cost of serving that extra customer via a headcount-dependent service model. This leverage is important to buyers because they can grow the earnings base they are acquiring much more rapidly, without the capital and management investment required by non-technology businesses.

- SaaS Valuation Multiples: The software delivery model is inherently scaled: once created, additional users can use the platform at virtually no marginal cost.

- Innovation Premium: technology companies are given a premium not only on current earnings but also on the anticipated trajectory of those earnings in the future – buyers model growth paths that mere non-technology businesses simply cannot plausibly support.

- Digital Competitive Advantage. The presence of proprietary technology in the business creates switching costs, network effects, and data moats, reducing competitive risk and lowering the buyer’s discount rate risk premium.

How buyers assess Proprietary Technology Value

When buyers assess a business’s technology resources, they apply a test: is the technology really proprietary, defendable, and transferable to new ownership? Technology that satisfies all three criteria earns the entire Innovation Premium. Generic (constructed using widely available platforms with no customisation), undocumented (known only to the developers), or personally licensed to the founder, technology is not. The evaluation procedure is strict, and buyers who seek the services of technical due diligence experts will notice the difference almost immediately.

3. Software, Data, and IP as Distinct Valuation Drivers

Software Valuation: from tool to asset

In a transaction context, Software Valuation is determined by whether the software is actually proprietary and whether it generates a defensible operational or competitive advantage. Scalable Digital Assets: Off-the-shelf software subscriptions have no standalone value in an acquisition; purpose-built platforms that automate core business processes, create network effects, or create switching costs for customers are valued as Scalable Digital Assets that reduce the buyer’s integration risk and support post-acquisition growth without proportional investment.

- SaaS Valuation Multiples SaaS companies with high growth and high retention: 6x to 12x ARR is typical of high-growth, high-retention SaaS businesses.

- In non-SaaS businesses that use embedded proprietary software, value is usually determined using a cost-to-recreate or relief-from-royalty method, pegged to the operational benefit the software provides.

Data Asset Value and the intelligence premium

One of the fastest-growing areas of Tech Business Valuation in the current market is Data Asset Value. Proprietary datasets accumulated over the normal course of business operations and not replicable within a short period of time create a type of Digital Competitive Advantage that is hard to acquire or replicate quickly. The value of a piece of data is based on its exclusivity, timeliness, granularity, and its direct ability to generate revenue or enhance decision-making.

The new dilemma facing advisory professionals conducting the Data Asset Value assessment is determining the true value of the data, not the business that created it. The most commercially plausible valuation method for proprietary datasets with quantifiable economic value is the income approach, which projects the incremental revenue or cost savings the data enables, discounted at a risk-adjusted rate. Where not, the cost-to-recreate methodology offers a bottom-up estimate that at least indicates that the information has positive economic value.

Intellectual Property Multiples: patents, trade secrets, and methodology

Intellectual Property Multiples indicate the legal security and economic exclusivity that the formal IP offers. Registered patents grant a temporary legal monopoly over the process or product being patented; trademarks protect brand recognition; registered designs protect aesthetic innovation; and trade secrets prevent the direct replication of a particular methodology and know-how. The individual categories of IP add different values to the Tech Business Valuation, and each category of IP requires a different evidentiary approach to prove the asserted value.

- Patents registered under the entity’s name, confirmed novelty, and a minimum of several years of remaining protection receive the highest direct Intellectual Property Multiples premium.

- Trade secrets and proprietary methodologies – which are not formally registered but are documented and secured by an obligation of secrecy – contribute to the Innovation Premium, provided buyers can confirm their protection and the competitive advantage they provide.

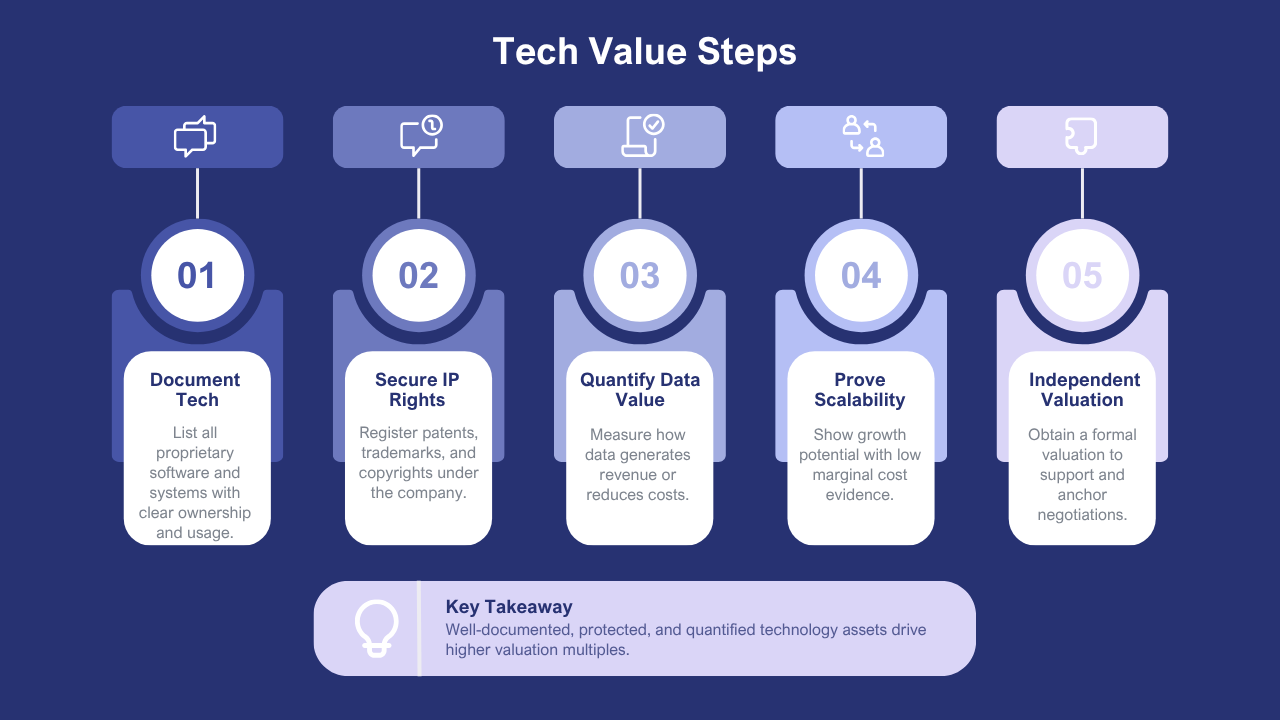

4. Five Steps to Build and Document Technology-Driven Valuation Premium

The technology premium a business would fetch in a sale directly correlates with the level of development, documentation, and protection of its technology assets. The five action steps below are the most profitable technology preparation actions that most businesses can afford to take during the 12-24 months before an intended departure.

Step | What It Involves | Tech-Driven Valuation Impact | Timing |

1. Document all proprietary software and systems | Prepare a technology asset register: list all proprietary software, confirm ownership in the entity’s name, document the functionality, the development history, and the operational dependency | Confirms Software Valuation basis to buyers; prevents disputes about what the business actually owns vs. what it licenses | Immediately: documentation is the prerequisite for everything else |

2. Formalise Proprietary Technology Value through IP registration | Ensure all patents are registered in the entity’s name; register trademarks for any branded technology or methodology; confirm software copyright is clearly assigned to the entity | Legally protects the Digital Competitive Advantage; removes the IP ownership risk discount buyers apply when registrations are informal or personally held | 3–6 months: registration processes have lead times; begin immediately |

3. Quantify the Data Asset Value | Identify all proprietary datasets; assess exclusivity, recency, and economic utility; document how the data generates revenue or reduces cost; prepare an income-approach or cost-to-recreate valuation for material datasets | Converts a qualitative “we have proprietary data” narrative into a documented, buyer-verifiable asset with a specific value attribution | 3‒6 months: requires structured analysis of data holdings and economic use cases |

4. Build the Scalable Digital Assets performance evidence | Document the scalability characteristics of the technology: revenue per user trends, marginal cost of serving additional customers, gross margin at different revenue scales | Supports SaaS Valuation Multiples or scalability premium arguments with historical evidence rather than forward projections only | Ongoing: this is operational data that should be tracked routinely; ensure it is available in a buyer-accessible format 6 months before marketing |

5. Commission an independent Tech Business Valuation for material assets | For technology assets that represent a significant proportion of the expected sale price, commission an independent valuation from a specialist with relevant sector credentials | Independent valuation provides the negotiating anchor that prevents buyers from substituting their own conservative estimate; it is most effective when the methodology and assumptions are documented to a standard that withstands technical due diligence | 6–12 months before going to market: sufficient time to respond to any valuer findings before the sale process begins |

The step with the longest lead time and the most irreversible consequences in the event of a delay is the formalisation of the Proprietary Technology Value through IP registration. Any IP ownership or ownership gaps identified during buyer due diligence cannot be resolved under transaction pressure in a manner that fully protects the seller’s value position. A registered patent or approved assignment of copyright made 12 months before the sale process, providing the seller with a clean, legally defensible ownership claim, and eliminates the discount offered by the buyer when they cannot themselves determine that what is being conveyed by the seller is what is actually owned by the seller.

5. Process, Real Cases, and Lessons

The technology valuation workflow

Live transaction Tech-Driven Valuation has a unique workflow that combines technical due diligence with financial analysis. The four-step process below is representative of how experienced advisors organise the technology asset assessment of a business in which software, data, or IP is a key driver of valuation.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Technology Asset Audit | Valuation & Benchmarking | Tech Due Diligence Preparation | Narrative & Negotiation |

Document all proprietary software, data assets, and IP; confirm ownership in entity name; assess scalability characteristics; identify any third-party dependencies or licensing gaps that reduce Proprietary Technology Value | Apply Software Valuation, Data Asset Value, or Intellectual Property Multiples methodology; benchmark SaaS Valuation Multiples against comparable transactions; prepare an independent valuation for material assets | Build technical documentation for buyer review: architecture diagrams, codebase ownership confirmation, data governance documentation; prepare responses to anticipated Tech Business Valuation challenges | Integrate Tech-Driven Valuation analysis into information memorandum; frame the Innovation Premium and Digital Competitive Advantage specifically for the most likely buyer category; defend technology valuation positions through to close |

Case 1: Data Asset Value that changed the transaction

An eight-year-old logistics technology business had spent eight years developing a proprietary database of freight rate benchmarks, carrier performance metrics, and route optimisation results, built on managing thousands of shipments. No internal value was ever assigned to the data, or it was formally described as an asset – it was merely an operating byproduct. When a strategic buyer entered the picture, their technology team identified the dataset as a top acquisition driver. There was no similar dataset on the market at the same level of granularity, and their technology team estimated the cost to duplicate it as three to five years of operational data collection. Using an income-based approach based on the incremental pricing premium, the data facilitated an analysis commissioned by the seller’s advisor, which yielded a figure of about $2.8 million based on the Data Asset Value. This was separately determined in the negotiation based on the enterprise value, calculated using EBITDA, and negotiated as a specific part of the valuation. The overall price of the transaction was greater than the initial indicative offer based on EBITDA by approximately $1.9 million.

Case 2: SaaS Valuation Multiples and the recurring revenue story

A software business compliance management team had developed a proprietary platform for a particular regulated industry. Recurring revenue was 1.4 million annually, with growth of 28 per cent per annum and a net retention rate of 114 per cent. Its former advisor had valued the business at 5x EBITDA – a typical service business multiple that did not in any way reflect its actual revenue model. The market benchmarks that could be used were 6x to 9x ARR, rather than 5x EBITDA, when an M&A advisor decided to reframe the business as a software platform with recurring revenue characteristics. A Tech Business Valuation analysis contrasting the business with disclosed transactions in the compliance software category supported the reframing. The final transaction value would have been around 7.2x ARR – significantly higher than the 5x EBITDA model would have delivered, and all entirely reasonable upon the Scalable Digital Assets profile of the business demonstrated.

6. Conclusion

Software Valuation, Data Asset Value, and Intellectual Property Multiples are not abstract concepts limited to Silicon Valley unicorns. They exist in all businesses that have developed proprietary technology, unique information, or a secure methodology that creates true Digital Competitive Advantage. Those businesses that have documented, protected and quantified these assets before the arrival of any buyer are the ones that capture the full Innovation Premium in a transaction.

For owners: start the technology asset audit today; register what can be registered; quantify what can be quantified. To advisors: reframe businesses that use technology through the correct lens of Tech-Driven Valuation before any interaction with a buyer. The difference between a 5x EBITDA result and an 8x ARR result of the same business is virtually always a difference in the framing and documentation of such a result, rather than a difference in the result itself.

Frequently Asked Questions

Q1. Why are software and data valuable business assets?

Software platforms, proprietary databases, and digital assets can generate recurring income, improve efficiency, and create long-term competitive advantages.

Q2. How do software businesses differ from traditional businesses?

Software businesses often have scalable revenue models, recurring subscriptions, and significant intangible assets that influence valuation multiples.

Q3. What are valuation multiples?

Valuation multiples compare financial metrics such as revenue or EBITDA with comparable businesses to estimate market value.

Q4. Why do software companies often receive higher multiples?

Strong growth potential, recurring revenue, high margins, and scalable business models often justify higher valuation multiples.

Q5. How does professional valuation improve pricing accuracy?

Professional valuers analyse market comparables, financial performance, and business-specific risks to determine appropriate valuation multiples.

1 thought on “How Software, Data and IP Increase Business Valuation Multiples”