Table of Content

1. Introduction: Valuing Customer Relationships

In most service-sector and B2B business transactions, the most valuable item being sold is not the furniture, the IT infrastructure, or the brand name. Customer base is the grouping of relationships, contracts and sources of revenue that a buyer is buying the right to sustain and grow. Customer Relationship Valuation and Contract Value Assessment are the core of how these transactions are priced, yet they are among the least understood aspects of the private M&A valuation process. A buyer who knows how to appreciate customer relationships and a seller who does not is a buyer with huge bargaining power.

For practitioners who have moved into the advisory/corporate finance community, the ability to value Customer-Based Intangibles is a real point of differentiation. The methods of quantifying the value of a customer base – Multi-Period Excess Earnings, Customer Lifetime Value modelling, Contractual Cash Flows analysis – are the same methods used by professionally acquiring companies, auditors carrying out purchase price allocation exercises, and litigation experts opining on the value of customer relationships in a dispute. A thorough grasp of these methods enables practitioners to make constructive contributions to discussions that most advisory clients find significant and daunting.

The article is targeted at business owners planning to make a sale who want to know how buyers will evaluate and value their customer base, and at junior professionals building technical capability to value customer bases in the customer intangibles space. It discusses the main valuation approaches applied to Customer-Based Intangibles, the information and analysis needed to support a credible valuation, and the real-world lessons from transactions in which the customer relationship value was either well-captured or poorly presented.

2. Why Customer Relationships Are Valued as a Distinct Intangible Asset

The commercial rationale for Customer Relationship Valuation

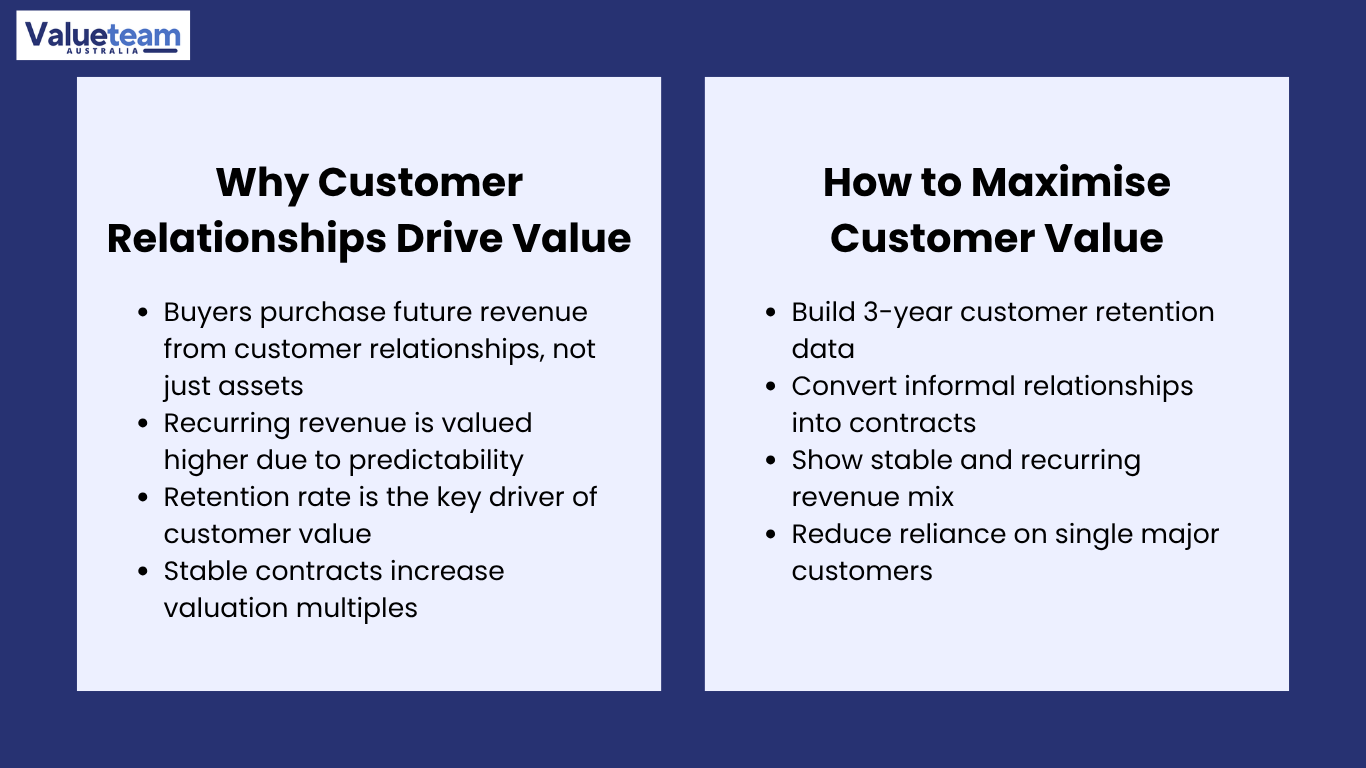

When a buyer buys a business, he is not buying a generic stream of earnings – he is buying particular economic relationships between identifiable customers. The expected duration of their existence determines the worthiness of such relationships, the revenue and profits they will generate for the new owner, and their transferability. Customer Relationship Valuation measures this economic benefit differently from overall business earnings because the customer base is an identifiable intangible asset that can be recognised separately in a purchase price allocation exercise under AASB 3.

- Customer-Based Intangibles satisfy the separability requirement of AASB 3: they can be separated from the business and sold, licensed, or transferred alone.

- Recurring Revenue Valuation is higher than transactional revenue valuation because the predictability of future cash flows is higher, which decreases the risk discount used.

- Customer Relationship Valuation: The most important input in any valuation of customer relationships is Client Retention Metrics: the rate at which the customer base decays over time.

The link to Revenue Stability Analysis

Revenue Stability Analysis is a fundamental aspect of due diligence because the quality of the revenue base directly influences both the valuation multiple applied and the assigned value to customer relationships. A business whose 70 per cent of revenues are held by clients who have signed formal multi-year contracts with the business, i.e., showing high Contractual Cash Flows stability, will be valued materially higher than a peer with identical absolute revenues but primarily project-based or transactional revenues. The Revenue Stability Analysis provides the quantitative basis for the customer relationship valuation: it demonstrates how stable the cash flow generation really is and how much of the customer base’s projected future earnings can be discounted to present value with confidence.

3. The Core Methods for Valuing Customer Relationships

Multi-Period Excess Earnings: the primary professional method

Combining the Multi-Period Excess Earnings (MEEM) method with the Multi-Period Excess Earnings (MEEM) method is the most widely accepted approach to valuing customer relationships in a formal intangible asset valuation setting. The rationale behind it is simple: the customer relationship generates a stream of revenue, which in turn generates earnings, and the earnings specifically attributable to the customer relationship are the result of subtracting a reasonable return on all the other assets that go to generate them. The fair value of the customer relationship is the present value of the excess earnings of the relationship over its remaining life.

- The so-called contributory asset charges (CACs) charged off in the Multi-Period Excess Earnings calculation represent a fair return on tangible assets, working capital, workforce, technology, and other intangibles that contribute to the generation of customer revenue; only the residual can be attributed to the customer relationship.

- In the case of the excess earnings stream, the discount rate reflects the risk associated with the customer relationship in that instance, which is usually larger than the overall business WACC to account for the attrition risk inherent in the projection.

- The most sensitive and most challenging input in any Multi-Period Excess Earnings model is the customer attrition rate.

Customer Lifetime Value and Contract Value Assessment approaches.

Customer Lifetime Value (CLV) models are a valuation approach that assigns a value to individual customers or customer groups based on the expected duration of the relationship. This is especially effective in situations where the customer base has distinct segments, such as different tenure, different revenue levels, different attrition characteristics, etc., which a single aggregate attrition rate would distort.

Contract Value Assessment is best applied where the business has formal, dated, quantified contracts with particular customers – service agreements, subscription contracts, or long-term supply arrangements. Contractual Cash Flows in such cases may be projected directly from the contract terms, with a probability adjustment to account for early termination or non-renewal. The Contract Value Assessment approach is more justifiable than attrition-based projections in due diligence, as cash flow projections are based on legal commitments rather than statistical estimates.

Valuation Method | Best Applied When | Primary Input | Key Limitation |

Multi-Period Excess Earnings (MEEM) | Most service and B2B businesses prefer the method for purchase price allocation, which is widely accepted by auditors and courts | Three-to-five year customer-level revenue data; historical attrition rates; contributory asset charge schedules | Attrition rate assumption is contested; CAC selection requires judgment; sensitive to discount rate |

Customer Lifetime Value (CLV) | Businesses with clearly differentiated customer segments or cohorts, subscription and SaaS businesses with cohort-level data | Customer-level revenue, cost-to-serve, and attrition data by cohort; customer acquisition cost | Requires granular customer data often unavailable in the SME context; model complexity can obscure rather than clarify |

Contract Value Assessment | Businesses with formal, quantified, long-term customer contracts; project-based businesses with backlog | Executed contract schedules with term, value, and renewal terms; probability of renewal or early termination | Only captures contracted revenue; does not value the broader relationship beyond the current contract term; requires contracts to be assignable |

Intangible Asset Pricing (Cost Approach) | As a floor check, where the income approach inputs are unavailable | Customer acquisition cost, retention investment, and time to recreate the customer base | Understates the economic value of a mature, retained customer base; does not reflect the earnings power of the existing relationships |

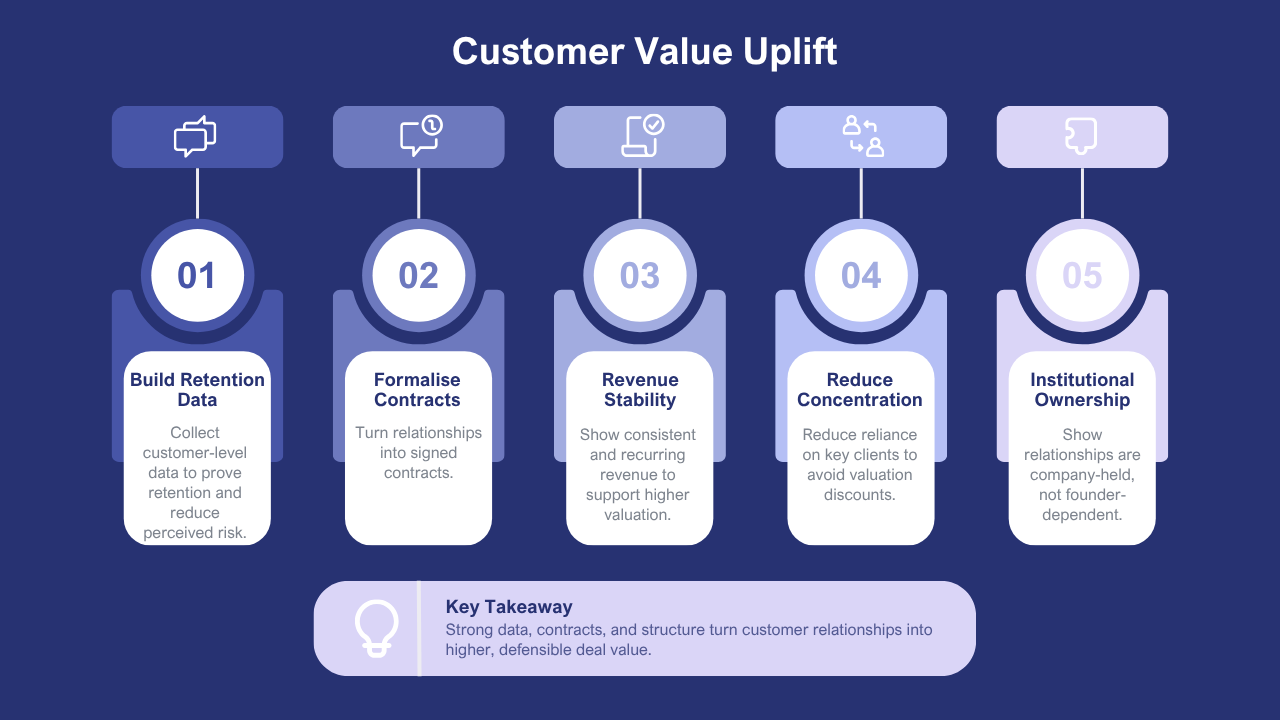

4. Five Steps to Document and Maximise Customer Relationship Value

The difference between a business that qualifies for full Customer Relationship Valuation credit in a sale and one that does not is almost always in preparation and documentation, rather than in underlying value. The five steps shown below are how seasoned advisors assist the sellers in constructing and presenting the customer relationship case.

Step | What It Involves | Why It Matters for Customer Relationship Valuation | Common Gap |

1. Build the Client Retention Metrics database | Compile at least three years of customer-level revenue data showing which customers have been retained, what they spend, and whether that spend has grown or declined; calculate attrition rate, average tenure, and revenue-weighted retention | The attrition rate is the most important single input in any customer relationship valuation; a well-documented, historically consistent retention record supports a lower attrition assumption and a higher value | No customer-level data system; attrition estimated from memory rather than records; retention calculated at account level rather than revenue level, which can mask the departure of high-value clients |

2. Formalise Contractual Cash Flows | Where customer relationships are currently informal, convert to written service agreements before going to market; ensure existing contracts are current, signed, and contain no undisclosed termination rights or change-of-control provisions | Formal contracts convert informal Client Retention Metrics into documented Contractual Cash Flows that buyers can verify; they also strengthen the transferability of the relationship | Customer relationships are maintained on a verbal or informal basis; contracts exist but have expired or are unsigned; change-of-control clauses are not checked for assignability |

3. Conduct Revenue Stability Analysis | Analyse the revenue base by customer tenure, contract type, and renewal pattern; segment into contracted, recurring but informal, and transactional revenue; demonstrate consistency across the prior three years | Buyers price Recurring Revenue Valuation at a premium over transactional revenue, demonstrating that the proportion and stability of recurring revenue directly affects the multiple applied to the earnings base | Revenue categorised by product line rather than revenue type; no distinction between recurring and transactional revenue in management accounts; no analysis of renewal patterns |

4. Address concentration risk | Identify any customer representing more than 15–20% of total revenue; take action to reduce concentration where time permits; prepare documentation showing the depth of the relationship where concentration cannot be reduced | Concentration risk is one of the primary attrition assumptions buyers challenge; a single large customer whose departure would materially affect the business commands a specific, material discount | Concentration acknowledged but not addressed; no documentation of the depth or contractual basis of the concentrated relationship; no evidence of steps taken to diversify |

5. Demonstrate institutional relationship ownership | Show that customer relationships are held by the team and the systems rather than by the owner personally; CRM records showing distributed relationship management; evidence that customers have dealt with multiple team members | Institutional relationship ownership supports a lower buyer-perceived attrition risk post-transaction; personal relationship ownership creates a specific risk that buyers price as a discount to the Customer Relationship Valuation | CRM data exists only in the founder’s email or head; no documented relationship history for key accounts; key customers cannot be identified who interact with anyone other than the founder |

The step most directly related to the test of transferability that all buyers use is step 5: demonstrating institutional relationship ownership. The question is not whether the relationships exist, but whether they will continue to exist after the founder’s direct involvement decreases or is eliminated. The preparation work that most directly discounts the attrition discount a buyer will impose on the Multi-Period Excess Earnings calculation is building evidence that they will, through CRM documentation, distributed account management, and verifiable customer interactions with multiple team members, perform.

5. Process, Real Cases, and Lessons for Practitioners

The customer relationship valuation workflow

The Customer Relationship Valuation process in a live transaction is a four-phase process that must be included in the entire sale preparation process. The data on attrition driving the model requires at least three years of customer-level records – records that simply cannot be assembled under transaction pressure unless these records already exist in a usable form.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Data Assembly | Methodology Selection | Model Build & Sensitivity | Presentation & Due Diligence |

Compile three-plus years of customer-level revenue data; calculate historical attrition rates and average tenure; segment by contract type for Revenue Stability Analysis; identify concentration risks | Select primary valuation approach: Multi-Period Excess Earnings for a broad customer base; Contract Value Assessment where formal contracts dominate; Customer Lifetime Value for segmented cohort analysis | Build the customer relationship valuation model; apply contributory asset charges; stress-test attrition assumption across a realistic range; prepare sensitivity analysis showing the impact of higher and lower attrition scenarios | Present Intangible Asset Pricing analysis in information memorandum; prepare responses to buyer challenges on attrition assumption; support purchase price allocation discussion with documented methodology; defend Contractual Cash Flows position |

Case 1: Attrition data that changed the valuation

A managed services business was being acquired, and the advisors of the acquiring company used a 15 per cent per year attrition assumption in their Multi-Period Excess Earnings model, based on an industry benchmark of similar businesses for which no specific data were available. The seller’s advisor compiled three years of client-level revenue records, demonstrated that the actual trailing attrition rate was 6 per cent per annum, and supported this with a detailed schedule of Client Retention Metrics showing retention of 47 identified client accounts. The Customer Relationship Valuation, created by the seller’s advisor based on a 6 per cent rate, yielded a value about $1.1 million higher than the analysis conducted by the buyer based on a 15 per cent assumption. The buyer had taken the lower rate with a slight modification. After considering the underlying data and the record of attrition evidenced, they could not easily disregard it. The difference between the purchase price actually paid and the price that would have been paid had the seller not prepared the data was about 800,000 in the buyer’s favour.

Case 2: Contractual Cash Flows that accelerated the deal

An example of a B2B software business that had invested over 14 months in formalising its customer relationships before going to market had 18 of its 22 significant accounts converted to signed 3-year service agreements with auto-renewal. When buyers reviewed the Contract Value Assessment during due diligence, the contracted revenue base accounted for about 82 per cent of total annual revenue, compared with about 34 per cent pre-formalisation programme. The Recurring Revenue Valuation of the contracted base by far outpaced what would otherwise have been possible with primarily informal arrangements. Due diligence was completed in five weeks, which is about three weeks less than for similar transactions, as the Contractual Cash Flows had been fully documented and the buyer could directly verify the revenue projections against executed contracts. The valuation multiple finally offered by the buyer was 1.2x the original indicative range, directly due to the contracted revenue quality.

6. Conclusion

CRV and CVA are not marginal additions to a business sale; they are among the most commercially important factors that will determine the final price in most service and B2B business acquisitions. Both the Multi-Period Excess Earnings methodology, the Customer Lifetime Value model, and the Contractual Cash Flows approach provide structured, defendable ways to quantify what buyers are actually buying: the right to continue generating economic benefit from the relationships the seller has created. The most disputed input is the attrition rate, and data that substantiates a lower rate is the most valuable preparation a seller can make.

To business owners: build the Client Retention Metrics database now, formalise customer relationships in written agreements, and demonstrate in CRM records that relationships are institutional, not personal. To advisors: the customer relationship analysis,s which safeguards the price of a seller, does not come out during the negotiation – it is created in the preparation phase, which utilises data that must already exist before any buyer shows up. Recurring Revenue Valuation is a reward based on documented stability; the work is the documentation.

Frequently Asked Questions

Q1. Why are customer relationships valuable?

Customer relationships generate recurring revenue, improve business stability, and contribute significantly to long-term business value.

Q2. Can contracts be recognised as intangible assets?

Yes. Long-term customer contracts and contractual relationships may qualify as identifiable intangible assets in certain transactions.

Q3. When are customer relationships commonly valued?

They are frequently valued during mergers, acquisitions, Purchase Price Allocation (PPA), and financial reporting engagements.

Q4. Which valuation methods are commonly used?

Professionals often apply income-based valuation methods that estimate the future economic benefits generated by customer relationships.

Q5. How does customer relationship valuation benefit businesses?

It provides a more complete assessment of business value and supports accurate financial reporting and transaction pricing.

2 thoughts on “Valuing Customer Relationships and Contracts in a Business Sale”