Table of Content

1. Introduction: How to Value a Business Before Selling

The sale of a business is likely to be the most significant financial decision most business owners make, and one of the most common errors is selling without knowing what their business is actually worth. A Pre-Sale Business Valuation is not a starting point for a negotiation; it is a driver of how the sale is structured, who the buyer pool should be, and what steps can be taken in the months leading up to a sale to increase the sale price. Without this, they either sell for less than they’re worth or alienate potential buyers.

The valuation of Business Worth Australia in the context of an impending sale is not based on a multiple of last year’s EBITDA; the size of the business determines the multiple. It requires a Financial Performance Review, an objective appraisal of the business and what makes it attractive to others, and a realistic expectation of the risks that buyers will use to price the business against you. The best Seller Valuation Strategy is one that is rooted in reality, not hope – and it is formulated before the sale is commenced, not during it.

This is a book for business owners selling their businesses, for junior advisors looking to develop their understanding of the transaction advisory service delivery and for anyone looking to understand what a professional Pre-Sale Business Valuation is. It explores the main valuation approaches commonly used in Australian private market transactions, the steps owners should follow in preparing and the mistakes that can cost money on the day.

2. Why Pre-Sale Valuation Changes the Outcome

Valuation as strategic intelligence

Pre-Sale Business Valuation, done 12 to 18 months before sale, provides an opportunity that a transaction valuation cannot: it allows the owner to respond. Every valuation reveals positive or negative value drivers: concentrated customers, owner-dependency, fluctuating margins, or unrecorded intellectual property. Armed with this knowledge, owners can resolve issues before buyers use them to justify discounts.

- Surface the value drivers that buyers are willing to pay for: recurring revenue, broad customer base, contracted customers, and scalable processes.

- Reveals the value detractors that buyers will leverage to negotiate lower prices: key-person risk, lack of documented processes, concentration risk, and outdated equipment.

- Sets a price benchmark that the owner can hold fast to in negotiation, supported by a documented process rather than opinion.

The timing advantage

An Exit Planning Valuation done in a rush (weeks before the business goes on the market) results in a valuation that reflects the situation as it stands, with no room for improvement. By conducting the same process 18 months in advance, the owner has time to address issues with financial records, spread risk across customers, document critical contracts, and establish a management team to reduce the business’s reliance on the owner’s personal connections. The outcome from the sale of a business that has been prepared for sale is consistently different from that of a business that has not been prepared for sale, often by 20 to 40 per cent of the sales price.

3. How Australian Businesses Are Valued: The Core Methods

The dominant approach: EBITDA multiples

The most common Valuation Method in Australia for most SME and mid-market deals is the EBITDA multiple. Here, the enterprise value is determined by normalising EBITDA and applying an appropriate multiple. The multiple factors in the market, the sector, and the business’s quality. Current EBITDA multiples for SME transactions in Australia range from 3x to 7x, with technology-enabled, high-recurring-revenue, and healthcare businesses at the top end.

- EBITDA Normalisation is the critical input – it cleans the reported EBITDA for one-off items, owner add-backs and non-arm’s-length transactions to give the true transferable earnings potential of the business.

- The multiple is driven by the buyer’s view of the business’s risk and growth potential – a company with high recurring revenue and strong management teams will command a higher multiple than one with erratic earnings and owner dependence.

- Market Value Assessment based on comparable transactions is an external data source for multiples (e.g., industry reports, broker-deal disclosures, IBISWorld data).

When other methods apply

EBITDA multiples are most common, but advisors use other valuation methods to cross-check. Discounted cash flow (DCF) can be applied to high-growth or capital-intensive businesses with future earnings potential well above current earnings. An assets-based computation can be used to estimate a minimum value for asset-intensive businesses. In reality, the best valuations combine two to three approaches and cross-validate them.

Valuation Methods Australia | How It Works | Best Suited For | Owner’s Consideration |

EBITDA Multiple (primary) | Multiply normalised EBITDA by a sector-comparable multiple; the headline method in most private market deals | Profitable businesses with two or more years of stable earnings | Focus on EBITDA Normalisation — every dollar of defensible EBITDA added multiplies into the sale price |

Discounted Cash Flow | Project future free cash flows and discount to present value at a risk-adjusted rate | High-growth, capital-intensive, or pre-profitability businesses | Growth assumptions must be substantiated by evidence; buyers will discount unsupported projections |

Asset-Based (floor value) | Value identifiable tangible and intangible assets at fair market value; less accumulated liabilities | Asset-heavy businesses; manufacturing; property-related operations | Useful as a floor check; rarely the primary method for a going-concern service or technology business |

Comparable Transactions | Benchmark against disclosed multiples from recent comparable sales in the same sector | Businesses in sectors with active M&A activity and available transaction data | Australian private data is thin; use with caution and supplement with sector-specific broker intelligence. |

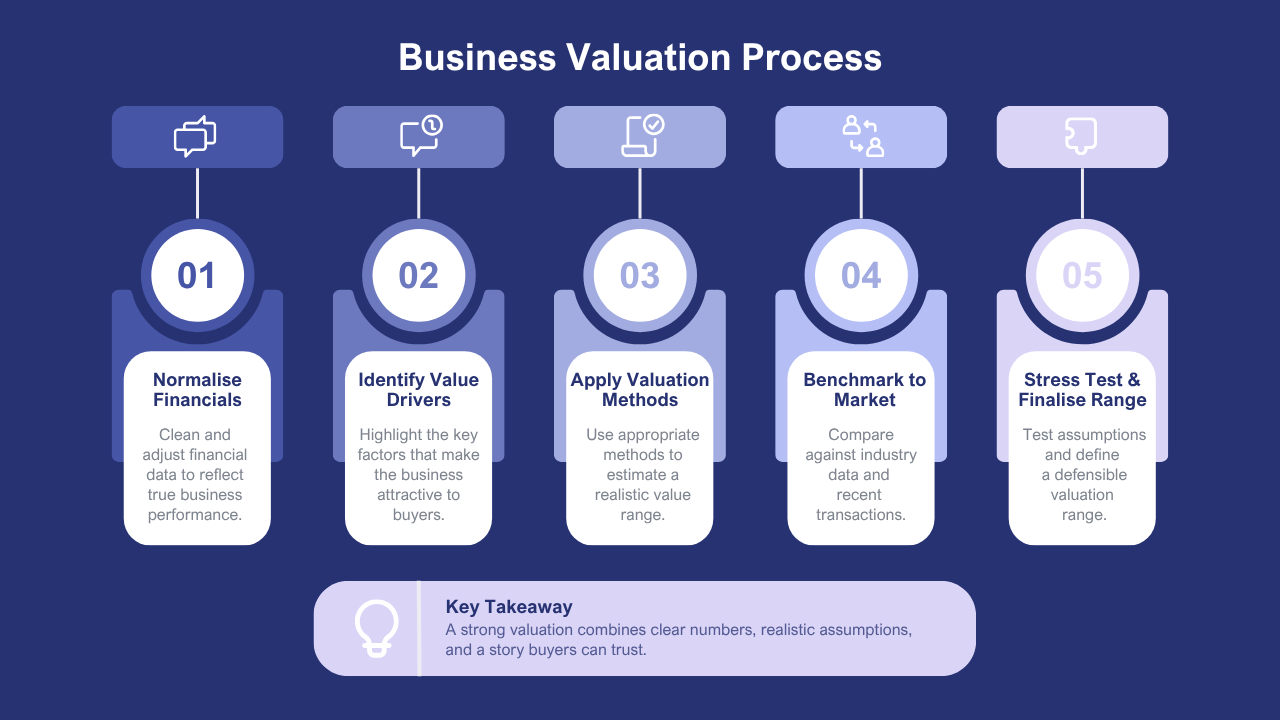

4. Five Steps to Maximise Value Before Going to Market

Owner Value Maximisation before a transaction is not about enhancing performance, but rather creating a business that is as good as possible when the buyer looks at it. The five steps below are the highest-value preparation activities an owner can undertake in the 12-18 months leading up to the planned sale.

Step | What It Involves | Impact on Value | Common Owner Mistake |

1. Commission a Pre-Sale Business Valuation | Engage a qualified independent valuer to produce a formal valuation; understand the methodology, the value range, and the specific factors that are suppressing the outcome | Establishes the negotiating anchor; identifies value improvement opportunities; reduces information asymmetry with buyers | Relying on broker opinion or rules-of-thumb rather than a methodology-supported valuation, arriving at a market price expectation before understanding how the business is actually valued |

2. EBITDA Normalisation and Financial Clean-Up | Reconstruct three years of accounts to remove owner add-backs, personal expenses, one-off items, and non-arm’s-length transactions; engage an accountant to prepare a sell-side quality-of-earnings analysis | Every dollar of defensible normalised EBITDA added translates directly into multiple times that value at exit; clean accounts reduce the buyer’s risk discount | Mixing personal and business expenses through the P&L; failing to document add-backs with supporting evidence; leaving reconciliation differences unresolved in the accounts |

3. Reduce key-person and concentration risk | Diversify the customer base if any single customer exceeds 20% of revenue; build and document a capable management layer; formalise systems and processes so the business operates without the owner | Reduces the risk premium buyers apply; broadens the pool of potential acquirers; may increase the multiple by 0.5–1.5x | Waiting until the sale process begins to address these issues, by which point there is no time to implement changes; buyers then use concentration risk as their primary price negotiation lever |

4. Business Sale Preparation: legal and contractual housekeeping | Ensure all customer contracts are current and assignable; formalise supplier agreements; check lease terms for change-of-control clauses; confirm IP is registered in the entity’s name and fully transferable | Prevents price chips in due diligence; reduces buyer’s perceived risk; accelerates the due diligence timeline | Discovering undocumented arrangements, expired contracts, or transferability issues during buyer due diligence, rather than proactively, by which point the seller is in a weakened negotiating position |

5. Develop the sale narrative | Articulate the business’s strategic value proposition: why this business, why now, and what growth potential exists for the right acquirer. Prepare an information memorandum that tells this story with evidence | .Attracts the right buyer category (strategic vs. financial); positions the business for a competitive process; supports a premium over the baseline EBITDA multiple. | Preparing a generic document that describes what the business does, rather than explaining why it is a compelling acquisition for a specific buyer type |

Step 2 – EBITDA Normalisation – is important because it is the most important and misunderstood preparation activity. Owners tend to assume that their “real” earnings are transparent to the buyer. In reality, the buyer and his or her due diligence advisors will build the normalised EBITDA from the bottom up – and unless the owner has pre-documented and substantiated his or her adjustments, the buyer will apply a conservative analysis. A quality-of-earnings report and opinion prepared by the seller’s accountant and disclosed early in the process sets the normalisation narrative and blocks the biggest source of value destruction in the due diligence process.

5. Process, Real Cases, and Lessons for Sellers

The valuation-to-sale workflow

Business Sale Preparation (BSP) has a sequence. Knowing where the critical decision-making points lie – and what might happen if things go wrong – is valuable information for owners and their advisors.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Valuation & Gap Analysis | Value Improvement (12–18 months) | Market Preparation | Sale Process & Negotiation |

Commission Pre-Sale Business Valuation; conduct Financial Performance Review; identify value gaps and preparation priorities; establish a realistic Business Worth Australia price range | Implement EBITDA Normalisation clean-up; reduce concentration and key-person risk; formalise contracts and IP; build management depth; document operational systems for Owner Value Maximisation | Engage M&A advisor; prepare information memorandum; apply Seller Valuation Strategy; identify target buyer list; commission updated Market Value Assessment before going to market | Manage buyer engagement; respond to due diligence using prepared documentation; defend normalised EBITDA with sell-side quality-of-earnings analysis; close at or above the targeted Valuation Methods Australia range |

Case 1: The value of early preparation

A professional services company began a Pre-Sale Business Valuation 20 months before its planned sale. The Pre-Sale Business Valuation highlighted two problems: (a) the owner personally controlled 65 per cent of the client relationships and (b) the business had a single client that accounted for 38 per cent of revenue. The owner invested 15 months in transferring client relationships to two senior staff members and diversifying the revenue stream. When the business was re-listed, the Market Value Assessment prepared by the prospective buyer’s advisors showed that the client relationships were institutional rather than personal, and that the revenue concentration had been diversified to 22 per cent. The business sold for 1.7 times the original indicative price, a return on investment unavailable to the owner.

Case 2: EBITDA Normalisation under pressure

An industrial company offered a broker-prepared indicative price for a business based on three years’ accounts. The accounts contained substantial owner add-backs that were not previously documented: personal motor vehicle expenses, excessive director salaries, and a property lease at an arm ‘s-length market rate. During their detailed Financial Performance Review, the buyer’s advisors recalculated the EBITDA, achieving a normalised EBITDA that was around 28% lower than the seller’s, and claimed the documentation for add-backs was insufficient. The seller lacked a sell-side quality-of-earnings analysis to counter this evidence. The sale price was based on the adjusted EBITDA. The lesson is a common one: Pre-sale EBITDA Normalisation documentation is money well spent.

6. Conclusion

In Australia, the process of selling a business begins months before it is put up for sale. The three essential investments that distinguish sellers who get their price from those who don’t start with a rigorous Pre-Sale Business Valuation, a disciplined EBITDA Normalisation and a Business Sale Preparation process. The Seller Valuation Strategy that works is one backed by data, done in advance, and based on a methodology that will stand up to buyer scrutiny.

For owners: begin the valuation process 12 to 18 months before the sale. For advisors: the most valuable service you can provide to a client is to help her/him understand the value of their business now – and what they can do to bridge the gap between their expectations and reality. Owner Value Maximisation is not a lottery; it is preparation, done in a timely way.

Frequently Asked Questions

Q1. Why should a business be valued before selling?

A business valuation helps owners understand the company’s fair market value, establish a realistic selling price, and improve negotiation outcomes.

Q2. Which factors influence business value?

Business value depends on profitability, cash flow, assets, liabilities, market conditions, customer relationships, growth potential, and industry performance.

Q3. Which valuation methods are commonly used?

Professional valuers commonly apply the Income Approach, Market Approach, and Asset-Based Approach to estimate business value.

Q4. How can owners maximise business value before selling?

Owners can improve financial performance, strengthen operations, maintain accurate records, reduce risks, and demonstrate sustainable business growth.

Q5. How does professional valuation support business sales?

An independent valuation provides objective evidence that supports negotiations, builds buyer confidence, and facilitates successful business transactions.

1 thought on “How to Value a Business Before Selling in Australia: A Practical Owner’s Guide”