Table of Content

1. Introduction: What Makes a Business More Valuable Than Its Balance Sheet?

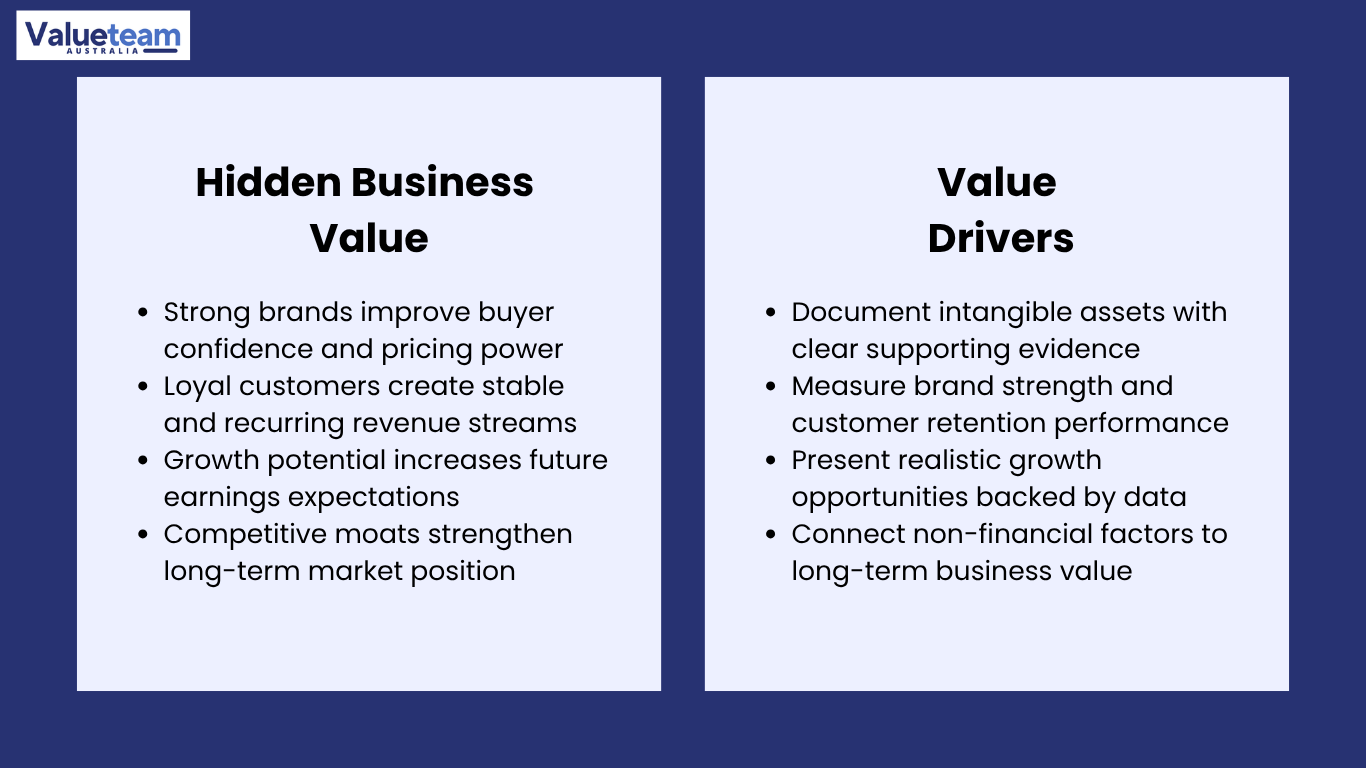

Take up the balance sheet of practically any private business, which has just been sold at a premium price, and you will find the same thing: the value of the transaction is far in excess of the net assets on the page. It was not the contents of the books the buyer purchased, but rather what the books simply failed to capture. The accumulated competitive position, customer loyalty, market reputation, and growth potential, which we never designed financial statements to capture, are always the largest part of the premium that sophisticated buyers pay. What motivates it, how buyers evaluate it, and how sellers can surface it are among the most commercially significant attributes of knowledge in M&A advisory.

This difference has immediate financial implications for business owners. A business that has developed true Intangible Value Drivers but has never identified or documented them will be valued only by buyers at its earnings multiple – the floor of what it is worth. A business whose owner has explained and proven those drivers will sell at a premium above that floor, since buyers will have a specific, defensible reason for paying more. The distance between the floor and ceiling is nearly a gap in evidence, but not in values.

This article explains what makes a business worth more than its balance sheet, how the most significant Non-Financial Value Factors are identified and evaluated and what the practical steps are to surfacing Off-Balance Sheet Value in a manner that translates into a higher transaction price. These structures are relevant both to how a buyer actually thinks about what he is buying and to how an advisor helping a client position his business thinks about what he is being offered.

2. Why the Balance Sheet Systematically Understates Business Value

The accounting convention that creates the gap

Accounting standards mandate that assets be recognised at cost and allow capitalisation of internally generated intangibles only under special conditions. This implies that the most valuable assets of a business which are a customer base that has been developed over 15 years, a brand reputation that has taken decades to be built, a proprietary process that creates operational advantage, a workforce culture that retains talent above market are carried at zero or at a cost basis which reflects how much it has spent over the years developing its present economic value. A balance sheet is a record of investment history, not the economic value.

- Brand and IP Value developed over years of consistent customer experience and word-of-mouth referrals do not appear as assets unless the brand was externally acquired; internally generated brands are not capitalised under AASB 138.

- And 96 per cent of customer relationships, which renew automatically year on year, are worth more than the historical cost of sales and marketing that acquired them. Yet, economic value is nowhere to be found in the financial statements.

- Strength of Business Moat – the competitive barriers that deter new entrants from eroding the business’s market position – creates long-lasting earnings power, which is inherently forward-looking and cannot be captured in a cost-based accounting framework.

What buyers are actually underwriting when they pay a premium

When a buyer purchases a business at a multiple greater than the net value of its tangible assets, the buyer is making a particular bet: that the Future Earnings Potential the buyer is acquiring is large enough, durable enough, and defensible enough to justify the premium. Enterprise Value Drivers – the specific characteristics of the business that make that bet more or less plausible- are the key determinants of the multiple applied and the confidence of the buyer that they can achieve their return. Buyers who are unable to determine specifically what makes the earnings durable will use a conservative multiple. Purchasers who can confirm endurance through brand information, customer retention data, competitive stance analysis, etc., will pay more.

3. The Key Sources of Off-Balance Sheet Value

Growth Potential Valuation: paying for tomorrow, not just today

The evaluation of the Growth Potential Valuation, the income that the business might produce within two to five years, and not the income that the business is currently generating, is one of the most important elements of any premium. A company with a documented, credible growth strategy – as reflected in pipeline data, product roadmap, market expansion opportunities, or a demonstrated ability to grow revenue faster than its industry – attracts a higher multiple than one with the same current earnings and no stated growth thesis. The growth premium is simply the capitalisation of the future EBITDA gain the buyer believes is attainable.

- Future Earnings Potential is not priced based on the earnings base, but on the normalised EBITDA. The same normalised EBITDA attracts a 4x multiple for a business that is not growing, and a 7x multiple for one that has demonstrated a growth trajectory and a plausible forward pathway.

- The most defensible type of growth premium is the Strategic Advantage Value – the particular capability, market position or customer relationship that gives the business access to growth opportunities that competitors cannot easily replicate.

Market Position Strength and the Competitive Moat

Market Position Strength indicates how difficult it would be for a competitor to cause the business to lose its current position. Businesses that have truly defensible positions, through brand loyalty, switching costs, regulatory barriers, network effects, or proprietary data, have a Business Moat Strength premium, which is independent of the premium on the quality of current earnings. Although current earnings may be modest, a robust moat indicates that current earnings will increase and continue to do so without the defensive investment that a weaker market position would necessitate.

Off-Balance Sheet Value Source | How Buyers Assess It | Multiple Premium Effect | Evidence Required |

Brand and IP Value | NPS, pricing premium over unbranded alternatives, unprompted awareness research, cost of customer acquisition relative to sector | 0.5–1.5x depending on strength and transferability | Independent brand research; IP registration records; documented pricing premium data |

Growth Potential Valuation | Revenue growth trend over 3 years; pipeline documentation; product roadmap; market size and share data; documented growth initiatives | 0.5–2.0x depending on the credibility of the growth narrative and the evidence supporting it | At least 12 months of demonstrated growth; documented pipeline; market size data from independent sources |

Market Position Strength / Business Moat Strength | Customer concentration and tenure; switching costs; regulatory barriers; network effects; technology differentiation; competitor analysis | 0.25–1.0x for documented moat characteristics that reduce post-acquisition competitive risk | Customer retention data; competitor landscape analysis; documented switching cost mechanisms; regulatory licence evidence |

Non-Financial Value Factors: management depth and team quality | Evidence that the business operates independently of the founder; key employee tenure and succession; management reporting quality; documented succession plan | 0.5–1.5x: key-person risk is the most common multiple suppressor in owner-operated businesses | CRM evidence of distributed relationship management; management reporting showing team-driven KPIs; employment contracts and retention plans |

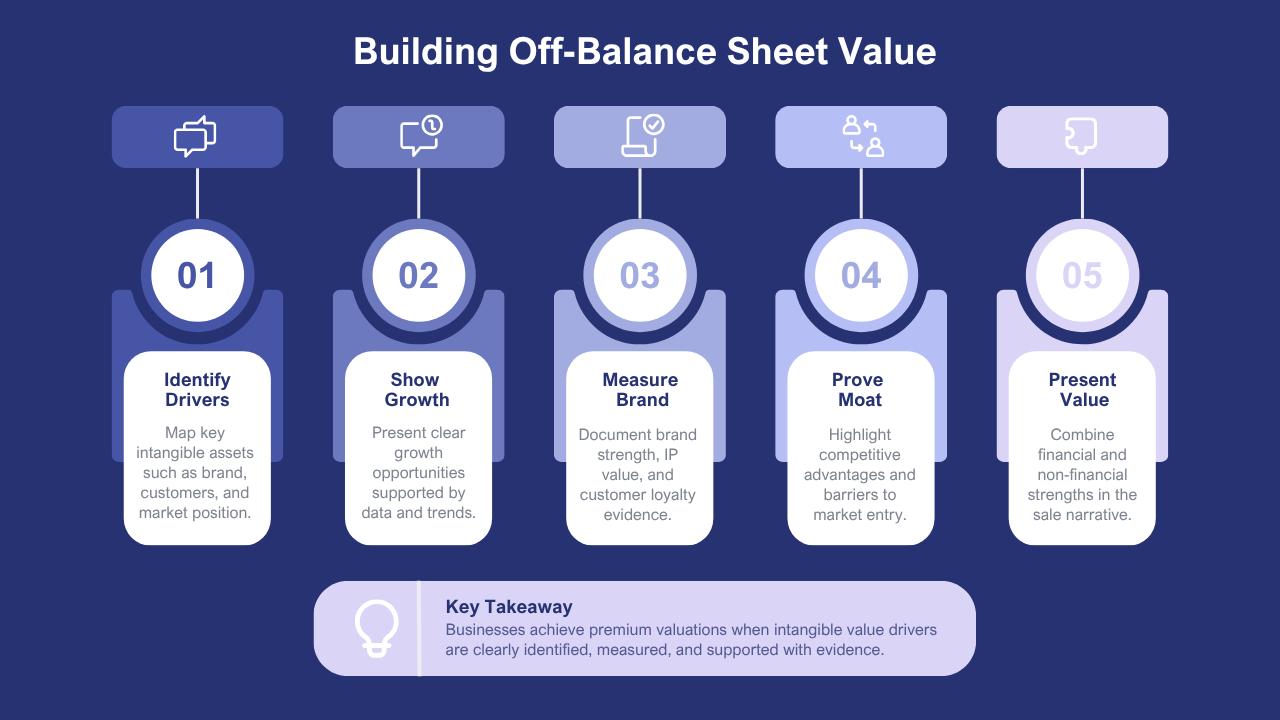

4. Five Steps to Surface and Evidence Off-Balance Sheet Value

Off-Balance Sheet Value is found in most businesses, but only monetised in a transaction when it is identified, documented and presented in a way that buyers can verify on their own. The following five steps are those experienced advisors use to help sellers transform Intangible Value Drivers into demonstrable, buyer-facing evidence.

Step | What It Involves | Value It Unlocks | Common Gap |

1. Map all Intangible Value Drivers | Systematically identify every non-financial value driver in the business: brand equity, customer loyalty, IP, management depth, competitive positioning, data assets, proprietary processes | Creates the complete picture of Off-Balance Sheet Value before any buyer sees the business; prevents material value from being overlooked | Sellers focus only on the obvious intangibles (registered IP, brand) and miss the less visible ones (customer retention patterns, operational moat characteristics) |

2. Quantify Growth Potential Valuation | Document the specific growth initiatives, market opportunities, and capability advantages that support a forward earnings trajectory above the current baseline; prepare a substantiated growth model | Converts an abstract growth story into a specific, evidence-based case for a premium multiple | Growth is asserted as a projection without historical support; buyers discount heavily unless at least 12 months of demonstrated growth trend is visible in the accounts |

3. Measure and document Brand and IP Value | Commission NPS measurement; calculate customer acquisition cost and compare to sector; compile IP registration records; prepare a brand valuation, or at minimum a factual brand evidence pack | Transforms qualitative brand assertions into buyer-verifiable data that anchors the negotiation | Brand value is described narratively without any data; buyers substitute their own conservative assessment, which is almost always lower than the seller’s view |

4. Document Market Position Strength and Business Moat Strength | Prepare a competitive landscape analysis; document the specific switching cost mechanisms, regulatory barriers, or network effects that protect the business’s position; quantify the cost for a competitor to replicate the position | Directly reduces the risk premium buyers apply; a documented moat supports a higher multiple by demonstrating earnings durability | Competitive position is described but not evidenced; buyers assess it conservatively when they cannot independently verify the claims |

5. Present Non-Financial Value Factors alongside the financials | Integrate the documented intangible value analysis into the information memorandum; connect each Enterprise Value Drivers element to a specific commercial outcome; frame the Strategic Advantage Value case for the most likely buyer category | Shapes the buyer’s analytical framework from the outset; buyers who receive a complete picture of both financial and non-financial value are more likely to offer at the top of the valuation range | Non-financial value is mentioned as background context rather than positioned as a primary driver; buyers treat it as unverifiable and apply a generic multiple |

The step that has the most direct influence on whether the work done in steps 1 through 4 converts to a higher offer price is Step 5 – presenting Non-Financial Value Factors and the financials. An information memorandum that conveys only financial information leaves the buyer to form his or her own opinion of the non-financial value, which will usually be more conservative than a seller’s view. An information memorandum that presents the financial data and a specific, evidence-based analysis of Intangible Value Drivers, growth potential, competitive positioning, and the quality of management provides the buyer with a framework that anchors their analysis at a higher level of confidence.

5. Process, Real Cases, and Lessons for Practitioners

The value surfacing workflow

Surfacing Off-Balance Sheet Value is a systematic approach to the process that is undertaken by seasoned advisors to incorporate into the entire sale preparation programme. The workflow below is in four phases that indicate the sequencing of this work and the financial preparation.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Intangible Audit | Evidence Building | Quantification | Narrative Integration |

Map all Intangible Value Drivers; assess transferability of each; identify evidence gaps; prioritise the three to five drivers most likely to affect the multiple in the target buyer category | Commission NPS and brand measurement; compile customer retention cohort data; document competitive positioning; build Growth Potential Valuation case with supporting market data | Apply recognised valuation methods to material intangibles where appropriate; prepare Business Moat Strength analysis; document non-financial value factors with specific commercial outcomes | Integrate Off-Balance Sheet Value analysis into information memorandum; connect Enterprise Value Drivers to specific premium arguments; frame Strategic Advantage Value for the most strategically motivated buyer category |

Case 1: Future Earnings Potential that was invisible without evidence

One media technology company had 3 years of development on a proprietary content distribution platform that reduced the company’s operating expenses by about 35 per cent compared to legacy competitors. This platform was not officially registered as an asset; it just worked, and the staff kept it. When the business was brought to market without any records of the technology, the initial round of buyer offers captured standard multiples in the media sector. The advisor to the seller commissioned an exercise in technical documentation and a cost-to-recreate analysis that determined the platform’s value at about $1.8 million, based on the labour and time needed to rebuild it afresh. A Strategic Advantage Value story was created that linked the platform to the 35 per cent cost advantage and reported on the technology intangibles and operational moat it had created, which supported an offer of about 1.4 million above the average in the first round. The Off-Balance Sheet Value had not existed; it was only a lack of evidence that it had existed.

Case 2: Market Position Strength that changed the buyer category

An independent, niche professional services company had developed a truly dominant position in a given regulatory compliance vertical in 12 years, with approximately 38 per cent market share in its segment. This positioning had never been measured or formally stated – it was just a description of how we are a leader in our marketplace. A formal Market Position Strength analysis, in which the 38 percent share, the 91 percent retention rate, and the cost of a competitor entering the market to develop the same recognition and client relationship from scratch was (estimated to take more than three years and spend over two and a half million dollars to do so) was done, the analysis identified a buyer category which had hitherto been invisible in the original process: sector consolidators who would pay a strategic premium to acquire the dominant position rather than build it. The updated sale process, aimed at this type of buyer, yielded an offer 42 per cent higher than the original financial-buyer offer. The Business Moat Strength was never new; it just had to be translated into the language that the most strategically motivated buyer would pay.

6. Conclusion

A balance sheet is less than the business’s value because a balance sheet was never intended to capture economic value; it was created to reflect historical cost. Off-Balance Sheet Value, in the form of Intangible Value Drivers, Growth Potential Valuation, Market Position Strength, and Business Moat Strength, is the actual driver of premium pricing in most private business transactions.

- The documented and evidenced Enterprise Value Drivers always attract higher multiples than the same drivers that are asserted but not documented and with no supporting evidence -the evidence gap is almost always higher than the underlying value gap.

- Things that are non-financial in the sense that they are presented as non-financial value factors, which must be presented alongside the financial data in such a way that ties each driver to a particular commercial outcome; those buyers who receive such an analysis would be more prone to price the business at the top of the valuation range.

- To owners: now is the time to start naming and documenting Off-Balance Sheet Value; to advisors: the information memorandum that unlocks a premium is the one that tells the complete story – financial and non-financial – with evidence that can be verified independently by the buyer.

Frequently Asked Questions

Q1. What does business value beyond the balance sheet mean?

It refers to valuable business attributes not fully reflected in financial statements, such as brand reputation, intellectual property, customer relationships, and workforce expertise.

Q2. Why are these assets important?

These intangible value drivers often contribute significantly to future earnings, competitive advantage, and overall business value.

Q3. Can these assets influence acquisition pricing?

Yes. Buyers often pay higher prices for businesses with strong intangible assets that support future growth and profitability.

Q4. How can businesses identify value beyond the balance sheet?

Professional valuation helps identify and measure intangible assets that may not be fully recognised in accounting records.

Q5. How does understanding these value drivers benefit business owners?

It enables owners to strengthen key assets, improve business performance, and maximise value before fundraising, mergers, or business sales.

1 thought on “What Makes a Business More Valuable Than Its Balance Sheet?”