Table of Content

1. Introduction: Business Valuation Cost in Australia

When business owners are considering a potential sale, a partnership restructure, or a fundraising event, their first question, almost always, is how much will a valuation cost? But it’s not always straightforward. Valuation Cost Australia is highly variable and depends on the reason for the valuation, the size and complexity of the business being valued, who is providing the valuation and the amount of documentation and formal reporting required. To the uninitiated, the spread of fees can be bewildering – and without a structured guide to the factors influencing value, it’s easy to either overpay for services that provide greater value than needed for the situation or underpay for a report that will not stand up to the scrutiny of a potential buyer, financing institution, or court.

This article is aimed at business owners considering a transaction, early- and mid-career professionals looking to deepen their understanding of the advisory industry, and those new to valuation or M&A who wish to understand the fee structure, the factors driving costs, and the questions to ask before engaging an advisor. Whether you need a formal Certified Valuer Cost report, a desktop review, or a sale-ready valuation, this guide will help you better understand which service you need and what you should expect to pay.

Knowing Business Appraisal Fees is not a matter of budgeting. It is a strategic one. Value is created by how much is spent on a quality valuation, and when. Business owners who invest in a reputable valuer early in the process, with a well-defined brief and enough time to do the job, tend to fare better than those who engage a valuer solely as a compliance exercise. For advisors, being able to explain to clients what they are paying for, and why, is one of the most obvious examples of value.

2. Why Valuation Fees Vary So Much

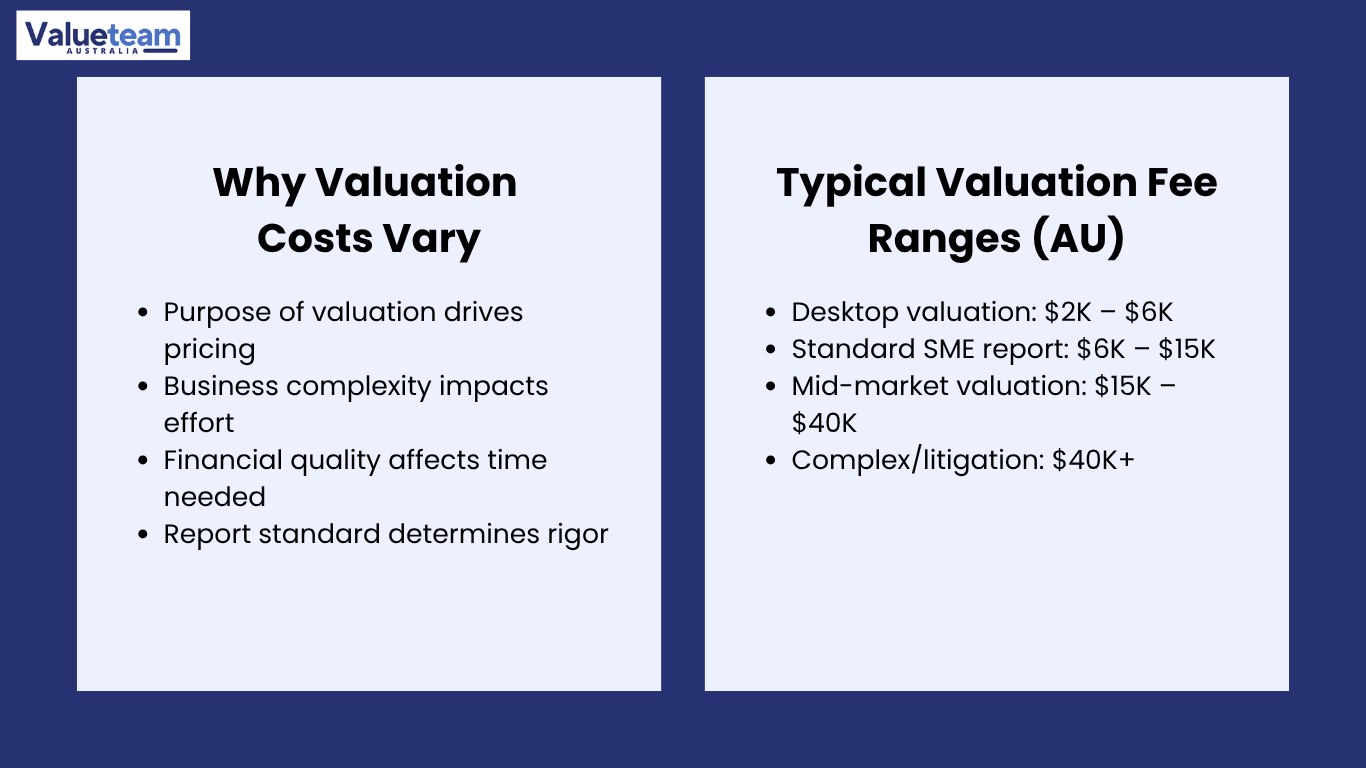

Business Appraisal Fees in Australia are highly variable. A desktop valuation of a sole proprietorship could cost just a few thousand dollars. Proper (litigation-level) valuations of a multi-entity business with disputed goodwill and multiple jurisdictions can cost tens of thousands of dollars. The bulk of SME transactions fall somewhere in between, where the fee is usually determined by the complexity of the financials, the purpose and audience of the report, the independence and credentialing of the Valuer, and the time required to normalise the financials and develop a defensible methodology.

The purpose of the report is a key factor in Valuation Report Pricing. A report prepared for a trade sale – where it will be reviewed by highly professional buy-side due diligence professionals – demands a level of care, disclosures, and support for assumptions beyond that required for a report prepared for an internal planning exercise. Likewise, valuations carried out for dispute resolution, family law, or ASIC purposes require a higher level of evidentiary rigour, which takes time (and therefore costs) to achieve. What type of report you need is the first question you should ask any provider, and it is a critical element in assessing whether a fee is reasonable.

The second factor is complexity. A company with audited accounts, a single operating entity, a simple revenue stream and no related party transactions is significantly easier (and therefore cheaper) to value than a company with multiple entities, intercompany charges, owner-managed expenses and a complex mix of revenues that must be painstakingly separated. The Cost of Valuation Services increases in direct proportion to the time a valuer must spend converting the financial records into a form suitable for valuation. Businesses that take the time to keep their accounts well-documented and organised before seeking a valuation consistently save time (and therefore money) with a valuer.

3. Valuation Cost Ranges by Engagement Type

Although every engagement is unique, the Australian market has developed quite similar Valuation Pricing Guide levels by engagement and business size. The table below provides an approximate guide for business owners and advisors on the range of costs for the most common valuation engagements.

Engagement Type | Typical Fee Range (AUD) | What Is Included | Best Suited For |

Desktop / Indicative Opinion | $2,000 – $6,000 | High-level multiple-based estimate; limited documentation; no formal report | Internal planning, early-stage sale preparation, ballpark benchmarking |

SME Valuation Fees — Standard Report | $6,000 – $15,000 | Normalised financials; methodology documentation; EBITDA and DCF analysis; formal written report | Trade sales of businesses with EBITDA under $2M; bank lending; minority buyouts |

Mid-Market Formal Valuation | $15,000 – $40,000 | Full financial reconstruction; multiple methodologies; market comparable benchmarking; independent sign-off | Businesses with EBITDA $2M–$10M; PE transactions; partnership disputes; litigation support |

Complex / Litigation-Grade | $40,000 – $100,000+ | Expert witness standard; cross-entity analysis; detailed sensitivity modelling; legal-ready documentation | Disputed transactions, family law, ASIC proceedings, complex group structures |

Certified Valuer Cost — Stamp Duty / Tax | $3,500 – $12,000 | ATO or OSR-compliant methodology; registered valuer sign-off; formal asset-by-asset assessment | Property-in-specie transfers, CGT events, R&D tax asset valuations |

The ranges reflect the Australian market as a whole (metropolitan and regional). Big Four and major firms tend to work at the top end of each range, due to their branding, resources, and the compliance significance of their opinions in material transactions. Specialist and boutique valuation firms, many with the same qualifications and adopting similar techniques, often offer similar value at a lower cost, especially in the SME market. This information is valuable for business owners and their advisors seeking to optimise their cost position while maintaining credibility.

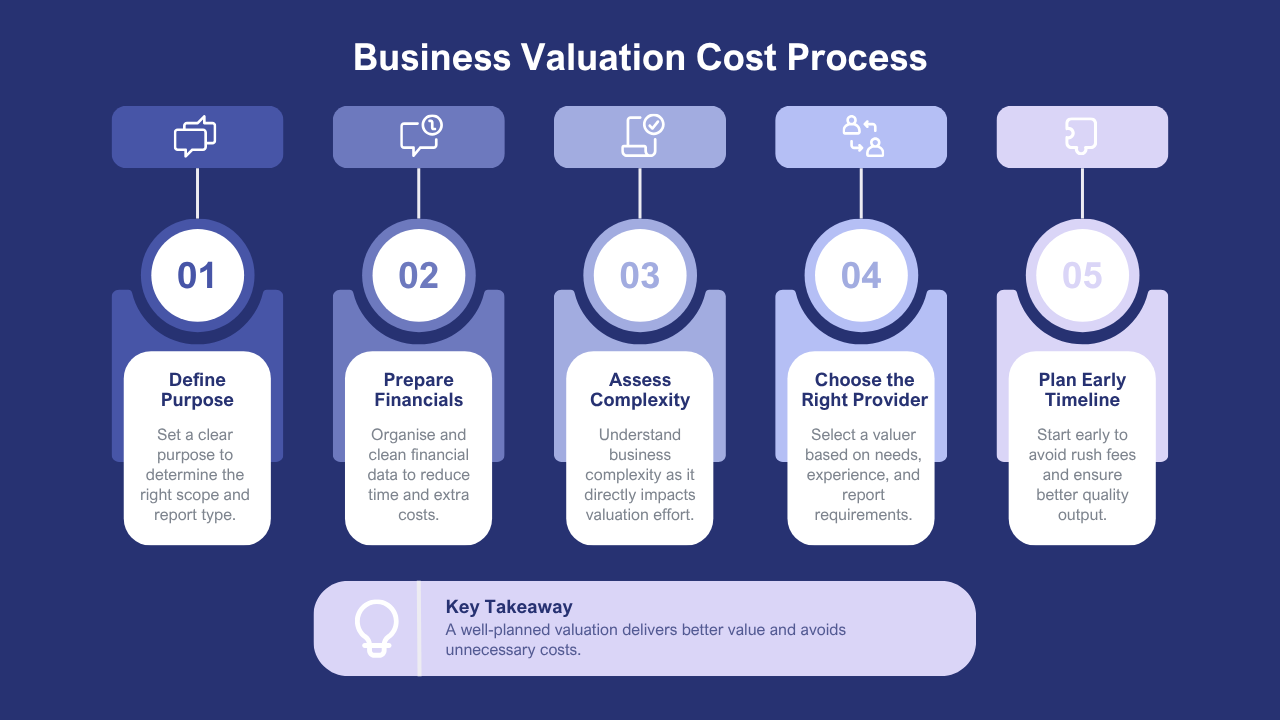

4. Five Factors That Drive Valuation Cost

Five Valuation Cost Factors determine a particular engagement’s position within the applicable fee range, regardless of engagement type or provider type. Knowing a little about each before seeking a quote helps business owners and their advisors to have a more meaningful discussion with potential providers – and to take action to minimise cost without compromising quality.

Valuation Cost Factors | Why It Drives Fee | How to Manage It |

Financial record quality | Disorganised or inconsistent accounts require significant reconstruction before any methodology can be applied, adding hours to the engagement | Engage a bookkeeper or accountant to clean and reconcile three years of accounts before briefing a valuer |

Number of entities and structures | Each additional entity requires separate analysis; intercompany eliminations and trust distributions add significant complexity | Rationalise group structures before a transaction if possible; document intercompany arrangements clearly |

Purpose and report standard | Litigation-grade and tax-compliant reports require additional methodology disclosure, assumption documentation, and formal sign-off | Be clear with the provider about the intended use of the report from day one; avoid scope creep mid-engagement |

Engagement timeline | Rush engagements command a premium; valuers who compress a two-week process into five days typically charge 20–40% more | Engage a valuer 8–12 weeks before you need the report; earlier where the business is complex |

Sector and comparables availability | Niche sectors with limited Market Comparables require more methodological work; sectors with thin transaction data require proxy analysis and additional justification. | Brief the provider on the industry context upfront; share any sector data or recent comparable transactions you are aware of |

The most easily managed cost factor for a business owner is the state of their accounts. Valuers are paid for time, and the time required to put together a jigsaw puzzle of unrepresentative accounts – reconciling management accounts to tax returns, separating owner expenses from operating expenses, documenting owner expenses as add-backs – is time that could be better spent, and will cost the client money. Companies that present to a valuation engagement with three years of reviewed financial accounts, a schedule of owner add-backs and management accounts will always get quicker and cheaper valuations than those who present a file of figures and say “make it make sense”. This is a simple, effective action every business owner can take in the lead-up to a transaction.

5. Choosing the Right Provider for Your Situation

A range of providers with different price structures, credentialing policies, and typical applications serve Australia’s Financial Advisory Fees market. Key take-outs from this are that business owners and their advisors can identify the most suitable provider for their particular circumstances, rather than relying on the most well-known brand name or the lowest fee quoted, which may not be the best choice in all circumstances.

Business brokers sometimes offer indicative valuations as an adjunct to their preparation service. Such valuations are usually part of the engagement fee or very cheap and serve as a point of reference for sellers entering a sales process. But these valuations are typically not appropriate for anything other than internal use: they are rarely subject to peer review, do not include methodology reports, and will not withstand the scrutiny of an experienced buyer or a due diligence professional. In any circumstance where the Valuation Report Pricing must incorporate defensible methodology and sign-off by an independent party – such as trade sales of a certain scale, bank finance, dispute settlement and taxation compliance – an independent valuer is needed.

The most typical vendor of formal SME Valuation Fees services in Australia is a chartered accountant with a CVA (Certified Valuing Accountant) qualification or equivalent CPD in business valuations. Mid-sized accounting firms often have specialist valuation practices which provide a good balance between financial understanding, professional qualifications and value for money in the $500K to $5M EBITDA range. Corporate advisors and investment banks typically service above this range and provide additional services (and costs) such as market positioning and transaction management, in addition to valuation. Getting the right match to the true needs of the engagement, rather than the brand-name, is always the most cost-effective solution.

6. Process, Challenges, and What the Market Teaches You

For those within and entering the advisory and valuation sector, it is just as important to understand the process and challenges of a typical valuation engagement as it is to understand the fees. The four-phase flow chart below shows how a typical formal Business Worth Assessment Cost engagement progresses from briefing to report, along with the challenges along the way.

Phase 1 | Phase 2 | Phase 3 | Phase 4 |

Scoping & Briefing | Financial Reconstruction | Methodology & Modelling | Report & Review |

Define purpose, report standard, and timeline; agree on fee and engagement terms; collect three years of financial statements and preliminary business overview | Normalise EBITDA; identify and document add-backs; analyse working capital, revenue quality, and balance sheet; flag information gaps for follow-up | Select and apply valuation methods; benchmark against Market Comparables; run sensitivity analysis; draft methodology rationale and assumption support | Draft formal Valuation Report Pricing deliverable; internal quality review; client discussion of findings; finalise and issue signed report |

Most cost misalignments start in Phase 1. When the brief is not clear enough about the report’s purpose, audience, and required reporting standards, it creates scope uncertainty that drives either cost blowouts or a report that doesn’t address the client’s needs. The most common example is a business owner who asks for a valuation report for a trade sale but does not disclose that the buyer has already said they will have a formal quality-of-earnings analysis performed. This factor changes the range and detail of documentation required in the vendor’s report to ensure that it is credible during the sale process. The advice and practice of taking the time to have a proper scoping discussion at Phase 1 helps avoid frustration and cost blowouts later.

Phase 2 – financial reconstruction – is the most variable in terms of time required, according to valuers. Business Appraisal Fees are quoted at the beginning of an engagement, and are based on an assumed quality of financial records. If this assumption is too optimistic – if records are not consistent from one year to the next, if management accounts do not tie to tax returns, if related-party transactions are not well documented – the time required to complete the work can be substantially greater than the original estimate. Business owners who have not allocated time to prepare their financial records for the appraisal briefing should factor in that this phase of the process will take longer (and cost more) than originally estimated.

Phase 4 – report and review – is where the importance of working with a specialist who has a deep understanding of the industry becomes clear. A valuation report that shows an understanding of the target’s industry setting, uses up-to-date and relevant Market Comparables, and uses a methodology that the target’s prospective buyers will understand and appreciate is a much more valuable product than one that is technically accurate but devoid of any specific industry context. This is a key lesson for junior analysts: the value of a valuation can’t be judged just by the financial model. It is also measured by how effectively the report translates the technical aspects of the analysis into a narrative that resonates with its target audience.

7. Real Cases and What They Reveal

One of the common issues in the Australian advisory market involves business owners who engage a desktop report as part of a preparation-for-sale process at a relatively low cost, only for the report to fall short when dealing with real buyers and their advisors. For example, take a trade company with a normalised EBITDA of around $1.2 million that has received an indicative opinion from its broker for a fee of $3,500. When a bid was received from a private equity-backed buyer, and the buyer’s advisors examined the vendor’s valuation reports, the desktop opinion was essentially ignored. The buyer’s advisors undertook an Earnings Quality Assessment from scratch. They concluded that the normalised EBITDA was approximately 18 per cent lower than the broker’s, due to undocumented add-backs and a revenue timing adjustment. The vendor ultimately retained an independent qualified valuer at the Certified Valuer Cost of $11,000 to prepare a formal report with a supported methodology – the cost of which could have been avoided by getting it right the first time.

Another case demonstrates the value of a timely investment. A professional services firm in the process of a management buyout engaged a mid-market accounting firm to conduct a formal valuation 12 months ahead of its planned buyout. The SME Valuation Fees were $13,500. The engagement highlighted a problem – a lack of separation between a single service line with a disproportionate share of revenues and the overall practice in the management accounts – that the vendor was able to resolve with a twelve-month revenue diversification program before the buyout negotiations began. The valuation at the time of the actual buyout was $9,000, which reflected the restructured financials. The two Valuation Cost Australia for the above engagements was $22,500. Still, the buyout price was about $380,000 more than the pre-diversification valuation – a return on investment for an advisor that didn’t need much calculating.

8. Conclusion: Actionable Insights

There is no one cost for a business valuation in Australia, and the advice to think of it that way will lead to either paying too much for a more complex assignment than is needed or paying too little for a report that doesn’t achieve its objective. Knowing the Valuation Cost Factors that impact fees – financial reporting quality, business complexity, purpose of the report, timeframe and availability of comparable data for an industry – allows business owners and their professional advisors to make informed choices of what is required, who to engage to provide it and how much it should cost.

For business owners who anticipate a future sale or restructuring, the most practical takeaway from this guide is about timing. Taking the time to engage a qualified independent valuer 12 to 18 months before a planned sale or restructure, rather than weeks before a sale, allows time to address issues that impact value, eliminates the time pressure that increases the Business Appraisal Fees and results in a report that is a true reflection of the business and its value, rather than its condition when the clock starts to tick. The Valuation Pricing Guide ranges highlighted here are not expenses to be avoided, but rather investments to be managed and planned.

For younger professionals working in the advisory or valuation markets, the real need is to develop an understanding of the whole range of engagement types and Cost of Valuation Services – not just the report writing end of the market. Knowing why a desktop opinion costs what it does, when it is and is not suitable, and how the market segments providers and credentialing is key to providing quality advice to clients. The business owners who get the best result are those whose advisors have encouraged them to pay for the right Financial Advisory Fees engagement and at the right time – and who have understood the difference between cost and value long before the sale pressure commenced.

Frequently Asked Questions

Q1. How much does a business valuation cost in Australia?

The cost of a business valuation varies depending on the company’s size, complexity, purpose of valuation, industry, and the level of analysis required.

Q2. What factors affect the cost of a valuation?

Valuation costs are influenced by financial complexity, business structure, available information, reporting requirements, and the scope of professional work involved.

Q3. Why should businesses invest in a professional valuation?

A professional valuation provides an objective assessment that supports business sales, acquisitions, financial reporting, taxation, and strategic decision-making.

Q4. Who typically requires business valuation services?

Business owners, investors, accountants, legal professionals, financial institutions, and corporate finance teams frequently require valuation reports.

Q5. How can businesses prepare for a valuation?

Maintaining organised financial records, accurate forecasts, and supporting business information helps streamline the valuation process and improve reporting quality.

1 thought on “How Much Does a Business Valuation Cost in Australia? A Complete 2026 Guide”